“It is difficult to think of a major industry that AI will not transform. This includes healthcare, education, transportation, retail, communications, and agriculture. There are surprisingly clear paths for AI to make a big difference in all of these industries.” – Andrew Ng

This month we’ve dissected Artificial Intelligence (AI) and its impact on three industries:

-

- Retail

- Healthcare

- Education

We’re finishing our industry overviews with Finance. The potential applications of AI from the back to front office are astounding.

But it’s not the number of potential applications that makes us excited. AI has the power to transform the way finance companies operate. From acquiring customers to differentiating their products. Even how they gain competitive advantages over peers.

In doing so, AI will rewrite the definition of a dominant finance company. We’ll see how AI changes the meaning of assets, production, and scale through company examples.

This essay will answer three main questions:

-

- What new competitive advantages does AI bring?

- How will AI transform the finance industry?

- What are some examples of companies doing this today?

Why this matters: Tomorrow’s finance winners will look very different from the finance of old.

Why you should care: AI creates stronger competitive advantages than ever before. Tomorrow’s leaders will be the ones that recognize this shift. Adopt new technologies. Then forge deeper and wider moats around competitors.

But before we paint a picture of finance’s future, we must look at what it is today: an industry built on antiquated competitive advantages.

Note: Data presented in this essay comes from World Economic Forum

Today’s Competitive Advantages Are Tomorrow’s Value Trap

Before AI, finance companies created dominant competitive advantages via five levers:

-

- Scale of assets: economies of scale provided cost advantages (think BlackRock)

- Mass production: Standardized products and physical footprints (e.g., the most mutual fund offerings on the market)

- Exclusivity of Relationships: Firms had access to special deal-flow due to size of assets

- High Switching Costs: Keep customers because it was too difficult/expensive to switch finance providers

- Dependence on Human Ingenuity: Achieve scale through adding workers and training labor

In an AI-first world, these levers depreciate and become legacy systems. This means investors looking for the above characteristics are looking at value traps. Finance companies of tomorrow won’t need large AUMs or cumbersome switching processes.

Investing in companies on such hypotheses will lead to suboptimal performance. Not because you picked the wrong investment. But because the companies themselves weren’t equipped to tackle an AI-first future.

If you get nothing else from this essay, get this. AI transforms each legacy advantage and changes the definition of a leading finance company.

It does this by altering each legacy system to fit an AI-first business model:

-

- Scaled Assets → Scaled Data

- Mass Production → Tailored Experiences

- Exclusivity of Relationships → Optimizing & Matching

- High Switching Costs → High Retention Benefits

- Dependence on Human Ingenuity → Value of Augmented Performance

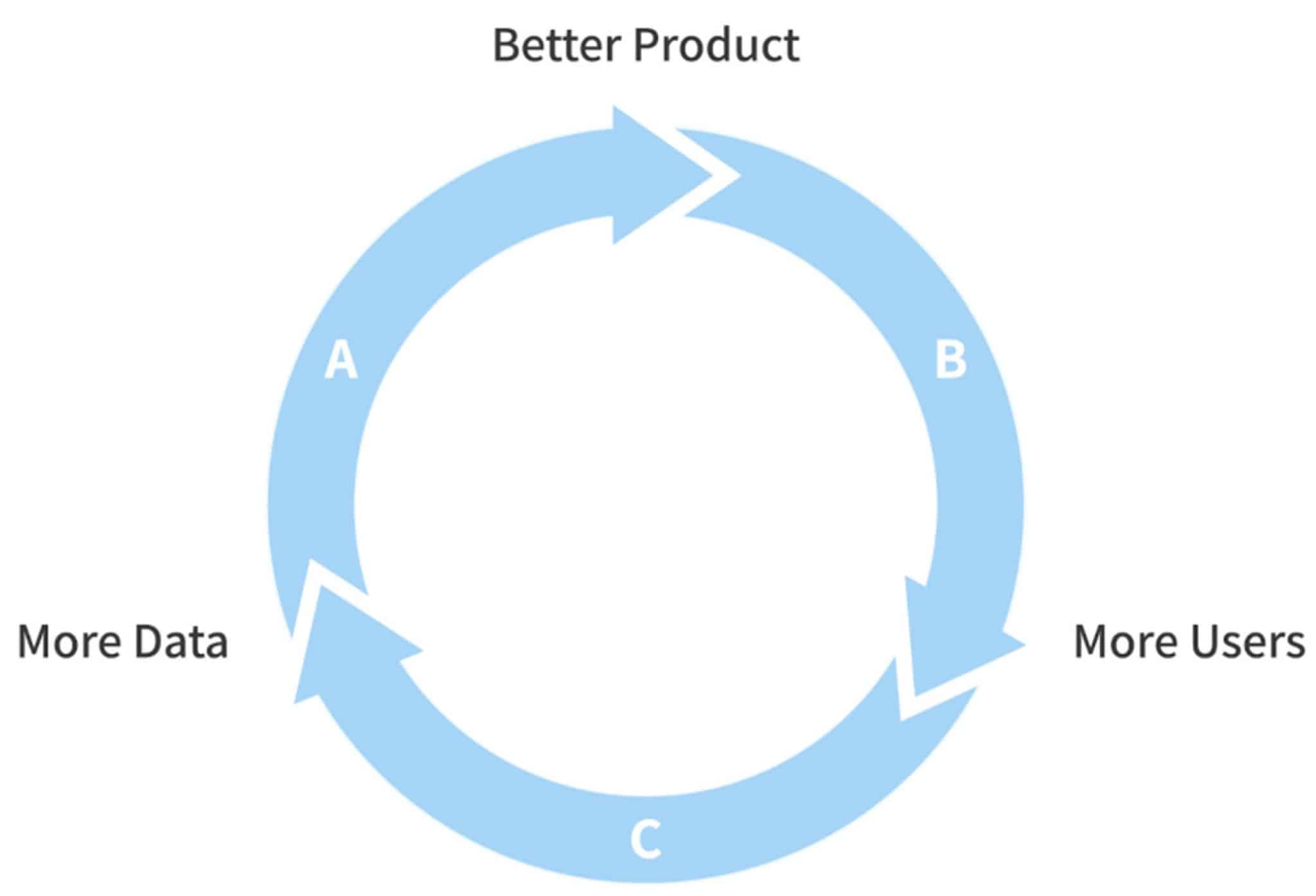

These new levers spawn defensible datasets and first-mover advantages.

This triggers a virtuous data cycle. Where better data leads to a better product. Which leads to more customers. Which brings in more (and better) data. The cycle repeats.

Let’s review our three most important levers in finance: scaled data, tailored experiences, and high retention benefits.

The Three Most Important Levers in AI Finance

Scaled Data

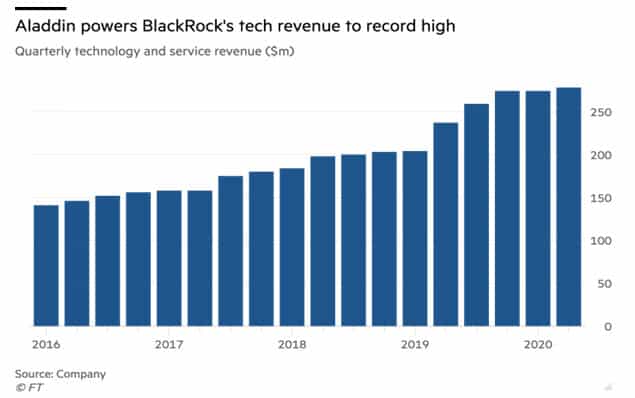

Traditionally, finance companies grew by amassing the highest AUM in the industry. Having the most money is great. It allows you to invest in R&D, hire more advisors/salespeople, and commands lower prices on investment products. BlackRock is the easiest example. The company has a mind-boggling $7.34 trillion in AUM as of 2019.

