Insiders Are Bailing Out… [Dirty Dozen]

He that would run his company on visible figures alone will soon have neither company nor visible figures to work with. ~ W. Edwards Deming

In this week’s Dirty Dozen [CHART PACK] we talk about speculators buying the dip in Qs along with that means for this selloff. We then discuss the very high insider sell ratio, look at active fund positioning, walk through Japan fundamentals, and end with an energy play that’s leading to the upside, plus more…

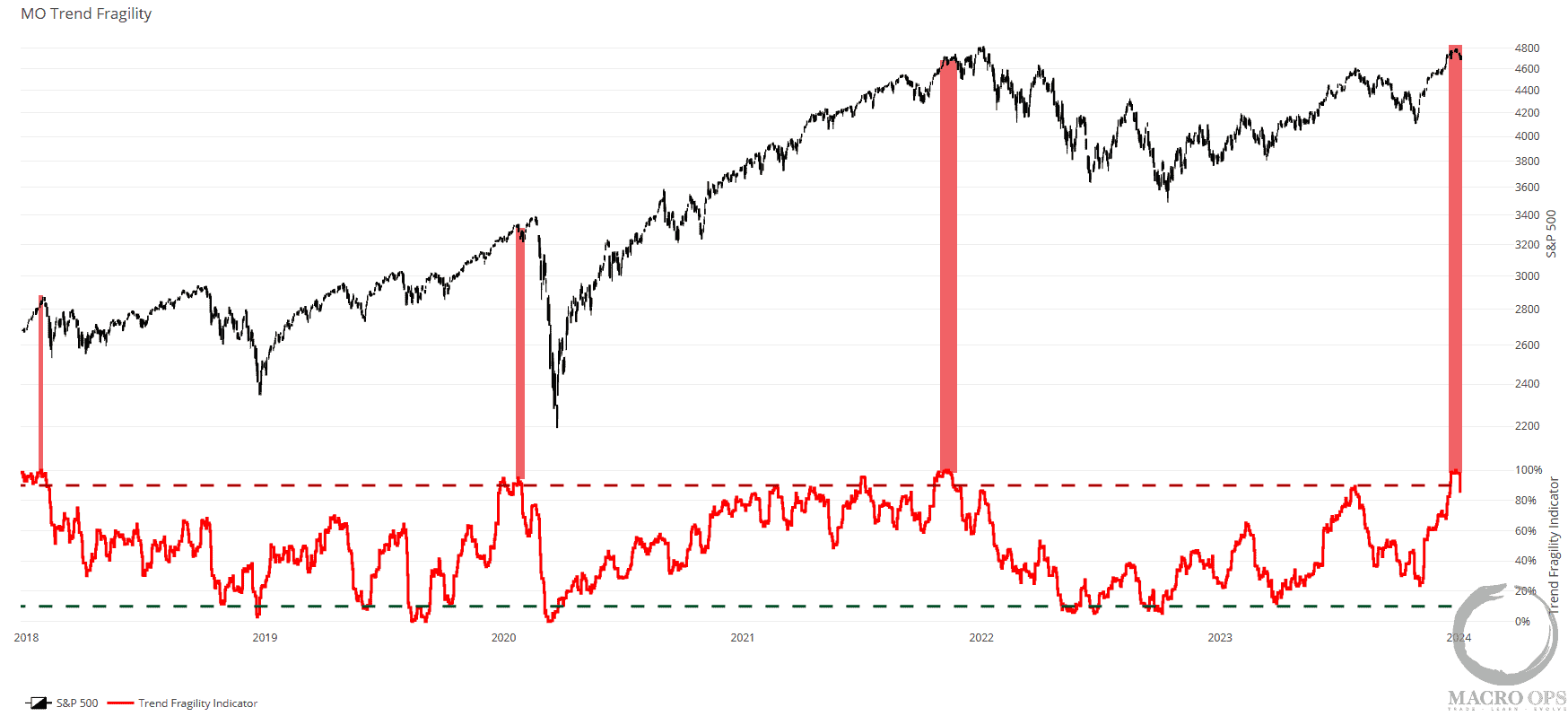

1. Our Trend Fragility indicator maintains its impressive hit rate with the sell signal that was triggered two weeks ago (link here).

2. Large specs added to their longs in Qs last week too, bringing their nominal positioning to 12m+ highs.

This is another sign along with the TF score that we should expect a continued period of chop and volatility with the risks skewed to the downside over the near term, until these hot hands can get shaken out some. My guess is we see the market correct sideways to down for the rest of the month.

3. But like we said the other week, this correction should be viewed as a retrace within a primary uptrend, meaning we’ll see the market continue to new highs once this pullback is done. The reason for this confidence is due to the intensity of this bull thrust, with 9 consecutive weekly bull bars to new all-time highs (Dow weekly chart shown below).

4. Interestingly, corporate insiders have been selling their stock as if they know something. The chart below shows the ratio of insider sales versus buys hitting new 12m highs (chart via @hmeisler).

![]()

5. Here’s BofA’s latest update on active fund positioning. Unsurprisingly, active managers have their highest overweights to the Mag 7 and one of their lowest exposures to value on record.

6. The Mag 7 has been underperforming the SPX for a few months now. We are of the growing conviction that this will be the year that the Mag 7 finally begins to materially underperform the market.

7. We keep beating the drums for select emerging markets, specifically Brazil, Mexico, and Turkey being an additional wildcard but one with considerable upside if the thesis works.

The best time to invest in EM is when you have triple tailwinds in outperforming currencies, bonds, and equities, which is what we currently have in Mexico and Brazil. The chart below from Koyfin shows the strong relative outperformance from EM bonds over the past 6 months.

8. We’ve been talking about the incredibly attractive long-term technical, fundamental, and macro setup in Japan for quite a while now. We may be getting close to another bull run soon. Here’s a weekly chart of the Topix.

9. GMO published a paper over the weekend outlining the fundamental reasons to own Japan. The piece is titled“The Four 4S Behind The Compelling Opportunity In Japan Equities”. Here’s the link and a clip:

We believe Japan is undergoing durable fundamental improvements and lasting change in attitudes toward shareholders. GMO’s 7-Year Asset Class Forecast framework sees Japan small value equities poised to deliver strong absolute returns of 12%, ranking them amongst our highest forecasts. Four “4s” make us particularly excited about small value equities in Japan right now:

- 4% Real Returns due to Fair Valuation: Japan broad equities look about fairly valued and priced to deliver 4% real returns.

- 4 New Initiatives: Four recent policymaker initiatives should provide support for company fundamentals and shareholder returns.

- 4% Alpha from Tilting to Small Value: Active managers who dial into cheap small value stocks stand to capture an additional 4% of returns.

- 4% Tailwind from Cheap Yen: If the yen reverts slowly back to fair value, USD-based investors stand to pick up a 4% tailwind.

10. And according to GMO, small caps are the market to go fishing in… Japanese small caps currently trade at a discount to market that’s in the 15th percentile of their history.

11. Our yield indicator (red line) continues to diverge higher, suggesting that the reversal in bonds isn’t quite done yet.

I’d have more conviction if we saw confirmation from copper/gold (blue) and lumber/gold (green). But the last time I looked small specs were getting quite long 10s, which suggests our yield indicator will probably be proven right.

12. Kodiak Gas Services (KGS) is hitting new all-time highs following its IPO at the start of last summer. KGS provides compression equipment natty transpo for the energy sector.

We’re just starting to dig into this name but are impressed by its relative strength. There’s a VIC write-up on them from back in October that you can find here.

Thanks for reading.