Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

Rising Interest Rates & Discovery (DISCA) — AK reviews the broader market, analyzes what rising rates mean, and also covers our long Discovery (DISCA) thesis.

Antifragile — AK uses an example from Billions along with others to explain Nassim Taleb’s antifragility.

Articles I’m reading —

This week, economist and China based punk rock music executive, Michael Pettis, wrote an excellent piece in Bloomberg on the US-China trade imbalance and why China buying more US goods won’t bring down the US trade deficit one whit.

The issue comes down to basic accounting. China could easily close its trade imbalance with the US, but that would simply lead to another country buying an equal amount less of US exports. The reason why is explained in Pettis’ national identity accounting framework and he lays out how this works. Pettis explains:

Under the current global system, the distribution of income in a number of countries — not just China, but also Germany, Japan, South Korea and several others — is distorted in favor of government and businesses rather than households. This is because these economies effectively subsidize manufacturing exports with various hidden transfers from households, including low wages and low deposit rates. The household share of income is consequently too low for domestic demand to absorb everything produced domestically.

Such distortions also lead to structurally high savings rates in these countries. Income can be consumed or it can be saved. Households consume most of their income while governments and businesses typically save all or nearly all of theirs. By giving the latter a disproportionately high share of income, and households a disproportionately low share, these countries automatically force up their savings rates.

The global economy, in other words, suffers from excess savings generated by a small group of high-surplus countries. The U.S. plays a stabilizing role by absorbing nearly half of this excess of global savings. That’s not because the U.S. has any need for such huge amounts of foreign savings, but because it has completely open, deep and flexible capital markets.

Since the US private sector is not wanting for additional financing (we’ve got plenty of cheap capital), this surplus capital flows right back out through the trade channel, in the form of greater imports into the US. This is an ironclad rule of the balance of payments. And so, we would have to address capital imbalances with the entire world, not just China, if we really wanted to reduce the US trade deficit.

Here’s the link to the article, it’s worth a read.

Also, check out this shareholder letter from Edelweiss Holdings (link here). It’s about how Scientism has polluted financial and economic thinking. It’s exceptionally well-written. Here’s an excerpt.

Intellectual poverty leads to fake thinking which leads to fake language. In fact, nearly all modern financial thinking is contrived. Its ideas and terminology are the product of only the last few decades. Consider that terms such as shareholder value, asset allocation, risk management, and EBITDA were very rarely used prior to 1980. The language we use to discuss our savings has warped into something unrecognizable to our grandfathers.

We consider this intellectual poverty to be the result of a greater moral poverty. The financial world confuses what is legal with what is moral, exaggerating the old agency problem. This comes from the increasing separation between someone’s actions and the outcome of those actions. The agency problem is a special one in the financial industry. In the real world, in every aspect of everyday life, whether at the dentist’s office, a restaurant or a hotel, if someone screws up, there are real consequences. In the financial industry, however, whether in modern banking, wealth management or management consulting, there are no material, long-term consequences for failing conventionally.

The age-old solution to the problem of agency, as the practical philosopher Nassim Taleb puts it in his recent book, is ‘skin in the game’. This has nothing to do with the popular concept of ‘alignment of interests’. The financial world thinks they can solve this problem with the right incentives. They believe that so long as the rewards for their actions are tied to the customer’s financial success, the agency problem is solved. But that’s wrong. Truly, it is not incentives that matter, but disincentives. That is, having skin in the game, or something to lose.

I couldn’t agree more…

Podcast I’m listening to —

I recently listened to a fantastic podcast from the team at a16z. In it, Sonal Chokshi and Marc Andreessen interview W. Brian Arthur who’s considered the father of complexity theory in economics — he was also one of the first people to recognize the potential for positive feedback loops / network effects of software based businesses.

The conversation is wide-ranging and eye opening. One of my favorite bits is when Arthur talks about how the market still drastically underestimates the scale of exponential growth for many of these tech companies. This is something that his friend, legendary investor Bill Miller, calls the “New York-Palo Alto arbitrage”.

Give it a listen, here’s the link.

Book I’m reading —

This week I’ve been reading an older trading book (published in 1986) titled Big Hitters, written by Kevin Koy. I can’t remember how I came across this one but I’m glad I did. It’s a fun read. The book is a compilation of interviews, with mainly old pit traders, in the same vein as Market Wizards — just not quite as good.

My favorite chapter is with Richard Dennis, who most of you will know is the famous commodities trader behind the Turtle experiment. Here’s a section from that talk.

Interviewer: Do you have any views on psychological makeup and its role in successful trading?

Dennis: I might talk about outer-directedness: That’s an interesting concept. Being inner-directed is a lot better for traders. Many people go home at the end of the day thinking, “It’s nice to have made a profit.” Even to the extent that is inner- or outer-directed, I try to tell people that’s one of the worst things to try to judge yourself by.

The other thing — correct in my opinion — would be to go home every day and know exactly how you did. “Did I do everything I was supposed to do? Did I get out of losers?”

