Manolete Partners (MANO) is UK’s leading third-party insolvency litigation finance (TPF) company. They command ~67% of the TPF market. MANO plays a crucial role in returning funds to creditors, particularly the HMRC. The company buys 80%+ of their claims, giving them full control of the outcome. The average case settles in 11.5 months, with MANO getting paid ~12 months post-settlement.

There are two main ways to fund litigation claims in the UK: TPF and CFA/ATE. The CFA/ATE method is commonly referred to as the “no-win/no-fee” funding. This method commands ~86% of the litigation finance market. The problem with no-win/no-fee is that it’s expensive. CFA/ATE financing can cost upwards of 200% of total damages. Third-party funding (MANO’s model) is a much cheaper option. MANO’s model costs ~10-12% of total damages. The company is a large fish in a small (but growing) pond of TPF claims.

Sparking the growth of the pond is the Jackson Reforms Act of 2016. This act encourages claimants to fund litigation services via third-party financing companies, like MANO. And as the clear market leader in TPF financing, MANO stands to gain the most from this piece of legislation.

The company sports a robust business model with significant operating leverage. Since 2016, MANO’s grown revenue from GBP 4.8M to GBP 18.68M as of 2020 (57% CAGR). They’ve expanded gross margin 2,200bps from 55% to 77% and increased EBIT margins by 1,430bps from 38% to 52.5% during that time.

MANO also has a long history of delivering exceptional returns from its insolvency claims portfolio. The company’s made 567 claim investments since 2010. In 353 (62.3%) completed cases, MANO’s delivered (on average) 187% ROI, 2.87x MoM, and a 133% IRR. They also boast a 90% success rate on purchased claims.

Today, the company’s buying more cases, expanding its in-house litigators’ network, and returning capital to shareholders. COVID will further exacerbate the need for litigation finance, offering a long runway for continued litigation investment.

The stock sits near its 2019 IPO offering at GBP 93M. If MANO executes and expands its share in total insolvency cases claimed, the company should be worth GBP 560M. That’s a 500% upside from current prices.

Reasons for the share price collapse include former major shareholders taking profits (Soros, etc.), deferral litigation cases due to COVID, and a general misunderstanding of unrealized/realized gains from settled cases.

What Makes Manolete Different?

When I say the words “litigation finance,” some investors will undoubtedly shirk behind their screens. Litigation finance resurfaces painful memories of the Burford (BUR) scandal, spearheaded by Carson Block at Muddy Waters Research.

Manolete is different from Burford in three key ways:

- MANO buys rights to the claims (i.e., they don’t fund the lawsuit)

- MANO settles cases in less than a year

- MANO is hyper-focused on a niche market (UK insolvency litigation)

Let’s start with the first distinction.

Buying Rights vs. Funding Claims

Manolete buys rights to lawsuits, much like investors can buy call options (or rights/warrants) on underlying stock positions. These “calls” give Manolete the right to file a lawsuit against a defendant if the potential reward generates a decent return for the partnership.

Buying rights to suits is a vastly different model (Burford’s model) than funding cases. When you fund a case, you have no direct ownership of the result. You can’t cut your losses if the suit incurs substantially more costs than expected.

Let’s use divorce settlement as an example. Say you decide to fund a divorce litigation case for $250K (I’m not a divorce lawyer, so making up numbers here). You pay the $250K to fund the case. Mediation talks get nasty, and both parties entrench themselves in their settlement desires.

Eighteen months later and both parties are still at each other’s throats. Since you’re funding the operation, the only way to get paid back is to keep investing in the case to conclude. Now you’re in another $250K. Etcetera, etcetera.

In short, there are massive diseconomies of scale when you fund claims. Every incremental dollar funded reduces the firm’s return on invested capital, thus lowering returns and lifting operating expenses.

Manolete doesn’t have this problem because they buy the right to the claim. Like a call option, they decide to execute that right. If a claim doesn’t make economic sense, they don’t buy. The company can cut their losses short (which they infrequently do). MANO averages GBP -9,000 on aborted claims.

The ability to execute on the claims you want versus funding the claims you need leads us to our second differentiator.

Quick Settlements: High Cash Conversion Leads To Higher Claim Values

Buying claim rights also allows MANO to choose cases that can resolve within a year. The company’s average claim-to-settlement period is ~11 months. From there, it takes ~12 months for MANO to receive the cash payments.

