My wife’s brother almost died last October because he wasn’t wearing a helmet.

He suffered severe brain bleeding and eye nerve damage.

For months the only thing he could do was lie in bed alone. No sounds or external stimuli. He couldn’t read a book or listen to music.

Just watching him made me depressed.

The sad part was all (or most) of that injury could’ve been avoided had he worn a helmet.

This is why this week’s Idea Note hits close to home.

I’m talking about MIPS AB (or MIPS). MIPS protects the brain from head injuries by making helmets safer. They insert a patent-protected device that allows the brain to rotate within the helmet.

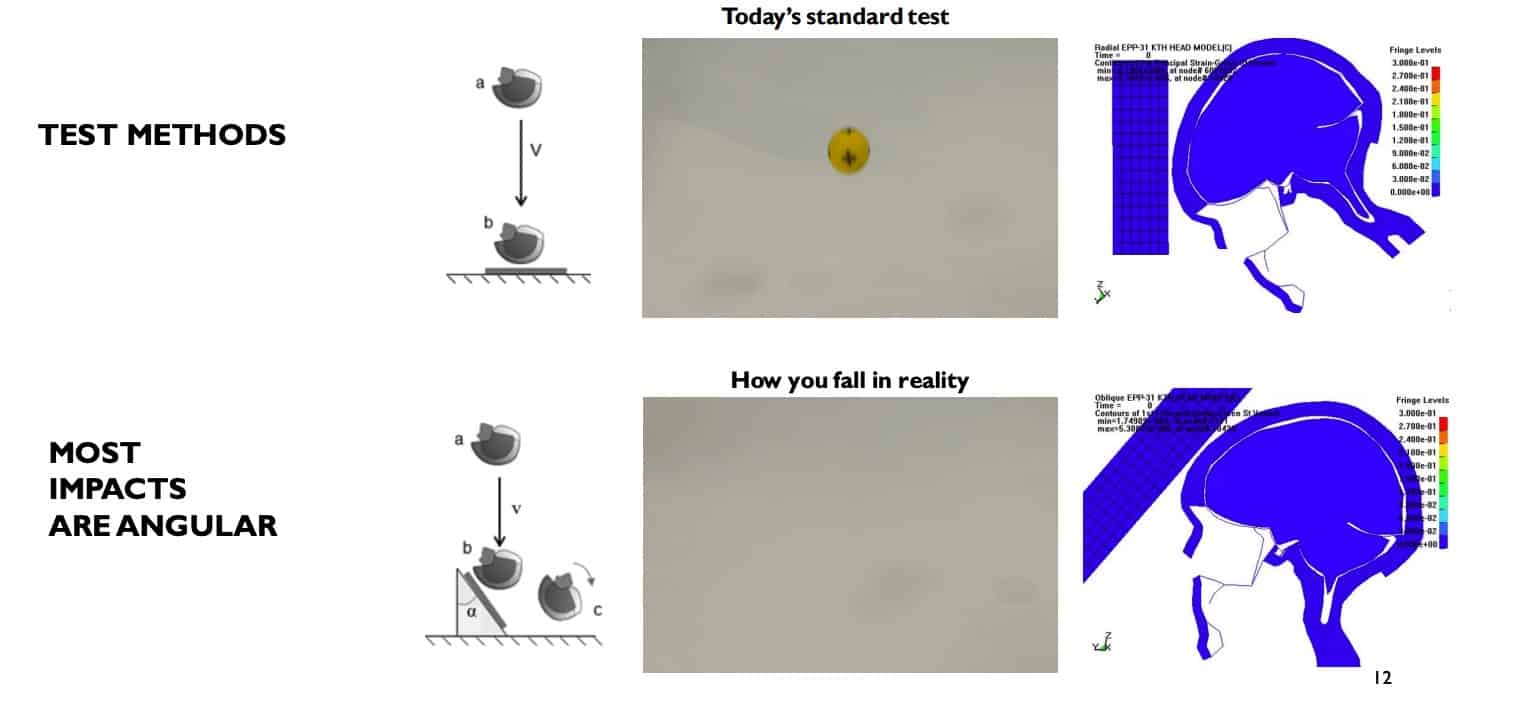

It doesn’t sound like a big deal, but it is. Most helmets are designed for direct (or linear) impact. Think of a straight jab to the face.

However, the most significant damage to the brain happens during rotational movements, like an uppercut.

You’ll see a boxer absorb straight jabs for 10 rounds, only to be knocked out by that one uppercut.

In other words, without MIPS, most helmets only really protect against linear impact. Unfortunately, most head injuries/accidents aren’t linear impacts. They’re angular, like falling off a bike or landing on your head after falling off a horse.

