80-20 Industry Primer: Tungsten

A Pareto Approach to Industry Analysis …

Tungsten is the smallest, most opaque commodity market we’ve covered in our 80-20 Industry Primer series. Global supply is ~106,000 tons, with recent spot prices around $305 to $325/mtu.

Nobody’s pitching tungsten on Twitter or Seeking Alpha. Almost every tungsten mining company profiled over the past 3-5 years is either bankrupt or on care and maintenance. And it’s too small of a market for the Big Boys (Vale, Glencore, Rio Tinto) to care about.

But the world’s hardest metal is at an inflection point. Tungsten’s three primary demand drivers (EV/electrification, semiconductors/robotics, and military) are all increasing and competing for the raw material at a time when Resource Nationalism threatens to remove 80%+ of the world’s supply from the market.

Tungsten has everything we want in a commodity thesis:

- Multiple accelerating demand drivers

- Bombed-out sentiment

- Lack of new supply

- Potential for massive supply/demand imbalance

But before we dive into the tungsten thesis, I want to let you know that our Collective Enrollment is now open!

The Collective is our full-kit soup-to-nuts service that provides research, theory, and a killer community of dedicated traders, investors, and fund managers worldwide.

We’ve been told that there’s nothing else like it on the web. If you’d like to tackle markets with our group (whom I should note has been having a great year in markets), just click the button below and sign up.

We’ve used these industry primers in other markets, like uranium, to capture big moves in industries with secular supply/demand tailwinds. And we’re doing more of the same in 2024!

As always, don’t hesitate to shoot me any Qs!

Join The Collective

Our goal with this 80-20 Industry Primer is to create a simple but robust global supply and demand model. From this, we can answer the most critical questions surrounding the Tungsten Thesis:

- Supply: How much supply is there currently, where will new supply come from, and how much will there be in 1-2 years?

- Demand: Who’s currently buying the supply, how much are they buying, and how will their buying habits change over time?

- Price: How do all of these changes affect the price of tungsten?

We develop deep conviction by doing our own work, stress-testing it against industry experts, and continually updating our models in the face of new evidence.

Let’s get after it.

The Supply Side: Primary & Secondary Deep Dive

To understand the future of any commodity industry, it is vital to understand its past. Let’s look at historical tungsten production and use cases.

History of Tungsten & Use Cases

Tungsten was discovered in 1783 by Spanish chemists and mineralogists Juan Jose and Fausto Elhuyar. But it wasn’t until 1855-1857 that Austrian engineer Robert Oxland patented a process for making tungsten steel.

Oxland’s patent paved the way for more industrialized use cases. In the early 1920s, German electrical bulb company Osram developed tungsten carbide by heating tungsten (also called “wolfram”), carbon, and hydrogen at 1,400-1,600 degrees Celsius.

The result is the second-hardest metal on earth behind diamonds. Tungsten scores 9 on the Mohs scale and 1600HV on the Vickers Hardness scale. For reference, diamonds score a 10 on the Mohs scale and steel alloy scores a 160HV on the Vickers scale.

Tungsten has many use cases given its hardness, heat/scratch resistance, and relative cheapness to diamonds. Here’s a list from the USGS’s 2018 Mineral Yearbook (emphasis added):

“The leading use for tungsten is as tungsten carbide in cemented carbides, which are wear-resistant materials used by the construction, metalworking, mining, and oil and gas drilling industries.

Pure or doped tungsten metal is used for contacts, electrodes , and wires in electrical, electronic, heating, lighting, and welding applications.

Tungsten is also used to make alloys and composites to substitute for lead in ammunition and other products; heavy-metal alloys for armaments, heat sinks, radiation shielding, and weights and counterweights; superalloys for turbine engine parts; tool steels; and wear-resistant alloy parts and coatings.

Tungsten chemicals are used to make catalysts, corrosion-resistant coatings, dyes and pigments, fire-resistant compounds, lubricants, phosphors, and semiconductors.”

I know there’s a lot there. But I want you to focus on three overarching use-case themes:

- Military

- Semiconductors/Robotics

- EVs

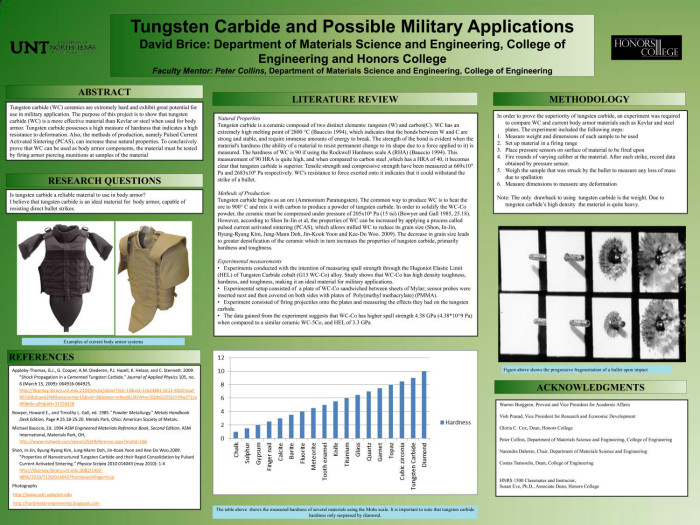

Here are some examples of tungsten military applications.

The big idea is that multiple industries are hungry for more tungsten in a supply-constrained environment. We don’t need to get every use-case demand projection right to be directionally correct on the supply/demand imbalance.

We’ll explain each of the three main demand drivers later. Next, let’s discuss primary supply.

Primary Production: Global & Country-Specific

Most tungsten supply comes from underground mines. I like how the International Tungsten Industry Association explains the mining/extracting process (emphasis added):

“[Tungsten is] frequently located in narrow veins which are slightly inclined and often widen with the depth. Open pit mines exist but are rare.

Tungsten mines are relatively small and rarely produce more than 2000t of ore per day.

Most tungsten ores contain less than 1.5% WO3 and frequently only a few tenths of a percent.

The ore is first crushed and milled to liberate the tungsten mineral crystals. Scheelite ore can be concentrated by gravimetric methods, often combined with froth flotation, whilst wolframite ore can be concentrated by gravity (spirals, cones, tables), sometimes in combination with magnetic separation.”

