The following is an excerpt from our Macro Intelligence Report (MIR). If you’d like to learn more about the MIR, click here.

On May 22nd 2010, computer programmer Laszlo Hanyecz ordered two Papa John’s pizzas. They were Hawaiian style. He paid $60,000,000. According to Laszlo, they were your typical Papa John’s, and tasted only “okay…”

In 2013, a Brit by the name of James Howells accidentally threw away a laptop worth over $45,000,000. He realized what he’d done a few months later and went down to the landfill to dig through mountains of garbage to no avail. James says he’s now “at the point where it’s either laugh about it or cry about it… Why aren’t I out there with a shovel now? I think I’m just resigned to never being able to find it.”

In 2009, a Norwegian named Christopher Koch made a $27 investment on a whim. The investment “annoyed” his then girlfriend who thought it was a waste of money. Today, his $27 investment is worth $30,000,000. Chris now owns property in Toyen, the wealthiest neighborhood in Oslo. He has a new girlfriend.

You’re probably wondering what I’m talking about. Who are these guys that would drop millions on a pizza or somehow forget about buku money stored on a laptop?

The common thread here is bitcoin — the first and most popular cryptocurrency.

I was having some fun with the numbers. You see, Laszlo didn’t really spend $60M on two Papa John’s pizzas. He paid $25 for them, but in bitcoins. 10,000 of them to be exact. It was the first recorded merchant transaction in cryptocurrencies ever.

But the price of bitcoins has gone up a bit since then.

A single bitcoin today is now worth over $6,000. Those 10,000 bitcoins that amounted to only $25 in 2010 are now worth over $60M. So in hindsight, it was an expensive pizza.

Bitcoin has had an annualized rate of return of 715% since then. As far as returns go, that’s pretty darn good…

If you would have bought $10,000 worth of bitcoin in 2009, when our lucky Norwegian bought his, your “investment” would now be worth roughly $1,200,000,000. Granted, you would have had to sit through horrendous volatility and numerous drawdowns in the +80% range, but still….

Alright, I’m done pointing at how extremely rich we all could have been if we’d just bought a couple pizzas worth of bitcoins a few years ago. We didn’t… we bought actual pizzas instead… so let’s wipe our tears and move on.

In this month’s MIR, we’re going to talk about bitcoin, cryptos, blockchains and all that good stuff.

There’s a lot of hype, one could even say a religious zealotry around cryptocurrencies’ future. It’s not hard to understand why. Bitcoin is up over 500% again this year and many of the other cryptocurrencies are up even more. Returns like that tend to create a fervent following.

Today our Macro Ops team will cut through the crypto zealotry to see what’s actually going on in the blockchain market. We’ll briefly talk about what Bitcoin is, where it came from, and how the market is likely to evolve going forward.

The Beginning… How Bitcoin Was Born

The Bitcoin origin story is a fascinating one.

It was first developed in 2009 by a group of computer programmers. They built it according to a cryptographic architecture created by a pseudonymous author who goes by the name of Satoshi Nakamoto.

The public still doesn’t know who Satoshi is. It’s believed that he actually might be a group of people and not an individual.

Either way, he (they?) are the largest holders of bitcoin after mining it in the early days. They possess more than 1 million of the coins. This puts Satoshi at 247 on the Forbes wealthy list.

Fun fact: There’s a conspiracy — which is probably true — that the NSA uncovered who the actual Satoshi is. When bitcoin was created, the US intelligence community became concerned that it was the product of a rival state like Russia or North Korea. The government was worried it could be weaponized someday against the US, perhaps by upsetting the dollar as the world’s reserve currency.

So the theory goes that the NSA used stylometry, which is the study of written language, in conjunction with their billions upon billions of data points to compare things written by Satoshi to things written by everybody else throughout the world. And the word is… they got a match.

