***This excerpt from a Market Note sent to Collective members last Thursday summarizes our risk-on thesis that we’ve been pushing for the past month. Enrollment to our Collective runs till Sunday. If you’d like to join, click the link below and get after it. Don’t hesitate to shoot me any Qs!**

Join The Collective

The TL;DR for those with short attention spans is: Buy… we’re back in risk-on.

Okay, here’s a quick summary of my current market thoughts, starting with the FOMC yesterday.

They went with the 50. This is what we were expecting. It’s also the right move.

The simple argument is that policy rates were too restrictive, as evidenced by the historically wide FF vs 2yr yield spread. And with a slowing labor market, the Fed was at risk of falling behind the curve. They needed to bring rates closer to neutral. And that’s what they started doing yesterday.

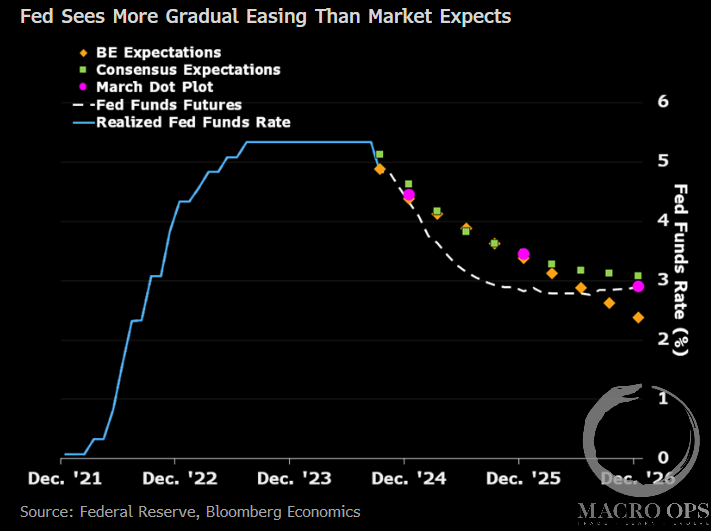

They also communicated that this type of “jumbo cut” won’t be the norm and that this is a preemptive move to stabilize the labor market. The median participant expects the FF rate to be at 4.4% by the end of 24’ and 3.4% at eoy 25’. So, 100bps cuts this year (versus 25bps in the June dot plot).

This is slightly more hawkish than the market’s pricing going into the meeting. I don’t put much weight on their dots, and so I wouldn’t read too much into this.

Look, this was a positive meeting for the Bulls. Powell and team acknowledged that they’ve shifted their focus from inflation to labor weakness. This is good as it means they’re not overanchoring to the recent past and getting caught fighting the last war. They’ll be responsive to any further softening in the labor data and won’t about-face too quickly should we get a stall in inflation (which we will soon due to base effects).

I’ve been seeing a lot of hysterical takes out there from macro pundits, saying all types of nonsense (see tweet below). These are best ignored.

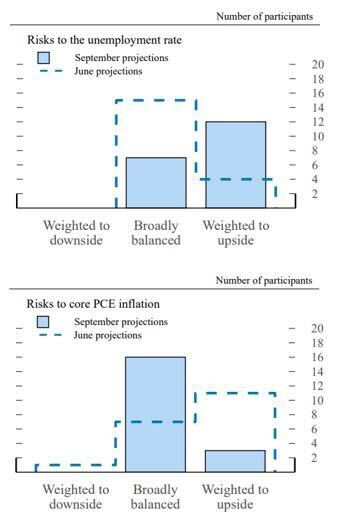

Regarding the dots, @JBar hit the nail on the head in our Slack, writing:

Been chewing on the Fed meeting and this is what I’ve got to say back to the “hawkish dots” bad for market crowd. You can never take an SEP at face value, but that’s especially true for this one. The key to this SEP is the clear shift in the balance of risks charts away from inflation to the unemployment rate showing the committee much more aligned on the risks than the path. Therefore the fed’s reaction function is likely to be dramatically understated by the face value of the baseline projections.

I’m also seeing many argue that cuts are bearish because it means a recession is coming or some such thing. Honestly, I don’t know. There’s lots of brain damage on the twitters, so be careful out there.

