Measured Moves… [Dirty Dozen]

Lord Yagyū once said, “I do not know how to defeat others. All I know is the path to defeat myself. Today one must be better than yesterday, and tomorrow better than today. The pursuit of perfection is a lifelong quest that has no end. ~ Hagakure: The Secret Wisdom Of The Samurai, via Brent Donnelly’s post

In this week’s Dirty Dozen [CHART PACK] we talk about measured move targets hit in the SPX, cover the recent BofA GFS highlights, discuss loose fiscal / tight monetary, update the bullish crude picture, then talk currencies and precious metals, plus more…

**Note: Enrollment to the Macro Ops Collective is NOW OPEN.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you want to develop a robust edge in this macro regime, make sure you become a member.

**Enrollment will stay open until Sunday, July 30th at midnight CST.

You can learn more about the Collective and what it can do for your investing here.

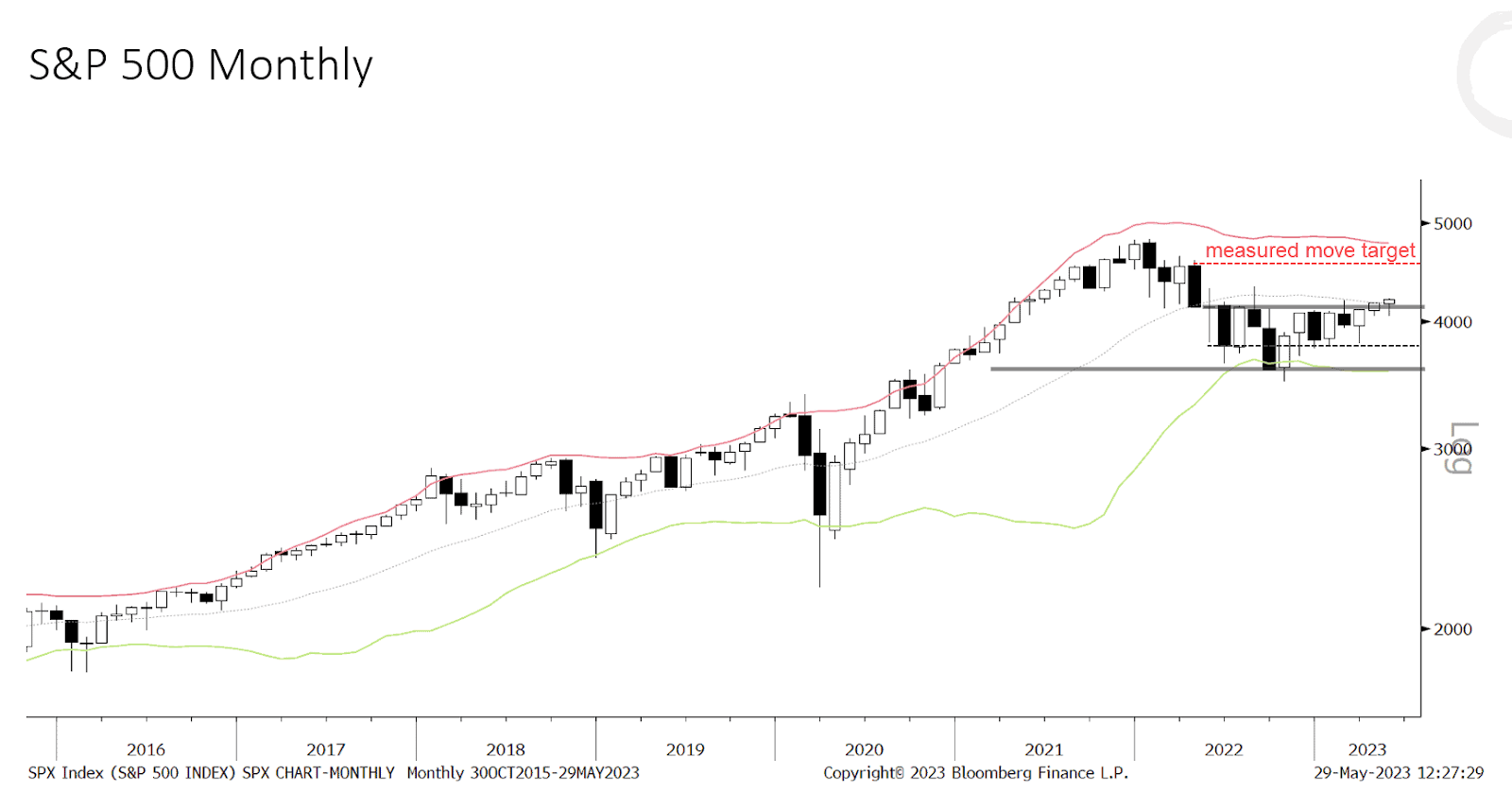

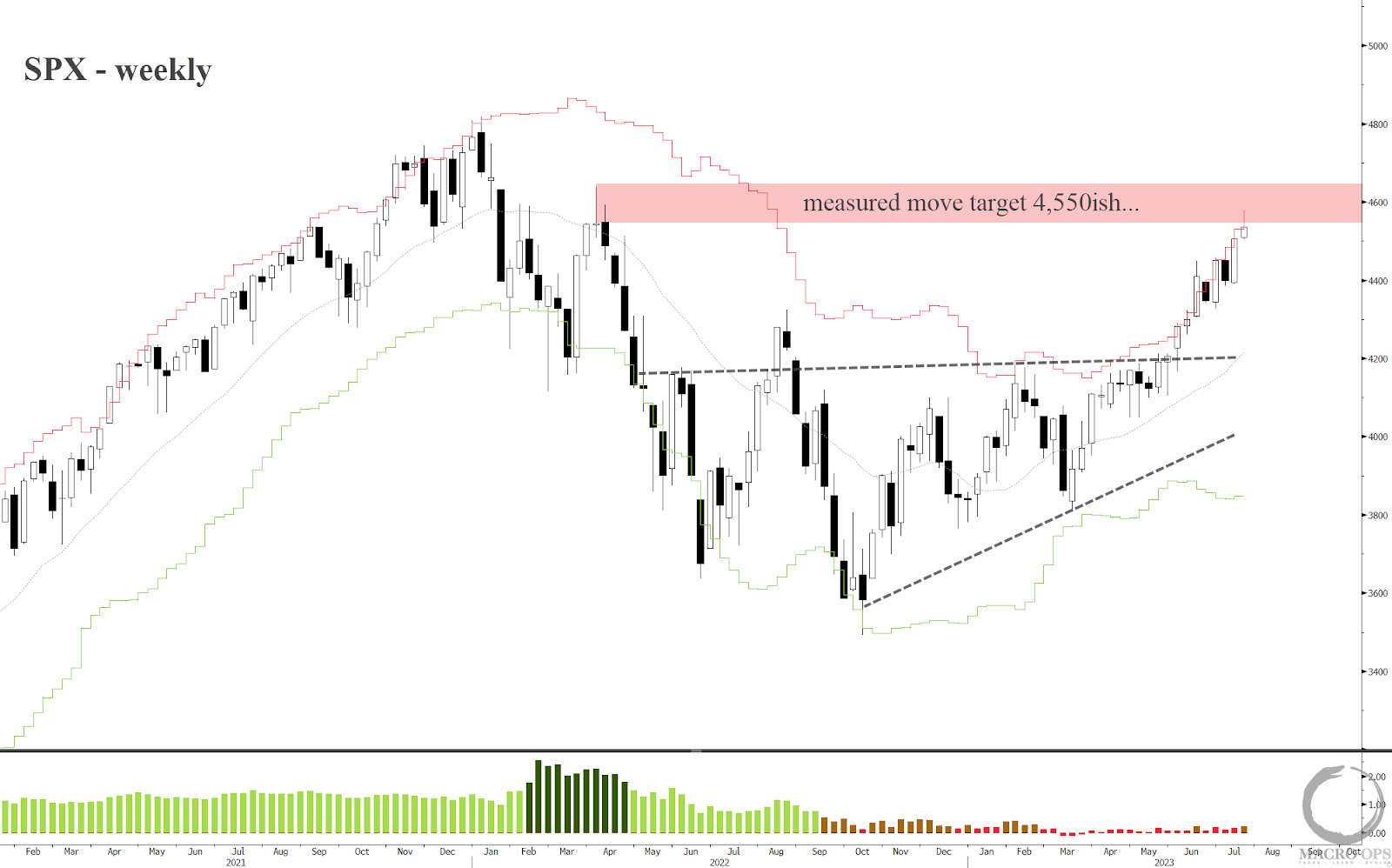

1. Back in the May 30th edition of DD I wrote ‘There are only two more trading days left in the month of May. Barring a strong bearish reversal it looks as though the SPX will end the month with a bull and confirmation breakout bar from its 10-month trading range.