Anyways, here’s how the original Satoshi Nakamoto white paper starts (you can read the whole paper here):

Commerce on the Internet has come to rely almost exclusively on financial institutions serving as trusted third parties to process electronic payments. While the system works well enough for most transactions, it still suffers from the inherent weaknesses of the trust based model. Completely non-reversible transactions are not really possible, since financial institutions cannot avoid mediating disputes. The cost of mediation increases transaction costs, limiting the minimum practical transaction size and cutting off the possibility for small casual transactions, and there is a broader cost in the loss of ability to make nonreversible payments for nonreversible services. With the possibility of reversal, the need for trust spreads. Merchants must be wary of their customers, hassling them for more information than they would otherwise need. A certain percentage of fraud is accepted as unavoidable. These costs and payment uncertainties can be avoided in person by using physical currency, but no mechanism exists to make payments over a communications channel without a trusted party.

What is needed is an electronic payment system based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party. Transactions that are computationally impractical to reverse would protect sellers from fraud, and routine escrow mechanisms could easily be implemented to protect buyers. In this paper, we propose a solution to the double-spending problem using a peer-to-peer distributed timestamp server to generate computational proof of the chronological order of transactions. The system is secure as long as honest nodes collectively control more CPU power than any cooperating group of attacker nodes.

The problem being solved here is a very important one in computer science. It’s called the Byzantine Generals Problem or BGP.

Here’s how BGP is explained: “[Imagine] a group of generals of the Byzantine army camped with their troops around an enemy city. Communicating only by messenger, the generals must agree upon a common battle plan. However, one or more of them may be traitors, who will try to confuse the others. The problem is to find an algorithm to ensure that the loyal generals will reach agreement.”

Silicon Valley VC Marc Andreessen explains the importance of this here:

More generally, the B.G.P. poses the question of how to establish trust between otherwise unrelated parties over an untrusted network like the Internet.

The practical consequence of solving this problem is that Bitcoin gives us, for the first time, a way for one Internet user to transfer a unique piece of digital property to another Internet user, such that the transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken place, and nobody can challenge the legitimacy of the transfer. The consequences of this breakthrough are hard to overstate.

Bitcoin is a digital bearer instrument. It is a way to exchange money or assets between parties with no pre-existing trust: A string of numbers is sent over email or text message in the simplest case. The sender doesn’t need to know or trust the receiver or vice versa. Related, there are no chargebacks – this is the part that is literally like cash – if you have the money or the asset, you can pay with it; if you don’t, you can’t. This is brand new. This has never existed in digital form before.

Marc Andreessen is a smart guy. He, along with many other tech geeks, are excited about what the mysterious Satoshi created.

We should make a quick and important distinction here.

There’s a difference between bitcoin and Bitcoin. Bitcoin, with a capital B, refers to the cryptographic protocol of the network, otherwise known as the blockchain.

Blockchain is the digital ledger that uses the cryptographic protocol proposed by Satoshi to solve the Byzantine Generals Problem — basically, the tech to help with our internet trust issues.

While bitcoin, small b, refers to bitcoin the currency. This is the token that’s connected to the Bitcoin’s blockchain network and which bitcoiners transact in. It’s also often used as a blanket term for cryptocurrencies in general.

There are now over 1,000 different cryptocurrencies that are similar, yet different, to bitcoin with a small b. This list is growing every day.

Summary:

- Bitcoin was developed from a cryptographic proof that was written by a pseudonymous person or persons who go by the name Satoshi Nakamoto.

- It was developed to solve the Byzantine Generals Problem of how to establish trust over an untrusted network like the internet, where transacting parties don’t know who they’re transacting with.

- Bitcoin does this through the creation of a digital ledger (the Blockchain) where two parties can exchange a digital asset in a safe and secured way to the extent that nobody can challenge the validity of the transfer.

- Bitcoins have gone up A LOT since they were created 8 years ago.

The Blockchain: A Revolutionary Technology

I suggest you spend five minutes and watch this quick YouTube video explaining Bitcoin (link here).

Here’s a quick description of Blockchain via Joseph Pham from Quora.

If you understand the concept of a blockchain, you will have heard people (especially in enterprise) talk about distributed ledger. It describes a technology that uses a write once, read only “database” system that is bound by cryptographic verification, and bound through a series of “blocks” (batches of data / datasets) that are subsequently verified into a “chain” sequence of linked batches over time. This characteristic is what gives the technology the name “blockchain”. Systems that spread / make copies of these blockchains available across a network are often referred to as distributed ledgers.

