The following is an excerpt from our weekly Market Brief. If you’re interested in learning more about Market Briefs and the Macro Ops Hub, click here.

The Fed is going to hike this Wednesday. They’ve made that clear. But why the complete reversal in tone since their last meeting?

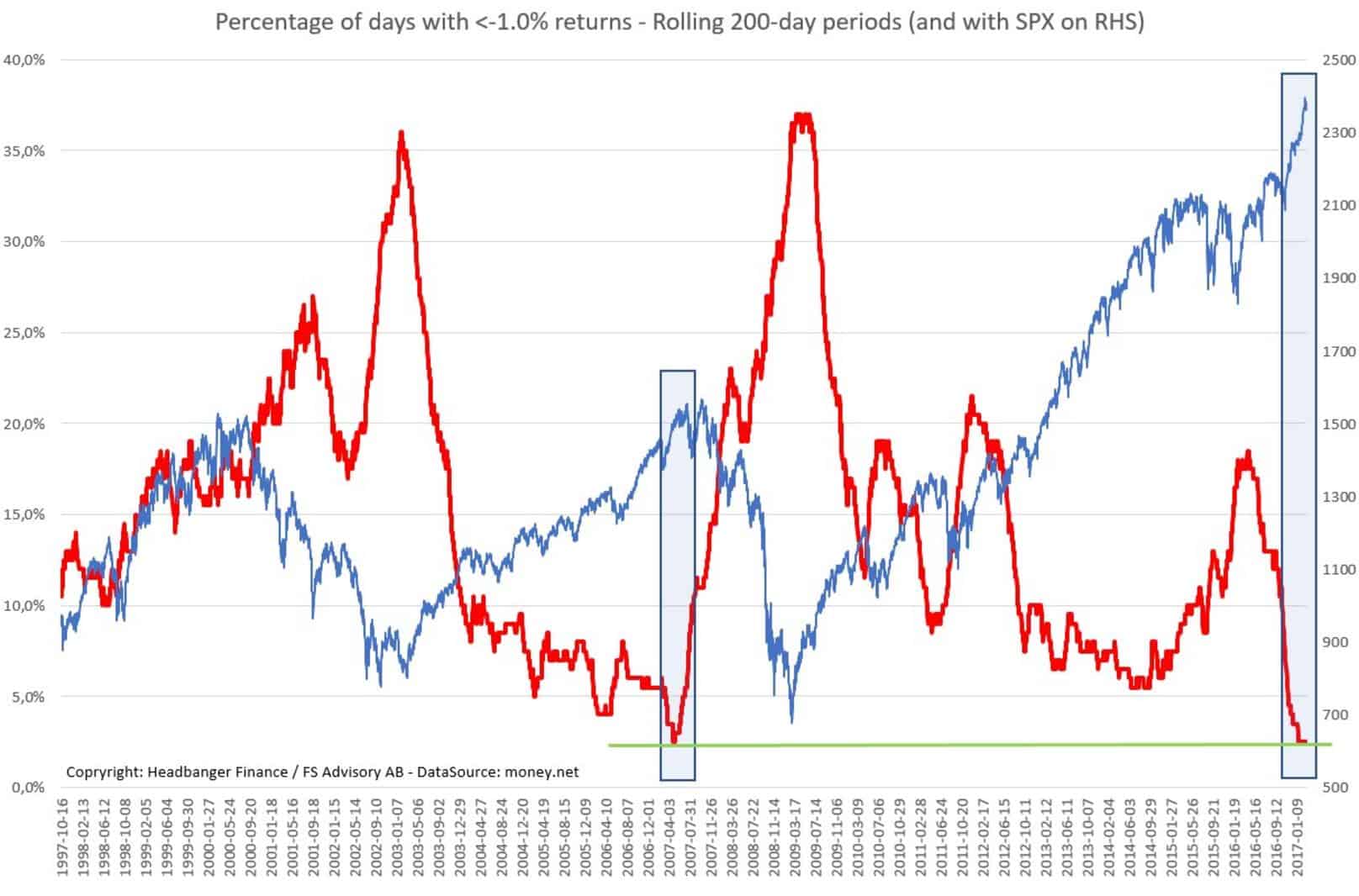

The answer is obviously because of the Fed’s unspoken third mandate — putting caps on bubbles. This is something it’s historically been poor at. But Yellen and team have commented in recent weeks on the market’s seemingly lack of concern over economic and political “uncertainty”.

Charts like the one below are evidence of this:

So the Fed’s gonna hike. But the real question is, do they talk dovish following this week’s hike as has been their modus operandi? Or do they increase their hawkish rhetoric out of fear that the market and expectations are running away from them?

I don’t know, but we’ll find out shortly.

We nailed the breakdown in oil. Our option play in Vol Ops should pay out nicely.

Now we just need to see if oil experiences another v-bottom reversal at its 200-day like it did the last two times, or if the third time’s the charm and she trips off the cliff here.

What happens to oil will have big implications because it’s wagging the tail of credit (see nearly identical chart below). If oil turns lower, then credit will continue lower and we’ll see spreads begin to widen and defaults increase.

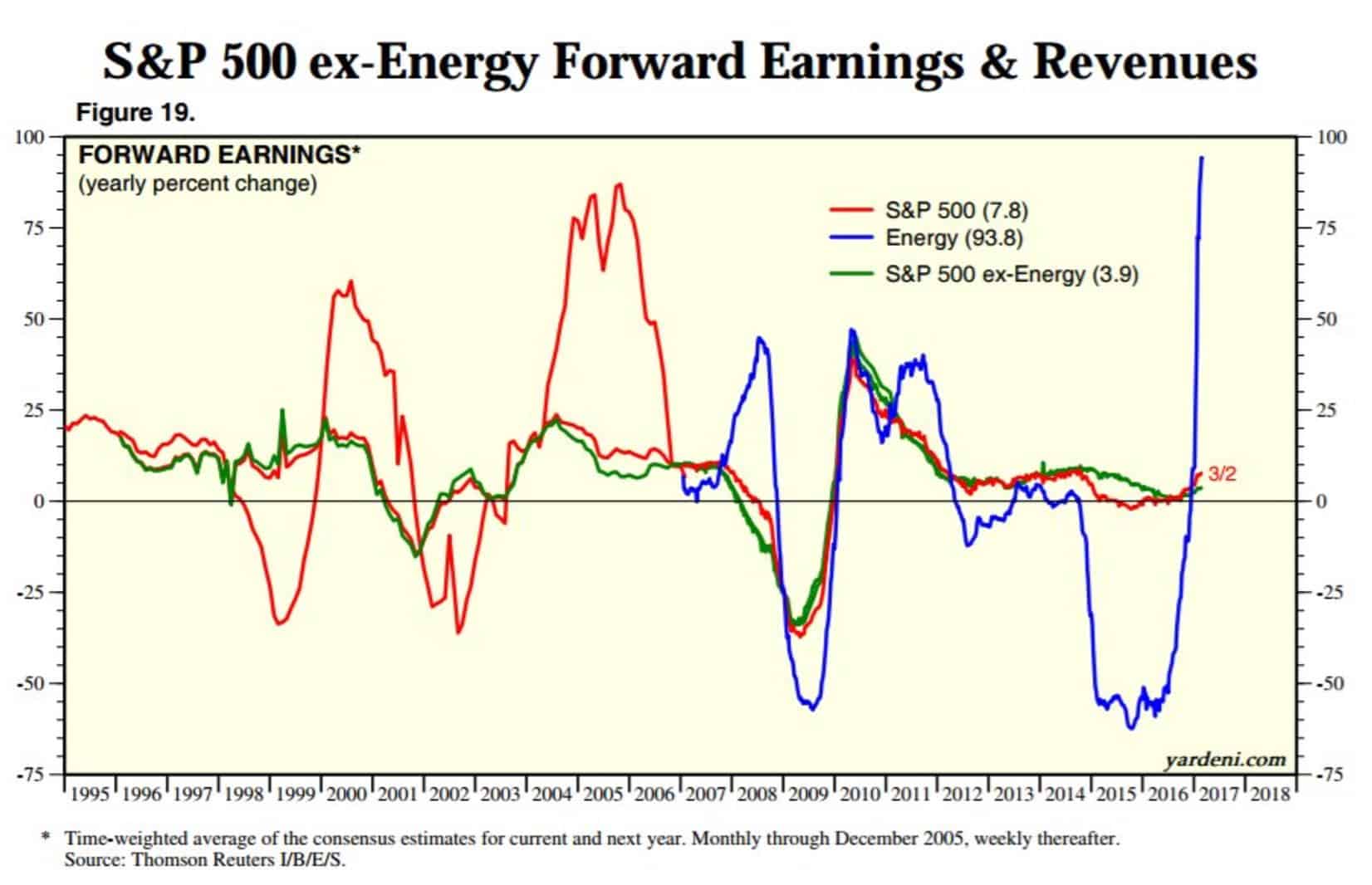

Not to mention what a lower oil price will do to S&P earnings over the coming year. The rebound in oil prices have been a big boon to earnings and revenue growth over the last year. The chart below shows expected forward earnings for the SPX, Energy and SPX ex-energy.

If oil prices roll over from here then expect that blue line to come crashing back down. And the green line showing S&P companies ex-energy doesn’t look a whole lot exciting either.

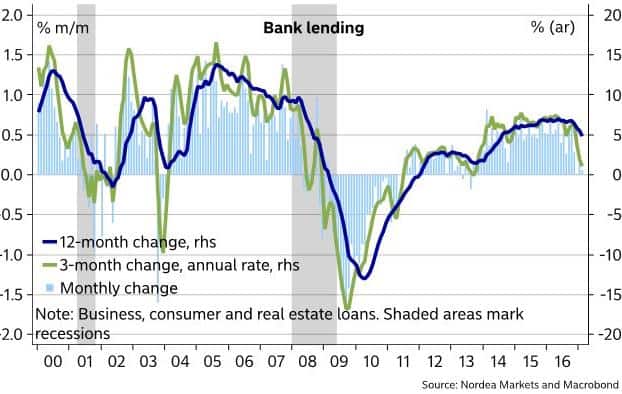