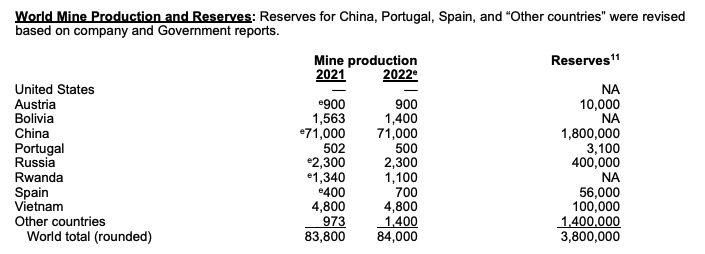

Three countries comprise ~93% of global primary supply:

- China: 84%

- Vietnam: 6%

- Russia: 3%

In other words, 87% of primary tungsten production comes from every Bond villain’s home country.

These countries also pose “Conflict Mineral” risks. Conflict Minerals are any raw material sourced through non-transparent supply chains. It’s like getting Ibuprofen from a man in a dark alley versus going to your local CVS.

The United States hasn’t reported primary tungsten production since 2015. Maybe due to “national security” reasons. Or maybe there’s just no tungsten production market in the US.

According to the USGS, there are only six US companies “with the capability to convert tungsten concentrates, ammonium paratungstate (APT), tungsten oxide, and (or) scrap to tungsten metal powder, tungsten carbide powder, and (or) tungsten chemicals.”

It wasn’t always like that. In the early 1920s, most of the world’s tungsten came from North America, with production split between Canada and Colorado, Nevada, California, and Arizona.

Tungsten is such a small market that we can go country-by-country to examine primary supply. Let’s start with Australia (data as of 2018-2020).

Australia

There are two main tungsten projects and mining companies in Australia:

- Mt. Carbine

- Kara

- Group 6 Metals (G6M)

- EQ Resources (EQR)

Mt. Carbine is currently the only active producing tungsten mine as of June 2023 (via EQ Resources). Group 6 Metals (G6M) restarted its Dolphin Tungsten mine in July/September 2023 but has only shipped 10t of tungsten concentrate.

Kara produced small amounts of tungsten (~40t) until 2016 before being put on care and maintenance.

Almonty Industries also had a tungsten project in Cairns, Queensland, which it put on care and maintenance in 2016.

Australia has the second-largest tungsten resource base globally, yet only one active producing mine. It’s a great example of capital starvation and low incentive prices in the industry.

Austria

Austria produced ~900t of tungsten from its Mittersill scheelite mine via Wolfram Bergbau und Hutten AG (or WBH), a subsidiary of mining/heavy equipment manufacturer Sandvik AB (SAND.OM).

Canada

Canada does not have a producing tungsten mine as of the USGS 2018 Mineral Yearbook survey. The only major project of note is the Sisson tungsten-molybdenum mine in east-central New Brunswick.

Northcliff Resources (NCF.TSXV) did a feasibility study on the mine in 2013. It even received federal and provincial approval in 2017; however, there has been no production.

If successful, the mine would produce ~4,420t/yr of contained tungsten over a 27-year mine life.

China

We don’t have individual mine production data. However, China has three central tungsten production provinces: Jiangxi, Hunan, and Henan. Together, they account for 84% of China’s tungsten production.

The Chinese government increased the country’s production quota to 111Kt in 2023, of which 65% will convert to WO3 (sellable tungsten) for 72,150 tons.

Democratic Republic of the Congo (DRC)

Two provinces control all of the DRC’s tungsten production:

- Kinshasa: 67%

- Maniema: 33%

Artisinal mining dominates DRC tungsten supply. There are no major “corporate” producers. This means that local kingpins rely on forced/slave and child labor to extract tungsten by hand.

The DRC is a listed “Conflict Minerals” country.

Kazakhstan

Kazakhstan does not currently have an active tungsten production industry. However, JSC NMC Tau-Ken Samruk and Chinese company Jiaxin International Resources Investment Limited agreed to establish a JV to kickstart Kazakhstan’s domestic tungsten industry.

South Korea

South Korea imports 95% of its tungsten from China and has no current domestic production. However, Almonty Industries (AII) wants to change that. The company is progressing on the Sangdong tungsten project southeast of Seoul. According to the company’s latest investor presentation, production should start in H1 2024.

If production goes as planned, Sangdong would generate ~7% of the world’s tungsten supply by 2027 and 43% of non-Chinese supply.

Portugal

Portugal produced ~500 tons of tungsten in 2022 from the Almonty Industries (AII)-owned Panasqueira mine.

AII is in the process of expanding the mine life by another 20 years.

Russia

Russia produced ~2,700 tons in 2022. There are four primary tungsten producers in Russia:

- Primorsky GOK JSC’s Vostok-2 Mine

- JSC Zakamensk’s Barun-Narynskoe

- CJSC Novoorlovsky GOK’s Spokoininskoe Mine

- LLC Lemontovsky Mining and Processing Plant

As we noted earlier, Russia accounts for ~3% of global production. They want to increase that percentage in 2023-2024. The country wants to start mining its Tyrnyauz tungsten and molybdenum deposit, which it hopes will 3.5x tungsten production by 2035.

Rwanda

Rwanda generated ~1,100 tons of tungsten in 2022. Most of the country’s production comes from artisanal/small-scale operations within two main provinces: Nyakabingo and Gifurwe.

In most of the processes, tungsten is the primary metal extracted. In others, it’s a byproduct of tin production.

Spain

Spain produced ~700t of tungsten in 2022. However, the country hopes to increase its production in the future. Almonty Industries (AII) plans to restart its Los Santos mine, which it put on care and maintenance in 2020.

There’s also the Barruecopardo joint venture between Oaktree Capital (yes, that Oaktree Capital) and Ormonde Mining PLC.

The mine, which restarted in 2019 after a 40-year hiatus, is expected to produce 140t per month at full capacity.

United Kingdom

The UK hasn’t mined tungsten since 2017 due to environmental restrictions, low tungsten prices, and lack of available capital. For a while, Wolf Minerals hoped to turn on its Hemerdon tungsten and tin project in Devon.

The open pit and beneficiation plant would’ve generated ~2,900t/yr of tungsten and 563t/yr of tin. However, Wolf couldn’t maintain positive cash flow during the ramp-up and on October 2018, declared bankruptcy.

Uzbekistan

Uzbekistan only has one operating tungsten deposit, Ingichki, which Ingichki Metals LLC controls.

