- Although cash flush, AAPL isn’t exciting investors anymore

- Its growth story hinges on China, where the macro picture is deteriorating

- India shows lukewarm demand as well

- AAPL isn’t innovating like they used to and is instead depending on stock buybacks

Distracted by the levitation acts of AMZN, GOOGL, FB, MSFT, and NFLX, investors have left Apple forgotten in a corner. Apple’s latest earnings report was positive, but there’s still concern over iPhone sales growth.

Apple is a complicated company with lots of moving parts. This gives investors the opportunity to focus on many different areas of its business. A popular topic is whether Apple should repatriate its cash. Everyone loves arguing the numbers and how it will affect the stock price. And although it’s fun to talk about, at Foundation we understand that it’s not important. It’s not what actually moves the stock price.

At Foundation we only focus on key drivers. A key driver is the one metric that overshadows all other metrics. It’s what Wall Street pays the most attention to. A stock’s price will change in line with how that metric changes.

For example, perma-bears love to rant about how ridiculous AMZN’s P/E ratio is. But in doing so, they fail to realize how the growth of AWS trumps that P/E ratio. AWS results have excited and exceeded investor’s expectations time and time again. These results are what propel the stock price. Wall Street doesn’t care about the P/E ratio right now. AWS growth is the key driver.

In Apple’s case, Wall Street has identified iPhone sales as its key driver. More specifically, the focus is on iPhone sales in China and India.

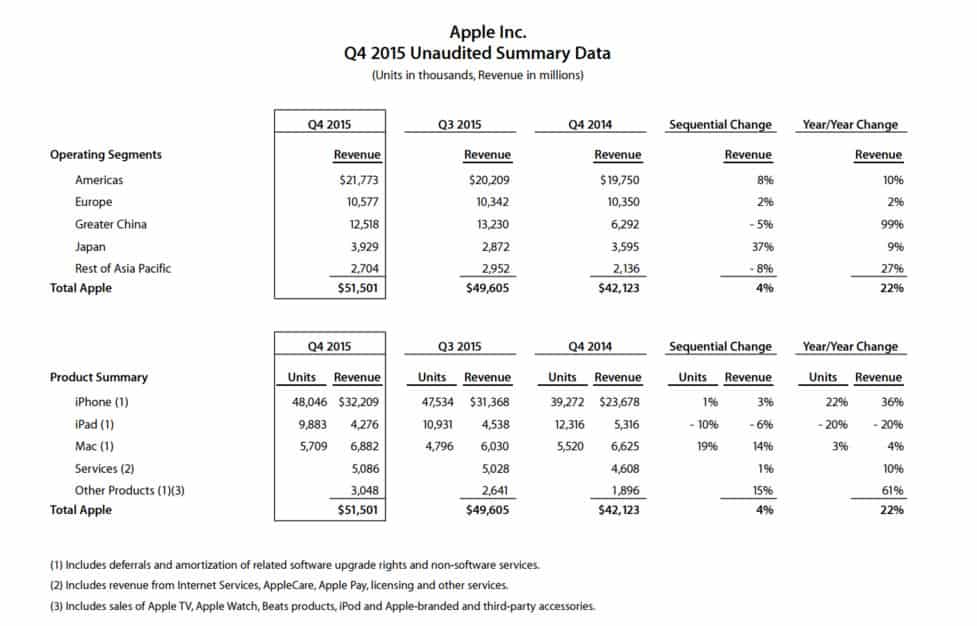

It’s not hard to figure out why iPhone sales matter so much. Just take a look at the sales breakdown from Apple’s most recent earnings report:

In fiscal Q4 of 2015, Apple made $51.5 billion in revenue. Of that revenue, $32.2 billion came from just iPhone sales. That means the iPhone makes up more than 60% of Apple’s revenue! Everything else in Apple’s war chest is miniscule compared to iPhone sales. So when investors think iPhone sales are slowing down, they get nervous.

Taking a closer look at these numbers shows that the smartphone market is maturing. Almost everyone in the developed world who wants an iPhone already has one. There’s not much potential growth left. Revenue in Q4 of 2015 for the Americas, Europe, and Japan was almost the same as it was in Q4 of 2014.

The only real growth available is in China. As seen above, revenue from China increased by 99% year-over-year in the last quarter. This is multiples of the growth rate of any other operating segment.

