This is part two of our monthly Trifecta Lens Pulse Report at the Macro Ops Collective.

Here’s a quick recap. At the end of each month, I present the top five performing Industry Thematics based on RS Inflection Scores. Then, I find and share the best charts / actionable setups within the top three thematics for collective research.

The goal is simple. I want to say: Here are the strongest thematics over the past 1-3 months; maybe they’ll become the next Relative Strength leaders, and here are the best setups within those thematics.

Last month, our Top Five RS Inflection Thematics were (1M returns):

- Ethereum (AETH): +9.28%

- Rare Earth (REMX): +23.40%

- S&P Metals (XME): +12.61%

- Solar ETF (TAN): +12.40%

- Lithium (ILIT): +15.09%

You can read last month’s RS Inflection Trifecta Lens Pulse here.

Before we dive into this month’s Inflection Leaders, I want to recap our August, Q3, and YTD performance. Here’s the data:

- August: +4.43%

- Q3-to-date: +1.29%

- YTD (as of August 31): +25.04%

We’re having a decent year, but we’re not satisfied with our performance versus the opportunity set. That said, we’re excited about the next four months of trading.

Oh, before we dive into the Inflection Report, I want to let you know that we’ve opened our Macro Ops Collective enrollment period. The Collective is the internet’s highest-quality group of dedicated traders, entrepreneurs, and fund managers. If you love dissecting markets, incremental (but compounding) daily improvement, and pushing yourself to be the best trader possible, you will love the community.

Click the link below to see for yourself. We can’t wait to have you in there.

This Month’s RS Inflection Leaders

Here are the top five thematics based on RS Inflection Scores. For reference, the RS Composite score ranks each theme based on the weighted total return for the 1-week, 1-month, and 3-month periods.

- Rare Earth (REMX)

- Silver Junior Miners (SILJ)

- Silver Miners (SIL)

- Junior Gold Miners (GDXJ)

- Gold Miners (GDX)

Notice anything about this list? It’s the same list as this month’s Composite Score.

This provides an opportunity to discuss one of the most powerful aspects of the Trifecta Lens Composite and Inflection Reports: Knowing what to own and when.

I’ve said this before, but sometimes the best stuff to own is what you already own. That’s true today. We own Composite and Inflection leaders.

In effect, matching Composite and Inflection Rankings is confirmation that we should own more of what’s working.

Here’s an example of why I love this new process.

Alex and I are getting bullish on oil and natural gas. But our Oil & Gas thematic ETF (XOP) has an Inflection Rank of 8.90 and a Composite Rank of 3.50.

Now compare these scores to their respective averages:

- Inflection: 7.37

- Composite: 14.38

Oil and gas is neither an Inflection nor a Composite leader. As such, we shouldn’t own these equities … at least not yet. And that’s the point.

The system forces us to invest money in themes that are working, and when we already own the things that are working, it forces us to do nothing. How great is that?

That makes this month’s Inflection Report … easy? We already wrote about the ideas within these thematics last week.

But that’s good! It gives us time to write about two significant developments in our portfolio companies: Magna Mining (NICU) and Idaho Strategic (IDR).

Both companies released new drill results over the past week that could drastically alter the size and scale of their respective assets.

Magna Mining (NICU): Finding The Next Morrison Deposit

I hate the term “company-maker,” but I’m going to use it here. NICU’s latest drill results at its Levack mine suggest the potential for another Morrison-like deposit.