“The April high (around 4,500ish or about 9% higher) is the measured move target for this breakout”.

2. Last week we completed the measured move. While the confluence of data we look at still (at least for now) supports the trend up in risk assets, this move is extended and getting a bit tired (our Trend Fragility indicator is now in the 80th percentile).

Our take is to stay long but tighten up stops, take partial profits, and lighten up on risk.

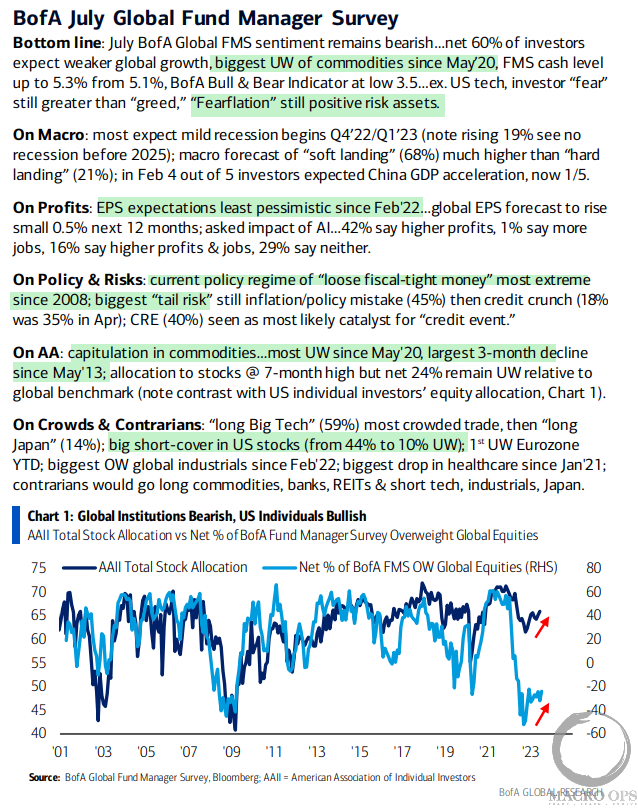

3. Here are the highlights from the latest BofA FMS…

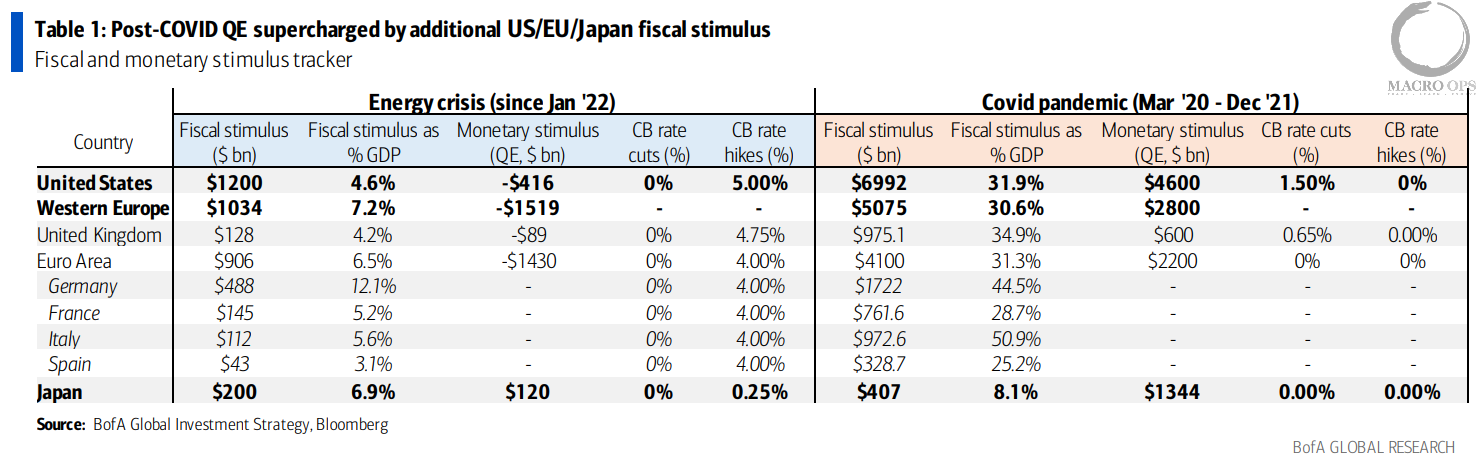