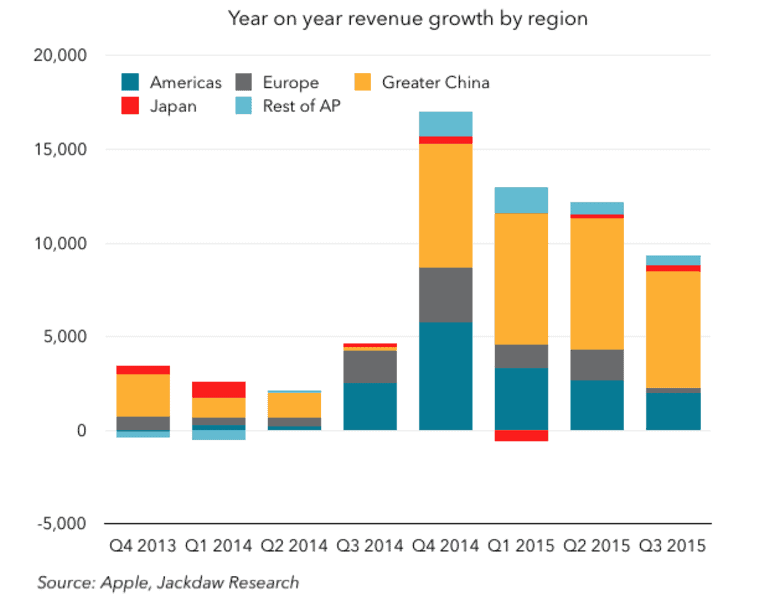

The chart below gives further insight into how China’s revenue growth has increased to dominate other regions.

Apple bulls are depending on China to drive future growth. They hope it will keep Apple on its epic run to a trillion dollar market cap.

But we see large problems with this narrative. The macroeconomic picture for China hasn’t been the rosiest as of late. And things don’t appear to be improving. It will be difficult for China to meet sales expectations in this type of environment.

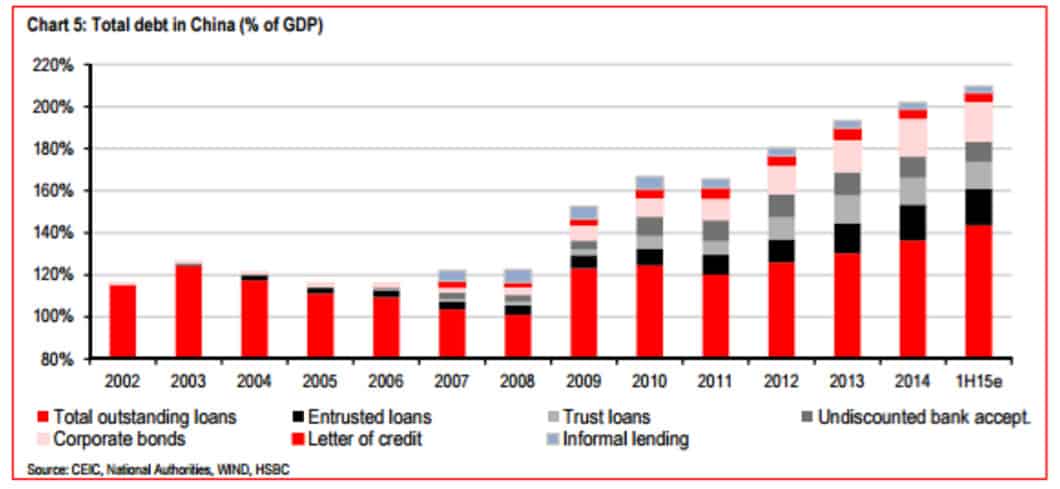

China’s economic growth is cooling because its debt is reaching an unsustainable level. Debt is what fueled much of the Chinese economy’s incredible rise in the last 4-5 years.