You can make a blockchain without distributing it, but it might not be as practical and useful for the real world applications you might consider with blockchains.

Bitcoin is just one configuration of blockchain technology, which integrates certain blockchain technology with innovative monetary incentives, social economics and cryptography. The innovative monetary incentive is to have a self verifying money supply – the bitcoins – which are basically entries in the ledger, that are determined mathematically, through solving a complex cryptographic puzzle (hashing), that must reach consensus (peer validation) and encodes a specific reward schedule (approximately every 10 minutes) and total supply of bitcoins (21 million).

A bitcoin is basically just a token value on a ledger (like in game gold and coin values in video games), that are created based on a set of system rules. There are a lot of Bitcoin based and bitcoin derived blockchain applications (using the Bitcoin open source data repository). These are usually referred to as Cryptocurrencies, as Bitcoin was designed to operate as an e-currency system.

I hope I’m not losing you. Stay with me, we’ll get through this tech talk soon enough.

Just to sum up, a blockchain is a digital ledger that encodes every transaction on its system forever. It uses cryptography to ensure the validity of these ledger entries. It’s basically a one-way street where once entries are encoded, it’s nearly impossible to hack or alter them.

I’ve heard the analogy used that each block of transactions in the chain is like a mosquito encased in amber — Jurassic Park style — and every time crypto miners authenticate a transaction and approve the entire blockchain, the amber gets thicker and thicker around the transaction. Meaning, the longer it lives on the blockchain, the more permanent it becomes; and more difficult (or impossible) to alter.

The blockchain can be distributed or not.

In Bitcoins case, and many of the other cryptocurrencies, this digital ledger is distributed across the world. The benefit of this is that no one entity has power over the network and the data is extremely safe and robust since it’s copied all across the globe. Many servers can be wiped out but the data (the Blockchain) will survive.

The bitcoins, or the crypto tokens, are used as an incentive system for miners on the network.

These digital miners use lots of computing power to solve the cryptographic puzzles (called hashing) that’s needed to encode the bitcoin transactions and maintain the integrity of the blockchain. The network works off a consensus. Once a majority of the miners agree on the answer to a hash, the attached transaction then gets recorded to the blockchain forever.

The Brookings Institute calls the blockchain “a foundational technology, like TCP/IP, which enables the internet. And much like the internet in the late 1990s, we don’t know exactly how the Blockchain will evolve, but evolve it will.”

That seems to be the broad consensus amongst technologists regarding blockchain’s potential — it’s revolutionary and will have as sizable impact as the internet itself. But nobody is quite sure exactly how, yet.

The reason is partly because the use cases for blockchain appear to be nearly limitless. Here’s an excerpt from a report by BofA on the subject.

To be frank, it’s difficult for us to think of a large industry where there is no applicability of a blockchain, given the technology’s ability to reduce data storage costs and prevent tampering. After all, blockchain at its core is just a way to store and access data. Startups, trials and proof-of-concepts are abundant in a myriad of industries. Blockchain technology could make tracking and managing digital identities more secure and efficient. A distributed ledger could aid online voting, cutting down on voter fraud. In financial services, the technology could ease payments and transfers; smart contracts could improve trade settlements. Smart contracts on the blockchain are being used to shake up prediction markets. In the music industry, the blockchain can be used to solve licensing issues: Artists, including English singer-songwriter Imogen Heap, have released music directly to fans via blockchain platforms.

Companies ranging from Walmart to Maersk are now using the tech to better track and manage their supply chains. A number of banks and brokerages like BNY Mellon are using it to record transactions.

It’s a safe assumption to say that blockchain is revolutionary and is here to stay. But like the internet in the early 90’s, we don’t know exactly how it will revolutionize things. And again, like the internet, it will probably take a decade or two at least for the tech to mature and dramatically add value.

Now that we’ve got that out of the way, what about the value in cryptocurrencies. Is there any?