But whether the market accommodates your strategy on any one day is pretty irrelevant to whether or not you did the right thing. One should not miss the point of my friend at the Board of Trade — he did the wrong thing every day he was making money — it just took a while to catch up with him. And if he would have concentrated on his form, what he was doing, thinking about it, having a strategy, asking himself, “How is this all going to end?,” he might not have blown out.

Instead, he was directed by the result. You cannot be directed by the result, it seems to me, and do the right thing. It’s not a good guide. I don’t think the results will tell you a hell of a lot. What it applies to is that you need an idea of what you’re doing and some confidence before the results will tell you anything.

We need to always focus on process over immediate outcomes. This is hard. In trading, we can go through long dry spells of days, weeks, months, even a year or more of sub-par performance. It’s important to separate the efficacy of your process from its immediate outcomes.

In poker, we call this “resulting”. Which is when players create too tight a relationship between the quality of their outcomes with the quality of their decisions. A large sample size is needed in order to pull actual signal from outcomes, in order to properly assess your decision quality.

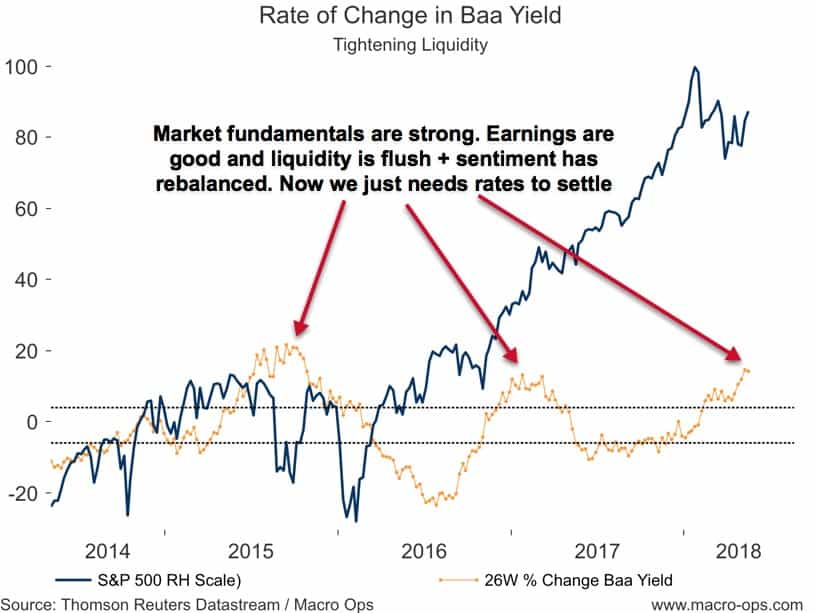

Chart I’m looking at —

We need interest rates to settle down in order for the next leg of the bull market to begin. This will require a little more market volatility to drive a bid into bonds. I think we’re seeing that now.

Trade I’m looking at —

GAIA is a stock we’ve covered extensively over the last year and a half. It’s a Netflix for new age spiritual type content (think guided meditations, specials on the power of positive thinking, and the occasional alien bit). It’s run by Jirka Rysavy, one of the best CEOs in the business.

It’s up roughly 120% since we first recommended it in our March 2017 Market Intelligence Report (MIR).

Unfortunately, I got knocked out of my position in the stock for a small profit a while back and have been watching from the sidelines the last few months as the stock trucks higher.

I’m probably going to write up a trade review of this one as it’s a perfect example of improperly matching one’s trade management with conviction level — I should have sized smaller and given the stock much more room to run.

But, because of how well the company has been executing and the long runway it still has ahead of it, I’m considering getting back in — this time with a much wider uncle point. Even though the stock has more than doubled since we first rec’d it, the trade is still highly asymmetric, in my opinion.

Here’s what I wrote in our March 2018’ MIR where I reiterated our buy recommendation on the stock.

Their service is expected to hit one million subscribers by 2019. That equates to a revenue run rate of roughly $110m. The business is fully funded for the next 24 months at which time it plans on lowering spending on customer acquisition and bringing down growth from the current 80% y/y rate to a more sustainable 20%.

So in under two years, this $200m market cap company will be generating free cash flow somewhere in the ballpark of $45-60m. And what type of multiple do you give a company that’s growing free cash flows at roughly 20% a year? 15 or 20x maybe?

Let’s be conservative and give it a cash flow multiple of 15. 15 times $50m is $750m which is 3.75x higher than where it’s trading right now. A 20x multiple would give it a market cap of $1B which would mean the stock would trade at $65 a share.

One of my favorite small-cap value hedge fund managers is Mark Sweeney, of Laughing Water Capital. He’s also long the stock and believes it’ll be trading over $60 within a few year’s time. You can read his update on GAIA in his latest investor letter, here.

Quote I’m pondering —

We are drowning in information, while starving for wisdom. The world henceforth will be run by synthesizers, people able to put together the right information at the right time, think critically about it, and make important choices wisely. ~ E.O. Wilson

This is especially true in the game of global macro. Learning how to effectively separate the wheat from chaff is much of the battle…

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.