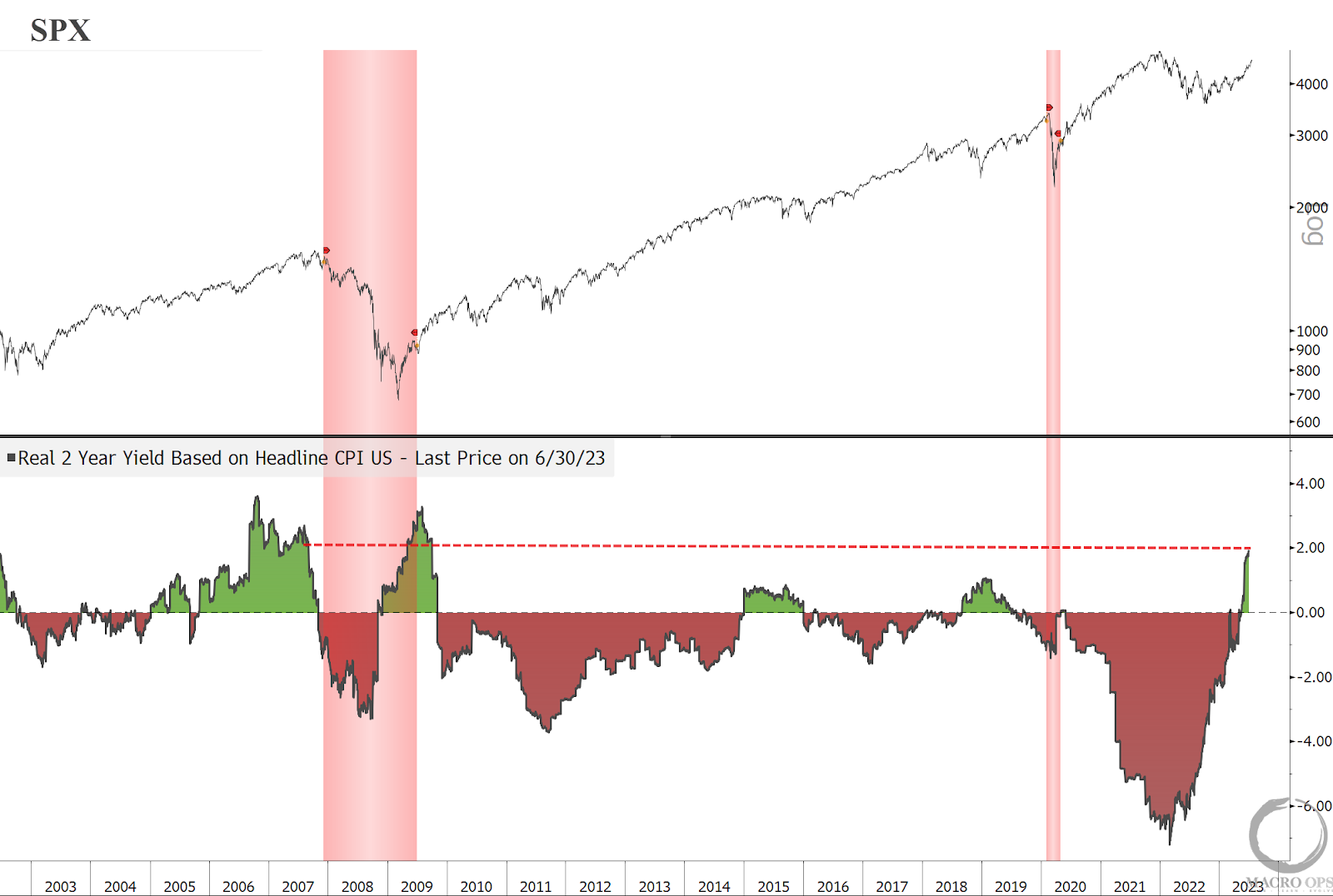

4. BofA says that “loose fiscal and tight monetary” is the new name of the game. While we agree that fiscal has and continues to be loose, the monetary side only became restrictive very recently.

5. The US 2y real yield was deeply negative up until just recently, thanks to high inflation and a Fed that was too slow to hike. It’s only now becoming restrictive and should start to be felt in risk-assets soon.

6. Plus, we’ve probably seen all of the benefit we’re going to see from inflation surprising expectations on the downside.