What are they worth? Is it a bubble or is this just the beginnings of the largest bull market in history?

Summary:

- Blockchains are the cryptographic technology underlying cryptocurrencies.

- There’s a broad consensus that this technology is revolutionary and will have far and wide-ranging impacts on many areas of the economy; similar to the internet.

- But like the internet in the 90’s it’s still early days for this technology and nobody is quite sure how it will evolve.

The video below explains more about blockchain’s potential:

Valuing Cryptos: Zeros Or Heros?

To value something we have to first define what it is and what it isn’t. And in the case of cryptocurrencies’, this is not exactly easy.

Let’s start with the obvious. Bitcoins, ethereum, Litecoins, and the hundreds of other crypto tokens are typically thought of as currencies, as their names imply.

But what makes a currency? And do these crypto tokens check the mark?

A currency is measured by how well it functions as two things:

- Medium of Exchange: Currencies exist to make transactional commerce possible. This means that the currency needs to be accessible, transportable, and fungible in that it’s accepted by large amounts of buyers and sellers as legal tender.

- Store of Value: Currencies have to act as a reasonable store of value. Meaning, buyers and sellers need to feel comfortable keeping a certain amount of their wealth in it, knowing it will retain its purchasing power.

Let’s start with cryptos as a medium of exchange. We’re going to focus on bitcoin, since with a market cap of $100B, it’s the most popular of all the cryptocurrencies.

Here’s NYU Professor Aswath Damodaran on bitcoin as a medium of exchange:

The weakest link in crypto currencies has been their failure to make deeper inroads as mediums of exchange or as stores of value. Using Bitcoin, to illustrate, it is disappointing that so few retailers still accept it as payment for goods and services. Even the much hyped successes, such as Overstock and Microsoft accepting Bitcoin is illusory, since they do so on limited items, and only with an intermediary who converts the bitcoin into US dollars for them. I certainly would not embark on a long or short trip away from home today, with just bitcoins in my pocket, nor would I be willing to convert all of my liquid savings into bitcoin or any other cryptocurrency. Would you?

There are a number of reasons why bitcoin has failed to make large inroads as a medium of exchange. One reason is that as the tech stands now, it’s a costly and timely transaction process compared to the available alternatives.

Here’s BofA again:

The problem with bitcoin as a peer to peer payment system is that it’s expensive, relative to conventional alternatives. This comes from the mining process. Mining isn’t a zero sum game. The economics of mining are pretty simple. There is a fixed reward per block mined. At present, each block generates 12.5BTC. So, each block mined produces in Dollars around 12.5*bitcoin/dollar rate. At present, this is around $60k per block. This is a function of the bitcoin price. There are roughly 2000 transactions in a block, give or take. This implies that around $30 of bitcoin are created per transaction at present. Economically, we would regard this as a cost of the transaction, although this is not how people always view it.

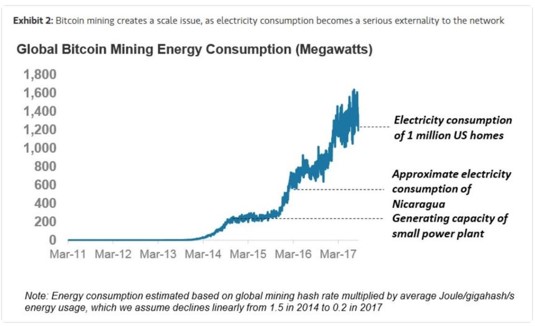

Miners need to be paid because the cost of mining (of applying CPU to blockchain hashing) is becoming prohibitively expensive. It requires enormous and increasing amounts of energy. The chart below demonstrates such:

The electricity being used to mine bitcoin is now equivalent to the amount it would take to power over 1 million US homes!

Or to put it another way, the total energy consumption of the world’s bitcoin mining activities is more than 40 times that required to power the entire Visa network. The annual energy consumption is equivalent to 13,239,916 barrels of oil!

