I spent most of the summer studying the copper market, its supply/demand dynamics, and potential future imbalances.

I found a market facing supply issues starting in 2025 due to The Great Electrification and the world’s race to Net Zero by 2050.

But that’s all in the future. Today, the market clears with supply matching demand at ~25Mt.

So, it becomes a question of what we must believe about future supply and demand to fulfill that imbalance. That’s where things get hairy.

Why? Because you must believe in the government’s ability to a) forecast future demand and b) see its Green Energy Transition plan to fruition in the initially stated timeline.

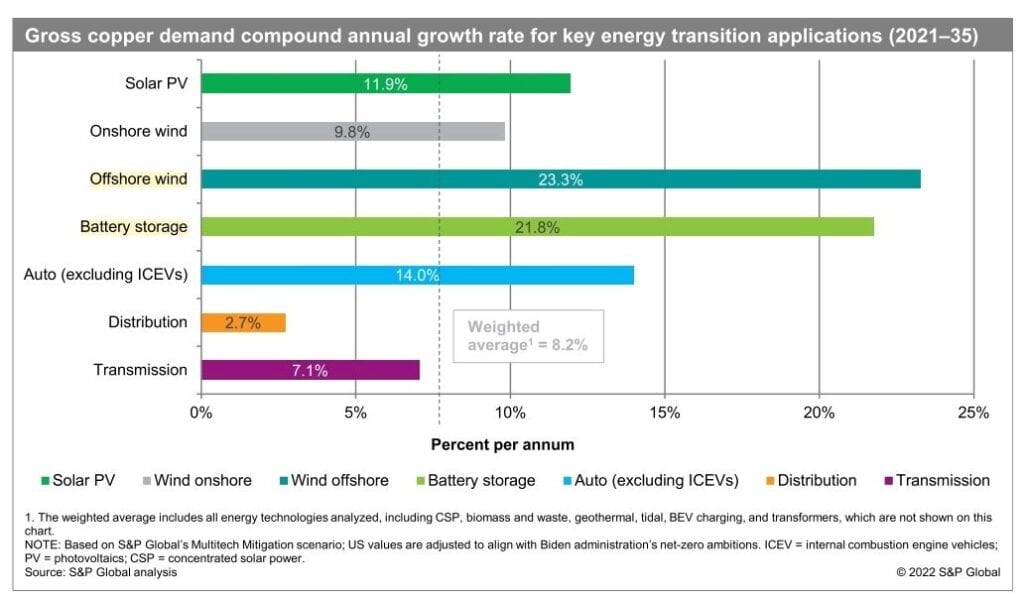

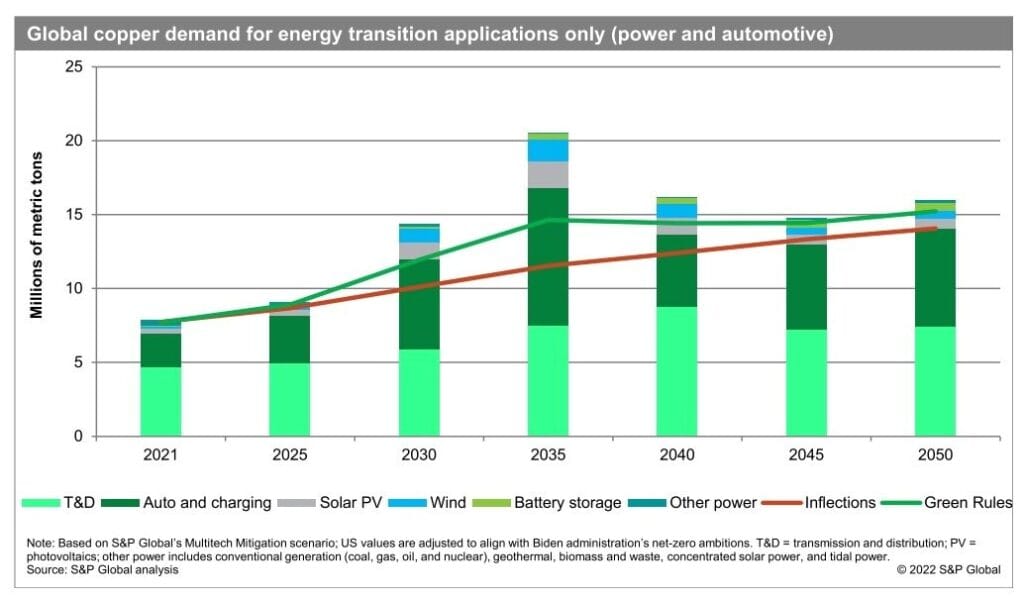

Here’s what I mean. For the Green Energy Transition to work by 2050, we’d need copper demand to grow by ~8.2% from 2021 to 2035. Where will this demand come from? Solar PV, Onshore Wind, Offshore Wind, Battery Storage, and EV Adoption (see below).

As a reminder, historical copper demand growth is ~2-3% or in line with global GDP. In other words, we’d need a 4x increase in copper demand over a decade to meet Net Zero 2050 goals.