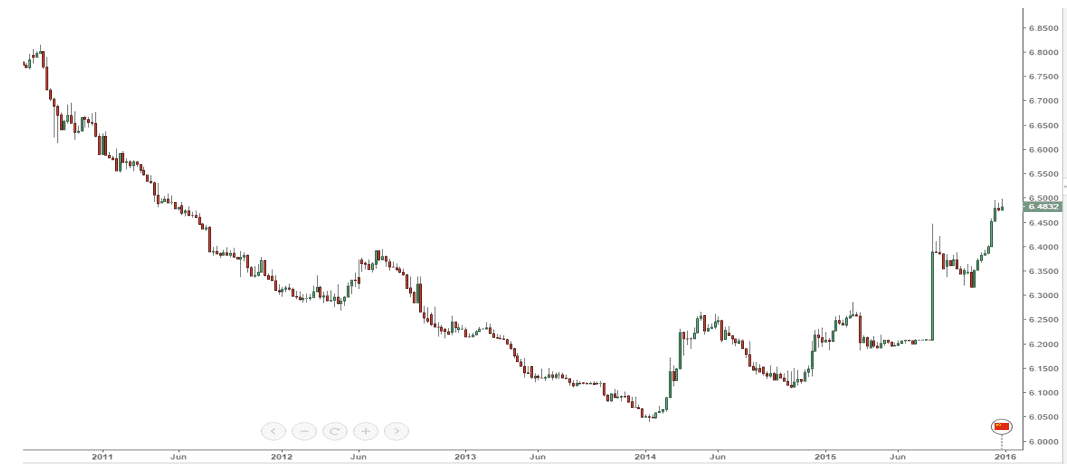

As seen below, China’s debt-to-GDP is now well above 200%.

This debt load acts as a deflationary force on the Chinese economy. Institutions struggle to service their growing debt costs as defaults and non-performing loans rise. In response, the Chinese government has no choice but to weaken its currency.

What has been borrowed, must be repaid — or devalued away. And instead of repaying, governments almost always choose to devalue. China is no exception. A weaker Yuan makes it easier to service debt loads. It also stimulates export demand by making Chinese goods cheaper in the global marketplace. We outlined the mechanics behind this necessary devaluation in our Renminbi Devaluation article.

Below is a chart of USDCNY. You can see that the devaluation has already started. The PBOC has begun to adjust its peg against the US dollar to make its currency cheaper.

The macro dynamics in China are a major threat to Apple’s Asian growth story. The weaker the Yuan gets, the more expensive it becomes for a Chinese citizen to buy an iPhone. Imagine walking into a Chinese Apple store in the midst of an economic tightening cycle. You’re already struggling and now on top of that you see prices (in yuan) rise! How are you going to afford that new iPhone?

India is a good precursor of what will happen in China. India has seen lukewarm iPhone sales due to similar foreign exchange headwinds.

iPhones in India are currently selling between Rs 62,000-Rs 92,000 depending on the model. This is Rs 8,500-9,500 more than the last year’s launch price. This is not only due to exchange rates, but also because the taxes on imported smartphones have increased. It costs 11.5% more in taxes to buy an imported smartphone this year than last year.

Retail stores in India are confirming lackluster demand due to these higher prices. Some stores are saying demand for the iPhone is only 10-20% of what it was last year. The stores continue to pile up their inventory in these poor conditions.

With pessimistic demand for iPhone sales overseas, the China/Asian growth narrative isn’t striking a chord with investors. Analysts continue to lower their estimates for the next earnings report. Many Apple suppliers have also come out and guided revenue down for next quarter. Analysts at Morgan Stanley, Raymond James, Baird Equity Research, and Bank of America, all cut their estimates for iPhone shipments. They cited reductions in build rates at Asian suppliers as the reason. A new report from Nikkei Asian Review also said based on talks with suppliers, iPhone production will be cut by 30% in the first quarter of 2016. None of this is good news for a company dependent on its smartphone sales.

Outside of the iPhone, Apple hasn’t done much with its products to excite investors. It has the means and cash to create something ground breaking, but instead prefers to sit on its heels. Since mid 2012, Apple has reverted to the “IBM” strategy of share buybacks. How creative….

Management has a shot to revive the magic with something new and exciting. But until they choose to take action, we believe Apple’s growth narrative is dead. Investors will continue to pass up on AAPL. They will instead hop on the momentum trains of FB, AMZN, NFLX, MSFT and GOOGL. Those companies’ growth stories are far more promising.

The sheer size of Apple’s market cap also damages its growth story. It’s already so big that further large gains don’t seem likely.

On top of that, Apple is also one of the most widely owned stocks by hedge funds. It’s considered a “hedge fund hotel.”

Do you know what happens when there’s a fire in a hotel? You get a bunch of guests all rushing for the exits at the same time, trampling over each other.

On the slightest hint of bad news or so-so performance, these hedge funds will pull out of Apple fast. And when everyone is selling like there’s no tomorrow, you get huge drops in price.