Quick turnarounds also matter because we’re working with discounted cash flows. Like any claim on future cash, one must discount cash received in the future to a present value. We do this because if we receive a dollar today, we can reinvest that dollar and generate some return for as long as we invest it.

The longer it takes to settle and receive cash, the lower its value is to investors. MANO’s most extended outstanding case is from 2017. 62% of their outstanding cases come from the current year’s cases.

Hyper-Focused: Riches in Niches

MANO can achieve quick turnarounds because they’re obsessed with one market: UK Insolvency Litigation. BUR, in comparison, does litigation for numerous countries, including North America, Europe, Asia, and Australia. BUR has also expanded its services to include portfolio finance, asset recoveries, and post-settlement investments. Something about a jack of all trades, master of none?

When it comes to litigation finance, hyper-specialization wins. MANO chose one type of litigation (insolvency) within one market (United Kingdom).

This level of focus made MANO synonymous with “insolvency litigation” inside the UK. A few companies tried competing with MANO inside the UK and failed (BUR, Ferguson Litigation, etc.).

This level of focus made MANO synonymous with “insolvency litigation” inside the UK. A few companies tried competing with MANO inside the UK and failed (BUR, Ferguson Litigation, etc.).

In a July 2019 presentation, an analyst asked MANO’s CEO Steven Cooklin whether he would expand its services into other countries (like Australia). His answer was perfect and told of the company’s strategic competitive advantage. I’m paraphrasing (emphasis mine):

“Here [in the UK], we know the defendants. We can see their property, we can see their assets, we can see what businesses they’re running. And we can buy the claims. The moment we step outside of that market I start to question all those assumptions. Purple Bricks, Marks & Spencer, Tesco, they’ve all had such problems [expanding outside the UK] and I’m determined not to make those same mistakes.”

