“Never forget the 6-foot-tall man who drowned crossing the stream that was 5 feet deep on average.” – Howard Marks

If Donald Trump were a stock, he would be Carvana (CVNA).

Bulls believe the stock is worth >$600/share. The bears think it’s a zero. Somewhere in between lies the truth about the company, its value, and its survivability over the next 12-18 months.

Two weeks ago, I recorded a Twitter Spaces (turned podcast) trying to answer that golden question: Will Carvana Survive?

As expected, both bulls and bears dug trenches, sharpened their theses, and went to war. I agreed with various points from both sides but left the Spaces as I began; without a clear answer.

CVNA Twitter Spaces is in the spotlight for this week’s 3 Big Things (3BT).

3BT distills my podcast episodes into bite-sized summaries. This week we’ll summarize:

- Bulls Say (Common threads in Bull theses, valuations, probabilities of survival)

- Bears Say (Common threads in Bear theses, what kills CVNA, management distrust)

- Markets Say (Stock and bond price embedded expectations)

It’s different from our usual 3BT, but I hope you enjoy it.

CVNA is many things. It’s loved and hated. Despised and cherished. However, we can all agree that it’s complex.

This post reduces CVNA’s complexity down to what matters most … Will It Survive?

Let’s get after it.

Bulls Say: Market Share Expansion, Margin Flexibility, and Customer Experience

CVNA bull @WolfofMStreet started the discussion with a few high-level bull arguments.

First, Wolf suggests, “The appetite of equity markets to continue funding something that could be a long term better mousetrap is going to remain very high.”

In other words, yes, things are terrible for CVNA today. But, the market eventually rewards better mousetrap businesses with more money (via capital raises or debt financing). Wolf’s reasoning for this includes a long-term secular decline in the cost of capital and a superior customer experience (based on convenience and selection).

While I agree that CVNA is building a better mousetrap, I don’t think equity markets care. Better mousetrap or not, investors want cash flow. They want survivability. CVNA doesn’t guarantee that the way something like CarMax or CVS can.

Wolf then explained that CVNA offers an incredible risk-adjusted return at today’s prices. You risk ~$24 to make ~$500 (where Wolf thinks CVNA could trade).

Even if you believe CVNA is a terminal zero, the probability-adjusted return profile screams “buy the damn thing.”

How do you get to $500/share? Wolf employs a back-of-the-envelope TAM calculation assuming the following:

40M cars sold annually * 10% CVNA Market Share = 4M cars sold via CVNA

Assuming a 10% market share and ~$5,000 gross profit/unit, CVNA would generate $20B in gross profit at 4M annual car transactions.

Richard Chu (@Richard_Chu97) joined the conversation and added several other bull thesis points. The points were:

- CVNA has enough liquidity to last another two years

- CVNA’s fraud claims are overexaggerated as management remains aligned with shareholders

- Used car prices will not drop sharply over the next 12-18 months

I pressed Richard on the 1-2 things that would crush his bull thesis. He responded with three “ifs”:

- If CVNA cannot fix its logistics issues (home-grown system versus outsourced transportation management system)

- If used car prices fall off a cliff (resulting in massive inventory write-downs)

- If auto loan default rates increase (substantial losses in financing business)

The final bull pitch came from 11111111 (@oneoneone_rsr), where he explained how CVNA can survive the next 12-18 months with existing liquidity. He notes that CVNA has ~$4B in liquidity. The company burned $600M in cash last quarter, $400M of which @oneoneone_rsr deems “excess spending.”

Here’s the rub. CVNA has ~1 year of runway at its “bloated” $600M quarterly cash burn. That $600M includes ~$2,000/unit in excess SG&A spending.

@oneoneone_rsr also explained that lower car prices might benefit CVNA, as it increases consumer demand/transaction volume and affordability.

Now on the topic of bankruptcy. @oneoneone_rsr admits that CVNA could “easily go bankrupt” if exogenous events like ABS market struggles and/or a sharp decline in car prices occur.

However – and this is the critical part of the thesis – the combined probability of each event occurring to topple CVNA’s house of cards is low. For example, the odds of flipping a coin and landing on heads is 0.5. The odds of landing on heads three consecutive times is 0.125.

CVNA Bull Thesis TL;DR:

- The company has enough cash to last ~1 year, assuming its worst-ever burn rate

- Used car prices won’t fall off a cliff

- CVNA is building the best mousetrap, which should allow it to tap financial markets at more attractive rates/terms

- Default rates won’t dramatically increase as consumers need cars to drive to work

Bears Say: Debt Burden, Auto Cyclicality, Competition, and Management Issues

We didn’t get too many CVNA bears in the Spaces. Which surprised me because of how loud they rant on Twitter. However, we did get some. Let’s start with Uncle Buck (@EcJayhawk).