MIPS allows helmets to better protect the head against angular and rotational impact.

Schools like Virginia Tech have verified the benefits of MIPS’s safety products. Customers also love it.

The company sold 12.6M protective units last year through 143 helmet brands.

MIPS isn’t a low-margin helmet manufacturer. In fact, it’s a high-margin, fast-growing business that’s barely tapped its addressable market. Its MIPS brand is synonymous with helmet safety and a small (yet invaluable) part of its customer’s cost structure.

Sure, the company’s expensive on a multiple basis. But it has all the ingredients of a long-term compounding machine.

During this Note, we’ll explain MIPS’s competitive advantage, its unique business model, and why it helps to think of the company not as a helmet device manufacturer but as an ingredients brand company.

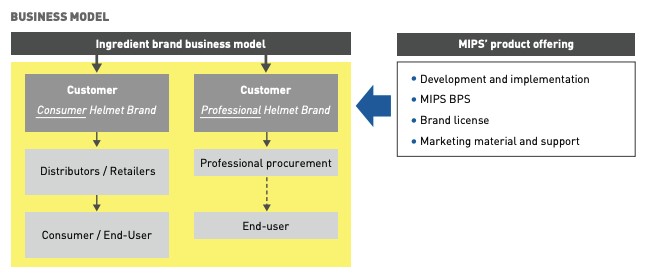

MIPS As An Ingredients-as-a-Service (IaaS) Company

The most important thing to understand about MIPS’s business model is that they create ingredients, not finished products.

The company explains it on their site (emphasis mine):

“Mips operates today as an ingredient brand. This means that Mips sells its products to helmet manufacturers who implement Mips technology in helmets that are then marketed to end users.”

In other words, MIPS is a COGS in the helmet manufacturer’s income statement.

MIPS offers a cheaper, better solution to helmet safety than manufacturers could make on their own.

Additionally, having a third party provide a “stamp” of safety approval allows consumers to feel like they’re buying a safer product. Not just some sales gimmick from the helmet manufacturer.

A good question at this point is, “why would helmet manufacturers want MIPS’s device?”

There are two main reasons. First, MIPS technology creates a safer, more effective helmet. Second, helmet manufacturers can charge more money for the MIPS-equipped helmet (usually $15-$20 more).

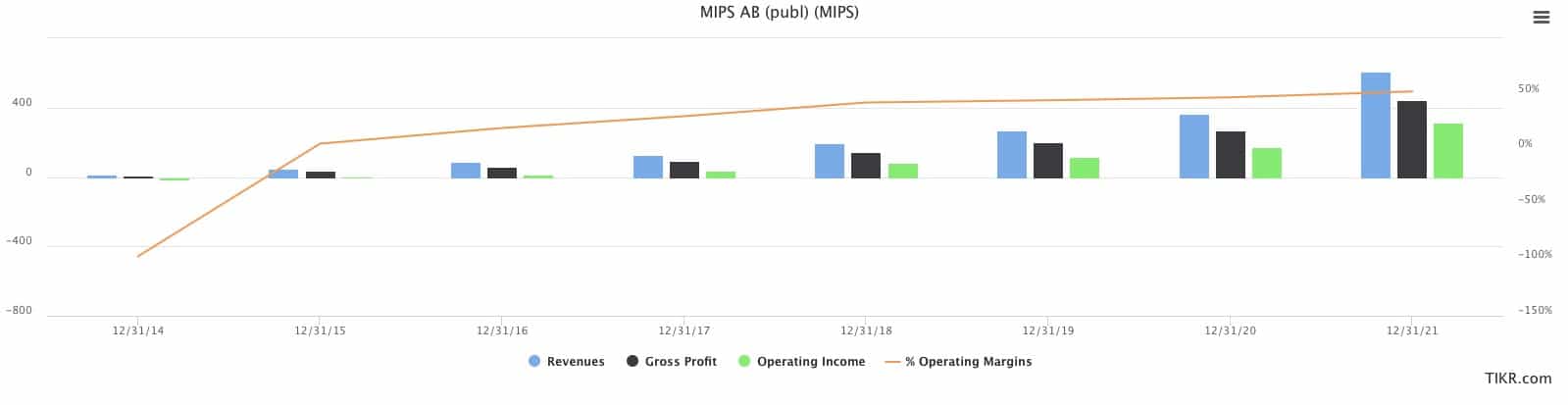

Ingredient businesses boast high margins, low inventory, and massive operating leverage.

One great example of this type of business is CHR Hansen (CHR). CHR produces cultures and enzymes that determine a food’s taste, texture, shelf life, and nutritional value.