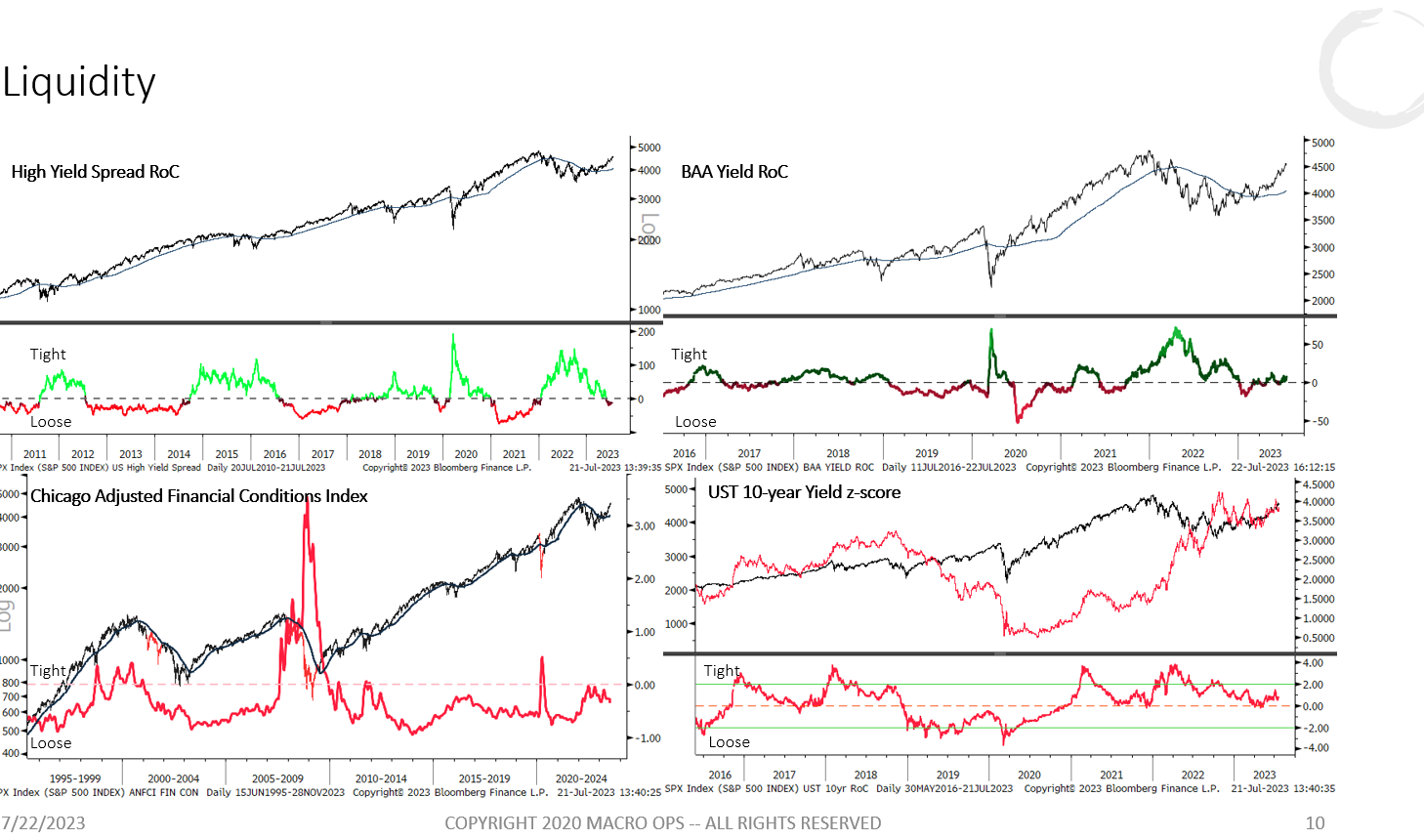

7. Which means we should expect liquidity, which is currently pretty easy, to begin tightening over the coming weeks and months.

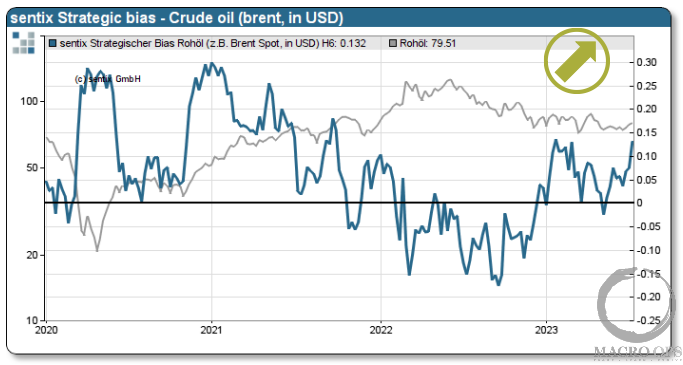

8. A potential inflationary tailwind is crude, which we’ve been pointing out over the past month was in a nice technical setup with a backdrop of historically bearish speculative positioning. Sentix’s latest survey also shows investor “Strategic Bias” for crude is rising, which is a positive for the Texas Tea.

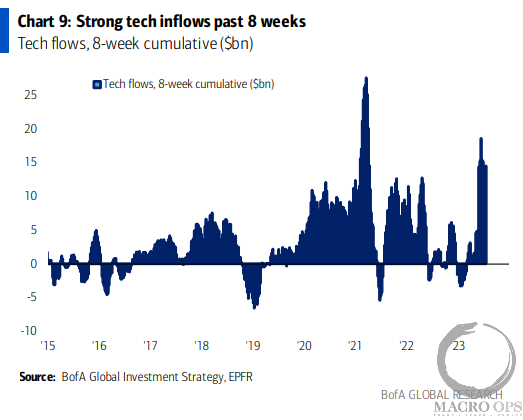

9. A breakout in oil will likely lead to a breakdown in bonds which should then put the pinch on richly valued overbought tech.