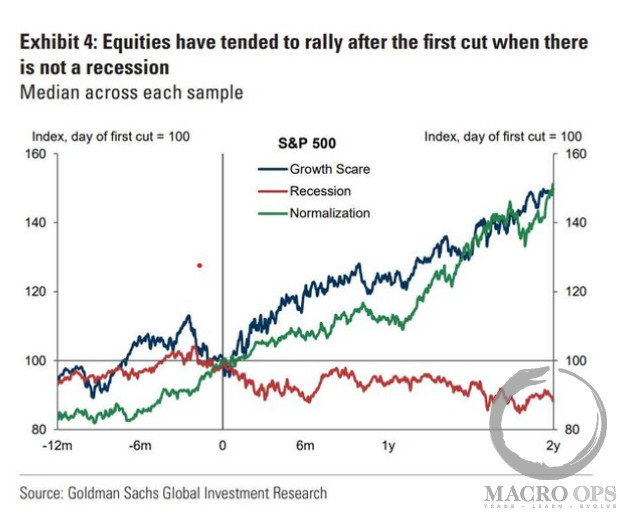

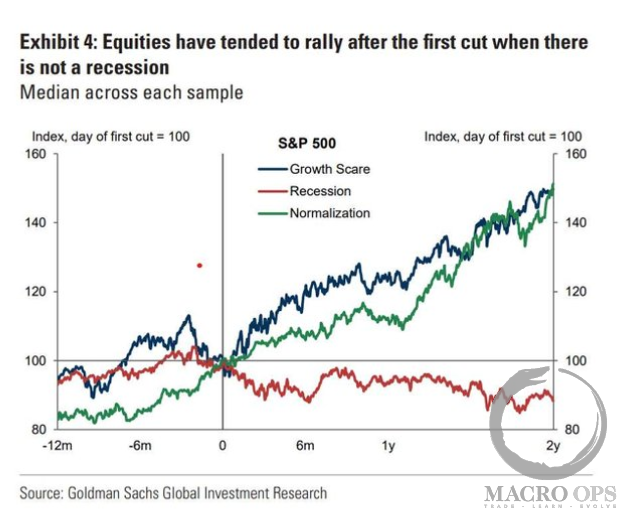

A recession is unlikely, especially now that the Fed is bringing rates closer to neutral. Historically, this has been very bullish for risk assets. See the GS chart below. Barring an external shock, we likely follow the blue line.

The SPX jumped to new all-time highs today, breaking out of its two-month sideways range. This is bullish.