Since 2006, CHR has doubled its EBIT margin and 9x’d net income margin.

MIPS is no different. Since 2014, the company has expanded gross margins from 50% to 73% while at the same time leveraging EBITDA margins 10x, from 5% to 50%.

There are a few ways MIPS generates such massive operating leverage. First, the company carries little-to-no inventory. They outsource the manufacturing of the devices to third-party contractors (mainly in China).

Last year, for example, the company generated SEK 608M in revenue with SEK 10M in inventory on the balance sheet.

Second, all the value is in the company’s IP. The physical product is mostly plastic (or plastic-like) material. Manufacturers only care about the safety the product brings and the yellow MIPS logo that it can smack on the helmet.

Finally, MIPS outsources its sales and marketing to its 143 brand customers. The company provides its customers with sales material and marketing education. But after that, it’s the brands that sell the product, not MIPS.

Over time, this has led to substantial SG&A compression from 126% in 2014 to ~17% in 2021.

The other way to think about MIPS is as a catalyst for increased revenue for every part of the helmet selling value chain. Here’s what I mean.

MIPS makes money by selling the safety device to manufacturers. Manufacturers make more money by upcharging their helmets to retailers due to the MIPS logo.

In return, retailers can upcharge the manufacturer helmet to customers because consumers are willing to pay top dollar for the highest quality safety device.

Everybody wins.

So we know ingredients businesses are good business. But what about the runway? How many helmets can MIPS still sell?

