Hope you’ve had a great week so far! Lots going on in the value corners of the markets. As always, we’ve got a bunch of Q4 Letters to roll through.

But before we do that, check out my latest podcast with Cliff Sosin of CAS Investment Partners. I had a blast listening to Cliff spout off knowledge bombs. It’s over 2 hours, so strap in and brace yourself.

-

- Episode 11: Clifford Sosin, CAS Investment Partners

Episode 11 is fast becoming one of the all-time most listened episodes. Granted, we have a whopping eleven. But hey, we’re growing! I’m excited to bring you this week’s episode. We’ve got a great guest!

Also, if you have the time, please subscribe and leave a rating/review of the podcast on Apple Podcasts. It goes a long way in spreading the word about the show. The larger the audience, the better the guests, the better the content. Help spur that flywheel!

With that out of the way, here’s the letters we’re dissecting this week:

-

- Maran Capital

- Pershing Square (Presentation)

- Laughing Water Capital

We also have Morgan Housel’s latest long-form piece.

This should be a doozy!

—

February 12, 2020

Richest Man Despite a Divorce: Not sure what I did in a past life, but I found myself watching the Oscar’s last night. I know, I feel ashamed. I watched long enough to hear a tremendous Jeff Bezos roast from Chris Rock. Rock spotted Bezos in the crowd and said, “Jeff Bezos is so rich, he got divorced and he’s still the richest man in the world. He saw ‘Marriage Story’ and thought it was a comedy.”

I couldn’t tell you who won what, but I laughed at that.

__________________________________________________________________________

Investor Spotlight: Keep Them Letters Coming!

GIFs by tenor

GIFs by tenor

We’ve got three great letters to dive into. The process stays the same. We’ll review the high-level theme of the letter, and then discuss each investment mentioned.

Dan Roller, you’re up!

Maran Capital Management: +24.8% in 2019

Dan Roller’s Fund returned 9.5% in Q4 and 24.8% in 2019. The Fund is unconventional, as Dan wrote in the first paragraph, saying (emphasis mine):

“Maran Capital Management is an unconventional investment manager. I feel that it needs to be, as it is aiming for unconventional — that is, superior — results.”