Not only are the costs of transacting and running the network absurd, but the speed at which transactions are processed are extremely slow. BofA lays out the problem:

To illustrate, Visa’s payment system processes 2,000 transactions per second, on average, and can handle up to 56,000 per second, if needed. Assuming similar transaction handling capabilities at other large payment schemes such MasterCard, UnionPay, AliPay etc, total digital payment transaction volume in the retail space can be an order of magnitude higher than the aforementioned 2,000 transactions per second. Assuming 20,000 retail transactions are processed every second, it would take about 100 minutes for one second’s worth of transactions to be recorded on the bitcoin blockchain.

Lastly, due to the astronomical rise of bitcoin and other cryptos over the last few years, the tokens have drawn quite a bit of attention. This has created a speculative fever where the tokens are not being bought for their value, or as a means to transact, but rather as a gambling vehicle used to bet on further price gains.

It’s a momentum driven market where everybody’s chasing returns. And that creates an issue because people don’t want to be like Laszlo Hanyecz and spend their bitcoins on a stupid Hawaiian pizza when those bitcoins could be worth many multiples of what they are today.

This creates a conundrum for cryptos. As Aswath Damodaran puts it, “It remains an unpleasant reality that what makes crypto currencies so attractive to traders (the wild swings in price, the unpredictability, the excitement) make them unacceptable to transactors.”

So bitcoin fails (currently) to meet the requirements of a proper medium of exchange.

What about store of value? Are cryptos a fiat currency similar to the US dollar, as many crypto fans proclaim?

Here’s economist Brad deLong’s take:

Underpinning the value of gold is that if all else fails you can use it to make pretty things. Underpinning the value of the dollar is a combination of (a) the fact that you can use them to pay your taxes to the U.S. government, and (b) that the Federal Reserve is a potential dollar sink and has promised to buy them back and extinguish them if their real value starts to sink at (much) more than 2% / year (yes, I know).

Placing a ceiling on the value of gold is mining technology, and the prospect that if its price gets out of whack for long on the upside a great deal more of it will be created. Placing a ceiling on the value of the dollar is the Federal Reserve’s role as actual dollar source, and its commitment not to allow deflation to happen.

Placing a ceiling on the value of bitcoins is computer technology and the form of the hash function… until the limit of 21 million bitcoins is reached. Placing a floor on the value of bitcoins is… what, exactly?

Bitcoins lack the essential qualities to make it a viable medium of exchange and store of value. Hence they can’t and shouldn’t be thought of as currencies or valued as such.

The things that make bitcoin a libertarian’s wet dream such as its decentralized nature and the fact that no one has control over the system, also means that it doesn’t have any true intrinsic value.

Its value is based completely off of people’s beliefs… and more importantly, people’s beliefs about other people’s beliefs.

Crypto fans call this the network effect — which is a term used to describe companies whose values increase the more people use their products, like Facebook. But this is a limp comparison.

Network effects when applied to tech companies are important because they lead to greater earnings power and value creation — the more people use a social network, the more others want to join, and the more advertisers will pay for access to the network and so on.

Real network effects actually create more value for the owners of the company and users of the product.

Bitcoin doesn’t sell anything and doesn’t produce any cash flows. It’s a non-currency that doesn’t quite work as a medium of exchange or a store of value.

It’s “value” is based purely off the beliefs of those who buy it. And this belief is that bitcoin is valuable because other people think it’s valuable. “If I buy it now, I’ll be able to profit at a later date by selling to somebody else”.

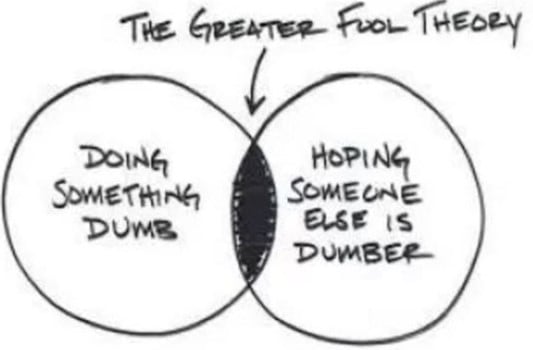

In trading parlance, this is called “Greater Fool Theory” or GFT.