These goals looked achievable with zero interest rates and massive government subsidies. But now, with interest rates at 5%, reduced government incentives, and runaway cost inflation, we’re seeing cracks in the demand story.

The reality is that Net Zero 2050 will not happen.

But before diving into why Net Zero won’t happen, its effects on copper, and why we prefer yellow cake over the red metal, I want to tell you about the Macro Ops Collective.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you want to protect your portfolio in this new market regime, make sure you become a member.

**Enrollment will stay open until Sunday, October 29th at midnight CST.

You can learn more about the Collective and what it can do for your investing here.

Alright, let’s start with Offshore Wind.

Offshore Wind Throwing In The Towel

S&P Global estimates that offshore wind will account for 23% of annual copper demand growth. How does this compare to what’s happening in reality?

Energy companies are backing out of offshore wind projects, citing increased costs, reduced subsidies, and supply chain issues.

One Spanish renewables company even paid $50M to get its offshore wind contract off its books.

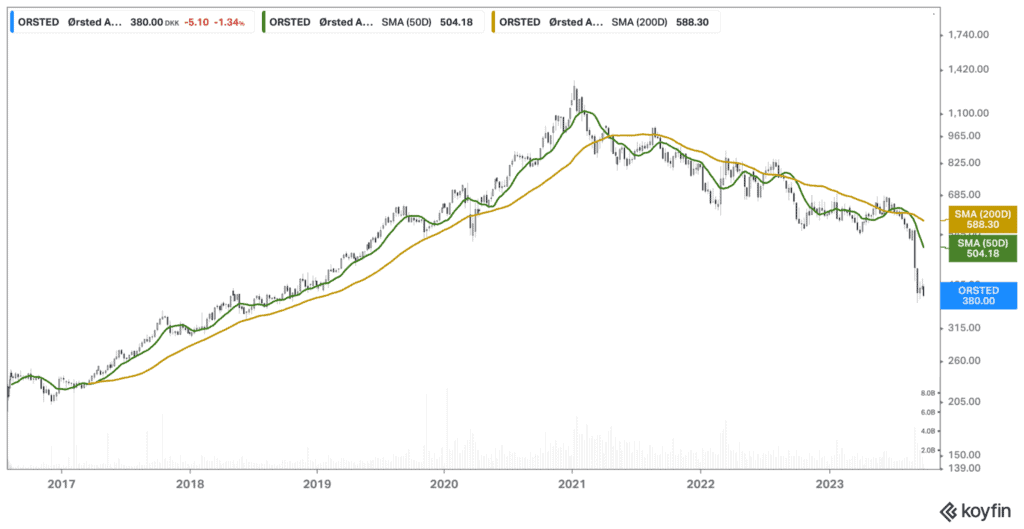

Even the world’s largest offshore wind farm developer, Orsted ($ORSTED), might dump its US offshore farm projects for a $2.1B write-down.

