Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Now for your latest Macro Musings…

Latest Articles/Podcasts/Videos —

Genghis John And The Ultimate Mental Model For Markets — Alex introduces Boyd’s strategic framework, the OODA loop and explains how it can be used to read markets.

Playing The Player Update: Another Major Buy Signal — Alex pulls together the latest macro data and makes the case for a continued bull run in equities. Sentiment has diverged far away from the fundamentals creating an attractive buying opportunity.

The Market Is Teeing Up — Another macro data dump. Alex pulls together even more evidence to show why the probability of a recession is low.

Articles I’m reading —

The FT published an article this week titled “Why Taiwan poses a threat to the US bond market” that discusses what I think is a critical phenomenon in markets today, which is that of a growing asset shortage (h/t to @Mark_dow). Here’s a few excerpts from the piece that explain:

Taiwan may be small, but the island has emerged as a financial superpower thanks to the thriftiness of local savers and an eye-watering current account surplus of about 15 percent of gross domestic product. The country now has the second-largest financial system in the world, relative to gross domestic product.

… The local economy is not big enough to accommodate these enormous sums, so Taiwanese financial institutions have funneled a whopping $1.2tn abroad.

Long-time Collective members will remember that I wrote about this idea in our June 18’ MIR titled “A Persistent Bid”, where I shared the following:

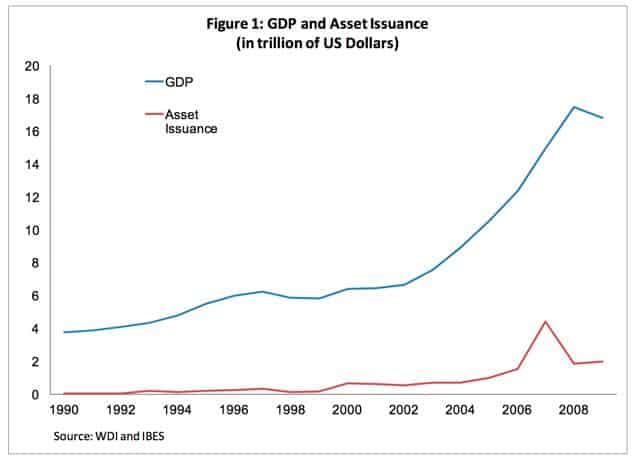

The IMF points this out in a recent paper, saying an “economy’s ability to produce output is only imperfectly linked to its ability to generate financial assets.”

The chart below proves this point. As emerging markets increase in size, their domestic financial markets lag far behind — financial assets grow at roughly half the rate of GDP. With a limited domestic pool of securities, EM savers end up having to invest the majority of their assets abroad.

The IMF hits at what this means for global asset demand, writing “improved macroeconomic fundamentals have raised the demand for financial assets. Rising income per capita in EMs, pension reforms in Latin America, increasing commodity prices in the Middle East and Africa, and limited consumption growth in East Asia have contributed to an increasing supply of domestic savings in EMs that needs to be invested.”

As emerging markets mature, their ability to generate credit and grow their money stock increases exponentially. And since EM financial markets can’t soak up this money supply, it means that an increasing amount of it has to flow into the US; which has the deepest financial markets in the world. This significantly raises demand for US assets.

Rick Rieder, the CIO at Blackrock, pointed out in a recent twitter thread (link here) that “Due to the demographic revolution in pension, insurance, and central bank assets, there is roughly 3x as much capital that needs to be invested today as was the case in the early-2000s”. Rieder goes on to note that though the widening US budget deficit (read, rising Treasury issuance) has helped meet some of this increased demand, it’s still not enough. He concludes by saying “This dynamic has resulted in a dramatic supply/demand imbalance for yielding assets, which is likely to persist for many years, and can be clearly witnessed in the impressive capital flows into income in recent years”.

This all might read as a bit wonkish but it’s an important dynamic to understanding certain asset prices and potential market risks, today. Here’s just a few practical examples of what I mean.

- This persistent bid for yield is keeping rates low and financial conditions (ie, liquidity) loose

- “When the ducks are quacking, feed them”… We should expect to continue seeing rising corporate debt, perhaps to fund more stock buybacks?

- Dollar funding mismatches among financial institutions in Asia are becoming a systemic vulnerability

Here’s the link to the FT article (porous paywall). And if you’d like to learn more on this subject, I highly recommend giving this recent San Francisco Fed podcast interview with cross-border capital flow expert, Brad Sester, a listen (link here).

I’m sorry but it’s pretty much all wonky recs this week as far as reading goes. Nonetheless, I think this is important stuff to stay abreast of. The last article I think you should read is titled “Dual interest rates always works” written by Fund Manager Eric Lonergan over at the Philosophy of Money blog (link here). Eric talks about the vastly underappreciated power of the ECB’s recent mon-policy ‘innovation’ in TLTRO. It’s a short read and understanding TLTRO could be as important, if not more so, than MMT in the coming years.