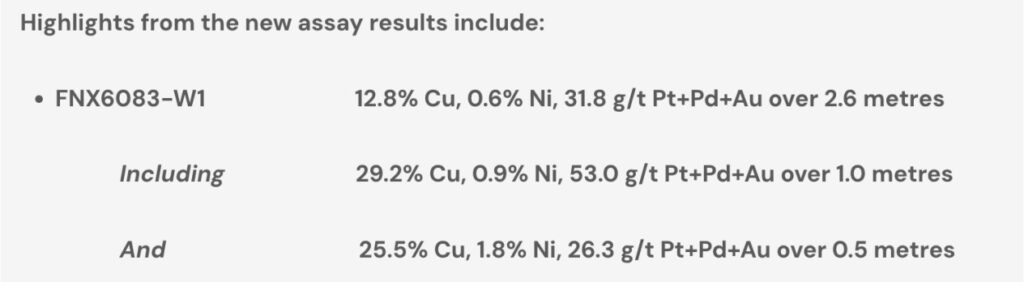

You can read the drill result release here (emphasis mine):

“Drillhole FNX6083-W1 was drilled to test an area 140 metres below drill hole MLV-25-14A (see news release dated July 9, 2025) which intersected 2.6% copper, 8.1% nickel and 17.8 g/t platinum + palladium + gold over 0.6 metres. Drillhole FNX6083-W1 intersected multiple mineralized intervals ranging from veinlets of copper rich chalcopyrite and bornite, to more than 1 metre of massive chalcopyrite. Magna is referring to this target area in the footwall of the No. 3 Zone as the Rob’s 2 (“R2”) target.”

But here’s the big news.

These drill results confirm that R2 hosts “bonanza-grade” copper-PGE mineralization. For reference, the global average copper grade is ~0.4-0.5%.

Some more context. Each ton of ore in that 29% copper 1-meter intercept contains roughly 644lbs of copper and nearly one troy ounce of precious metals (gold + platinum + palladium). At today’s commodity prices ($6.9/lb Ni, $4.6/lb Cu, $3,530/oz Au, $1,409/oz Pt, $1,137/oz Pd ), that translates into $7,000+ worth of metal per ton.

Let’s step back and discuss the history of the Morrison Deposit.

FNX Mining (yes, the same company that NICU CEO Jason Jessup and his entire NICU management team previously worked at) discovered the Morrison Deposit in 2005 at the Levack mine.

Morrison was a high-grade copper-PGE zone located ~600 meters southwest of the new R2 target area. FNX mined it from 2009 until 2018/19, producing ~2.0 million tons grading 7.1% Cu, 1.4% Ni, and 8.1 g/t Pt+Pd+Au over its life. For reference, the historical Levack mine contact ores averaged ~1.3% Cu and 2.0% Ni.

Think of the Morrison Deposit like a giant chocolate chip cookie. Levack is the entire cookie with some chocolate chips spread throughout. The Morrison Deposit, however, is the gooey center where all the chocolate chips settled to create a molten, delicious treat. Can you tell I’m writing this late at night?

Two more things on Morrison’s geology before we continue:

- The Morrison deposit consisted of a network of massive chalcopyrite veins (the most common copper-bearing mineral) that ranged from <1 m up to ~6 m thick, often carrying very high precious metal values.

- Morrison exhibited a distinct “vertical mineralogical gradient”, meaning it had narrow upper veins rich in nickel and wide lower veins containing significant amounts of copper, platinum, palladium, and gold.

I mention all of this because these latest drill results suggest that the same thing is happening in the R2 zone.

The initial shallow footwall intercept (MLV-25-14A) at R2 was nickel-dominant (8.1% Ni with modest Cu), like Morrison’s upper Rob’s Zone, while the new deeper intercept (FNX6083-W1) is copper–precious metal dominant (29.2% Cu with modest Ni, plus high PGE).

NICU’s management even said the quiet part out loud (emphasis mine):

“The mineralogical zonation between the nickel-dominated veins in drill hole MLV-25-14A and the copper and precious metals-rich veins reported today in FNX6083-W1 appears to be consistent with that seen in the Morrison Deposit.”

If anyone would know the similarities between the two, it would be the team that found the original Morrison deposit!