The Valeant mess is a great example of what can happen to a hedge fund hotel. The drawdowns are swift and vicious.

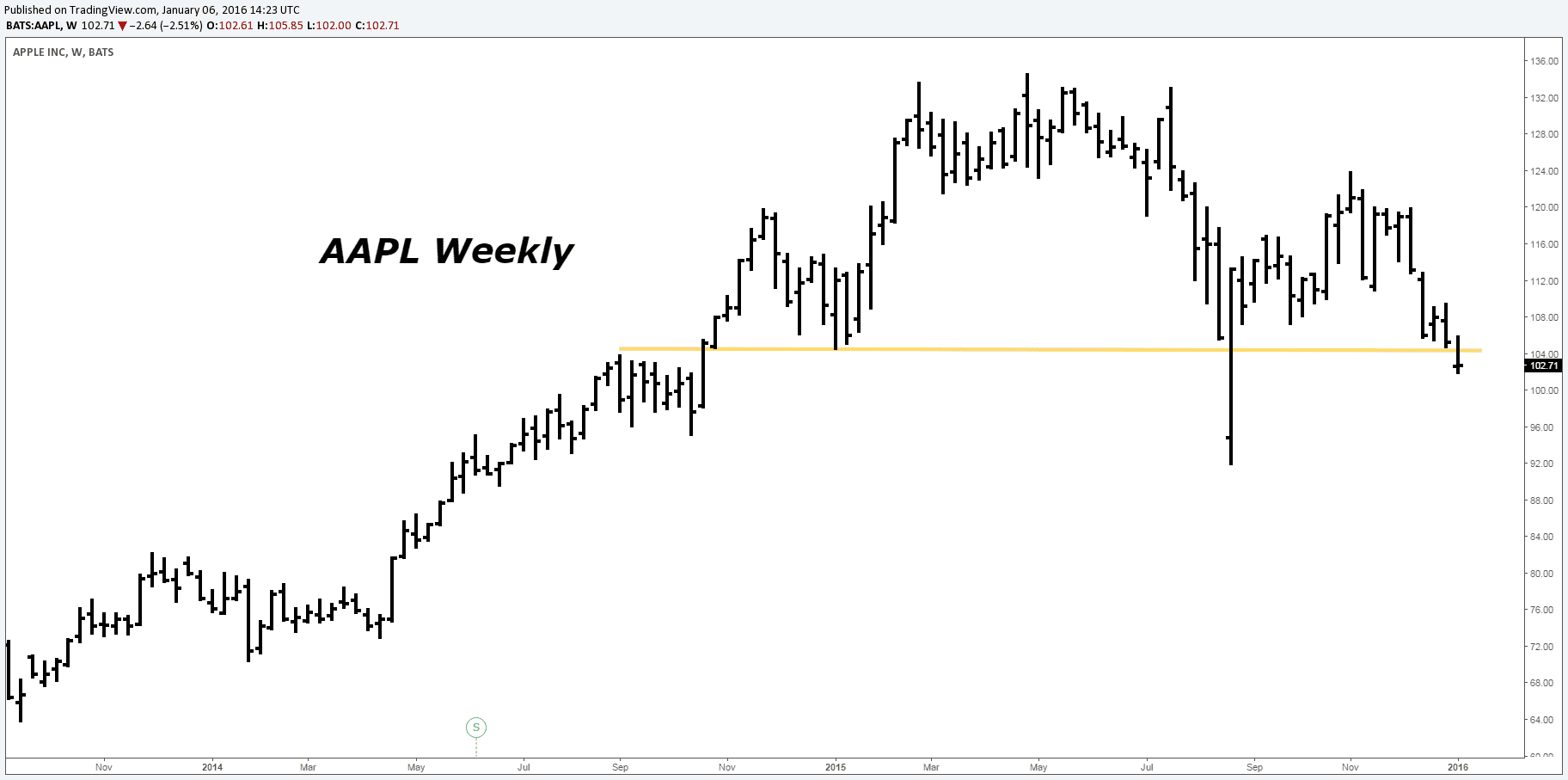

If you take a look at Apple’s price action below, you’ll see the topping process is already playing out. Apple has broken a support line extending back over a year. It will only drop further from here as investors stampede out of the stock.

Until Apple management finds something new to captivate Wall Street, we believe the upside for Apple is limited. Investors should exit and come back when Cook and the gang decide to “cook up” something more meaningful with their war chest.