Wikipedia explains GFT as:

The price of an object is not determined not by its intrinsic value, but rather by irrational beliefs and expectations of market participants. A price can be justified by a rational buyer under the belief that another party is willing to pay an even higher price. In other words, one may pay a price that seems “foolishly” high because one may rationally have the expectation that the item can be resold to a “greater fool later.”

The Oracle of Omaha, Warren Buffett, agrees.

He calls bitcoin a bubble, stating “You can’t value bitcoin because it’s not a value-producing asset”. But “people get excited from big price movements, and Wall Street accommodates” making bitcoin a “real bubble in that sort of thing”.

Maybe bitcoin should then be thought of as equity in a pre-revenue biotech startup. A startup with no leadership (it’s decentralized), no product yet of intrinsic value, and a growing number of nearly identical competitors entering the market every single day.

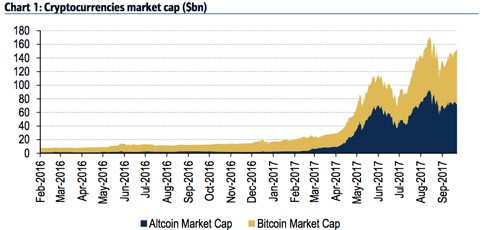

But the shares of the 1,000+ various cryptocurrencies have a total market cap of $176B and growing. New shares are being issued every single day. Many, some, or maybe none, will eventually create intrinsic value somehow… but nobody knows exactly how quite yet.

A better comparison of how to think about bitcoin’s value might be trading cards (think Magic or Pokemon) or in-game artifacts like a flaming sword in World of Warcraft (I don’t know if the flaming sword is a thing but let’s pretend it is).

Unlike a pre-revenue startup that may produce actual value someday, trading cards and in-game artifacts only have value because they have devoted fans and there’s a false scarcity of these objects injected by their makers.

Neither of these have intrinsic value of any sort, but they have a price that fluctuates according to their popularity. So yeah, that’s a better comparison. Bitcoins are like a $6,000 Pikachu card.

Do you want to buy some bitcoin now?

Summary:

- Bitcoin is neither a good medium of exchange or a good store of value, making it a terrible currency

- Bitcoin is “valued” purely through its popularity and Greater Fool Theory — making it more similar to a Pokemon card than a real currency

Here’s a quick video explaining how difficult it is to value Bitcoin:

My Take On Investing In Bitcoin

As a long-term investor, I wouldn’t touch any of these with a ten foot pole even if my arch nemesis — you know who you are — was holding.

It’s a total crapshoot and gamble. This market is purely speculative at this point.

But since I am speculator, would I trade it?

Hell yeah, why not?

Traders love this type of positive volatility. And bitcoins have all the right ingredients to drive this trend even higher. It’s really the perfect “asset” for creating a frenzied mania along the likes of the Tulip and South Sea bubbles.

These ingredients are:

- It’s impossible to value: Anybody who tries is lying to you and themselves. And this is great, because when something has no intrinsic value, it can be either zero or infinity or somewhere in between since there’s absolutely nothing reliable to gauge it off of.

- Greater Fool Theory: It’s value relies entirely on what the other fool is willing to pay for it. That’s it and that’s the only thing you need to analyze in this market when making buy and sell decisions.

- It’s a compelling and complex story and humans love stories: One of the best things that bitcoin has going for it is that nobody really understands the tech and what it’s actual use cases will end up being.

- It’s anti-government/anti-establishment attributes make it a perfect tech for the times: Populism is rampant as well as distrust in institutions around the globe. The idea of a speculative instrument outside of institutional control has the perfect appeal.

- It’s a global market: Anybody anywhere can play bitcoin (though in some countries it’s harder than others). This means there’s a huge pool of potential fools who still haven’t bought in.

And to top it all off, we’re in the perfect macro environment for a huge speculative bubble.

We’re coming off a period of horribly negative global sentiment stemming from the Great Financial Crisis. And long periods of negative sentiment are typically followed by the opposite.

