***This is an excerpt from a Long Pull Report sent to Collective members on September 11 outlining our bullish precious metals thesis we’ve been pounding the table for over a year. Enrollment to our Collective runs till Sunday. If you’d like to join, click the link below and get after it. Don’t hesitate to shoot me any Qs!**

We have a lot to cover in the precious metals space this week. M&A markets are heating up, the metals keep trading higher, and junior mining developers/producers continue underperforming.

This week, we explore the latest PM mining deals to see what prices the majors will pay for Tier-1 assets.

We explain how to interpret these deals to arrive at a quick per-ounce relative price paid, which we can then use to compare other deposits/projects.

Finally, I share my Mining Stock Journal spreadsheet to track junior miners’ relative valuations and prospects easily.

Alright, let’s get after it.

Drilling vs. Acquisition: Which Way, Miner Man?

The precious metals M&A market is heating up … fast.

Gold Fields acquired Osisko Mining for $1.57B last month. First Majestic (AG) bought Gatos Silver (GATO) for $970M last week. And this week, AngloGold Ashanti (AU) bought Centamin for $2.5B.

Here’s why this is important.

The large gold/silver miners know they can’t grow reserve/resource ounces fast enough organically. It’s too expensive, takes too long, and involves miles of government and social red tape.

So what do they do? They buy other producers and developers with Tier-1 deposits that they can bolt into their existing operations.

These smaller companies have already done all the permitting, social licensing, and drilling to confirm the resources. All that’s left is to mine.

I’ve spent the past year listening to mining company earnings presentations. I hear two common phrases: “It’s cheaper to buy ounces in the ground than drill for them” and “Even if we drill a great hole, the market doesn’t care, and our stock will trade lower on the news.”

There’s little incentive to drill in this environment.

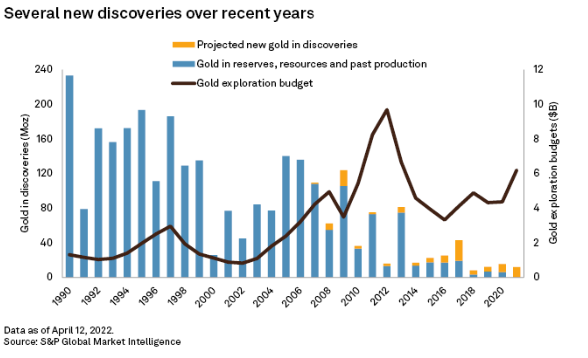

But it’s more than that. As my friend Alberto Alvarez tweeted two weeks ago, we’re not finding much gold anymore.

The below graph shows gold discoveries over time.

Gold exploration budgets peaked in 2012 with nothing to show for it.

Like copper, all the easy gold has been mined/discovered. What’s left is low-grade and deep underground, which shifts the cost curve higher.

From 1970 to 1990, the gold industry found at least one 50Moz deposit and at least ten 30M+ deposits. Yet since 2000, the industry has yet to find one 50Moz deposit.

So, drilling is expensive, time-consuming, and politically/socially risky, and you’re also fighting a trend of declining discoveries.

Capital isn’t the problem now. At current gold prices, producers are generating significant free cash flow.

Suppose you’re the CEO of a major gold producer. Which path would you take to expand your reserves? You’d save the headache and buy ounces from junior developers.

This brings us to an important question: how much should you pay for ounces?

Analyzing The Latest Precious Metals M&A Transactions

Producers use a few key variables to value an acquisition target, namely:

- Jurisdiction

- Resource/reserve size

- Mine type (open pit/underground)

- Expected mine life

- Margins (AISCs, grade, etc.)

All the factors we covered in our 80/20 Mining Stock Analysis Primer.

The better the jurisdiction, the bigger the resource, the lower the cost of the mine, and the longer the mine life, the higher the price a producer is willing to pay for that asset.

Deal 1: Gold Fields Buys Osisko Mining

Gold Fields paid $1.6B for Osisko Mining. The acquisition gave Gold Fields 100% ownership of the Windfall Project, one of the highest-grade gold deposits (8g/t) globally in a Tier-1 district (Abitibi region of Quebec).

According to Osisko’s 2022 Feasibility Study, the Windfall Project would produce 300,000oz of gold annually for an initial mine life of 10 years. The deposit also has 5.15Moz of Indicated & Inferred resources.

So, to recap … Gold Fields bought a Tier-1 jurisdiction asset with world-class grades, low costs (<$900/oz AISC), and a significant resource with at least a 10YR mine life.

We can value this transaction in two ways: price paid per life-of-mine (LOM) production ounces and price paid per resource ounces.

- Price paid per LOM ounces: $533/oz (300Koz * 10YR = 3Moz / $1.6B)

- Price paid per total resource ounces: $311/oz (1.21Moz of indicated + 3.94Moz of inferred / $1.6B)

In other words, Gold Fields paid an average of $422/oz for Osisko Mining’s gold resources.

Deal 2: First Majestic Buys Gatos Silver

First Majestic (AG) paid $970M to acquire Gatos Silver (GATO), consolidating three world-class silver assets under one company.

The GATO acquisition will immediately add 9Moz of silver-equivalent (AgEq) production and contribute $70M in annual free cash flow (13.9x multiple).

There are three ways to value this acquisition besides the above FCF multiple.