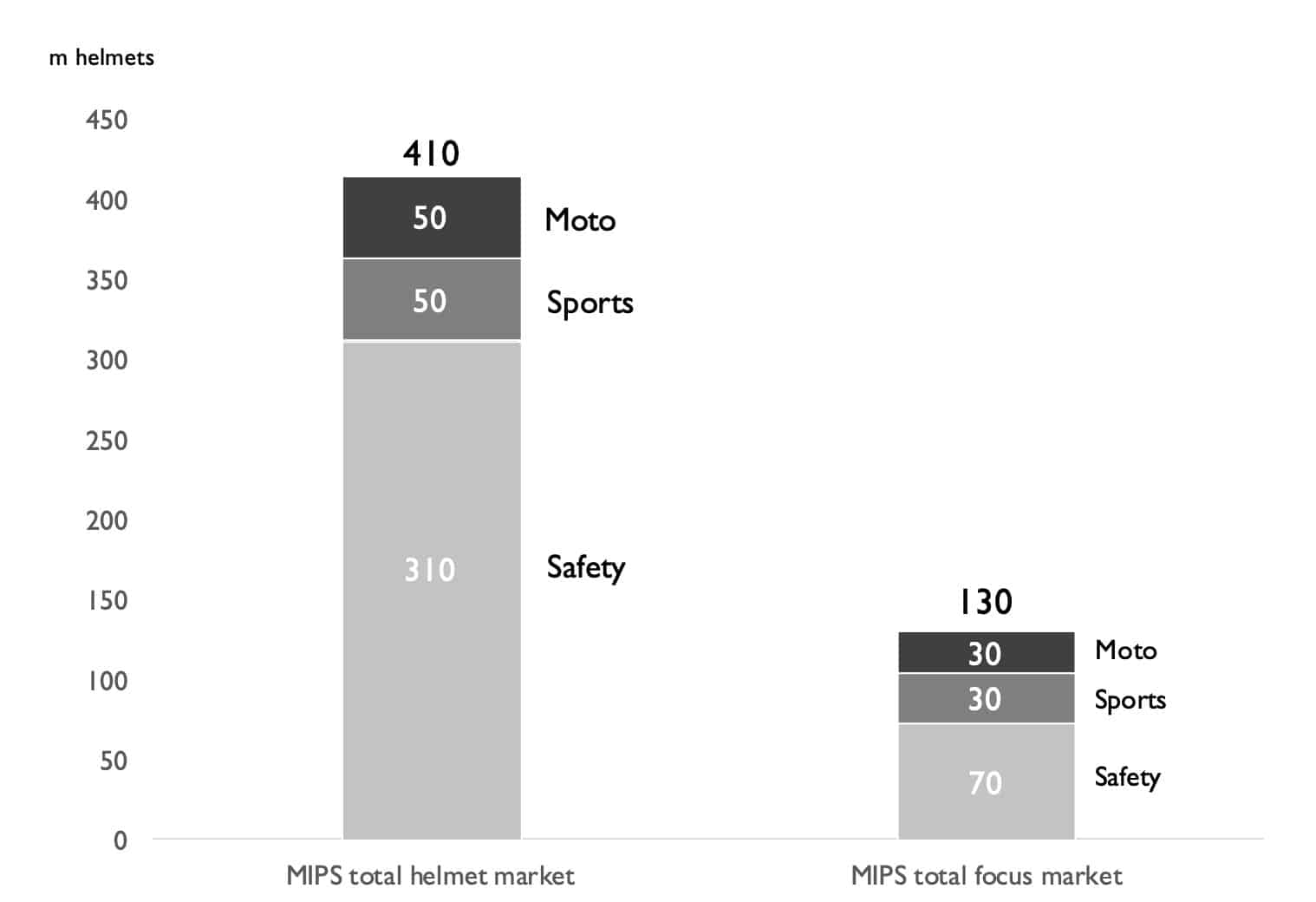

MIPS: Reaching 130M Helmets

MIPS sells three types of helmet devices:

- Sport: Bike, Snowsport, Equestrian, Hockey, Mountaineering

- Moto: Road Bike, MX

- Safety: Industrial, Military, Police & Fire Squad

The company currently generates ~94% of its revenue from Sport helmets and the rest from Moto.

MIPS thinks it can sell 130M helmets in its addressable market. Here’s how it breaks down:

- Sports: 30M helmets

- Moto: 30M helmets

- Safety: 70M helmets

Safety is a huge opportunity for the company, and it’s off to a great start.

You can read management’s thoughts on the safety segment during the latest earnings call (emphasis mine):

“In safety, we have established a strong customer base in 2021. We have launched partnerships with 9 different helmet brands, with 8 of them already starting to supply MIPS products to the market. We are creating an organization to continue to educate the market and support sell-through with our partners. And no change versus previous communications, volumes will start to increase throughout the year.”

MIPS sold 12.6M helmet devices last year, or ~10% of its target market. There’s plenty of room to grow.

Over time, MIPS can capture a greater share of its highly successful Sports Market (50M helmets).

How do they get to 130M helmets? By becoming the expected safety feature in every helmet made.

The MIPS brand is synonymous with “best in safety.” Eventually, the yellow MIPS logo goes from a “nice to have” to a “must have” for every sport, moto, and (potentially) safety helmet. Helmets without the logo will lose share to those with the logo, and the rest is history.

What does that look like from a revenue and earnings perspective?

How Big Can MIPS Get?

As mentioned earlier, MIPS generated SEK 608M in revenue last year on 12.6M helmet installations. That’s ~SEK 48 per helmet in revenue.

Suppose MIPS captures 25% of its 130M helmet market over five years. That gets us 32.5M helmets for SEK 1.56B in revenue.

Let’s also assume MIPS generates ~50% EBIT margins, giving us SEK 780M in operating income.

Assuming a 75% FCF conversion rate, we get SEK 585M in FCF at 32.5M helmets.

That’s ~29x the current market cap. No low expectations here!

I’d argue that 29x FCF for an ingredients company is actually a cheap price. Put down the pitchforks and hear me out!

Remember CHR? Since 2014, CHR has traded at 54.6x Market Cap/FCF.

I know, it’s wild assigning a 50x FCF multiple to a company. But what if we can get away with it here?

Assuming a buyer would pay 50x FCF at 32.5M helmets, we’d get ~SEK 29B in market cap (SEK 1,125/share). That’s 73% higher than the current price.

Where Can We Go Wrong?

Not only does paying a high price mean you need a lot to go right. But more importantly, not much can go wrong, either.

One major risk with MIPS is that most third-party manufacturers reside in China. MIPS needs to find ex-Chinese manufacturers between rampant COVID lockdowns and China-specific tariffs.

Also, what happens if MIPS reaches market saturation and every helmet has a MIPS safety device? What sounds like an ideal scenario quickly turns into a commodity product with little differentiation between helmet manufacturers. Will products then compete on price, style, etc.? And will MIPS get squeezed out in the process?

Finally, there’s the stock price. Again, there’s a lot of growth baked into the current price. And yes, MIPS can get there. But there’s not a ton of margin of safety at these prices. Remember, our above scenario assumed a 50x FCF exit multiple.

Concluding Thoughts

MIPS is an excellent business and is currently valued like one. Ingredient brand businesses have historically commanded premium multiples, and MIPS is no different. The company has enough runway to double its current helmet count and has barely tapped its largest market, Safety.

The company’s inventory-light business model generates incredible operating leverage, allowing MIPS to sustain 45-50% EBIT margins over time at scale.

MIPS is an exciting opportunity to own a high-quality ingredients business growing revenues at 30-40% per year at 50%+ EBIT margins. Maybe a business like that should trade at 50x FCF!