Central banks have kept the world flush with easy money by keeping interest rates low and printing billions in new money. In macro terms, we say that global liquidity is flush.

And this creates the perfect environment for asset bubbles. This was perfectly described by 18th century editor of The Economist Walter Bagehot when he said:

One thing is certain, that at particular times a great deal of stupid people have a great deal of stupid money… At intervals, the money of these people — the blind capital, as we call it, of a country, is particularly large and craving; it seeks for someone to devour it, and there is a ‘plethora’; it finds someone, and there is speculation; it is devoured, and there is ‘panic’.

This is why we’re seeing celebrities like Paris Hilton and Floyd Mayweather advertising their own initial coin offerings (ICO’s are alternate coins that typically get split off the ethereum blockchain and become their own separate “currency”).

Since anybody can “fork” off a blockchain network (it’s all open source), everybody can create their own crypto token. And they are. And people, lots of people, are buying them…

Blockchain “startups” have raised a disclosed $1.85B in just the first half of this year.

This is leading to some outrageous scams that are often unwittingly being promoted by these said celebrities.

Take the example of Centra.

Centra was a recent initial coin offering that raised $30 million and was promoted by Mayweather and rapper DJ Khaled.

Centra made big promises of partnering with Visa and creating the first debit/credit card for the crypto market, amongst other grand visions.

The problem is that these were just empty words.

It was found that the company hadn’t even talked to any of the major credit card companies, employed no computer programmers, that the founders previously ran a luxury rental car service in Miami of all places, and their listed CEO was a fictional (as in completely made up) person.

The “founders” of Centra now have $30 million of investors’ money. Of which, they can choose to do anything they want… like buy a bunch of Maseratis or life-sized cheese molds of themselves, and investors be damned….

An “investor” in the Centra ICO posted on Reddit defending the company and it’s crypto tokens saying “What’s important is that Centra is being endorsed and they have a product. That’s what matters to investors”.

This is the type of highbrow “investor” who is now driving prices higher in the crypto market.

Again, the vast majority of the players in this market don’t care about “trivial” things like made up CEOs and not having a real business model. They just want a higher price to sell into, a greater fool than them.

Centra is not an isolated incident. This is happening more and more.

I find this extremely fascinating from a behavioral investing standpoint.

We’re witnessing what may well become one of the largest speculative bubbles in history. And people are becoming full-on punch drinking devotees. The more this zealotry spreads, the more crypto prices will rise, which will reinforce their beliefs and bring in ever more greater fools!

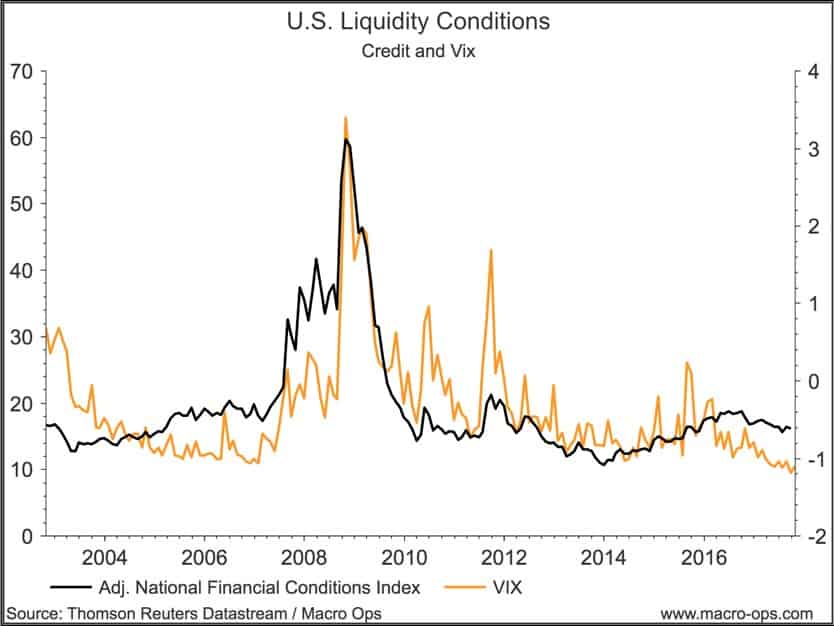

To play this kind of speculative bubble one needs to work off the technicals — which are very good in bitcoin where pure emotion/sentiment dominates price action — and keep a close eye on the liquidity.