The moral of the story is that life as an offshore wind farm manufacturer isn’t much fun when the government replaces its nipple with a pacifier.

That doesn’t look like an industry that can sustain 23% annual copper demand for over a decade.

This begs the question …

If Not Then … When?

There will never be another time with interest rates so low, government policies so friendly, European weather so favorable, and investor appetites so whetted.

It reminds me of the scene in Dumb and Dumber when a bus of Miss Universe candidates asks Harry and Lloyd to oil them up before a show.

But instead of dropping everything and joining the Tour of a lifetime, offshore wind companies did this …

If offshore wind didn’t succeed in that environment, when will it?? I don’t mean this rhetorically, either. The industry faces structural issues that are only getting worse.

Inflation is here to stay.

Labor shortages will worsen.

And good luck financing deals at anything <8-9%.

The rebuttal, of course, is that governments can do whatever they want. And if they decide offshore is the future, offshore will be the future.

That’s fair.

But say that happens. The problem is that inflation would skyrocket, further exacerbating offshore’s cost problem and leading to more significant financing issues … can you see the reflexive loop here?

The Babe Bus has left the station. And with it, the industry’s hopes of 23% annualized copper demand.

So, if we can’t trust offshore wind copper growth, what about Electric Vehicles? According to S&P Global, EV adoption will account for 14% annualized copper demand growth till 2035.

Unfortunately, the auto industry faces the same issues as offshore wind.

What Happens When The EV Music Stops?

When costs were low and subsidies high, auto giants like Ford, Renault, and BMW pushed heavily for EV adoption. For instance, you couldn’t go two seconds without an EV commercial in last year’s Super Bowl.

This made sense in light of the UK government’s ban on all ICE cars by 2030. With the ban, it wasn’t a stretch to forecast EV adoption driving 8%+ annual copper demand growth.

Unfortunately for Copper Bulls, the town is back that way …

Last week, the UK government pushed its ICE ban to 2035, five years from its original start date.

The auto giants got what they wanted with enough complaining and lobbying dollars. Why were they so scared? See offshore wind.

Between input cost inflation, labor shortages, and chaotic supply chains, producing an EV today is significantly more expensive than a few years ago.

Here’s an example from an FT article (emphasis added) …

“ACEA, which represents EU carmakers including BMW, Volkswagen, and Renault, said on Monday this could cost the bloc’s automakers €4.3bn over the next three years, potentially reducing electric vehicle production by some 480,000 units, the equivalent annual output of two midsized factories. It would also hit UK-based manufacturers that export to the EU.”

Notably, the British Government finally realizes we don’t have enough of the critical metals necessary to make EVs at scale.

We can’t quickly supply the market with more critical minerals (new mine construction takes 10-20+ years from development to production).

In other words, the terminal life/value of ICE cars (and all its subcomponents) is now longer than most anticipated. (Sidenote: There’s a trade to play with this information. But I don’t know what yet. Maybe something around ICE/diesel engines, etc.).

The estimated growth rates from EVs and Battery Adoption (8% and 23%, respectively) won’t happen. So where does that leave us?

A Realistic Map of Copper Demand Sources

The truth is that copper’s “Green Energy” demand sources will undershoot Net Zero 2050’s estimates, potentially by a lot.

Here’s how I’m forecasting copper demand growth going forward.

First, I start with the foundation of copper demand: Electrical wiring, building construction, transportation, industrial machinery, and transmission and generation.

These sources will account for ~22Mt of demand by 2025.

From there, I add 2021’s Transmission and Distribution and Auto and Charging demand from our “Green Energy” projections. Remember, I don’t trust offshore wind and EV adoption growth estimates. I’d rather be surprised on the upside than disappointed on the downside.

According to S&P Global, Transmission and Distribution (T&D) accounted for ~5Mt of demand in 2021, with Auto & Charging adding another 4-5Mt (see below).

That gets us ~31Mt in estimated copper demand by 2025. Consensus forecasts for 2025 supply are around 27Mt.

In other words, we could see a ~4Mt deficit or ~12% of estimated usage by 2025.

Why I Need More Gap

Is a ~4Mt supply deficit enough for me to get excited and buy copper futures/producers? No, it’s not. Especially when you weigh copper against other supply/demand imbalance themes … like Uranium.

The main reason is that a 4Mt deficit doesn’t allow much wiggle room if I’m wrong on demand estimates.

For example, China accounts for 30-40%+ of copper growth, and they’re slowing. Not to mention transitioning from a construction-led to a service-based economy. India is a future growth driver, but they consume less than 3t of copper per 1,000 people. China consumes 16t per 1,000 people.

If we enter a major global recession, I must also assume some contraction in copper’s most significant demand sources (building construction, etc.).

However, I’m by no means a copper bear. I love the long-term setup and believe copper’s supply issues are more severe than most people (want to) believe.

I’m plowing money into a more asymmetric supply/demand imbalance … One with a more robust, predictable demand source mostly agnostic to global recessions or the commodity input price.

Of course, I’m talking uranium.

Yellow Cake Over Red Metal

A great way to measure the magnitude of a commodity thesis is the percentage gap between supply and demand a few years out and your conviction in the drivers of either supply, demand, or both.

I ended the first half of the essay saying that copper’s gap, though at 12%, wasn’t as attractive as uranium, which we own in size, and has significantly more attractive supply/demand drivers.

We wrote a 41-page Uranium Industry Deep Dive for our Collective members, which you can read once you join 🙂

I won’t repeat what I wrote in that report. But I’ll highlight the most critical components of the uranium thesis, namely:

- Supply and demand drivers

- Stickiness of demand

- The magnitude of the future supply/demand gap

The rest of the essay aims to explain why I prefer uranium over copper.

Uranium’s Supply/Demand Drivers

One of the reasons why I like the uranium thesis is that there are only a few supply/demand drivers. Let’s start with the supply side.

Nearly all of the world’s uranium supply comes from ten mine locations, eight countries, and five major mining companies.

On the one hand, this makes supply easy to track. But it also makes it susceptible to severe disruptions. For instance, if Cameco (CCJ) has issues at one of its mines, it could significantly impact global supply.

Copper isn’t like that. Yes, you have a similar country concentration risk with Peru and Chile. But there are thousands of copper producers globally and even more projects in the pipeline.

Uranium also has more geopolitical risks than copper. Most of the world’s uranium comes from Kazakhstan, which has issues with Russia.

Finally, uranium shares the same cost inflation issues as copper (or any mining company), like labor shortages, fuel inflation, and lower grades.

Supply Side Advantage: Uranium

Then there’s the demand side.

We covered copper demand in the first piece, which includes Electrical wiring, building construction, transportation, industrial machinery, and transmission and generation.

We added Transmission & Distribution and Auto & Charging as the only “Green Energy” demand drivers over the next few years.

The most important thing about copper demand is that most demand is CAPEX, not OPEX.

Capital Expenditures are, for the most part, voluntary expenses to improve existing facilities and develop new technologies/products. Think of it as spending more money on the higher end of Maslow’s Hierarchy.

On the other hand, OPEX spending maintains existing infrastructure. It supports the basic needs of society (again, lower-range hierarchy stuff).

Here’s another way to think about it:

- Capex = Netflix/Disney+ subscriptions

- Opex = Mortgage and utility bills

CAPEX-driven demand is bad for commodities because global demand slows massively during economic contractions. People spend less on wants and more on needs.

Uranium is 100% OPEX spend. Nearly 75% of uranium demand comes from utility companies. The utility companies buy uranium to fuel their power plants, which they use to provide baseload power to society.

People still need electricity during recessions.

Moreover, uranium is a fraction of a power plant’s total cost structure, making them somewhat price-agnostic buyers … something copper will never have (mainly due to substitutability from aluminum or silver).

To recap, you have opex-driven demand from a price-agnostic buyer versus capex-driven demand from price/economically sensitive buyers.

Demand Side Advantage: Uranium

That brings us to the last factor … the magnitude of the future supply/demand gap.

Who’s Got The Bigger Gap?

As mentioned earlier, copper will likely have a ~4Mt deficit or 12% of global usage.

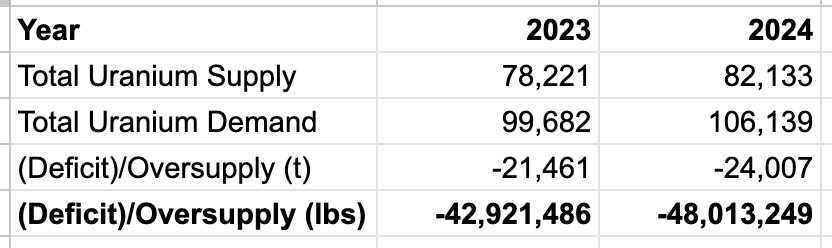

What about uranium? See our internal estimates of the uranium supply/demand deficit from our Uranium Deep Dive …

We estimate a nearly 50Mlb supply deficit by 2024 or ~16% of total global usage.

16% is larger than 12%, but not by a lot. That’s why demand driver conviction is so important.

Over the next 12-18 months, which commodity has a more attractive demand picture? The one whose consumption is primarily tied to economic growth/development and maybe the Green Energy transition? Or the one that’s mission-critical and a small COG in a large, OPEX-driven demand cycle?

We choose the latter. It’s why uranium is our book’s largest position (~15% at cost) and why we’re reducing our copper exposure.

The question at this point becomes what’s the best way to get exposure to uranium in your portfolio. Here’s how we’re thinking about that question.

Generally, you buy junior explorers/miners as part of a barbell approach to commodity investing. You assume higher risk in hopes of higher reward. However, the more I dig into uranium, the more I realize that the best way to play this trade is to be long U.UN.

Our bull thesis on uranium concerns one theme: that spot prices must rise.

We get direct exposure to that thesis through U.UN.

More importantly, we do not need to incur single-stock/single-mine risk to express this bull thesis. Of course, you can point to the junior uranium explorer charts from the last bull cycle and go, “See! This is why you should buy miners!”

There are a couple of issues with that logic.

First, most of those small junior miners are now much larger. The law of large numbers makes an equivalent price movement almost impossible.

Second, investors only had one way to play uranium in the last cycle: through the miners. They didn’t have U.UN, Yellow Cake (YCA), or Uranium Miner ETFs like we do now.

There are more options to gain uranium exposure without idiosyncratic mine risk. Plus, why expose ourselves to all the mining issues like labor shortages, cost inflation, and geopolitical issues if we don’t need to?

Given the supply/demand imbalance over 2024-2025, the risk/reward in U.UN is just as attractive as any single-stock bet when considering idiosyncratic risks.

I know one fund manager that invests in uranium mining companies. And that’s all he does. So, you could commit the next 5-10 years studying the uranium space to find the best mining company only to be rug pulled by government taxes or mine floods.

Or you could buy U.UN, monitor the supply/demand deficit magnitude, and sleep well at night.

I’m still excited about copper’s future supply/demand gap. But as of now, I’d rather buy an asset with opex-driven demand and a price-agnostic buyer than an economically sensitive derivative of global capex spending.

If you enjoyed this post, the names we trade, and how we think about markets, consider joining the Macro Ops Collective.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you want to protect your portfolio in this new market regime, make sure you become a member.

**Enrollment will stay open until Sunday, October 29th at midnight CST.You can learn more about the Collective and what it can do for your investing here.