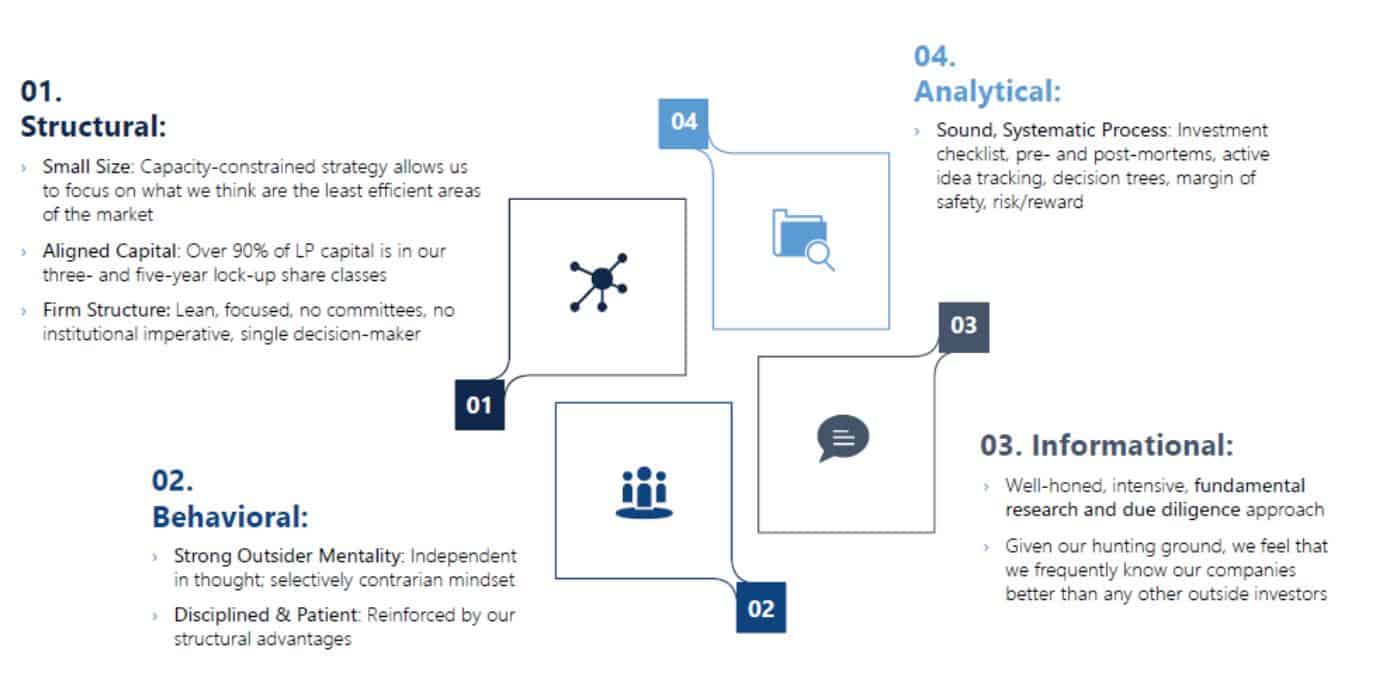

WIthin this unconventional structure, Dan sees four distinct competitive advantages:

-

- Structural (i.e., small size)

- Behavioral (i.e., disciplined & patient)

- Informational (i.e., intensive, fundamental research)

- Analytical (i.e., sound, systematic process)

Here’s the infographic of each advantage:

Dan mentions four companies from his top five holdings:

-

- Clarus Corp (CLAR)

- Ranger Energy Services (RNGR)

- RCM Technologies (RCMT)

- Scott’s Liquid Gold (SLGD)

Let’s figure out why he likes them …

Clarus Corp (CLAR)

Dan thinks CLAR has the potential to be a multi-bagger. Here’s his take (emphasis mine):

“The balance sheet is clean, and the aligned management team is comprised of great operators and skilled capital allocators. I believe fair value today is in the high teens; my five-year base-case valuation is $35/sh, and my five-year upside case is $45/sh.”

Let’s check out the chart …

Catalysts for future growth (per letter):

-

- Black Diamond Equipment improving margins and revenues

- Potential growth in apparel and footwear segment

- Sierra Bullets segment

Ranger Energy Services (RNGR)

Here’s what Dan likes about RNGR:

“Ranger is an off the beaten path domestic energy services company trading at a very cheap price. It is illiquid, small cap, and a ‘broken’ IPO, yet has high insider ownership (60%+), is well run, taking share, gushing cash and buying back stock.”

It’s hard to disagree with Dan’s thesis when the company’s doing numbers like these:

-

- Run-rating ~$50M of EBITDA ~$30M FCF

- Currently trades ~3x EBITDA and 30% FCF yield to equity

- Trades at ~0.5x tangible book

Maran believes RNGR has around 100% – 300% upside under various scenarios. Let’s go to the charts …

Scott’s Liquid Gold (SLGD)

Maran holds over 5% position in SLGD. The letter doesn’t dive into specifics on SLGD, but here’s some quick highlights:

-

- Market Cap: $28M

- EV: $23M

- EV/EBITDA: 7.8x

- Gross Margins: 35%

Here’s the chart …

———————————-

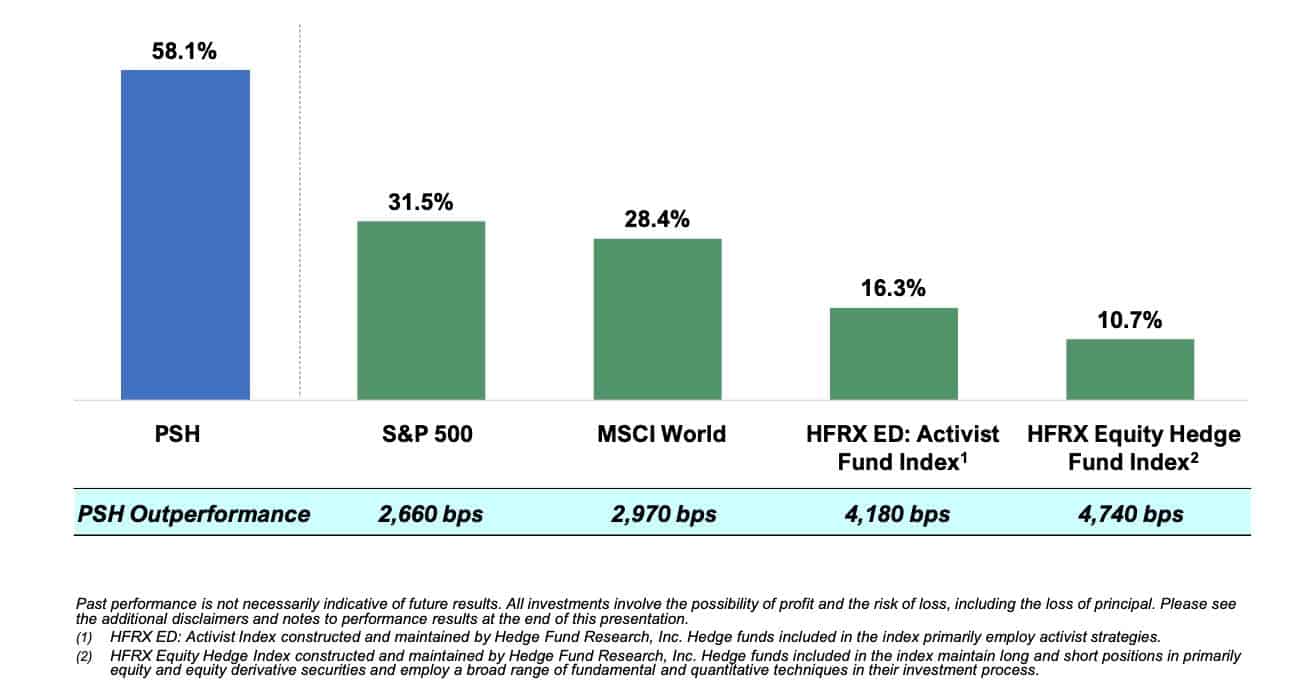

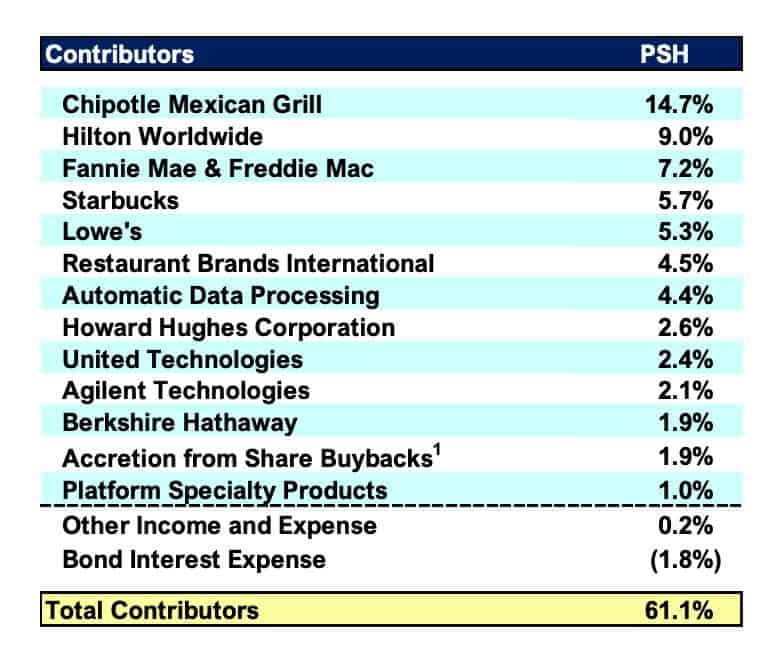

Pershing Square Capital: +51.2% in 2019

Bill Ackman killed it in 2019. Pershing increased NAV 58% and returned 51.2% for shareholders. Not bad. On the heels of such increases, Pershing initiated a 2% dividend yield, similar to the S&P 500.

The Fund (PSH) also bought back $224M in shares between June 2019 and Feb 4, 2020.

PSH beat the S&P by 2,660bps. And it was the fifth time PSH generated net returns of 39% or higher:

So which companies contributed to PSH’s returns?

All of them.

Yep. And to make sure that you know, PSH put a slide in their deck that reads:

“We did not have any detractors in 2019. Every portfolio company generated positive returns.”

Flaunt it when ya got it, I guess? Either way, here’s the return breakdown for Ackman’s holdings:

Let’s take a look at Ackman’s latest investment, Agilent (A).

Agilent (A)

Agilent is a leading analytical measurement company. They sell instruments, consumables and services to identify, quantify and analyze molecular properties of substances / products.

Here’s the quick-hit financials:

-

- Market Cap: $26.2B

- Enterprise Value: $27B

- EV/EBITDA: 20x

- Gross Margin: 54%

- EBIT Margin: 20%

Ackman believes shares are undervalued for two main reasons:

-

- Margins can expand

- Underlevered relative to peers

Agilent sports 25% EBITDA margins, which is good. But not as good as their peer Waters (WAT) which does 35%.