However, the country ceased production from Ingichki in 2014.

In 2017, IFG Capital Partners signed an agreement with Uzbekistan’s state geology department to explore seven other potential tungsten deposits in Samarkand. The $300M deal hopes to establish a new tungsten deposit containing ~130Kt.

Vietnam

Vietnam produced ~4,800t in 2022. 91% of the country’s supply (4,350t) comes from one company, Nui Phao Mining Ltd (Masan Resources on the Vietnam stock exchange). Nui Phao is the largest producer outside China and operates one of the lowest-cost tungsten mines globally.

In other words, ~6% of global tungsten supply comes from one mine in Vietnam. That is not antifragile. Due to lower grades and lower throughput from its beneficiation plant, Nui Phao has seen tungsten production decline 15% YoY.

Zimbabwe

Zimbabwe’s flagship tungsten mine, RHA Tungsten, is on care and maintenance. I read an article suggesting that the mine would restart in 2022, but I haven’t seen anything to confirm that.

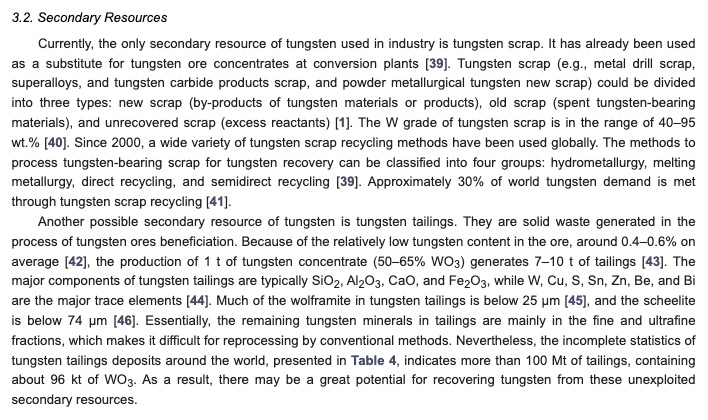

Secondary Supply: What It Is & Where It Comes From

Secondary supply is easy to define but impossible to track. There are two kinds of secondary supply: recycled scrap materials and stockpiles.

Recycled materials account for ~25-30% of global supply or ~21,000 tons annually.

Here’s a snapshot of secondary tungsten supply from an April 2021 MDPI Journal article.

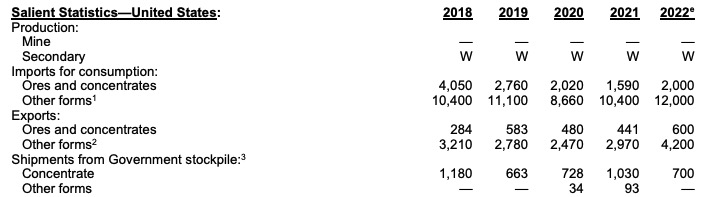

The other form of secondary supply is government stockpiles. For example, the United States buys, sells, and stores tungsten (along with other critical minerals) under the Defense Logistics Agency (or DLA).

These reserves are a fail-safe if China or Russia remove global supply.

It’s impossible to predict how much DLA has tungsten at any given time. However, we can see the trend in stockpile sales since 2018 (see below).

The last two lines show that from 2018 to 2022, the US has sold 4,301 tons of tungsten. The US has spent the past two decades draining its critical mineral stockpiles (easier than raising taxes, right?).

In 1952, the US critical mineral stockpile was worth $42B (inflation-adjusted). Today, it’s worth $888M. The US has sold ~76Mlbs of tungsten alone during that timeframe.

I bet the US defense department is structurally short tungsten after decades of zero wars, an oversupplied market, and no incentive to stockpile after WWII. Historically, the US could tap domestic mines for more tungsten; if that didn’t work, they’d import some from China.

But both of those options are gone. The US has severely underinvested in tungsten production, so it can’t meet incremental stockpile demands at current WO3 spot prices. And China, as we’ve discussed, will likely ban more, not fewer, critical minerals.

How do I know that the US is approaching a stockpile problem? Take this Defense News article from May 2022 (emphasis added):

“Congress has repeatedly authorized multimillion-dollar sell-offs of the U.S. strategic minerals stockpile over the past several decades, but Washington’s increased anxiety over Chinese domination of resources critical to the defense industrial base has prompted lawmakers to reverse course and shore up the reserve.

The House Armed Services Committee will seek to bolster the National Defense Stockpile of rare earth minerals in the fiscal 2023 defense authorization bill, Defense News has learned. And earlier this week, the Defense Department submitted its own legislative proposal to Congress asking the committee to authorize $253.5 million in that legislation to procure additional minerals for the stockpile.

The stockpile includes valuable minerals essential to defense supply chains, such as titanium, tungsten and cobalt.”

You don’t make those types of decisions if your tap is full. Then, a few months later, in December 2022, Senator Tommy Tuberville of Alabama wrote an op-ed in the Federal Times, encouraging the US to build domestic critical mineral supply chains (emphasis mine):

Where are we getting our imports? Mostly from Russia, China, and their surrogates around the world. We’re importing these materials from one country waging brutal and unprovoked war on one of our allies and another country with a human rights abuse record that’s too long to list — not to mention the other nations they prey upon for financial and military gain.

All the while, America boasts these minerals in abundance right here. This is a disgrace — and it’s a serious threat to our national security and military preparedness.

America’s enormous mineral wealth is sitting right under its citizens’ feet in vast tracts of federal and state lands. Yet, we import more than 50% of our supply of 31 of the 35 critical minerals as defined by the Department of Interior. We import 100% of our supply of 14 of the same minerals. And our dependence on foreign countries is growing.

You don’t see these stories with full stockpiles and BFF relations with China.

Unfortunately, the US’s pending tungsten stockpile issues come when its military inventory approaches new lows.

NATO Military Committee Chair Rob Bauer recently said of US military inventory:

“The bottom of the barrel is now visible. We started to give away from half-full or lower warehouses in Europe”

We’re approaching an inflection point in tungsten supply. The US will quickly run out of stockpiled tungsten and flip from net seller to buyer over the next 12-18 months.

Moreover, there is a non-zero probability of China banning tungsten supply from global markets, just like it did germanium and gallium earlier this year.

And if I’m honest, it’s a win-win for China if they do. They’ve spent decades building domestic supply chains from raw material production to smelting and refining. The US hasn’t.