Indicators are pointing South for the credit cycle. The chart below is a prime example of an end of cycle liquidity suck. Falling liquidity = falling demand = falling growth = asset prices adjusting lower.

The 12-month, 3-month and 1- month change in bank lending (an aggregate of business, consumer, and real estate loans) growth is rolling over and looks like might actually start contracting later in the year.

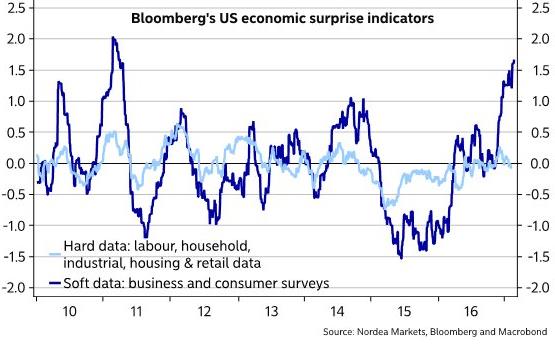

This liquidity tightening is happening all while sentiment and retail participation is markedly picking up. The chart below shows soft data (dark blue) which is various business and consumer sentiment survey data compared to the hard numbers (light blue) which report actual data on the economic state of our country.

Large divergences between exuberantly optimistic soft data and the actual hard numbers as shown in the chart above don’t have a history of working out well for those giddy individuals.

My call last week for a coming market retrace still stands. The divergence between breadth and credit is still there (has actually widened more). I suspect the market levitates for the next few days and starts selling off into the end of the week.

I’m not calling a top here, just a retrace. The highs haven’t been made on this market yet. It has some more room to run. But expect things to start getting a lot more bumpy…

The above is an excerpt from our weekly Market Brief. If you’re interested in learning more about Market Briefs and the Macro Ops Hub, click here.