Uncle Buck came out swinging (emphasis added, paraphrased):

“Despite the share price declines, CVNA’s valuation still isn’t super attractive. It trades at a 50% premium to Carmax (KMX) and hasn’t growth units sequentially.”

Maybe CVNA earns a 50% premium over KMX if it’s growing like a weed. But according to Buck, it’s not.

Moreover, Buck mentions CVNA’s marketing spend and the putrid returns generated for new transactions (emphasis added, paraphrased):

“Carvana spent $155M in marketing in Q1 to grow units by 15,000 in Q2. They’re spending $1,200/unit on acquisition cost yet they’re not growing like they were.”

Buck also thinks CVNA’s long-term 10% market share is “unsubstantiated.” Maybe it is, but what is a reasonable market share assumption if CVNA survives and achieves its long-term goals?

Buck then explained CVNA’s aging inventory and how it could lead to an “inventory event” (i.e., massive write-downs). Which was one of Richard Chu’s primary concerns.

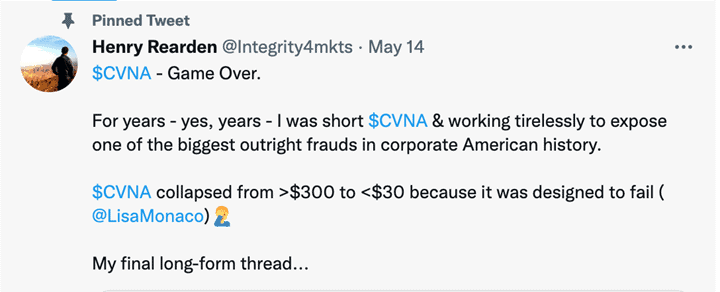

Finally, Henry Rearden (@Integrity4mkts) joined the discussion and provided his bear take. Henry went viral for his CVNA bear thesis, which you can read here.

Here’s how Henry described his Variant Perception (emphasis added, paraphrased):

“Our variant perception was that CVNA was a bankruptcy remote entity to its parent company, Drive Time. CVNA would funnel positive economics to the parent company (Drive Time) while leaving growing liabilities and losses for the bankruptcy remote, Carvana.”

Rearden reminded listeners that his CVNA short thesis has “more or less played out” with the stock down 90%+ from its all-time highs.

A frequent rebuttal to Rearden’s bear thesis was that CVNA was the “Amazon of Used Car Retailing.” While it sounds nice, it’s not true. AMZN generated cash as it grew. Its customers paid AMZN money upfront, and AMZN would use that cash to buy books (or other things) to ship to customers.

CVNA is the opposite of AMZN. The company requires absurd amounts of money to start, and most of its customers require loan financing to buy a car. This means CVNA absorbs most of the cost of purchasing a vehicle, hoping its customers pay over time.

With its current liquidity, Rearden thinks CVNA cannot make it through the 5’ average river. Moreover, he believes the company’s deal with Apollo Asset Management was a “prepackaged bankruptcy.”

Markets Say: Company Heading For Bankruptcy In 12-18 Months

Do you want to know a secret? Nobody on the Twitter Spaces expected to change their minds. In fact, bulls and bears dug deeper in their stances.

But what does the Market say about CVNA?

CVNA trades at ~$25/share for a $2.6B market cap and ~$8.7B Enterprise Value. The stock is down 90%+ from its all-time highs. The equity is priced for bankruptcy within the next 12-18 months.

What about the bonds?

CVNA’s bonds are yielding nearly 16% (check out the image from Henry Rearden below):

The bond market also thinks CVNA is going to zero.

Everyone thinks the 6’ man won’t make it across the 5’ deep river. Even if they’re right, the risk-reward at current prices isn’t worth the bet.

Sure, CVNA might not survive. Heck, maybe there’s a 95% chance that they die. But what’s the expected value of that 5% chance they survive? What’s the payout? And is it worth a small, deep-OTM options-type position?

I learned a lot from this Twitter Spaces. But I left without a clear direction on CVNA’s future. My base case is that “we’ll see what happens” remains the best play, and if we do anything at Macro Ops, it’ll be a small DOTM-like equity bet (risking ~1% of our capital).

CVNA is a lot of things. It’s loved and hated. Despised and cherished. But most of all, it’s complicated.

Wrapping Up: Where To Learn More

Thanks for reading, and I hope you learned something. Check out these resources if you want to learn more about Carvana or the bull/bear cases: