RAIL designs, manufactures, and sells railcars and railcar components for transporting bulk commodities and containerized freight products in the United States and Mexico.

According to its website, the company offers a range of railcars, including open-top hoppers, mill gondola cars, intermodal and non-intermodal flat cars, coal cars, bulk commodity cars, covered hopper cars, coil steel cars, boxcars, woodchip hoppers, aluminum vehicle carriers, and articulated bulk container railcars.

It’s a boring business with a bombed-out chart that 99% of investors have overlooked.

But RAIL is the picture-perfect example of our Trifecta Lens approach to trading markets. And it’s what makes Macro Ops different from any investor/trader you read about online.

The Trifecta Lens approach combines Technicals, Fundamentals, and Sentiment to give us the best odds of success. Each of these must align before we take a position. Funny enough, when we ignore the Trifecta Lens criteria, we lose the most money.

We found RAIL on a technical breakout, which led us to do further research to find bullish-inflecting fundamentals that would send the stock price higher. Finally, we bought RAIL when sentiment was at extreme lows. Nobody has discussed the idea in years, and you’ll barely see it mentioned on Twitter/X.

How do you get access to these ideas and this framework of trading markets?

Enter the Macro Ops Collective.

The Collective is our full-kit soup-to-nuts service that provides research, theory, and a worldwide killer community of dedicated traders, investors, and fund managers.

We’ve been told that there’s nothing else like it on the web. If you’d like to tackle markets with our group (whom I should note has been having a great year in markets), just click the button below and sign up.

As a Collective member, you’ll learn all about our Trifecta Lens approach to markets. The one that allows us to confidently trade any market, any instrument, in any market regime.

This is just one example of our numerous trades this year, allowing us to outperform the market since 2020.

If the Collective sounds like a group you want to call home, join us at the link below. We’re running an extended Labor Day sale, so spots will fill up fast.

Back to the write-up and a preview of our Trifecta Lens Framework and position sizing philosophy, starting with Technicals …

Technicals: Left-For-Dead Chart w/ Monthly Breakout

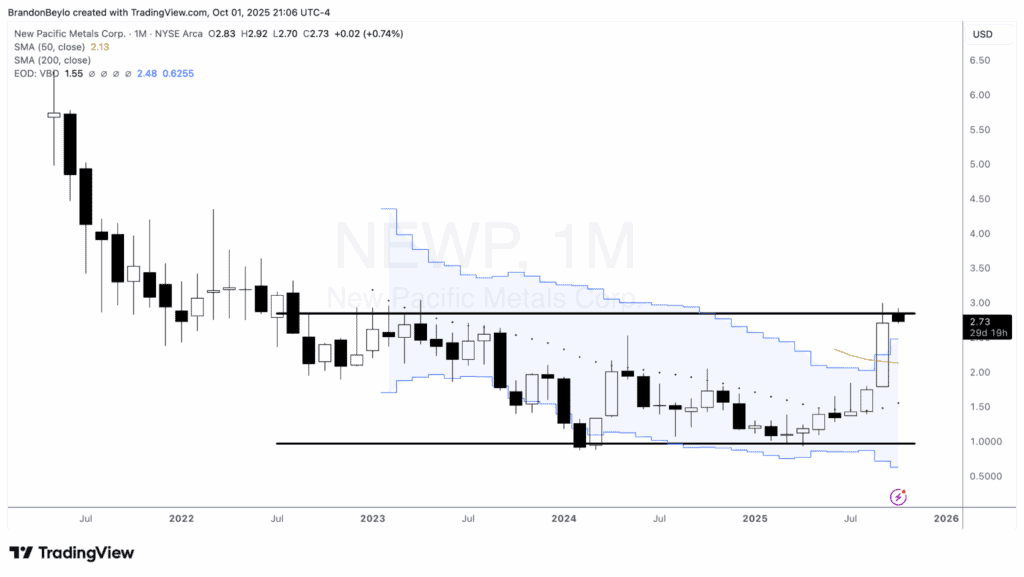

Check out the RAIL monthly chart below.

The stock has been down 69% since its inception. In other words, anyone who bought this stock and held it for any period has lost money.

However, the chart is inflecting this month, with August posting a massive bull breakout bar above its upper Bollinger band. A monthly close around this price would confirm the trend change.

Sentiment: Nobody Wants To Touch This Stock

Nobody is looking at this stock.

The latest ValueInvestorsClub write-up is from 2014. Seeking Alpha hasn’t written about the company since 2023.

One analyst covers the company, and two people talk about it on Twitter.

On the surface, RAIL is a low-margin manufacturer in a highly cyclical industry with a history of operating losses and financing troubles.

The company lost money on an EBITDA basis every year from 2017 to 2022. Quantitative value-based screens won’t catch this name.

Still interested?

Fundamentals: Inflecting More Than The Share Price

The company is inflecting on all aspects of its business – revenues, margins, orders, backlog, and cash flow (see below).

RAIL spent the past four years investing in its new Castanos Mexican manufacturing facility. This led to annual operating losses and -$20K in gross profit per railcar sold.