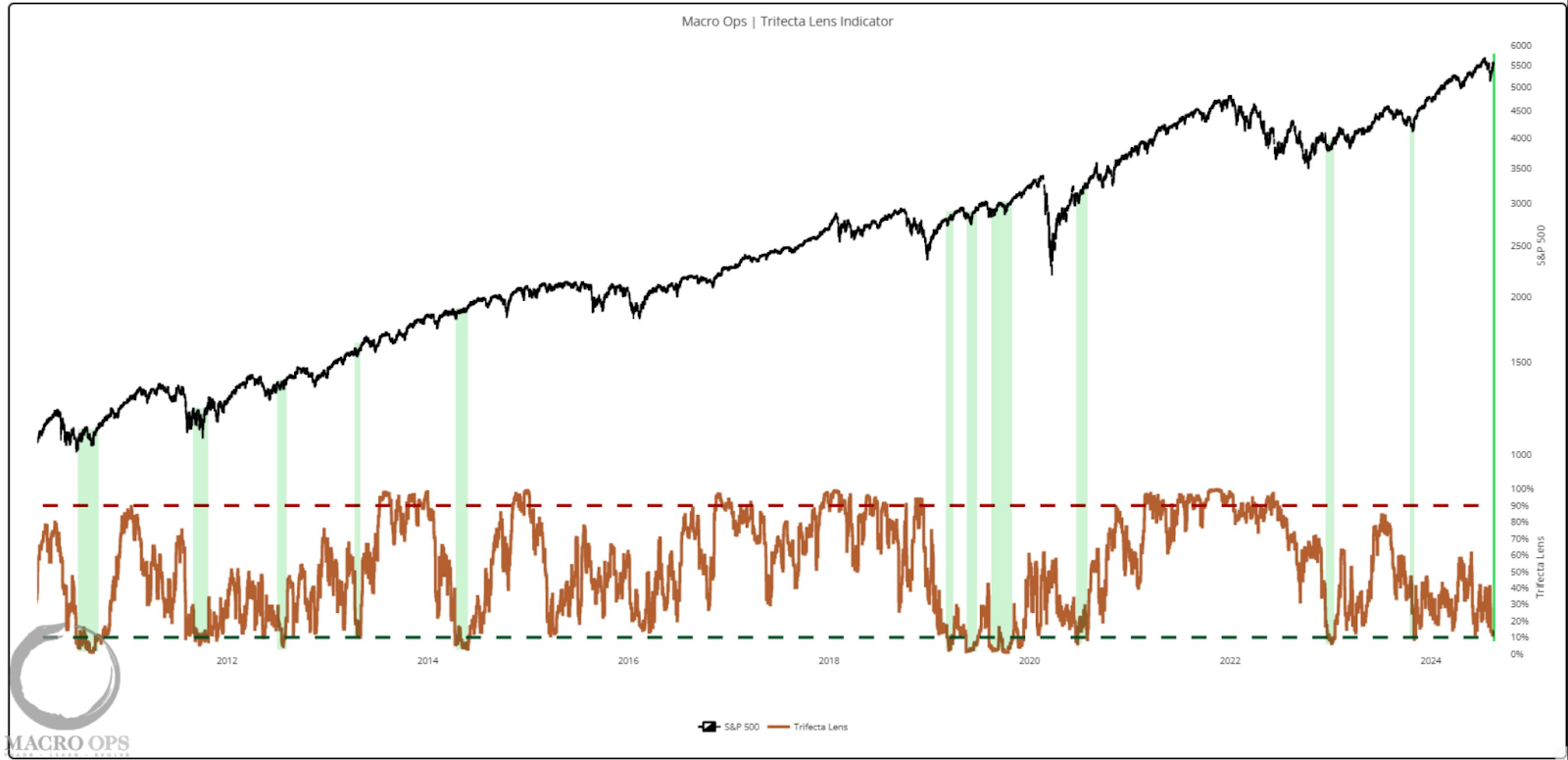

Remember, this new high follows the major buy signal from our long-term Trifecta Lens indicator just a few weeks ago.

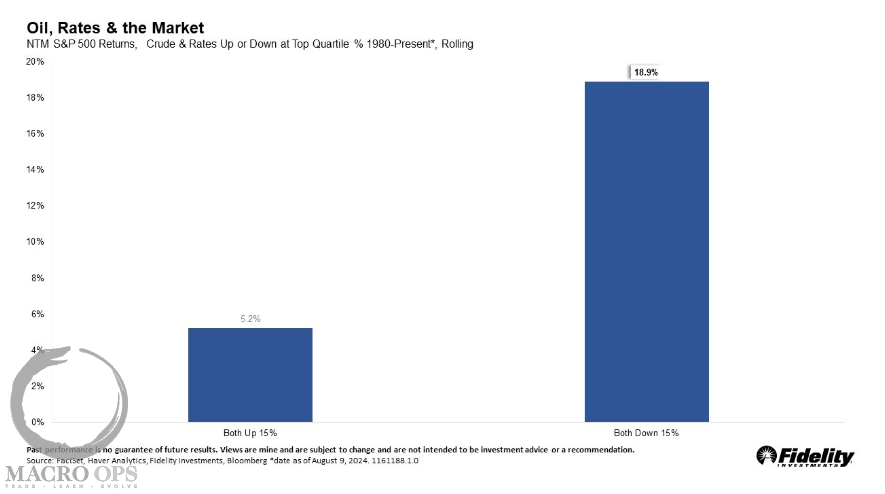

This is in addition to the double tailwinds from the fall in oil and yields over the past few months (via Fidelity).

“Oil and rates are now down double-digit amounts over the last twelve months, something that hasn’t happened since 2020. While the move is a bottom quartile event for both, the two moving together at this pace (both up and down) happens only 10% of the time.