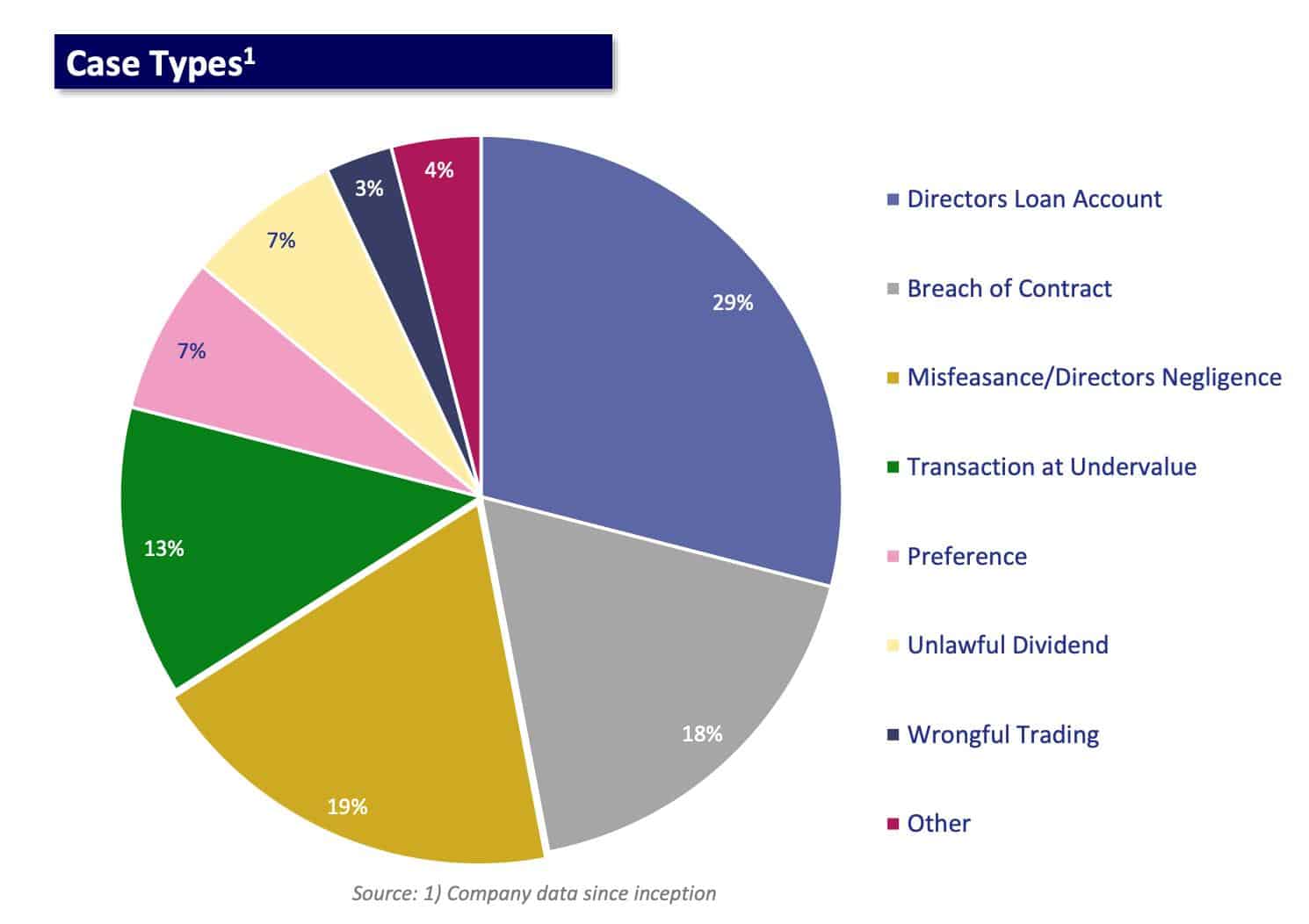

Another benefit of hyper-focus is the company’s ability to “autopilot” its claim approval process. MANO only does seven types of insolvency litigation (above).

By focusing on the seven above cases, MANO can make faster decisions on whether to buy a claim or not. More immediate decisions mean MANO is often the first-mover in taking insolvency litigation claims. You can see the company’s case selection process below:

MANO also solves the agency risk problem for many insolvency plaintiffs (IP). MANO is the logical partner for IPs as UK’s leading insolvency litigation firm because there’s a personal claim on the case’s outcome. If given a choice, would you choose MANO or an unknown, non-UK company?

Manolete’s Current Claim Portfolio

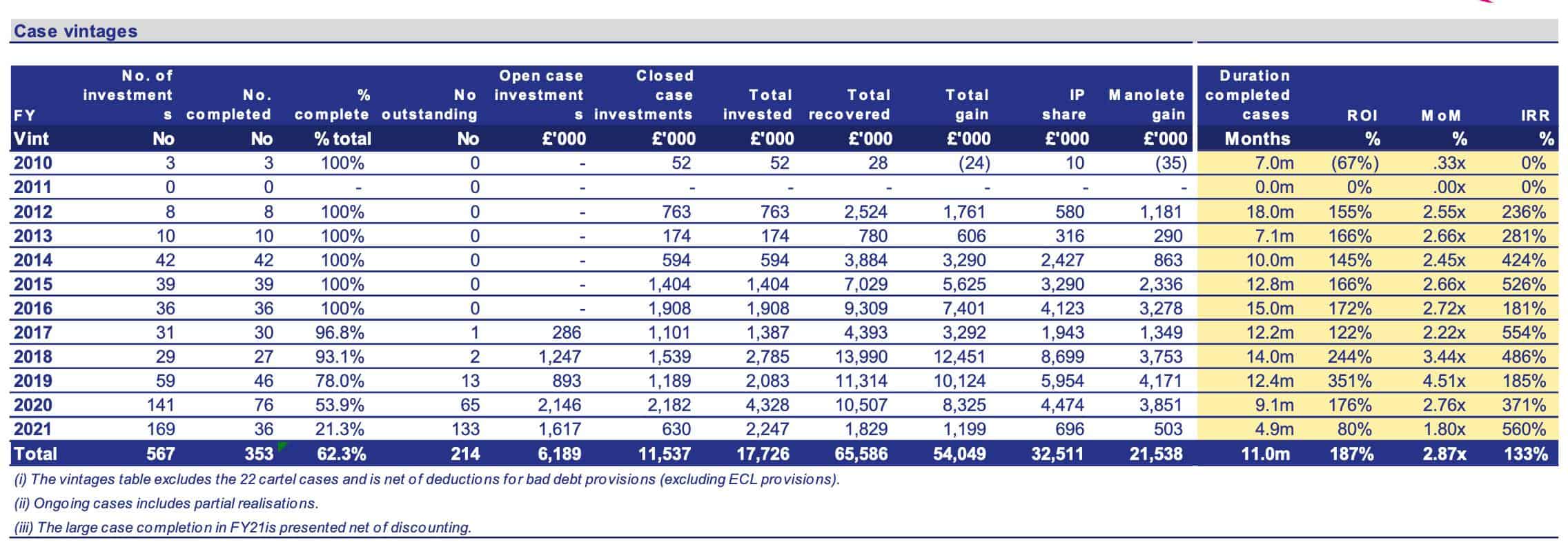

Below is the “case vintage” table for MANO’s claim portfolio. Think of this as an acid test for the company.