Today, RAIL generates $6.6K in EBITDA per railcar sold at 60% production capacity with minimal capex requirements (management guides 0.5% – 0.7% of revenues).

Since 2021, the company has gained market share in North America by growing orders by 9.4% annually versus the industry average of 0.2%, representing ~10% of the NA market (see below).

Here’s CEO Nick Randal on the industry outlook.

What’s interesting about RAIL – and the broader railcar industry – is how RAIL competes and differentiates itself from its competitors.

RAIL doesn’t compete with railcar lessors (think of equipment rental companies). Instead, it partners with them to build the railcars they need.

More companies are shifting towards the lease business. One Tegus transcript highlighted that the railcar manufacturing industry had consolidated from ~24 suppliers a decade ago to 4-6 today.

Leasing railcars is a better business model—higher margins, higher cash flows, and less capital-intensive.

But someone still needs to make the railcars.

RAIL says, “You guys do the leasing thing. We’ll keep making these railcars and selling them to you.”

The company generates 10-12% gross margins and 5% EBITDA margins as a manufacturer. But if you’re one of the only games in town …

So, to recap, you have a business with inflecting revenues, margins, backlog, and profits … and it’s yours for ~0.2x NTM sales and 5x EBITDA.

Earnings Power Inflection: New Tank Orders & Capacity Expansion

There are two ways RAIL can increase earnings power over the next 2-3 years:

- Penetrate higher-margin product segments like tank cars/tank conversion

- Increase capacity at the Castanos manufacturing facility

This quarter, the company announced a major tank car conversion order. This will allow it to capture some of the 8,000 tank car market, which currently has a 0% market share.

Tank car orders are higher-margin products. One Tegus interview mentioned gross margins of 20-30%.

More tank car/conversion orders RAIL means a higher consolidated gross margin.

RAIL can also increase earnings by expanding production capacity at its Castanos facility. At 60% capacity, the company generated $6.6K in EBITDA per railcar.

A higher capacity allows RAIL to spread more fixed costs across more railcars, improving per-railcar EBITDA margins and profits.

For example, increasing capacity from 60% to 70% would translate into $7,700 in EBITDA per railcar. 80% capacity gets us $8,800 in EBITDA per railcar.

How do you generate higher capacity? More orders.

Railcar deliveries should average ~40,000 units/year over the next few years, supported by a healthy railcar fleet and storage percentage (see below).

Now that we understand the company’s earnings drivers let’s construct a back-of-the-envelop model for the next three years.

Let’s assume RAIL expands production capacity from 4,500 railcars delivered in 2024 to 5,500 by 2026. During that time, the company produced more high-margin tank railcars, which increased the gross profit margin from 11% to 13%.

Finally, we assume capacity improvements add ~200bps to the EBITDA margin from 6.5% to 8.5%.

By 2026, RAIL could generate $700M+ in annual revenue, $93M in gross profit, and $60M+ in EBITDA.

The current market cap is ~$110M.

Before we extrapolate investment returns under the model, I want to discuss the company’s outstanding warrants and potential dilution.

RAIL has ~19M common shares outstanding, ~2M shares worth of employee options and warrants at the current stock price ($5.50), and another 13.81M shares worth of convertible warrants.

In other words, the company could increase its share count from 19M to 36M depending on strike prices, etc. (see image below).

This is where the red flags appear. According to the company’s latest 10-K, these public convertible warrants have an exercise price of $0.01/share (see below).

In other words, it means RAIL receives almost no cash for the additional dilution.

Let’s construct a fully diluted enterprise value with 36M shares outstanding.

Current assets include:

- $37M in cash

- $16M in receivables

- $65M in inventory (sale-ready railcars)

Debt includes:

- $84M in preferred stock (sits senior to ordinary shares)

So, the updated cap table would look like this.

This dramatically changes our expected returns and, thus, the attractiveness of the investment (see below).

FCF yields declined from ~14% in 2024 to 23% in 2026, which isn’t bad, but it’s not the face value of 48% under the non-dilutive assumption.

Conclusion: Wait and See + A Lesson Learned

The good news is that the company could take its free cash flow, pay off the preferred stock, and refinance to stunt some warrant dilution.

Management can improve the capital structure and in turn, the investment opportunity.

I’m fine holding our current “invest-then-investigate” position and waiting to see what they do.

We risked 75bps of actual capital at a $3/share stop. If things turn south, we’ll jam stops and exit this position with a <25bps loss.

This is the power of buying starter positions. I learned about a new industry and did the necessary research to add to our position should we see improvements in the capital structure.

One last thing… our port has been chopping around the mid 30% to mid 40% year-to-date returns for the past two months. It’s a grind but that’s part of the game. But the above setup — should it play out as we think it will — is going to create some big opportunities going into the end of year. And we think these are potentially nut making trends in the work.

Also… we’re running our yearly labor day sale this week where we’re offering 20% off membership to our Collective. For more info on what the Collective is and what exactly it offers, click here. We only run this sale once a year so if you’ve been sitting on the fence, now might be a good time to join the group. Don’t hesitate to shoot me any Qs. Cheers!