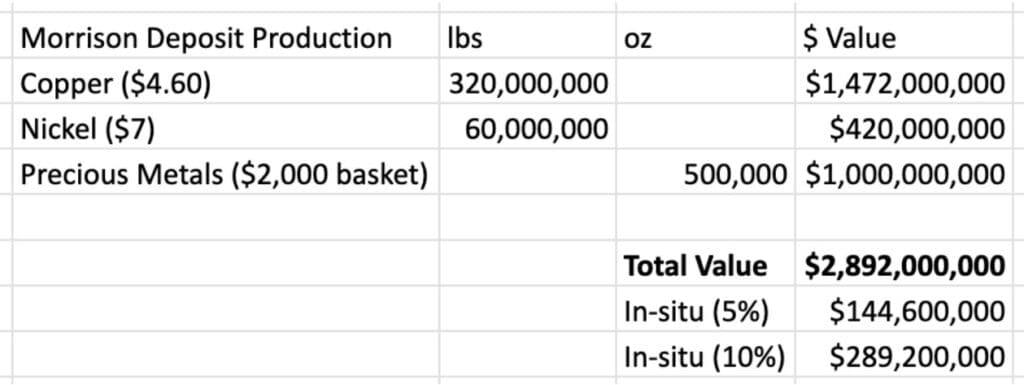

Let’s put some numbers around what another “Morrison-type” deposit could mean for the company. The original Morrison deposit was a 2M ton high-grade ore body that produced 320 million pounds of copper, 60 million pounds of nickel, and over 500,000 ounces of precious metals.

Here’s the in-situ value of that production assuming today’s prices (remember, we’re only giving credit to Morrison’s produced ore).

In other words, if (and that’s still a big IF) NICU finds another Morrison-style deposit, it could add ~$3B in gross metal value. Of course, you discount that gross value to find an in-situ value. But what’s the correct in-situ percentage? It’s higher than 5% and maybe higher than 10%.

R2 is located on an existing mine property with underground access nearby (Levack is adjacent to Magna’s operating McCreedy West mine and already has some infrastructure in place), making any development faster and cheaper if the deposit proves viable (via additional drilling).

We’re not alone in our analysis, either. SCP Research added $100M to its NICU valuation after the R2 drill result news (emphasis added):

“We update our model to reflect 2Q25 actuals and lower cash (C$27m) but add $100m of nominal exploration upside ahead of follow up drilling on the new R2 target. As drilling brings visibility to the potential scale of this new discovery, we expect this to change.”

NICU printed new ATHs on the drill result news. I’ve also seen lots of long-time shareholders increase their position at ATHs on the back of this news, which is something you don’t always see.

We have a 3% notional position in the portfolio and will add to it on pullbacks within the uptrend (we might even use Chris M’s new ATR indicator – more on that in a future Long Pull Report).

NICU is in the early stages of becoming a multi-billion-dollar company with multiple producing mines in a Tier-1 jurisdiction, run by an exceptional and aligned management team. What more could you ask for?

Alright, onto Idaho Strategic (IDR)!

Idaho Strategic (IDR): The Next Mountain Lemhi Pass

Last week, IDR announced the discovery of a carbonatite-hosted REE occurrence at Lemhi Pass.

Here’s what I wrote in #ideas-equities after the news release:

“Today’s IDR news release showing the presence of carbonatite with strong rare earth elements (REE) mineralization is a BIG DEAL. It could drastically change the value of the company’s REE assets, much higher than previously thought.

There are two main reasons for this excitement:

- It was initially thought that most of IDR’s carbonatite ore was in the Northern Mineral Hill Property. This release confirms the presence of carbonatite at the southernmost Lucky Horseshoe property. This significantly expands the potential resource.

- The carbonatite found today is the primary lode source of REE mineralization at Mountain Pass in the U.S., Mount Weld in Australia, and Byan Obo in China – the three major REE operations globally.”

Let’s start with the Mountain Pass comparison, mainly because it’s the most exciting/sensational, and I can’t help myself.