As we mentioned earlier, MANO’s quick settlement time (11 months) means fewer outstanding cases and more cash payments. There are four key metrics when assessing MANO’s claim book:

- Total Invested

- Total Recovered

- Total Gain

- Manolete Share Gain

Since 2010 Manolete’s spent GBP 17.7M buying claim cases. That’s an average of GBP 31.26K per case.

The company recovered GBP 65.6M from completed cases, or GBP 185.8K per case. From there, MANO collected GBP 54M in revenue from those closed cases or GBP 153M. In other words, 82% of the amount recovered flows through to revenue to split between the insolvency party and MANO.

MANO’s total split of completed case recovery gains is GBP 21.54M or GBP 61K per case. In other words, MANO gets 40% of the total profits, giving 60% to the insolvency partners.

Over the last decade, the company’s averaged 187% ROI, a 2.87x MoM (money multiplier), and a 133% IRR.

These figures are mouth-watering, no doubt. But the company can increase its returns over time through its natural economies of scale.

MANO’s Increasing Returns To Scale

Remember the funding-based diseconomies of scale discussed earlier? MANO (thankfully) has the opposite “problem.” Since the company buys rights to claims, they control both sides of the ROI lever: amount invested and total gain recovered.

Since MANO is one of the most substantial capitalized insolvency firms in the UK, they can buy higher-dollar claims than their peers incrementally. That means (potentially) higher total gains recovered.

Since MANO is one of the most substantial capitalized insolvency firms in the UK, they can buy higher-dollar claims than their peers incrementally. That means (potentially) higher total gains recovered.

But here’s the best part. It costs MANO the same amount of money (in operating expenses) to analyze and process a higher-dollar deal.

Over time, these two levers (higher-dollar claims and fixed operating costs) can generate substantially higher ROIs, MoMs, and IRRs.

The Rapidly Growing Pond of UK Insolvency Litigation

Insolvency litigation is a rapidly growing sub-sector of the UK’s financial industry. The country has between 14K – 20K corporate insolvencies and 40K+ personal bankruptcies in a given year. On average, there are ~2,300 insolvency cases per year generating ~GBP 750M in cash recoveries.

There are three reasons why MANO will get a larger part of the insolvency case pie:

- MANO Solves The Robin Hood Dilemma

- TPF Will Continue To Take Share (Jackson Reforms)

- Increased Cases Due To COVID

Let’s break each down.

MANO Solves The Robin Hood Dilemma

The UK sucks when it comes to resolving insolvency litigation claims. They’re 14th in the World Bank ‘Resolving Insolvency’ Ranking. The single most important criterion in this ranking is creditor recoveries.

Improving the UK’s insolvency ranking is crucial because it solves its ‘Robin Hood Dilemma.’ Here’s what I mean. The creditors (MANO’s insolvency plaintiffs) are honest suppliers, innocent customers, and do-good businesses.

The people screwing these honest plaintiffs aren’t as clean. They’re shady businessmen/women engaging in illegal tax fraud. Tax fraud leaves Her Majesty’s Revenue & Customs (HMRC) short on revenue, negatively affecting UK hospitals, schools, and other government services.

MANO acts as ‘Robin Hood’ for these unheard insolvency plaintiffs. Like Robin Hood, MANO robs (in this case, lawfully takes) from the corrupt to give to the poor (rightful victims).

A low Resolving Insolvency ranking would reduce people’s incentive to start businesses in the UK. The Times ran an article in January 2021 outlining this concern (emphasis mine):

“The Royal United Services Institute think tank said that fraud against businesses, individuals and the public purse has reached “epidemic levels” in recent years and a poor response from the authorities “undermines [the] UK’s critical financial infrastructure and the reputation of the UK as a place to do business.”