Charts I’m looking at—

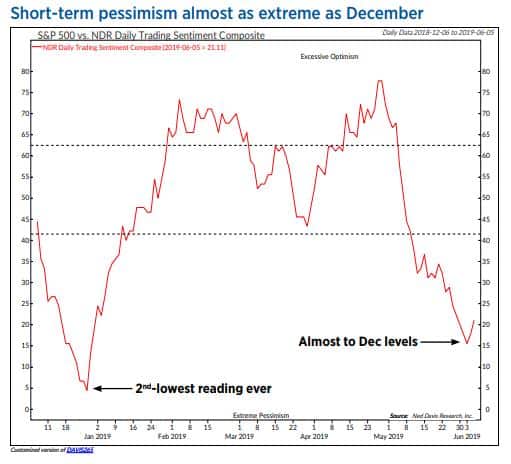

Over the last week, I’ve been pointing out the bearish extremes in a number of sentiment indicators we track. The NDR Daily Trading Sentiment Composite shows just how pessimistic traders have become (h/t @edclissold). The composite hit 16% on Tuesday. It was only lower for six days in December when the second lowest reading ever was recorded.

What does this mean?

Reading sentiment is more an art than a science. And it’s best used in conjunction with both technicals and fundamentals. A reading like this certainly isn’t bearish. I can’t help shake the feeling though that we’ll likely see one more corrective leg down, for a full sentiment capitulation, before the next major leg up. But who knows? Respect price and mind your risk…

Podcast I’m listening to —

Barry Ritholtz’s latest MiB podcast with Scott Galloway is exceptional and I highly recommend you give it a listen. They talk about Scott’s latest book “The Algebra of Happiness” which is his accumulated learnings for living a fruitful life. They also chat about big tech, debate the failures of our tax code, as well as the “elitist” syndrome plaguing our university system. It’s an hour well spent. Here’s the link.

Video I’m watching —

The Stanley Druckenmiller was interviewed on stage this past week at The Economic Club of New York (link here). Druck talks about how he flipped from all in on equities to piling into bonds at the start of May after the President tweeted something disparaging about trade talks with China; which of course was right when stocks rolled over and bonds shot through the roof.

He also talks about some of the things he looks at to read markets (I’ve written some about this here and here). Basically, he looks at the forward cyclical parts of the market to get a read on the economy and trend of the broader indices. Things like trucking, industrial metals, semis etc…

Anyways, give the interview a watch.

Book I’m reading —

This week I started reading “Investing: The Last Liberal Art” by Robert Hagstrom. I had actually started it a few months ago, but I’m usually reading 4 to 5 books at a time and this one ended up getting put to the side for a while. But I’m glad I picked it back up again as I’m enjoying it so far. It’s an easy read and I’ve come across some good nuggets (I’m about halfway through).

The book is similar to Mauboussin’s “More Than You Know” or like a shorter version of “Poor Charlie’s Almanac”. Hagstrom explores mental models pulled from biology, physics, psychology, philosophy and so on… and then shows how they can be applied to markets and investing. I’ll be sharing my book notes with Collective members once I’m done.

Here’s a section from the book where he shares some bits of wisdom from the first book written on the stock market, “Confusion of Confusions” by Joseph de la Vega in 1688.

Vega’s “Confusion of Confusions” is easily summarized. In the Second Dialogue, Vega lists four basic principles of trading—as relevant today as they were 325 years ago: The first principle: Never advise anyone to buy or sell shares. Where perspicacity is weakened, the most benevolent piece of advice can turn out badly. The second principle: Take every gain without showing remorse about missed profits. It is wise to enjoy what is possible without hoping for the continuance of a favorable conjuncture and the persistence of good luck. The third principle: Profits on the exchange are the treasures of goblins. At one time they may be carbuncle stones, then coals, then diamonds, then flint-stones, then morning dew, then tears. The fourth principle: Whoever wishes to win in this game must have patience and money, since values are so little constant and the rumors so little founded on truth. He who knows how to endure blows without being terrified by the misfortune resembles the lion who answers the thunder with a roar and is unlike the hind who, stunned by the thunder, tries to flee.

Funny how much of that still applies.

