Musings: The Illusion of the Great Moderation and an Update on Shipping

Alex here with your latest Friday Macro Musings. As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.Latest Articles — Your Monday Dirty Dozen [CHART PACK] — We look at the widening gap between the positive hard data and the horrendous soft data, we check in on global central bankers to see what they’re up to, take a look at earnings season and where the beats and misses are trending and more.Value Hive: Investor Letters, Options Trader Wins Big and More! — This edition is LOADED with investor letters as we clear the deck for one of our favorites: Scott Miller. We’ll touch on some other things, such as a trader turning $700 into $100K+. Artko Capital continues to kill it. And Howard Marks discusses negative rates.Articles I’m reading — If you’re looking for a good laugh then give Matt Levine’s latest on the WeWork/Softbank circus titled “How Do You Like We Now” a read (link here).Daniel Want of Prerequisite Capital shared his latest quarterly letter. I enjoy Daniel’s letters, the guy has good taste in books and always finds a way to weave in interesting quotes and excerpts into his writing. Here’s the link along with an excerpt he shared from Garet Garret’s terrific book “A Bubble That Broke the World”, published in 1932.

“The general shape of the universal delusion may be indicated by three of its familiar features.

-

-

- First, the idea that the panacea for debt is credit.

- Second, a social and political doctrine, now widely accepted, beginning with the premise that people are entitled to certain betterments of life.

- Third, the argument that prosperity is a product of credit, whereas from the beginning of economic thought it had been supposed that prosperity was from the increase and exchange of wealth, and credit was its product.

-

Result: Much more debt. A world‐wide collapse of foreign trade, by far the worst since the beginning of the modern epoch. Utter prostration of the statistical serpents. Credit representing many hundreds of millions of labor days locked up in idle industrial equipment both here and in Europe. It is idle because people cannot afford to buy its product at prices which will enable industry to pay interest on its debt. One country might forget its debt, set its equipment free, and flood the markets of the world with cheap goods, and by this offense kill off a lot of competition. But if this thought occurs to all of them, and so all with one impulse, raise very high tariff barriers against one another’s goods, to keep them out.”

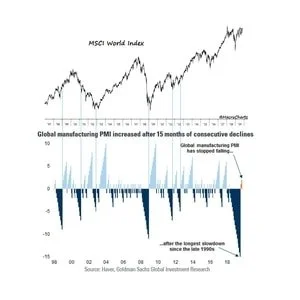

I’ve been meaning to write an update on shipping but then I saw Kuppy’s latest I figured he did a better job than I could so why bother, I’ll just share his instead (link here). The important takeaway is “operating leverage”. Charter rates have been going through the roof — a VLCC recently chartered for $300k a day — while operating costs stay the exact same. This means that the rising higher margined revenue passes directly through to shareholders; one reason why bull markets in shipping can get as wild as they do.Lastly, Srinivas Thiruvadanthai of The Levy Forecasting Center, published this excellent paper calling out the problems with inflation targeting and our over-reliance on monetary policy to boost aggregate demand.Srinivas points out that “The mechanisms by which monetary policy works to stimulate demand inevitably leads to rising private sector debt ratios and a tendency toward asset price bubbles” and “The stability created by the so-called Great Moderation in reality was an illusion, and it compromised the resilience of the financial system.” He goes onto make the case that we need a total rethink of our economic policy framework, one that emphasises fiscal policy and not just leverage induced demand.I agree on all points. Unfortunately, I don’t think we’ll see any significant changes until we use up the very last bit of our monetary policy (balance sheet expanding) juice.Charts I’m looking at—@MacroCharts shared this great chart on the twitters this week. The Global PMI is back in the green after it’s longest slowdown since the 90s. Podcast I’m listening to — A few weeks ago I shared the research piece titled “Bubble or Nothing” that was put out by the Jerome Levy Forecasting Center. It was an excellent paper and is essential reading if you’re trying to understand the increasingly binary macro environment we’re in, and a fragile binary one at that. This week Bloomberg’s Oddlots podcasts had on David Levy, one of the coauthors, to discuss how the economy works in a world of oversized balance sheets and leveraged risk taking. It’s a good listen. Here’s the link.Trade I’m considering — Not a trade, though there’s certainly trades to be made off this broader trend, but a number of markets are breaking out globally. This is important for a few reasons (1) it means that markets are looking past the current manufacturing recession and betting on a coming recovery (2) the strongest bull trends happen when markets around the world push higher in unison and (3) capital has become incredibly concentrated in the US due to chasing of US relative outperformance. This trend has flipped since August and if it continues it can become self-fulfilling as capital outflows drive USD lower, making RoW more attractive, leading to greater RoW outperformance and more capital outflows from the US etc...

Podcast I’m listening to — A few weeks ago I shared the research piece titled “Bubble or Nothing” that was put out by the Jerome Levy Forecasting Center. It was an excellent paper and is essential reading if you’re trying to understand the increasingly binary macro environment we’re in, and a fragile binary one at that. This week Bloomberg’s Oddlots podcasts had on David Levy, one of the coauthors, to discuss how the economy works in a world of oversized balance sheets and leveraged risk taking. It’s a good listen. Here’s the link.Trade I’m considering — Not a trade, though there’s certainly trades to be made off this broader trend, but a number of markets are breaking out globally. This is important for a few reasons (1) it means that markets are looking past the current manufacturing recession and betting on a coming recovery (2) the strongest bull trends happen when markets around the world push higher in unison and (3) capital has become incredibly concentrated in the US due to chasing of US relative outperformance. This trend has flipped since August and if it continues it can become self-fulfilling as capital outflows drive USD lower, making RoW more attractive, leading to greater RoW outperformance and more capital outflows from the US etc... Quote I’m pondering —

Quote I’m pondering —

“Victory smiles upon those who anticipate the changes in the character of war, not upon those who wait to adapt themselves after they occur.” …General Giulio Douhet (1869-1930)

Anticipate, anticipate, anticipate…If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.Have a great weekend.