- Price per ounce of total LOM production

GATO’s 2023 LOM plan has an original mine life of 7.5 years, which gives us 49.5Moz over the life of the mine. $970M / 49.5Moz = $19.60/oz.

- Price per ounce of average annual production

GATO will produce 6.6Moz of silver annually. $970M / 6.6Moz = $147/oz

- Multiple of Annual Production

We can also consider valuation as the price paid as a multiple of annual production value (i.e., the commodity’s price multiplied by annual production ounces).

So for GATO, that’s $970M / (6.6Moz * $28) or $970M / $185M = 5.24x

Using English, AG paid 5.24 years’ annual silver production at $28/oz for GATO.

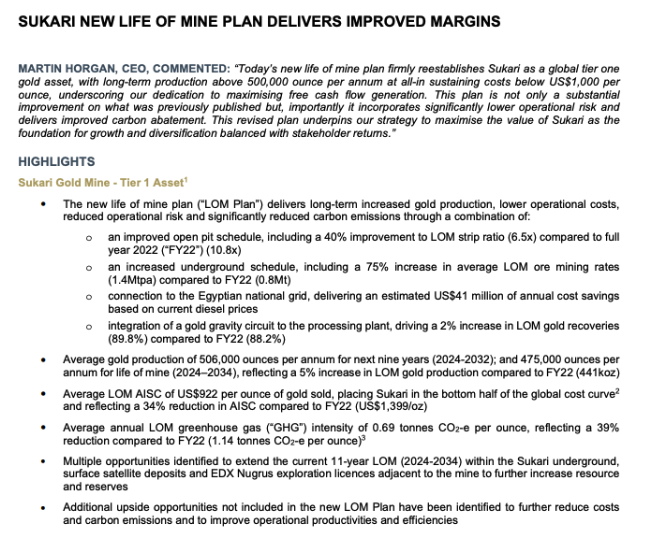

Deal 3: AngloGold Ashanti Buys Centamin

AngloGold (AU) paid $2.5B to acquire Centamin (CEE) and its flagship Sukari gold mine in Egypt.

Sukari is one of the largest gold mines globally, producing 5.9Moz of gold cumulatively since 2009.

Let’s review our mining M&A checklist to see why AngloGold bought Suakri.

- Jurisdiction: Africa (mining-friendly and low-cost)

- Resource: 8.3Moz resource base

- Annual production: Sukari has an average annual production estimate of 485,000-500,000oz

- Mine Life: 11 years

This is a great asset.

Let’s examine our valuation methods.

- FCF Multiple Method

According to the acquisition press release, the Sukari mine generated $78M in FCF during the first two months of Q3 2024. This is a rough estimate, but that’s $458M in annualized FCF or 5.5x.

- Price Paid Per LOM Production Ounces

Sukari should produce ~500 Koz/year over its 11YR mine life for 5.5Moz in LOM production. $2.5B / 5.5Moz = $449/oz

- Price Paid Per Total Resource Ounces

CEE has a total of 8.3Moz in gold resources. $2.5B / 8.3Moz = $301/oz.

AngloGold paid, on average, $375/oz for CEE and its Sukari gold mine. Remember, Gold Fields paid an average of $422/oz for its gold acquisition.

What Does This All Mean?

Gold producers are paying premiums for high-quality deposits and projects. This makes sense because it’s cheaper to buy ounces than drill, and producers are making record-level profits at current gold prices.

What if $300-$500/oz is the new floor? How cheap are some of these junior developers and producers in that pricing environment?? This is how you get a massive bull market in junior mining.

Eventually, the majors capitulate and pay up for ounces to replenish reserves. This drives more capital into the industry, further expanding prices and valuations, and gives majors yet another avenue to acquire companies via all-stock transactions.

These deals above are just the tip of the iceberg.

Major producers don’t buy for next quarter or next year’s earnings potential. They see the 5-10YR outlook … the big picture … and they’re telling you that gold prices will be much higher then than they are now.

The good news is that we know their investment criteria from reverse-engineering these latest deals.

Sharing My Junior Mining Stock Investment Journal

I created an Excel spreadsheet “journal” to track every junior mining stock I research, which you can find here.

My goal is to add as many high-quality mining stock ideas as possible. This will allow us to quickly identify the cheapest ideas in the best jurisdictions with the lowest costs and highest grades.

There are four main tabs:

- NPV, IRR, and Capex: Calculates NPV-to-Market Cap, NPV-to-Capex, project IRRs, and initial mine life assumptions

- Resource Valuations: Measures a company’s total resources and provides Market Cap (MC)/Resource Valuation

- FCF Analysis: Basic FCF multiple estimates based on current metals prices, AISC estimates, and annual production

- Quality Scorecard: Ranks qualitative/quantitative aspects of a company to provide an “attractiveness” percentage out of 100%

Conclusion: We Know The Criteria … We Just Gotta Find ‘Em

I’m giving you the tools to find and invest in the next great junior mining play. Last week, I shared my Perplexity Collection models to quickly assess and value any junior mining company.

This week, I shared how I analyze a mining M&A deal from qualitative factors to quantitative measurements.

We are at the beginning of what could be a decade-long precious metals bull market. And 99% of generalist investors have no idea how to operate in that environment.

But you do. So, let’s get after it.

If you enjoyed this piece and want to learn more about our trading philosophy and community of the internet’s most ambitious investors/traders, consider joining The Collective.