Liquidity, which is the availability of money and demand in the global system, always precedes market moves.

A tightening of liquidity means a tightening of credit conditions. This leads to lower future demand and is a sign that investors are discounting greater risks in the market.

When global liquidity starts to drain (the black line moves higher on the chart below), rising volatility (orange line) typically follows.

And when market volatility rises, investors begin to reprice risk. The repricing of risk leads to lower demand and hence fewer fools to sell risky assets to. Fewer fools means less buyers and less buyers in a momo market leads to more sellers. This creates the scenario where you have a bunch of freaked crypto zealots all clambering for a shrinking exit at the exact same time.

This is when a boom leads to bust. And the warning signs will show on the various liquidity indicators beforehand.

(Note: If you want to learn how to track liquidity to get ahead of the bitcoin crash, then check out this guide right now.)

The chart below is from Peter Brandt. It shows bitcoin forming a classic parabola. This is a common technical pattern in a speculative bubble.

We should continue to see the channel narrow and compress as the dips get bought more quickly and prices rise. When the price hits the top of the parabolic channel we should expect a retrace of at least 50%. The current price target is $6,800, not far from where bitcoin is currently trading.

Buyers should beware once they see liquidity begin to tighten at the same time bitcoin is trading near the upper range of its channel. That will be a setup for a large pullback.

This setup is aligning perfectly with the launch of bitcoin futures by the CME. This is a huge deal for the bitcoin trading community because it opens the floodgates to institutions and other participants who can only trade on regulated exchanges.

It also allows guys like us to easily short bitcoin when the eventual bubble pops!

You can read more about the brand new CME bitcoin futures by clicking here.

Conclusion:

- The Blockchain is groundbreaking technology that, like the internet in the early 90s, will transform industries is ways none of us can fathom.

- Bitcoins have no intrinsic value and it’s unclear how they develop any. Their “worth” is based purely off having a greater fool to sell to. The market is dominated by punch drunk speculators.

- Bitcoins and other crypto tokens don’t meet the requirements of a currency and are closer to trading cards or in-game virtual objects that only have market prices due to a devoted fan base and false scarcity.

- Bitcoin is the perfect asset for a speculative bubble: it has no intrinsic value so it can’t be objectively assessed, it has a complex and compelling story, it’s global, and it’s the perfect anti-establishment tech for the times. Because of this, bitcoin probably still has a ways to rise.

- Bitcoins should not be bought as a long-term investment but instead traded on a purely technical basis.

- Liquidity and technicals are the only forms of useful analysis to use on the crypto market simply because they help identify regimes where there’s likely to be increasing or decreasing Fools to sell into.

As for the future of the crypto and blockchain market in general, I think Matt Levine of Bloomberg has the best take. Here it is:

Look, I know I sound like a cryptocurrency/blockchain skeptic. I guess I am one, fine. But Walmart’s mangoes are being tracked throughout the supply chain in an auditable distributed database that makes them much easier to follow than previous methods did. A syndicated-loan blockchain probably will work better than the current system of transferring syndicated loans by, like, faxing signature pages. “Tokenization” of some transactions or ownership interests will probably turn out to be useful, and might change how the markets for digital advertising or cloud storage or housing or whatever work.

But the way I like to think about it is that cryptocurrency might be to the 21st century what stock was to the 17th century: an administrative change in the bookkeeping for ownership of certain assets that over time completely transformed the economy and the world, with a power that the early innovators could hardly have dreamed of. But also, the first like 300 years of the history of stocks were filled with hucksters and hype and bubbles and disaster. Cryptocurrencies and blockchain really could be revolutionary technologies that will ultimately pervade every aspect of the economy, even while almost every individual project could be nonsense.

The above was an excerpt from our Macro Intelligence Report (MIR). If you’d like to learn more about the MIR, click here.