We could see 200-400% price increases if China restricts tungsten supply, as Ronald Limbaugh explained in his book Tungsten in Peace & War (emphasis added):

“The increase in supply from these sources was not enough to balance the loss of tungsten from Communist countries during a period of strong worldwide demand (Grainger, 1965; Engineering and Mining Journal, 1967). As a result, the annual average U.S. price of tungsten concentrate in 1966 was more than four times greater than that of 1963.”

As Robert Friedland said in a recent Northern Miner convention, “you would’ve needed a telescope to see these prices.”

With that said, let’s create the supply side of our model.

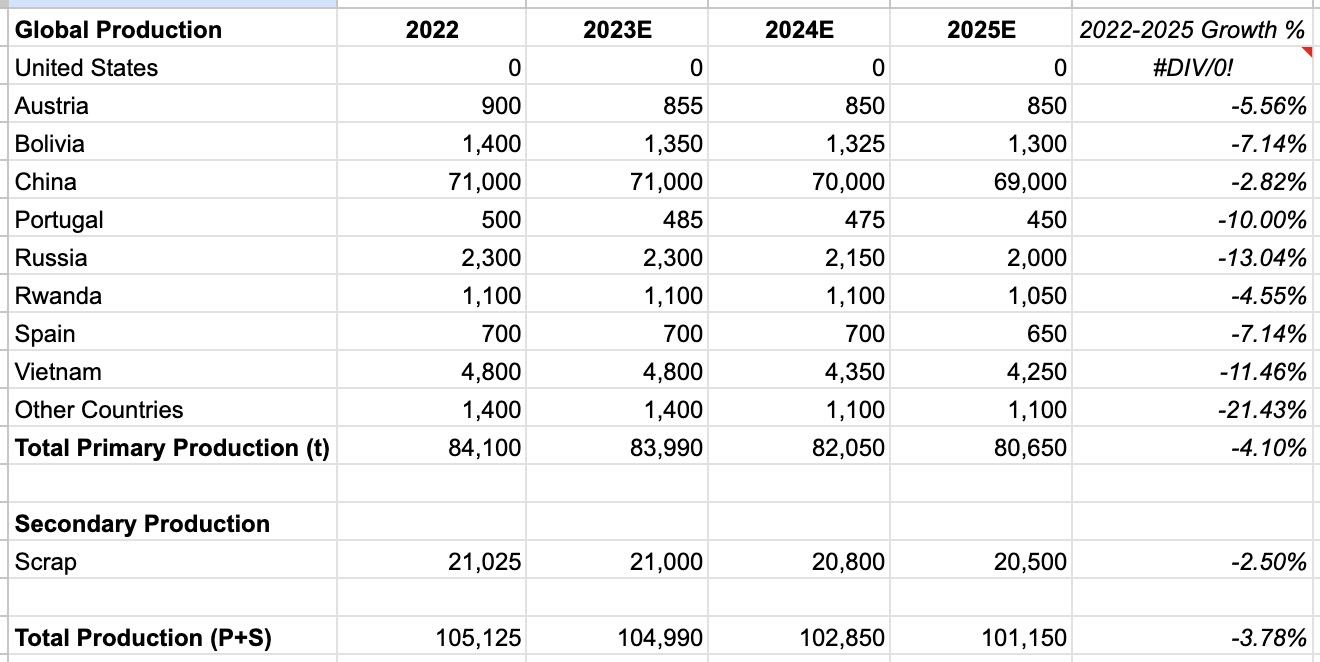

Making The Supply Side Of Our Model

We made the following assumptions in our supply-side growth model. First, we assumed that global supply would shrink by ~4% annually from 2022 to 2025 due to:

- Longer lead times for new tungsten mines

- Increased environmental regulations

- Lower grades at existing mines

- Resource nationalism

Here are the results.

There are a few things to remember about the supply model. Vietnam, for instance, relies on one mine for its entire production. Issues with that mine could result in drastic negative changes to our supply estimates.

The same applies to countries relying on artisanal methods, like Rwanda.

I should also mention that starting January 1, 2026, the US Department of Defense will implement a more widespread ban on critical mineral imports from conflict zones like China, Russia, Iran, etc. All of which negatively affect supply.

How To Update Our Supply-Side Model

The USGS Mineral Yearbook/Survey Summary provides some of the best information on global tungsten supply. But that’s an annual publication. Between releases, we can set Google alerts for “tungsten mining” or “tungsten production.”

We can also create a Koyfin watchlist for every mining company with “tungsten” in its description.

Finally, just follow the news. War outbreaks in Rwanda probably aren’t good for Rwanda’s artisanal tungsten mining operations. A flood in Vietnam might not be good for Vietnam’s only tungsten mine. China restricting half its global supply … you get the idea.

Concluding Supply

Tungsten is a small and highly opaque market, which is both good and bad. It’s good in that you can analyze every producing country within a few pages of this report. But bad in the sense that production data is often unreliable, hidden from the public, or just a plain guess.

The best we can do is get supply directionally right. We don’t need to stick it within 1-2 tons to make a lot of money off the potential deficits.

Onto demand.

The Demand Side: Primary & Secondary Drivers

Tungsten demand is pretty straightforward. As I mentioned, there are three main demand drivers:

- Military

- Semiconductors/Robotics

- EVs

Let’s start with Military Demand.

Military Demand

It’s easy to slip and write 5,000 words on every global conflict that could/would/might happen in the next 12-24 months. But I won’t. If anyone should do it, it should be Alex. So Alex, if you’re reading this, get on it!

What we can broadly say is that the world is leaning more towards global war today than it was a few years ago. Israel and Palestine. Russia and Ukraine. China and Taiwan. Three international conflicts with the US caught in the middle.

War is great for tungsten demand. So great that tungsten prices increased by 700% during World War I. Back to Limbaugh’s book (emphasis mine):

“In one two-week period of tense diplomacy in the summer of 1915, prices quoted for high-speed steel nearly doubled. As submarine warfare took its toll on Allied shipping, tungsten rose an astonishing 700% above prewar prices, dropping back later in the year after ore imports eased domestic shortages …

Lead jumped 250% in the first year of war, and then dropped 28% in the last two week sof July 1915.

Ferrotungsten, quoted at $0.60/lb in 1914, was up to $2.50/lb by July 1915. Pig iron rose from $13.75/ton in mid-1915 to $34/ton by the end of the war. Mercury jumped more than 30%.”