Carbonatite: The Primary Ingredient For Tier-1 REE Deposits

Over half (51%) of all global REE resources are in carbonatite-associated deposits, and the world’s three largest REE deposits – Mountain Pass (USA), Mount Weld (Australia), and Bayan Obo (China) — are carbonatite-associated deposits.

Just to give you an idea of the size of these carbonatite deposits:

- Mountain Pass: 18.9 million tonnes of ore grading 7.06% REO (as of 2020)

- Mount Weld: 18.9 Mt at 8.3% TREO

- Byan Obo: ~48Mt REO at ~6% grade (could be as high as 100Mt, but it’s China, so who really knows)

There are four main reasons why carbonatite-associations can potentially produce mega deposits:

- Large Intrusive Bodies: Carbonatites form large pipes, dikes, or complexes, allowing for high tonnage potential. Some carbonatite deposits (like Mountain Pass or Iron Hill in Colorado) can span kilometers. Contrast this to the high-grade, narrow veins that IDR initially assumed based on historic drilling/surface samples.

- Continuity & Mineability: The intrusive nature of carbonatite means mineralization can be relatively continuous both along strike and at depth. This allows for bulk mining methods to leverage the high-tonnage, low-grade ore.

- Higher REE/Thorium Content: Carbonatites tend to have lower radioactivity relative to their REE content. In other words, carbonatite-associated deposits require fewer specializations and permitting to mine.

It’s one of the reasons I love the District Metals (DMX) uranium deposit. The uranium is of a low-enough grade for conventional mining by “generalist” miners, not just highly specialized uranium companies.

Carbonatite would allow IDR to mine its REE deposit without complex permitting and tailings management (read: lower cost and more feasible).

- Favorable Metallurgy: Many carbonatite REE deposits contain bastnäsite or related carbonate minerals, which are easier to process than monazite. Don’t get lost in the geology jargon.

All you need to know is that bastnastie is easier to process than monazite. Monazite-hosted REEs require an entire chemical plant to extract REEs. Carbonatites require a more straightforward, staged process.

Here’s why this matters: Lemhi Pass may host a carbonatite dike swarm or a small intrusive complex associated with its major faults, rather than a series of high-grade, narrow veins, which would rewrite the district’s geology.

Before the carbonatite find, geologists assumed Lemhi Pass was a collection of 87 separate narrow veins. Mining that system would require moving equipment to each new vein, doing underground mining with no economies of scale.

A continuous carbonatite deposit would enable IDR to design a single mine (perhaps an open-pit mine) to extract the bulk of the resource, rather than multiple small underground workings. This consolidation dramatically improves economies of scale.

The company explains the significance of finding carbonatite at Lemhi Pass, its Southernmost property, versus historically assumed Mineral Hill (emphasis mine):

“Until this recent discovery, historic geologic reports led many to believe that the carbonatites within the Idaho REE-Th Belt were confined to the northern portion of the Belt, where IDR’s Mineral Hill REE project is located. Discovering a carbonatite at the Lucky Horseshoe prospect at Lemhi Pass, the southern most recognized project in the Idaho REE-Th Belt, changes this narrative.”

Said differently, everything from Mineral Hill to Lemhi Pass becomes in play for more carbonatite.

Conclusion: Another Potential Company-Maker

Carbonatite-hosted REE deposits form the Mountain Passes, Mount Welds, and Bayan Obos of the world, delivering the tonnage and continuity required for long-term production.

The Lucky Horseshoe carbonatite discovery has effectively transformed the outlook for Lemhi Pass. It suggests the district’s REEs are not just in scattered fractures, but sourced from a significant igneous system with potentially large continuous REE-rich bodies.

This opens the possibility of Lemhi Pass becoming a major REE resource with world-class deposit characteristics and adding billions in potential NPV if drilling can prove out the thesis.

As I said earlier, sometimes the best stuff to buy is what you already own. And we want to own more NICU and IDR.

Quick reminder … If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the button below and sign up. We look forward to seeing you in our Slack!