“The signal itself is somewhat asymmetrical: oil and rates going up more than 15% isn’t necessarily bad for stocks (they return 5% the year following), but both going down is quite good, historically offering almost 20% returns. That illustrates the magnitude of the tailwind we’re currently seeing. Importantly, those strong returns happen even though both oil and rates do tend to bounce back after falling this much.”

For the past few weeks, we’ve been pointing out that breadth remains strong and at levels/trend direction that historically led to more upside follow-through.

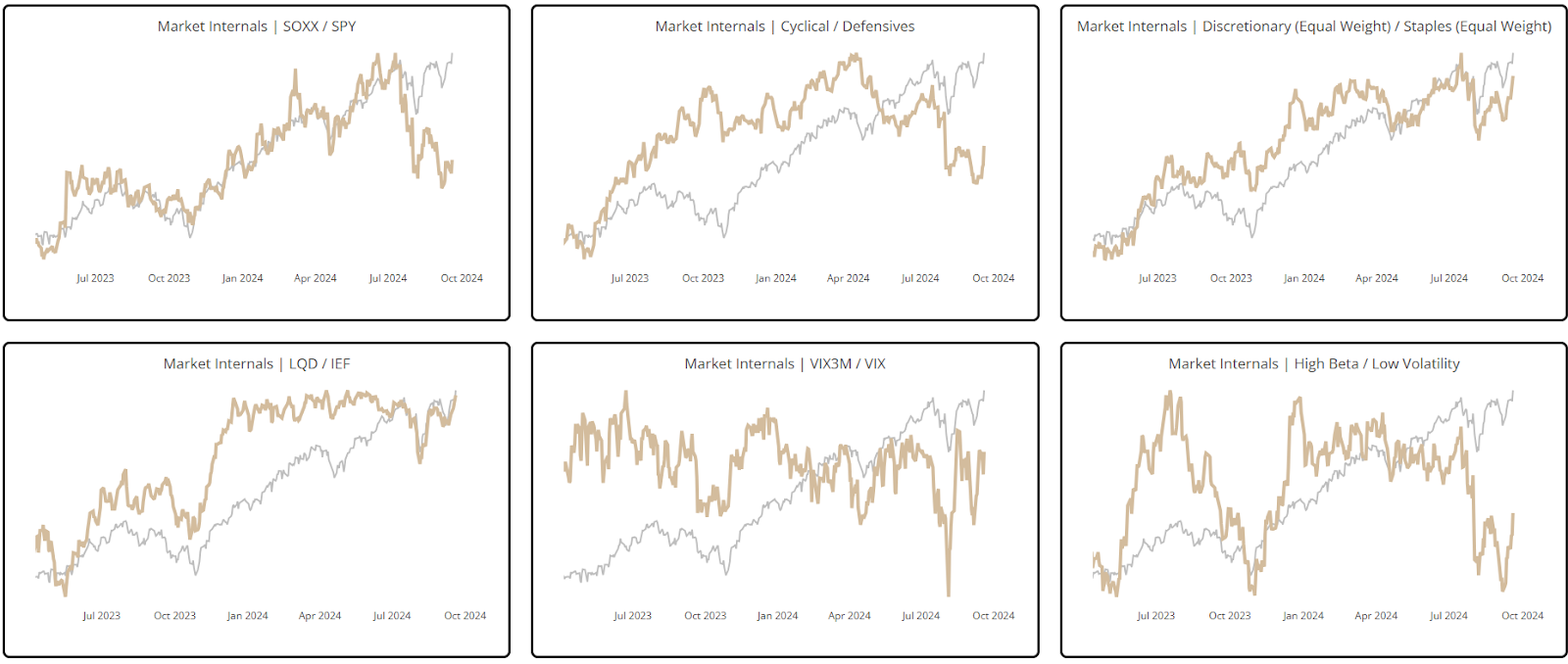

Weakness in market internals has been our biggest concern over the short-term path. But even here, we’re seeing these begin to inflect higher.

LQD/IEF (bottom left) is back near year-to-date highs. High vs Low Beta, along with Discretionary vs Staples, are trending up.