These price movements are possible in tungsten during wartime.

Almonty Industries (AII) published a few examples of recent military tungsten applications in its October investor presentation:

- Poland ordered 116x M1A1 Abrams tanks with tungsten armor (deliverable end 2024) + further 250 Abrams tanks (deliverable 2025/2026)

- Romania and other countries also expressed their interest in Abrams tank

- France increased the military budget by 40% for this decade

- Australia announced biggest military budget in decades

- Japan has recently unveiled an ambitious military build-up, renowned as the most significant since World War II, commonly referred to as “rearmament”

- China increased their military budget by 7% and is working to become the leader in hypersonic projectiles

All of these things point to greater tungsten demand.

If you think about it, tungsten is the perfect military metal. It’s nearly as hard as diamond, incredibly heat-resistant, boasts a high melting point, and is non-toxic. Here’s a great graphic from the University of North Texas on tungsten’s military applications.

Today, military accounts for ~10% of global demand or 8,410 tons.

Let’s shift to our second primary demand driver, Semiconductors/Robotics.

Semiconductors & Robotics

Tungsten is an ideal metal for robotic arms in heavy equipment manufacturing due to its high melting point. There’s something called an “EDM Process” in manufacturing. Which basically means that you use a spark (i.e., flame) to cut metal. The more heat-resistant and high melting point the metal is doing the EDM process, the better.

Using tungsten as an EDM process is also cheaper than using diamonds, silver, or gold.

Then there’s tungsten applications in the semiconductor industry. I had no idea, but semiconductor fabricators use tungsten hexafluoride gas to cover chips in a thin tungsten layer.

Doing this increases the chip’s conductivity while insulating it from higher temperature exposure (remember tungsten’s high melting point). The gas also allows the chips to interconnect and generate electrical signals.

We’ve covered semiconductor demand many times over the past year, so I’ll copy/paste what I wrote in our Tin Industry Primer (see below).

But take something like semiconductors. The world has an insatiable demand for more data centers, advanced AI/ML, autonomous vehicles, and wearable devices. That’s not stopping, either.

Here’s McKinsey’s latest AI Hardware report on semiconductor demand (emphasis added):

“AI applications generate vast volumes of data—about 80 exabytes per year, which is expected to increase to 845 exabytes by 2025. In addition, developers are now using more data in AI and DL training, which also increases storage requirements. These shifts could lead to annual growth of 25 to 30 percent from 2017 to 2025 for storage—the highest rate of all segments we examined.”

Let’s look at Data Center spending from 2017 to 2025E to put that into perspective. In 2017, Data Centers had a market value of ~$5-6B, split between “Inference” and “Training” data storage.

By 2025, McKinsey estimates that Data Centers will reach a market value of ~$13-15B, with $9-10B coming from “Inference” data and $4-5B from “Training” data.

In fact, we’ve been pounding the table on semiconductor demand since 2020.

Sure, technology and semiconductor demand will decline in a global recession. But the only thing that does is push the long-term thesis back 1-2 years.

Companies like Intel are spending $20B+ to build two new semiconductor foundries in the United States.

Tungsten is a direct beneficiary of the global hunger for more chips.

Finally, there’s EV-driven demand. This one’s simple. There is currently ~1.5kg of tungsten in every EV. However, that could change.

Battery manufacturers and auto OEMs are testing niobium tungsten oxide as a way to reduce charge times and increase power density within EV batteries. If successful, it would increase the required tungsten by 1kg to 2.5kg per EV vehicle.

EVs currently represent ~30% of global tungsten demand at ~25,200 tons. A change from 1.5kg per installed vehicle to 2.5kg would result in an additional ~17,000 tons of demand.

Other Demand Drivers

EVs, Semiconductors/Robotics, and Military represent 50% of global tungsten demand. The other 50% include industries like:

- Mining: 13%

- Energy: 10%

- Construction: 8.5%

- Aerospace: 8%

- Consumer: 6%

- Other 5%

We’re bullish on all of those end markets and think demand far outpaces supply over the next 2-3 years.

But let’s test that assumption as we build the demand side of our model.

Building The Demand Side Of Our Model

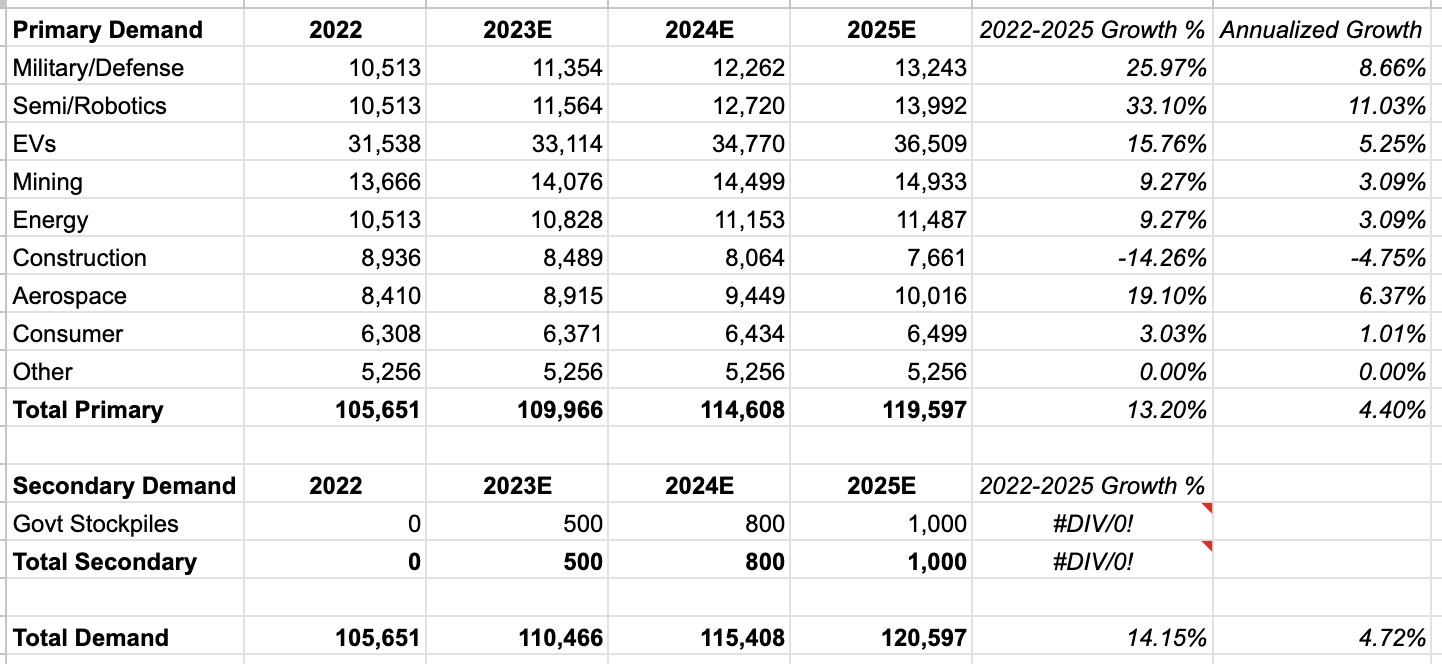

We’re making the following assumptions in our demand model:

- 9% annual growth from military/defense

- 11% annual growth from semiconductor/robotics

- 5% annual growth from EVs

- Increase to 1,000 tons of government stockpile purchases

- ~4% annual growth in total

Here are the results.

Our model shows that the demand for tungsten will increase from 105,651 tons in 2022 to 119,597 tons by 2025.

There are a few ways we can be off in our demand model.

First, we could drastically underestimate military demand at ~9% annual growth. Military demand could grow by 20-50% annually if we enter a serious military conflict.

Second, EV demand could collapse as tungsten metal adoption fails to gain traction, reducing our ~5% annualized growth to zero or negative.

Finally, overall tungsten demand could compress if we can’t get new supply online in time (i.e. if tungsten prices stay low and mines remain in care and maintenance).

Bringing It Together: Estimating Tungsten Deficits

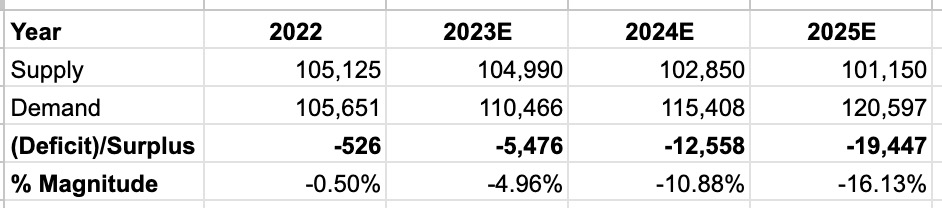

Alright, we’ve done the work to create supply and demand side models. Now it’s time to estimate future potential deficits and their subsequent magnitudes.

Here are the results from our model.

According to our model, tungsten is already in a slight deficit, and by 2025, it will be short over 19,000 tons for a 16% supply deficit.

This is a significant supply shortfall. To compare, our copper deficit is estimated at ~5%, uranium at ~12%, and tin at ~15%.

The next question is how do we play this deficit in financial markets? Like tin, there aren’t many ways to do it. Let’s dig in.

How To Play The Deficit In Financial Markets

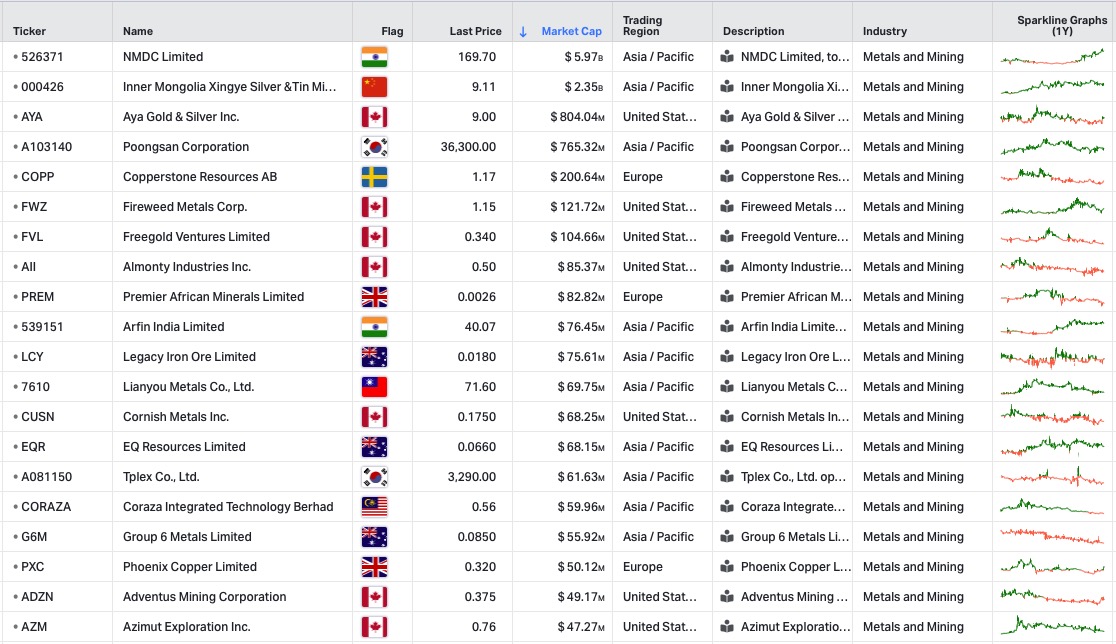

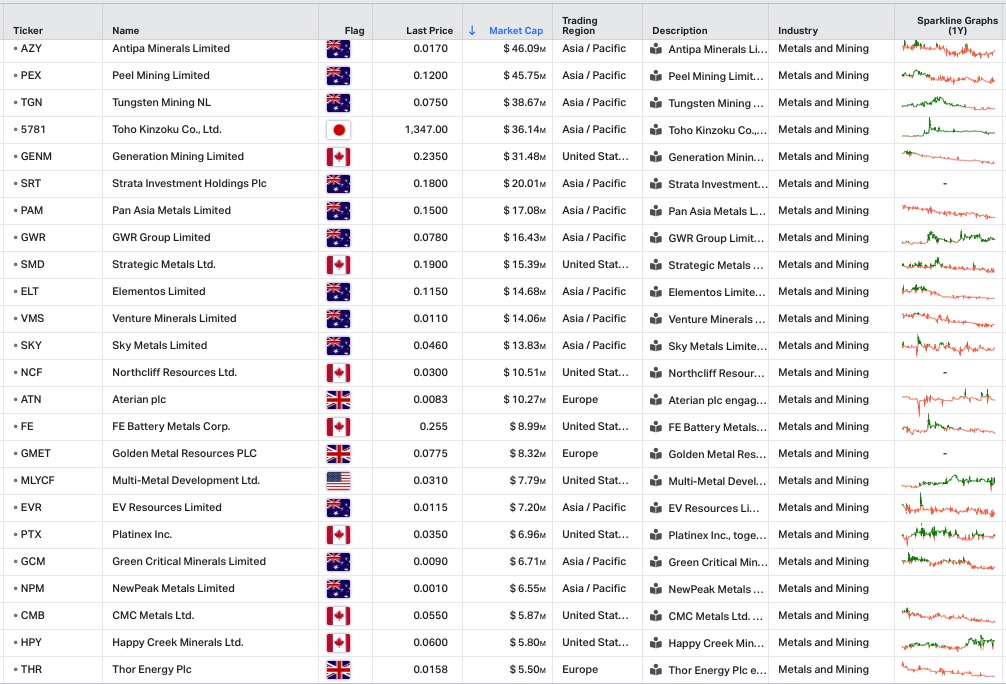

I ran a Koyfin screener for any company with the word “tungsten” in its business description (plus removing Chinese-listed companies). This gets me 45 results (see below).

I notice two things when running this screen. First, the 1YR charts are all terrible. Two of the most tungsten-focused miners are small-to-micro cap stocks trading in Australia or Canada’s TSXV.

Only a handful of the 45 names exclusively explore/mine tungsten. Most miners on the list produce tungsten as a byproduct of either silver, gold, copper, or tin.

And when I say bad charts, I mean awful charts.

These are the charts you want to see in bombed-out, capital-starved industries. It means nobody cares about these companies. They’re left for dead.

But we want a more liquid market cap to express our views. That’s why I like Almonty Industries (AII).

Almonty Industries (AII)

Almonty Industries (AII) is a pure-play tungsten miner with an $85M market cap and a $158M EV.

The company has one producing mine (Panasqueira), two current projects, one mine on care and maintenance, and another mine under construction.

There are a few reasons why I like the company. First, the CEO owns 19.50% of the common shares with a history of operating and selling mine assets at an earnings premium.

Second, the company has a 15-year offtake agreement with The Plansee Group at a floor price of $235/mtu with no upside cap. The offtake agreement alone will provide $580M in revenue at run-rate annual production levels.

Third, the Sangdong deposit in South Korea is a terrific asset. It’s the world’s largest tungsten deposit based on Inferred Resources (230,222 tons of contained WO3). It contains 3x higher average grades than Chinese deposits. And it’s in the lowest-quartile cash cost, nearly half as low as Chinese SOEs.

The other good thing about Sangdong is that it’s a past-producing asset. This means it has all the existing infrastructure and necessary permitting approvals to restart production.

AII has funded Sangdong through debt and equity issuance. The company secured project financing from KFW Ipex Bank with attractive terms:

- $75M credit facility

- 3M LIBOR/SOFR + 2.3% Interest

- 2YR Grace Period

- 6.25YR Repayment Period

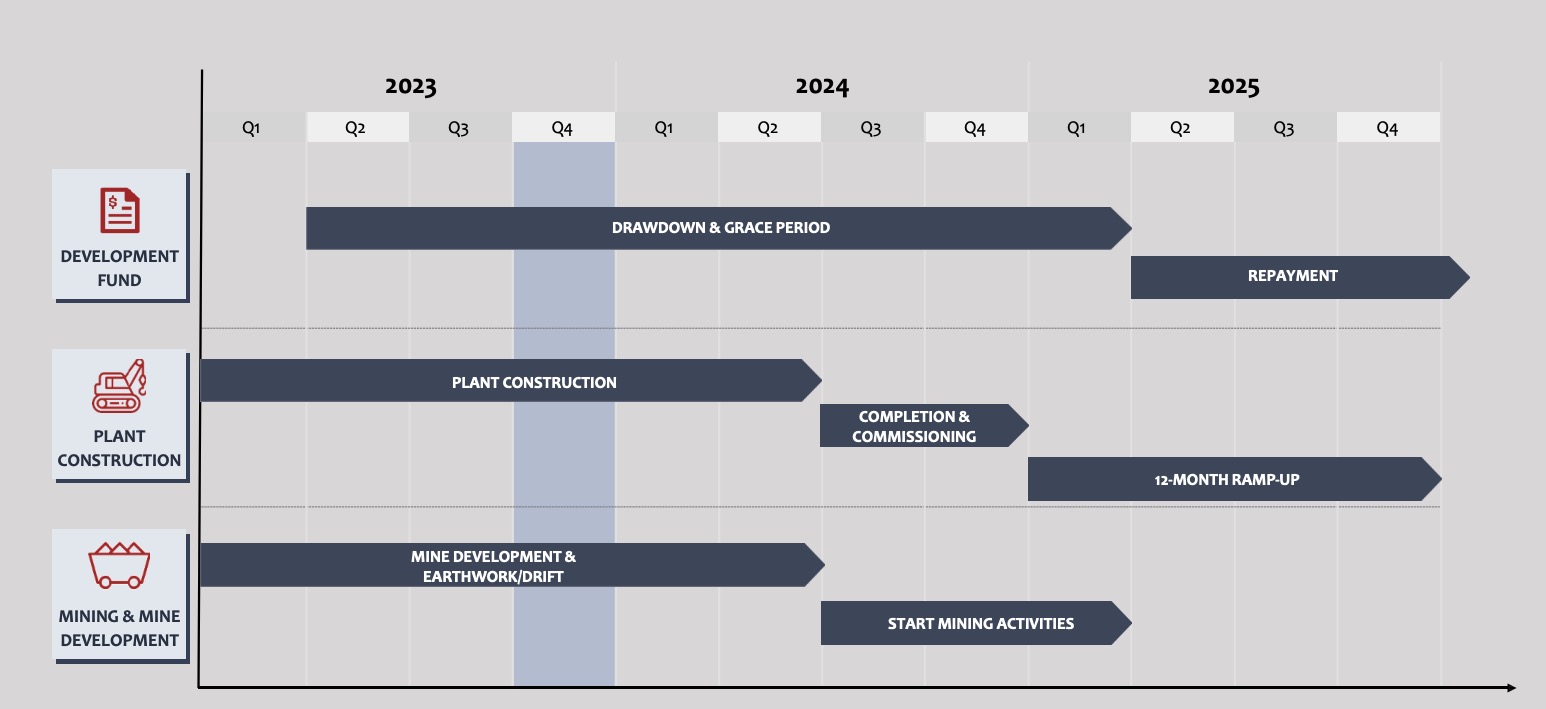

Here’s the latest Sangdong project timeline (via AII’s October 2023 presentation).