Asset levels of that size create positive feedback loops that attract even more capital. Yet a greater feedback loop exists in the world of data. BlackRock’s Aladdin is a testament to the power of Scaled Data.

According to an FT.com article, Aladdin is BlackRock’s “system [that] links investors to the markets, ensures portfolios hold the right assets and measures risk in the world’s stocks, bonds and derivatives, currencies and private equity.”

Aladdin’s asset levels are astounding. The article notes, “Today, $21.6tn sits on the platform from just a third of its 240 clients, according to public documents verified with the companies and first-hand accounts. That figure alone is equivalent to 10 percent of global stocks and bonds.”

This “central nervous system” creates new income streams for the company. Aladdin did $947M in revenue last year. BlackRock CEO Larry Fink wants BLK’s technology segment (almost 100% Aladdin) to generate 1/3rd of total revenue by 2022.

Scaled data is the first-movers paradise. Whoever amasses the most data can create the best products. That’s exactly what BlackRock is doing with Aladdin.

Having the largest dataset allows you to create new products and services others can’t match.

Tailored Experiences

Mass production made it easy for companies with large asset bases (like BlackRock) to generate high-margin revenue. Mass-produced products help spread total costs over a larger pool of units. This lowers the incremental cost to make each unit, thus raising margins.

But mass production robs larger companies of two important features: personalization and customization.

AI allows large companies to offer customized products once reserved for wide-eyed start-ups.

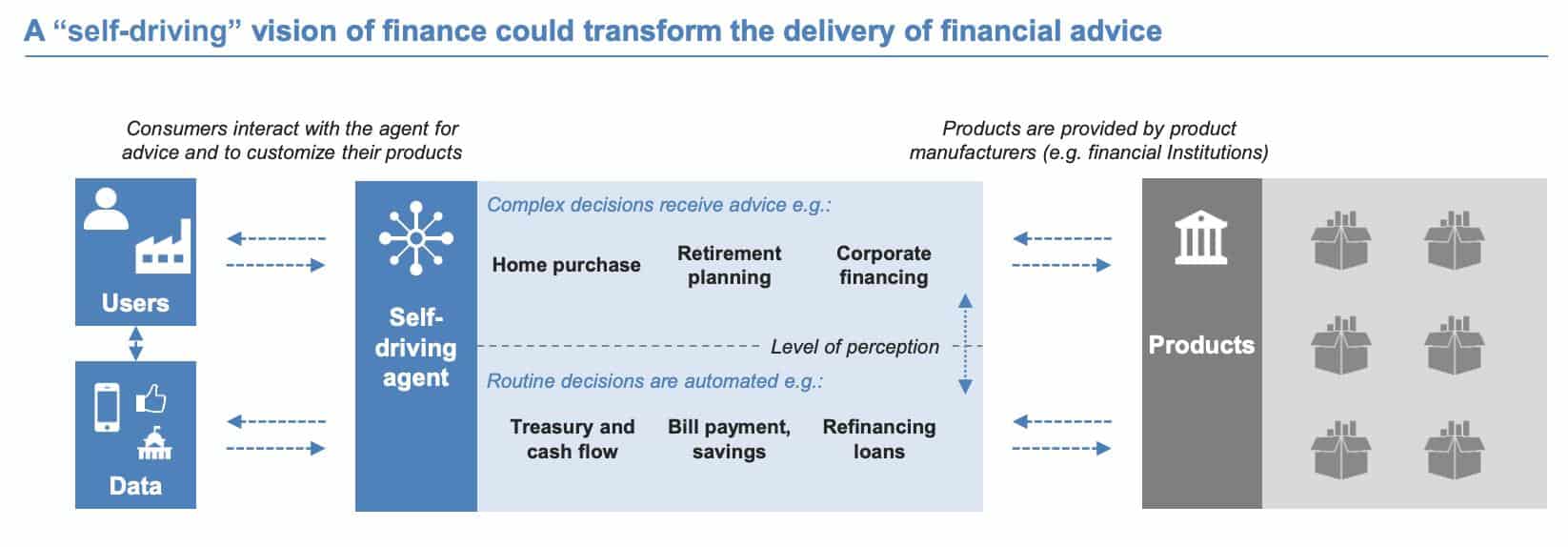

The World Economic Forum outlines this new AI-based personalized reality (emphasis mine):

“Advanced recommendation engines can be used to customize the features and price for each financial product, using data from a variety of sources, including customers, groups and third-party sources. Automated, sophisticated advice allows for a frequent, proactive and personalized service that is not economical under traditional human-based customer service models.”