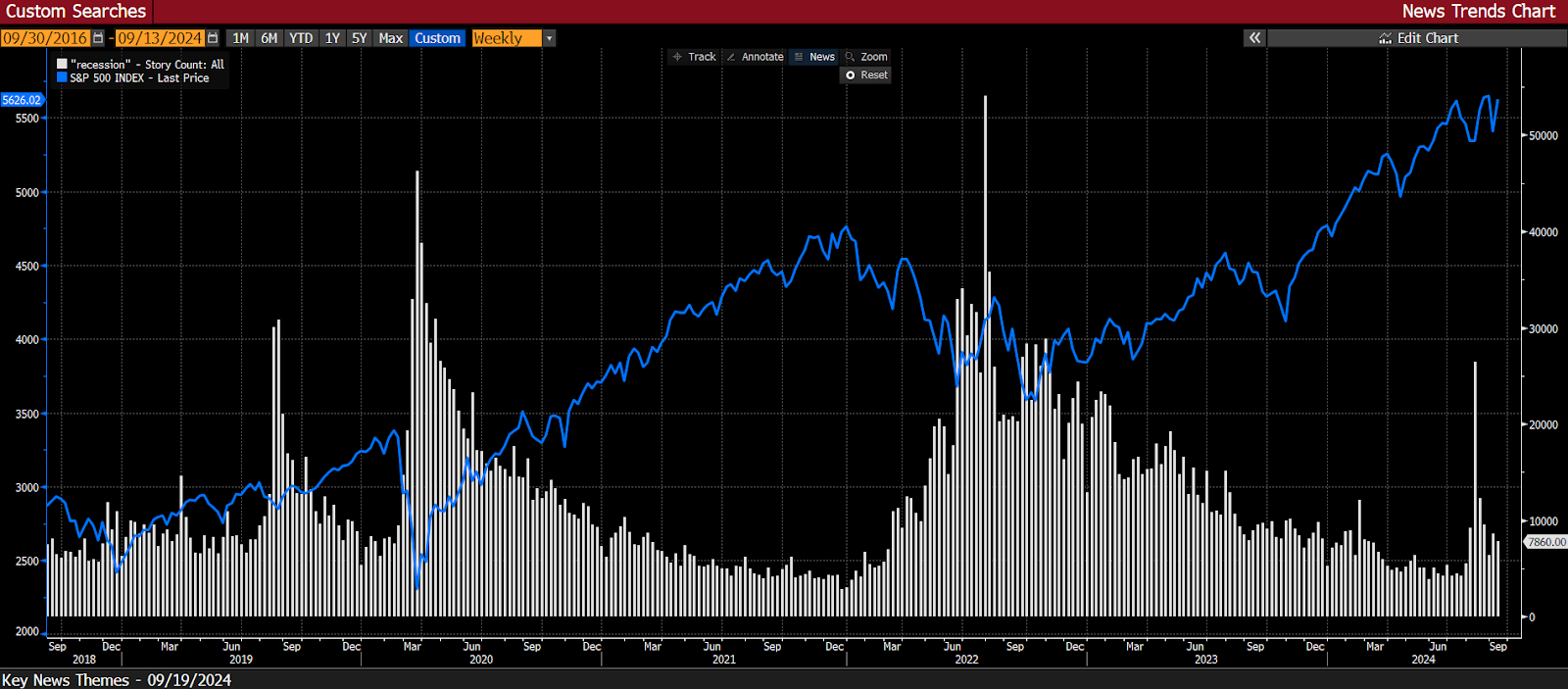

Our Trend Fragility score is neutral. BofA’s Bull & Bear indicator is neutral. Mentions of “recession” recently have spiked to their highest level since lat 22’ (white bars). This is with the market at/near highs. All of this tells us that there’s plenty of idle cash to drive this trend higher…

This is a bullish backdrop. So we’re starting to add back risk. Jump into the Slack to see our latest portfolio moves. Ignore the incoherent, bearish babbling out there. There’s a lot of it. And it’s bad for your brain cells but good for those of us who are long and buying.

I’ll be out with more soon. Just wanted to get this out there to share what I was seeing.