And given that the entity getting screwed the most is the HMRC, there’s a strong reason for the UK parliament to act in favor of improving insolvency litigation.

TPF Will Continue To Take Share

As we mentioned before, third-party financing represents ~14% of the total insolvency case market. That percentage will increase over the next decade, thanks to the Jackson Reform 2016 Act.

As we mentioned before, third-party financing represents ~14% of the total insolvency case market. That percentage will increase over the next decade, thanks to the Jackson Reform 2016 Act.

Check out the spike in MANO’s new quarterly cases since the Jackson Reforms.

MANO went from 5-7 new cases per quarter to 20-40 over the last year.

This trend will continue as more insolvency cases go to TPFs because they’re 13x cheaper than no-win/no-fee alternatives.

COVID Will Spark New Wave of Cases

COVID-19 relief packages sparked a wave of fraudulent business activity. While many businesses have closed during COVID, there’s a wave of companies kept alive by free-money financing. The easy money policy will end at some point. And when it does, the UK will see a massive increase in insolvency cases.

MANO outlined a few reasons why COVID will lead to increased cases in their latest investor presentation (emphasis mine):

“Insolvencies have been deferred, not averted.” Disappointing for business owners, great for MANO.

Thinking About Valuation: A Potential 5-Bagger

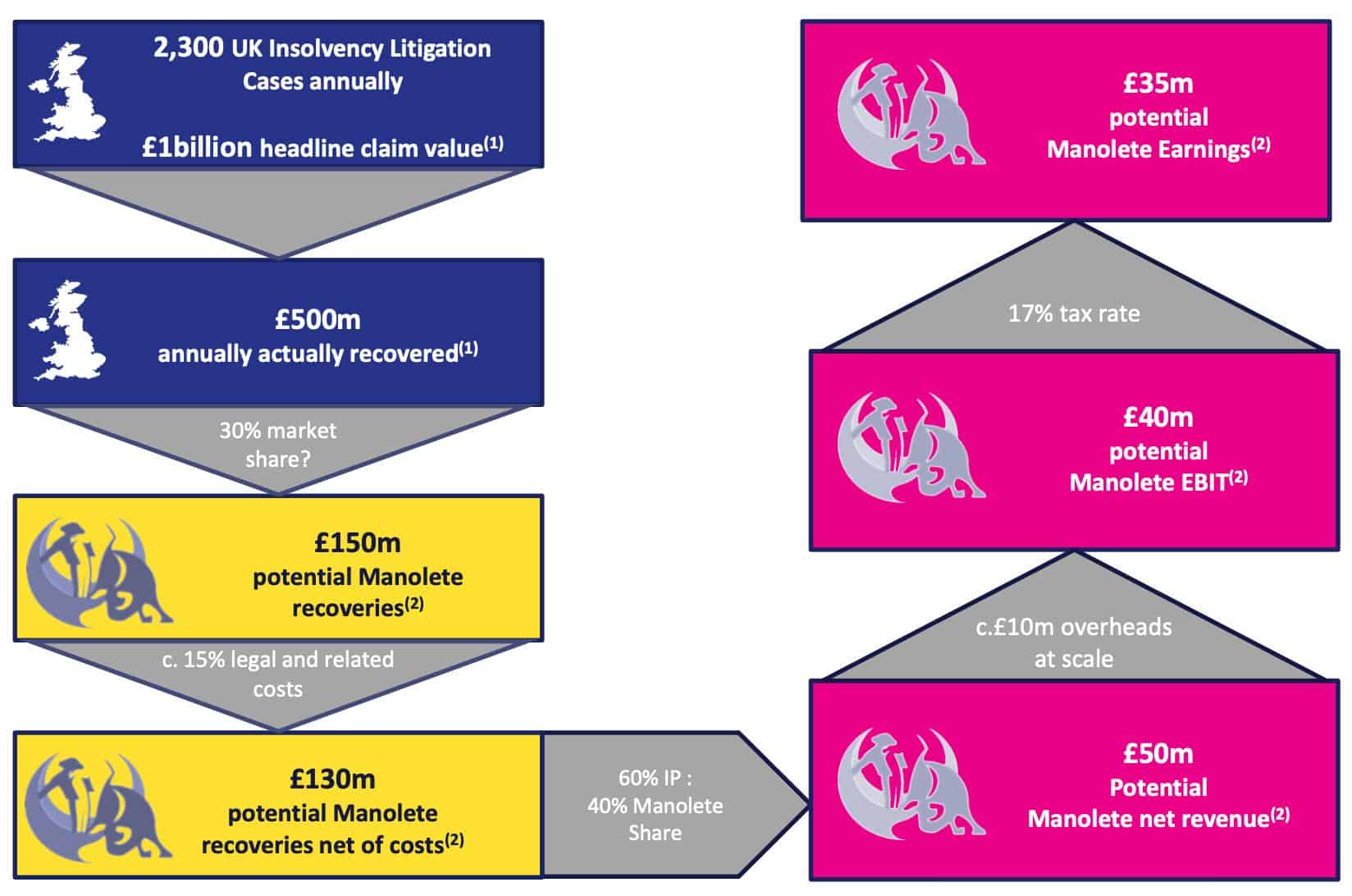

MANO gave investors a roadmap to get from the total market to the company’s after-tax earnings in their 2019 investor presentation deck (see below).

Let’s walk this out.

There are ~2,300 annual cases generating GBP 1B in claim value. The company updated the annual recovered amount to GBP 750M in their 2021 pitch deck, reflecting a more generous portion of claim values converting to revenue.

With this GBP 750M in recovered claims, MANO management thinks they can capture 30% total market share. A 30% market share gets MANO GBP 150M in company recoveries. It costs the company ~15% of recovery revenue to service the claims. That leaves us with GBP 130M in net recoveries for distribution between IPs and MANO.

The company assumes a 60 IP / 40 MANO split on net recoveries, giving MANO GBP 50M in net top-line revenues. At scale, the company will spend ~GBP 10M/yr in overhead costs, leaving us with GBP 40M in EBIT.

Apply a 17% tax rate on EBIT, and you get GBP 35M in after-tax earnings. We can argue that 30% market share is high or low. I’d favor the “too low” side as MANO’s shown competition to try to enter the space and fail.

This time last year (March 2020), the company traded for ~16x normalized earnings. If we attach that same multiple to our above assumptions, we get a GBP 560M market cap company.