Tomorrow’s leaders will create “self-driving” financial services/products. APIs and third-party platforms make this possible.

Citi does this with their new mobile app that allows customers to link third party accounts into one easy-to-read platform. Citi benefits by seeing how their customers spend money and where they can offer complementary products.

High Retention Benefits

Past financial models relied on high switching costs to keep customers. Businesses weren’t incentivized to create the best product for the customer. They wanted to make the hardest-to-switch product. This is a subtle yet powerful distinction.

Optimizing for switching costs opens the door for a more customer-centered competitor to take share. Think of TIKR/Koyfin and Bloomberg. People hate Bloomberg. In turn, they love TIKR because they almost get everything they need without the stress of Bloomberg’s UI and price.

Let’s invert that idea. Companies that optimize for superior customer outcomes faceless fierce competition.

How do finance companies achieve this? By using the first two levers (scaled data and tailored products).

Better customer data allows a company to provide customized and tailored products/services. This leads to customers spending more time and money on these products, birthing more data. This enables companies to create even more customized products and tailored services.

Customers won’t leave because they want to stay. Not because they can’t leave.

We discussed this in-depth in our post The Delta Model: How To Love Customers & Win Business. Here’s a snippet on how businesses can redefine the customer experience to lock-in high retention rates (emphasis mine):

“Brands with the best price, coolest product or most memorable marketing campaign might not have an advantage compared with those that exhibit emotional intelligence and communicate with care, honesty, and empathy, and build trust as a result. In times of crisis, people want to be seen and understood, and they are extremely sensitive to tone and motive. Are you reaching out to help them — or to sell them something? Does your outreach feel authentic and caring — or does it appear self-serving?

Here’s what we’ve learned so far:

-

- AI will transform the competitive advantages of finance companies

- Investors looking for legacy finance models are searching for value traps

- The three most important levers in an AI-based finance industry are Scaled Data, Tailored Experiences, and High Retention Benefits.

The finance companies that leverage AI will create higher barriers to entry, stronger customer relationships, and higher switching costs through customer loyalty.

Next, we’ll look at how AI attempts to solve finance’s most pressing challenges.

The Scope of AI Opportunities

According to the WEF, AI solutions fall on a spectrum from “Doing the same things, better” to “Doing something radically different”. There are five main strategies that occupy this spectrum:

-

- Leaner, faster operations

- Tailored products and advice

- Ubiquitous presence

- Smarter Decision-Making

- New Value Propositions

Let’s review each of these strategies.

Leaner, Faster Operations

Leaner, faster operations streamline mundane back-office tasks which reduce operating costs. Finance companies love this because costs matter in a commodity industry.

A great example of this is Freee (4478.JP). Freee provides back-office accounting software for small-medium sized businesses.

A great example of this is Freee (4478.JP). Freee provides back-office accounting software for small-medium sized businesses.

Another US-based company using this strategy is Bill.com (BILL). BILL provides software-as-a-service, cloud-based payments products, which allow users to automate accounts payable and accounts receivable transactions, as well as enable users to connect with their suppliers and/or customers to do business, manage cash flows, and enhance office efficiency.

Tailored Products & Advice

Like we mentioned earlier, Tailored Products & Advice are Finance companies’ weapons of choice. Consumers already enjoy personalized offerings from Facebook, Twitter, Google, and Spotify. It’s only a matter of time before they expect the same from their bank or investment manager.