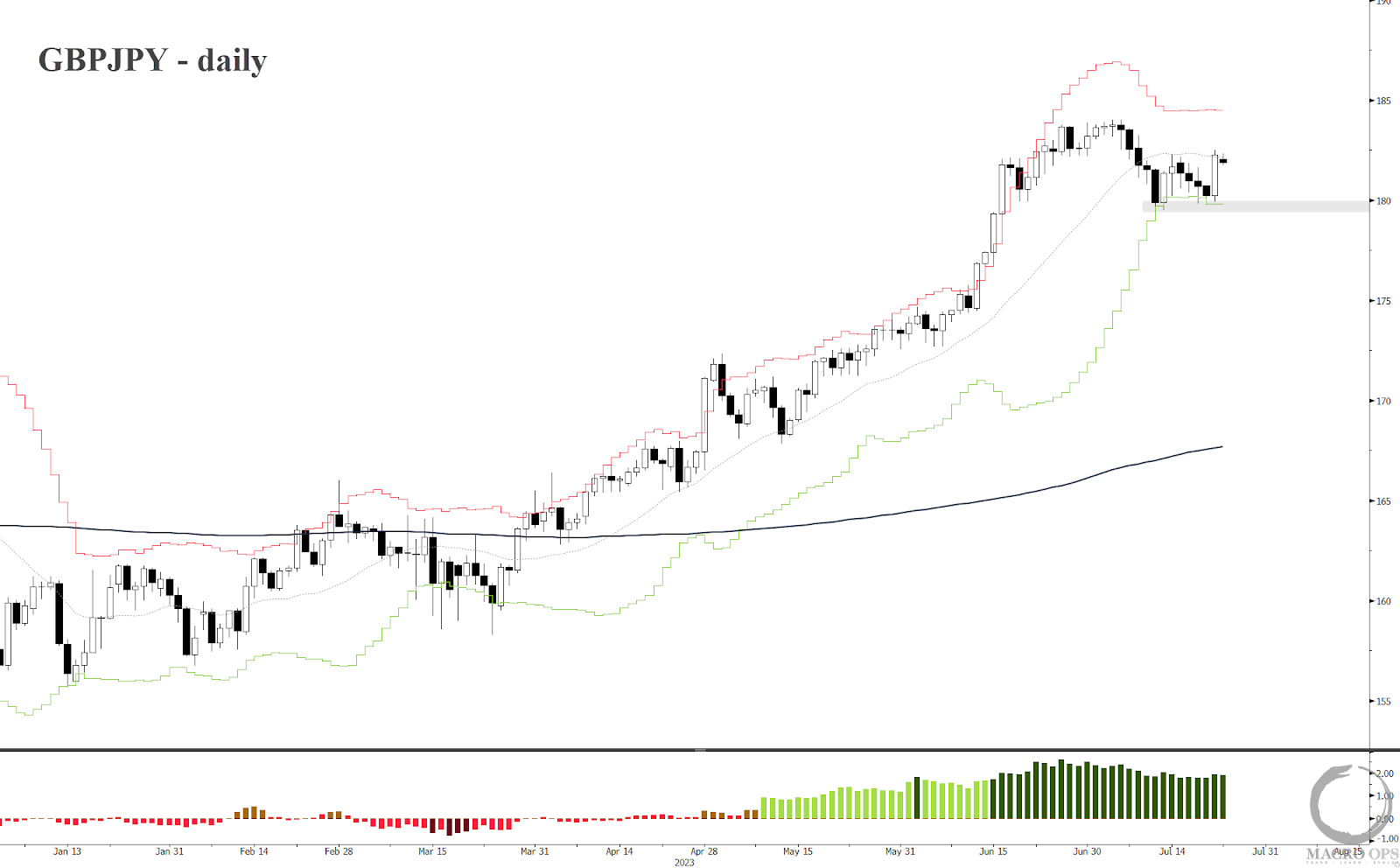

10. A few weeks ago we pointed out the one sided positioning in JPY (short) and GBP (long). While specs have covered some of their JPY shorts, they remain all in on the pound.

11. I still like shorting GBPUSD here, especially if we see it retrace some of its recent selloff. And the GBPJPY short I mentioned earlier this month continues to setup. I’d short on a close below the grey line or a reversal near recent highs.

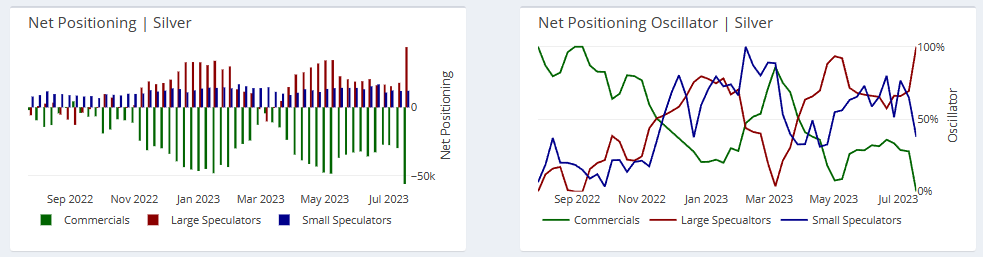

12. We’re very bullish on precious metals over the next few years but positioning has us tactically playing them on the short side at the moment.

Take silver for example. Last week large spec positioning in silver saw a significant jump to over 1yr highs. And from the technical side, silver is at the upper range of its multi-year range and so susceptible to mean reversion back near its midline of current congestion.

Thanks for reading.