Phase 1 of plant construction should close by year-end 2023. Actual mining activities should start by Q2 2024. The LOC paydown begins at the end of Q1 2025.

So, the company has ~3-4 quarters to profitably mine and build cash reserves to meet their obligations without further diluting shareholders.

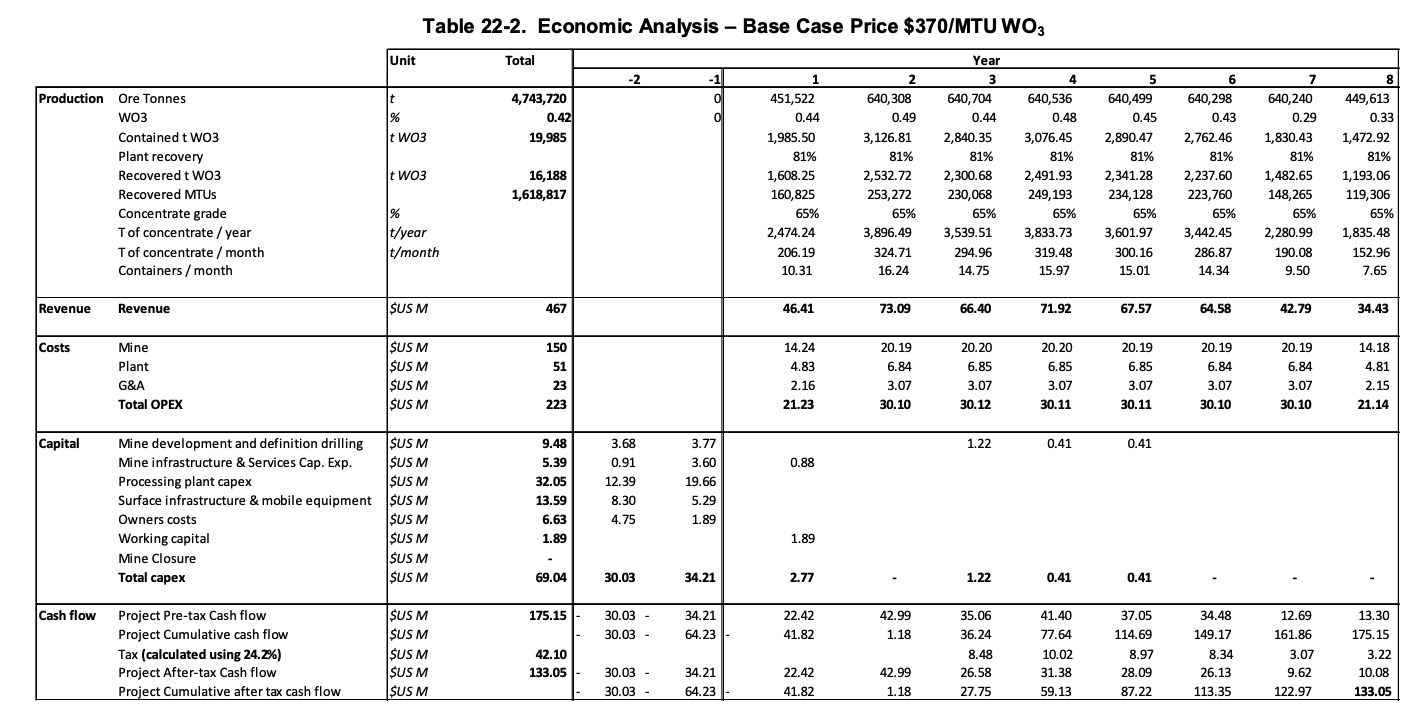

How much cash can the Sangdong mine generate? The current tungsten price is around $300-$325/mtu. AII ran its feasibility study at $370/mtu, which is higher than the current price but not unrealistic given the supply/demand imbalance we discussed earlier.

Here’s the cash flow model from the study.

AII estimates that Sangdong will generate a net cumulative $133M in after-tax cash flow.

Remember, we’re not bullish on AII because we think it will stay around $370/mtu. Tungsten prices can rise 25, 50, or even 100% in a severe supply crunch. And when that happens, tungsten producers trade at premium prices. For reference, CEO Lewis Black sold a prior tungsten producer for 21x earnings in 2007 after a supply squeeze from four years of declining production (2004-2007).

However, this is still a mining company with plenty of risks. First, the company has drawn down $50M+ on its $75M credit facility. If it needs more capital above $75M, expect it to come from share dilution.

Second, capex costs could rise as mining companies face labor shortages, cost inflation, and heavy equipment supply chain issues.

Finally, tungsten is a critical mineral with military/defense applications. There is a scenario, albeit somewhat dystopian, that the US government decides, “you know what, I think we’ll take Sangdong from here,” and nationalizes the mine.

I’m also not rushing to buy here. Yes, the stock is down 60% from its recent highs. But I want lower prices. I’ll get excited if AII hits CAD 0.35 or a ~CAD 80M market cap. At that price, you could buy the company for a ~25% cash flow yield if tungsten prices get (and stay) above $370/mtu.

Conclusion: Stalking A Capital-Starved Industry

Tungsten has all the ingredients for a massive supply/demand imbalance over the next few years. Multiple demand drivers from military/defense, semiconductors/robotics, and EVs are jockeying for more tungsten supply.

At the same time, the industry has been oversupplied for nearly a decade, and there’s no incentive to bring new capacity online at the current price. Plus, there’s the growing concern that China, the world’s largest producer, could turn off its supply at any point in the name of Resource Nationalism.

The result is an industry with a potential 19,000-ton deficit or 16% of total demand. History shows that when that happens, tungsten prices skyrocket, the miners make tons of money, and assets/deposits trade for 20x+ earnings.

Nobody’s talking about, looking at, or even thinking about tungsten. Reading this Industry Primer puts you in the top 1% of investors knowledgeable about tungsten. All that’s left is to sit and wait for the market to give us our fat pitch price.