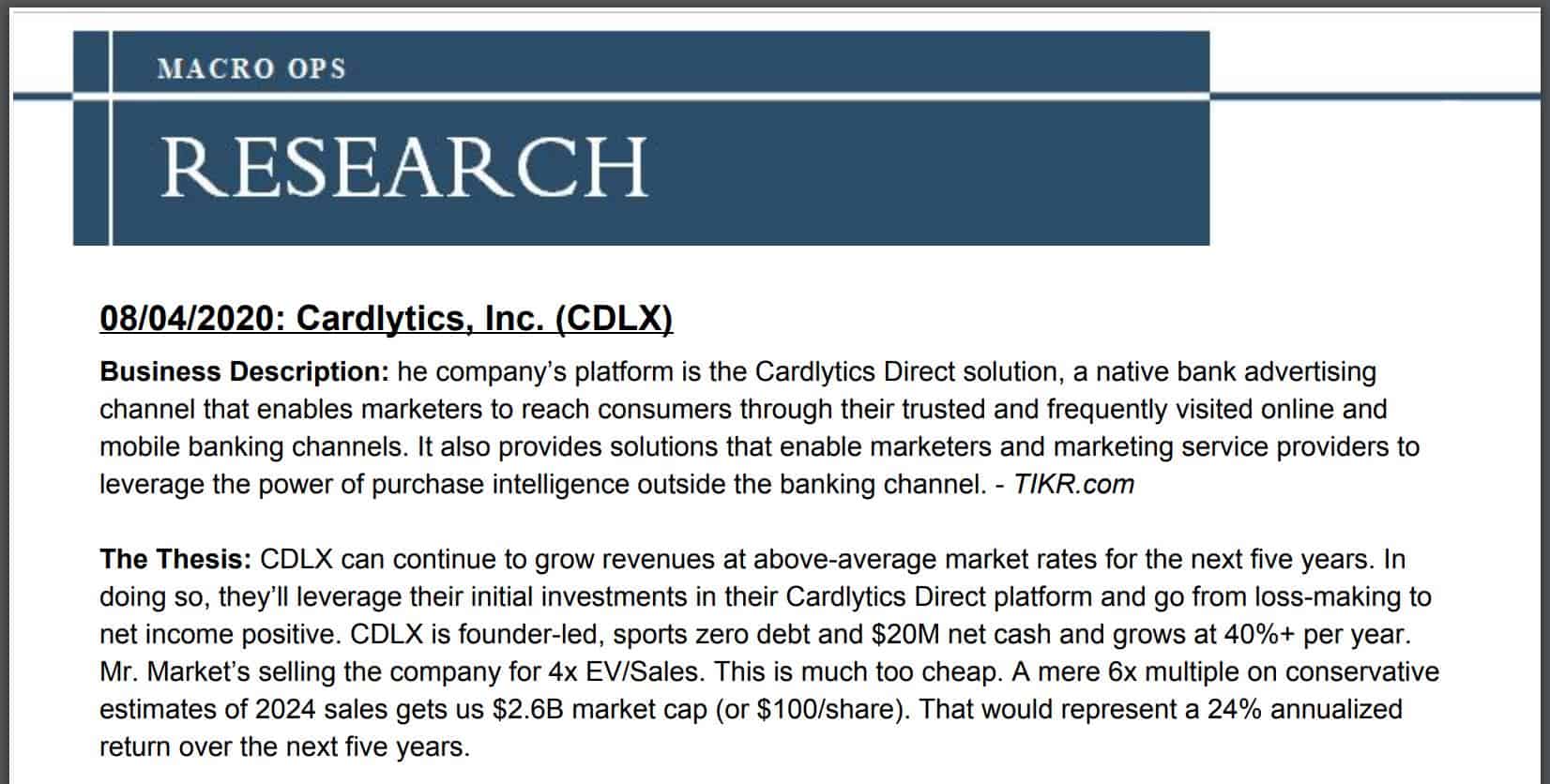

One example of this in public markets is Cardlytics (CDLX). We own CDLX at Macro Ops. Why? They help credit card companies match their customers’ actual spending habits with discounts on items they already buy.