The stock currently trades at GBP 93M. Our above valuation implies a 502% upside for MANO’s stock or a 5x return on our money.

Say we cut MANO’s market share assumptions in half (from 30% to 15%). That still gets us GBP 17.5M in after-tax earnings. Sticking a 15x earnings multiple on that figure gets us GBP 262.5M in market cap, or 182% upside.

Moreover, the company hasn’t issued any additional shares since its IPO. The business lives on cash from internal operations. Management’s also made it clear they don’t see a need to issue further shares.

Risks & Potential Rebuttals

There are a few ways this investment can go wrong. First, the company could lower its claim underwriting standards. Lower underwriting standards would decrease their winning case percentage while increasing operating expenses (lowering margins, ROI, and IRRs).

Second, the company expands into tertiary markets like Australia or other European countries. The whole point of their competitive advantage is their dedication to hyper-local market niches.

Third, the company can’t maintain equitable recovery revenue splits with its IP partners. We don’t want to see IPs capture 70-80% of the revenue split. It’s crazy to think that MANO could survive in this scenario, but equity shareholders wouldn’t benefit.

Fourth, MANO’s lawyers decide to split off and start their own insolvency litigation business. In-house turnover is a low probability event given the agency risks associated with insolvency cases. The company also boasts a 100% retention rate from their in-house lawyers since IPO. It’s hard to leave when many lawyers receive pay raises from their previous employer when joining MANO.

Fifth, debt gets out of hand, and the company can’t collect on its claimed cases to service the interest payments. I’m not against MANO assuming more debt. After all, the company’s generating 187% ROI on bought claims. They also have a line of credit with HSBC at ~2.5% interest. That’s a good formula: borrowing at 2.5% to invest in 187% (average) ROI claims.

Concluding Thoughts

MANO is one of the most asymmetric investment opportunities we’ve seen in the last two years. As a standalone asset class, insolvency litigation can generate uncorrelated returns from the broader market. MANO wins by dominating the local market and focusing on its hyper-niche specialty.

Profit-taking from large institutional investors (Soros, Premier Asset, Canaccord) and COVID-deferrals drove the stock down to prices not seen since its IPO. Yet since that time, the company’s 5’xd operating income and expanded profit margins to 50%.

We’re long shares at Macro Ops and will continue to add to our initial investment.