Also, the company’s Net Debt / LTM EBITDA rests at 0.8x. Yet its peers have an average of 3x leverage.

Here’s the chart …

Congrats to Ackman’s stellar 2019. Hopefully he continues his success in the years to come.

———————————-

1 Main Capital: +25.2% in 2019

Yaron Naymark runs 1 Main Capital Management. If you haven’t already, follow him on Twitter. He adds tremendous value to your timeline. Anyways, back to the letter.

1 Main Capital returned 12.4% in Q4 and 25.2% for the year. Since inception, the Fund’s returned 10.7% compared to 19% for the S&P 500 and 8.5% for the Russell 2000.

Top contributors to the Fund’s performance included:

-

- Alphabet (GOOG)

- Altigen (ATGN)

- Hemacare Corp (HEMA) — Exited in Q4

- KKR & Co. (KKR)

- Mastech Digital (MHH) — Exited in Q4

- Sanofi Contingent Value Right (GCVRZ) — Exited in Q4

- Total Site Solutions (TSSI)

At the end of the year the Fund’s top five positions were:

-

- Issuer Direct (ISDR)

- KKR & Co. (KKR)

- MasterCraft Boat Holdings (MCFT)

- RCI Hospitality (RICK)

- Total Site Solutions (TSSI)

The top five positions accounted for ~45% of the Fund’s assets.

Let’s break each down.

Issuer Direct (ISDR)

ISDR is a communications and compliance firm that helps corporate issuer clients disseminate information. Why is ISDR interesting? They’re switching from a project-based revenue model, to more of an annual platform style. Here’s Yaron’s take (emphasis mine):

“Over the last few years, the company has been in the process of transitioning its business model away from project-based engagements to annual platform subscriptions, which has in turn increased the predictability of the business but has also temporarily suppressed revenue growth. Additionally, in the last year, the company was impacted by the rapid decline of its investor commentary business.”

On top of that, the company’s core business (ACCESWIRE) grew 70% in Q3 and 40% YTD.

Before we get to the charts, here’s the quick-hit financials:

-

- Market Cap: $44M

- Enterprise Value: $29M

- EV/EBITDA: 20x

- Gross Margin: 70%

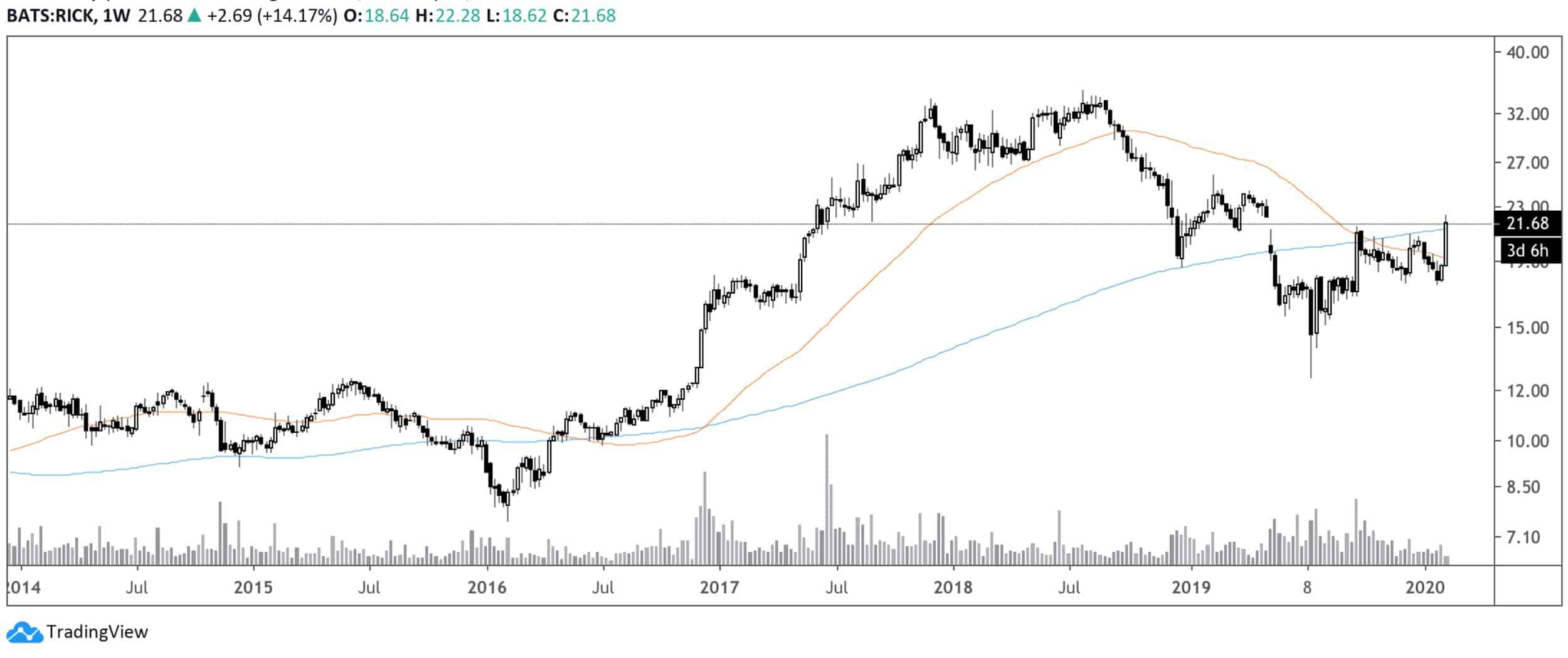

RCI Hospitality (RICK)

RICK is the Fund’s largest position going into 2020. According to the letter, it’s been a drag on performance since inception. There’s reasons for the performance drag, as Yaron explains:

“As we sit here today, RICK is late to file its annual 10-K with the SEC for the third time in as many years, had its auditor resign late last year and is under formal investigation by the SEC regarding a series of negative articles published about the company by an anonymous short seller. “

Ouch. So why did 1 Main add to this investment? Here’s 1 Main’s take:

“To summarize, based on the company’s valuable assets, capable management team and strong cash flow, I have a tough time seeing how we lose much and can easily see us making multiples of our capital in this investment in the coming years.”

The company has around $200M in owned real estate and trades at 5x FCF. The little debt they have is covered by that significant cash flow generation. Will it be enough to overcome the accounting speed-bumps and short seller reports? Time will tell.

Here’s the chart …

Total Site Solutions (TSSI)

TSSI provides services for the planning, design, deployment, maintenance, and refurbishment of mission-critical facilities in the United States. It operates in two segments, Facilities and Systems Integration.

Here’s why 1 Main Fund likes the company:

“Today, the company is focused entirely on the modular data center market. Modular data centers allow its users to scale their capacity over time on an as-needed basis, compared to traditional data centers which require much more capital investment for greater upfront capacity than is needed today. This allows for a steadier pipeline of service work for clients, who require ongoing planning, configuration, rack construction, server integration, deployment and maintenance.”

Check out the quick-hit financials:

-

- Market Cap: $24M

- Enterprise Value: $22M

- Forward EV/EBITDA: 2.8x

- Gross Margins: 36.5%

Here’s the chart …

__________________________________________________________________________

Resource of The Week: Nothing is Inevitable

GIFs by tenor

GIFs by tenor

Sorry, Thanos. According to Morgan Housel, you’re not. In fact, nothing is. And that’s the point. Housel’s latest piece, History Is Only Interesting Because Nothing Is Inevitable, sheds light into this phenomenon.

Housel uses history to paint a picture of the laughable arrogance of humanity’s hindsight bias. Take this quote for example (emphasis mine):

“That stuck with me. Here we are, bloated with hindsight, knowing the crash after the roaring 1920s was obvious and inevitable. But for those who lived through it – people for whom the 1930s was a yet-to-be-discovered future – it was anything but.”

Going further, Housel notes that in the heat of the moment, people weren’t worried about a Depression. They celebrated in the prosperities of America:

“When we look back at the late 1920s we think about crazy stock market valuations and shoe-shine boys giving stock tips. But that’s not what people paid attention to at the time. The newspapers are filled with charts like these: rational, level-headed, and fuel for optimism.”

The entire paper’s worth the read.

__________________________________________________________________________

Tweet of The Week: Less Instagram, More Reading. More Writing.

The average Instagram user spends 21 minutes on the app per day.

That’s almost *128 hours per year.*

The people doing this will also tell you they have “no time” to read, to write, to workout.

Reading, writing and lifting have become a huge source of competitive advantage.

— Ryan Stephens 🥃 (@ryanstephens) February 11, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!