Trade I’m considering —

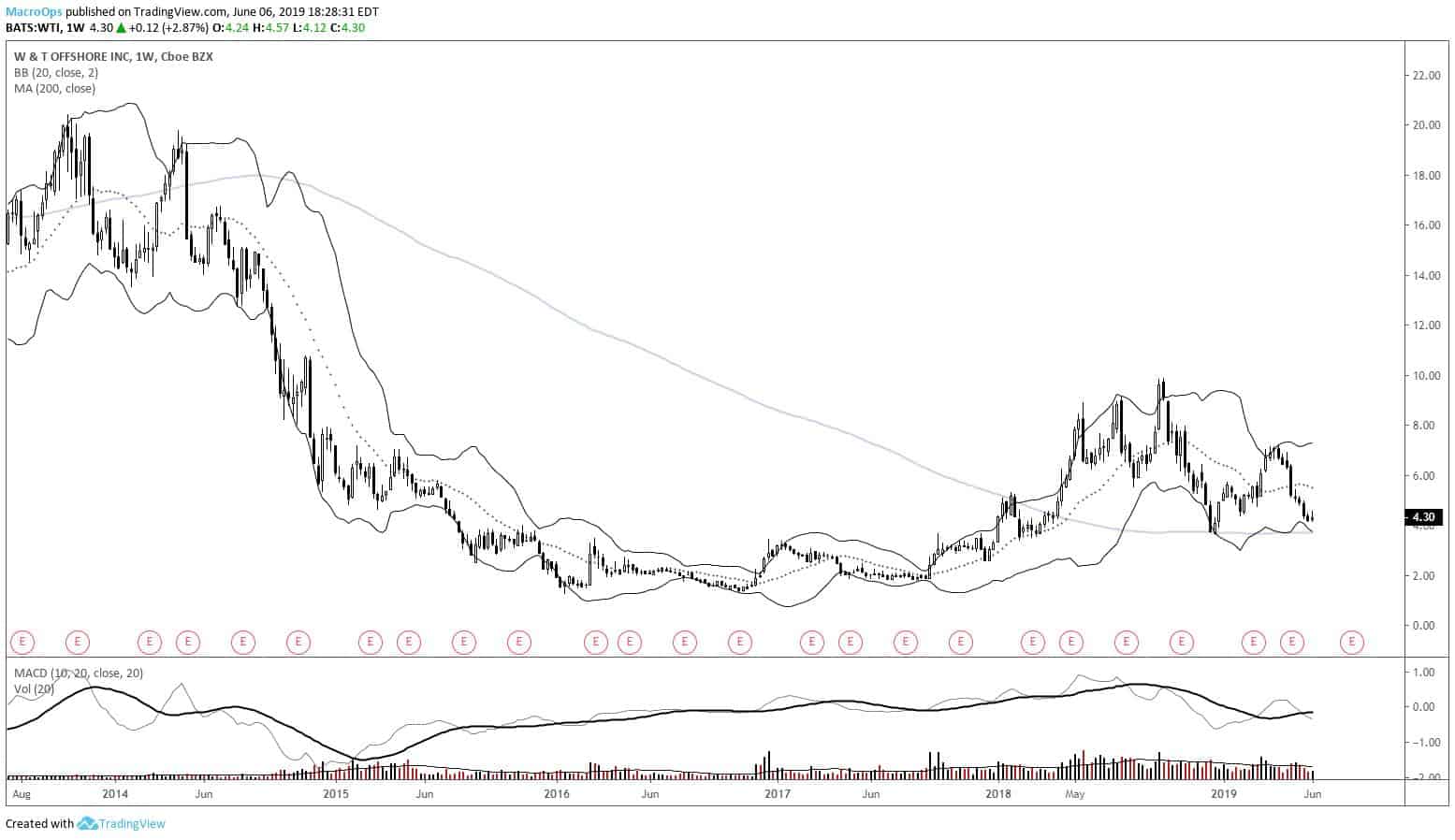

In following with one of my current macro thematics which is “short overvalued growth, buy value” I’ve been spending the majority of time looking at incredibly beaten down left for dead stocks that apparently nobody else is interested in owning. Naturally, many of these names happen to fall in the energy space and I’ve pitched a few of these names in Musings over the last few weeks.

I plan on writing up an in-depth report on this sector of the market next week for Collective members. I think there’s incredible positive asymmetry on offer in this space. And I believe the recent weakness in crude is more a result of what became stretched bullish positioning — that’s currently being washed out — than it is a reflection of poor supply/demand fundamentals.

Anyways, here’s one of the stocks on my radar W&T Offshore (WTI). Longtime readers will be familiar with this one. I first pitched it back in 2017 when it was trading for just over $2 a share. It ended up being one of our better traders over the following year. And now I’m thinking we’re getting close to another major buying opportunity.

The stock trades for just over 3X EV/EBITDA. It’s nearing significant support in its lower Bollinger Band and 200-weekly moving average. If the dollar breaks to the downside soon, we could see a significant pop in oil along with these energy plays. I’m also seeing signs that long-term capital is beginning to makes its way back into the space.

Quote I’m pondering —

Meditation on inevitable death should be performed daily. Every day when one’s body and mind are at peace, one should meditate upon being ripped apart by arrows, rifles, spears and swords, being carried away by surging waves, being thrown into the midst of a great fire, being struck by lightning, being shaken to death by a great earthquake, falling from thousand-foot cliffs, dying of disease or committing seppuku at the death of one’s master. And every day without fail one should consider himself as dead. ~ Yamamoto Tsunetomo, Hagakure: The Book of the Samurai

And on that note… That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.