One example of this in public markets is Cardlytics (CDLX). We own CDLX at Macro Ops. Why? They help credit card companies match their customers’ actual spending habits with discounts on items they already buy.

Tailored Products are perfect for large banks with a hand in every service (insurance, investments, loans, etc.). AI helps translate disparate data into actionable insights. This allows large corporations to create customized products by combining all product silos.

Ubiquitous Presence

Ubiquitous Presence is one of the most interesting AI finance opportunities. The WEF defines Ubiquitous Presence as (emphasis mine):

“A presence [that] allows institutions to tie directly with customers’ ongoing experiences without distracting from their end goals”

In other words, any service that’s a means to an end. Think physical credit cards. You swipe the card (the means) to get what you want (the ends).

Ubiquitous Presence admits that these processes are (for the most part) unconscious decisions. And soon we’ll stop caring what card we use as long as we get the product or service we want.

Ubiquitous Presence admits that these processes are (for the most part) unconscious decisions. And soon we’ll stop caring what card we use as long as we get the product or service we want.

This creates exciting opportunities in the world of digital-first applications. More people are using apps like Mint, Personal Capital or Acorns to track their spending. Finance companies that integrate seamlessly with third-parties will gain more customers.

It also means that more people are completing transactions and processes online. Insurance claims are a great example. Companies like Lemonade (LMND) use AI to process and pay claims in seconds. And if the AI can’t figure it out, LMND has a team of human insurance agents waiting to help.

Ubiquitous Presence is also seen in Amazon’s newest venture, Amazon Go. Amazon Go is a revolutionary grocery store experience. There’s no check-out line. No cashiers. You don’t even have to pay at the store. Everything’s done through your Amazon account.

More companies will do this because the opportunity to capture customers at the point of ubiquity is enormous. What’s stopping Visa or Mastercard from partnering with leading omnichannel retailers?

Here’s what that reality could look like. You walk into a Best Buy or Bed Bath and Beyond. Find your item. And walk out because those stores partner with Visa’s omnichannel program.

Smarter Decision-Making

I heard Andrew Ng, a pioneer in AI, on a podcast (the name of which escapes me) discuss the most basic definition of machine learning. He said (and I’m paraphrasing). “Any time a machine, computer, or algorithm takes data as an input and tries to make predictions off that data. That is machine learning.”

Making smarter decisions is the entire point of machine learning. We wouldn’t risk creating a real-life Terminator if that wasn’t true, right?

There’s myriad ways to make smarter decisions in finance applications:

-

- Insurance companies better manage risk parameters

- Third-party data collection companies drive better insights

- Trading departments leverage AI to reduce cost of trade execution

A good example of a company leveraging AI to help other companies make smarter decisions is Riwi Corp (RIW.TO). The company provides real-time, proprietary data from 220 countries around the world. Companies can purchase this data as a service and use it to make better decisions about trades, public policy, or product placement.

New Value Propositions

If semiconductors obey Moore’s Law, finance companies bow at the feet of arbitrage. It’s hard enough to compete in an industry dominated by lowest-cost providers and commoditized product offerings. But with AI, finance companies can rise against arbitrage. They can create new investment strategies from differentiated datasets.

In short, new value propositions will come from new ways of using either existing data or new data. Breakthroughs will happen at the insight and application layer.

We’re seeing this in the ETF space where companies create ultra-niche thematic ETFs or “smart beta” strategies.

Conclusion

The number of AI applications in finance is exhilarating. As an investor, I can’t wait to see what new business models and strategies come out of this industry breakthrough. AI will change what it means to be a dominant finance company.

The old model of growing assets, mass-producing products, and creating frustration-based switching costs are over. Scaled data will create tailored experiences for customers which will translate to high retention benefits and a virtuous competitive cycle.

If you liked this essay and want to learn more about AI and its impact on other industries, give these a read: