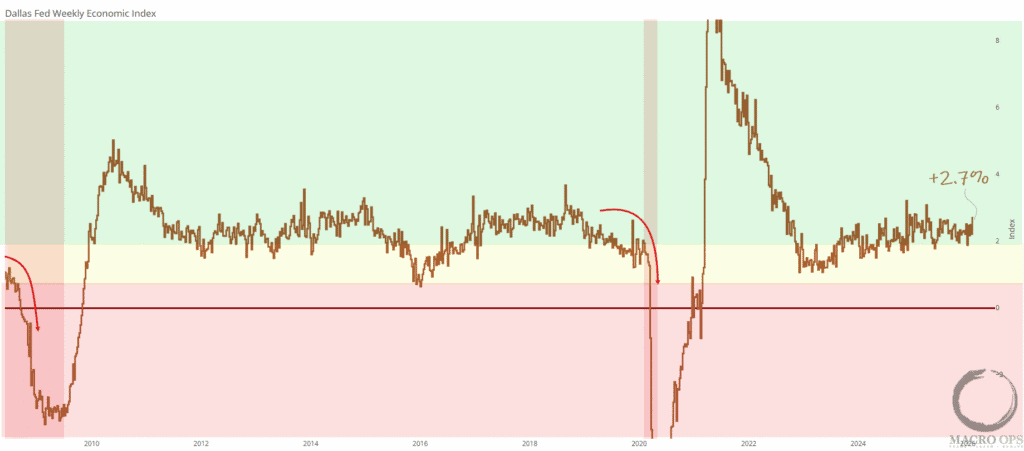

Summary: A breakout failure, hawkish Warsh surprise, weak seasonality, and High Trend Fragility suggest odds favor a sentiment washout is on the table. But strong breadth and internals indicate any correction should remain contained, sub -7 %. Stagflation risk is rising for the second half, bonds remain precarious, and energy names are showing strength.

***The MO port finished 2025 up +50.8% and is currently up +24.6% ytd in 26’. If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the below and sign up. We look forward to seeing you in our Slack!***

Join The Collective

1. ES continues to compress after a bullish breakout failure last week in the March contract. This failure, coupled with the high Trend Fragility / BofA Bull-Bear Sell signal, and slightly negative Warsh Fed announcement, put it odds on that the market is headed for a positioning/sentiment rinse during this seasonally weak month of Feb.

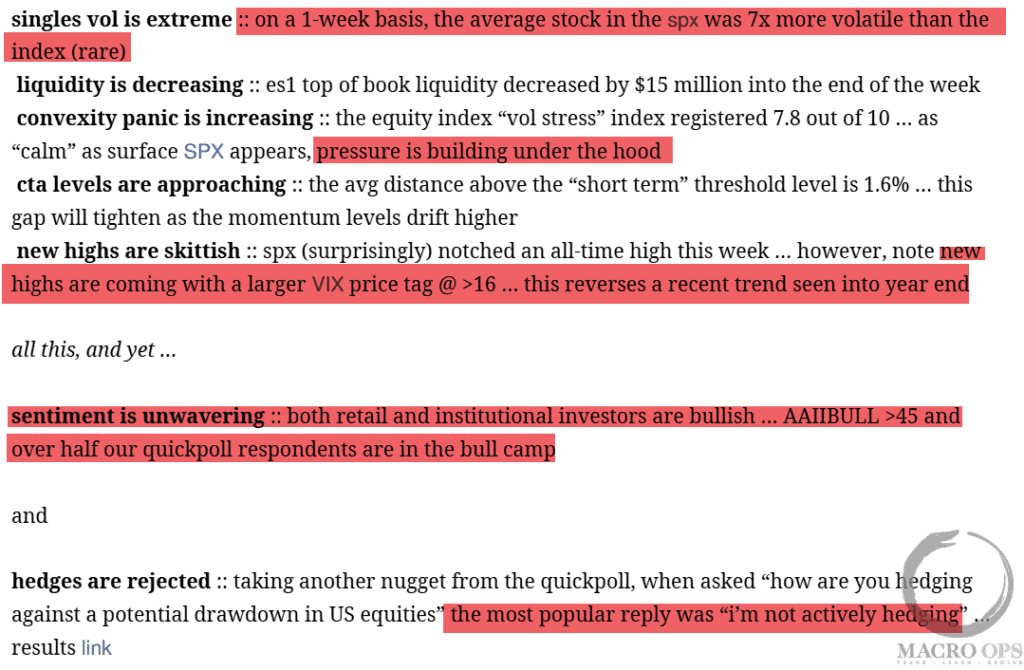

2. Some interesting points from GS over the weekend (emphasis by me)… sentiment is unwavering… I’m not actively hedging.

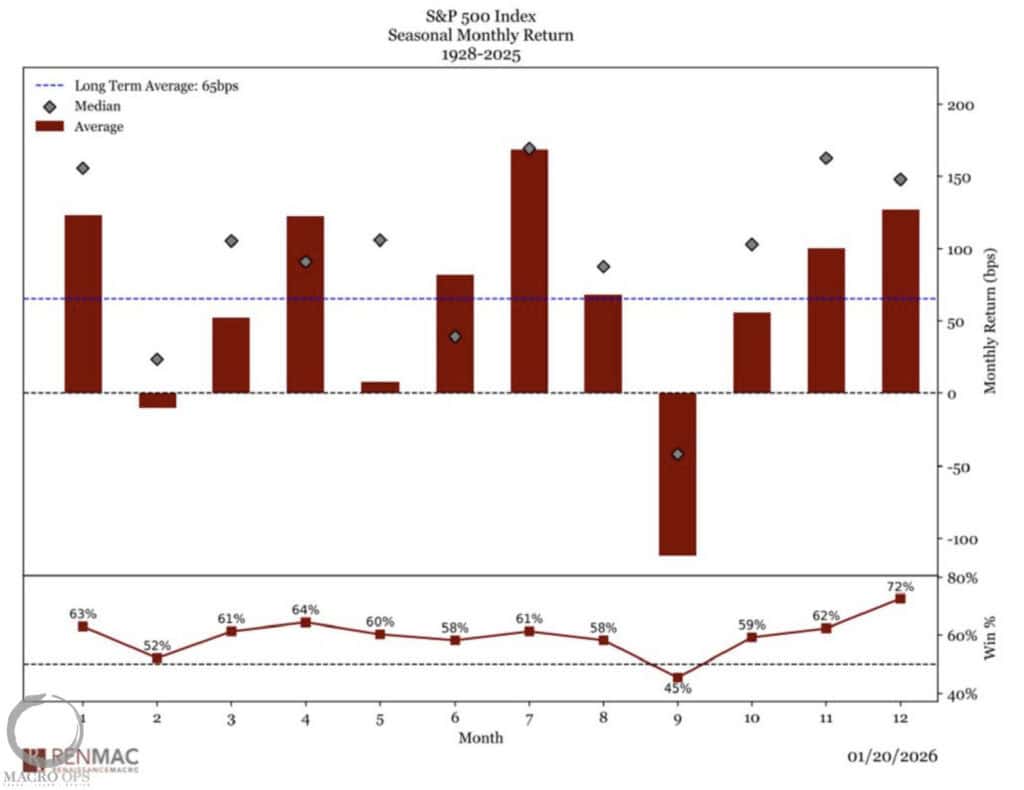

3. February tends to be the second-worst-performing month for the SPX (chart via @RenMacLLC.

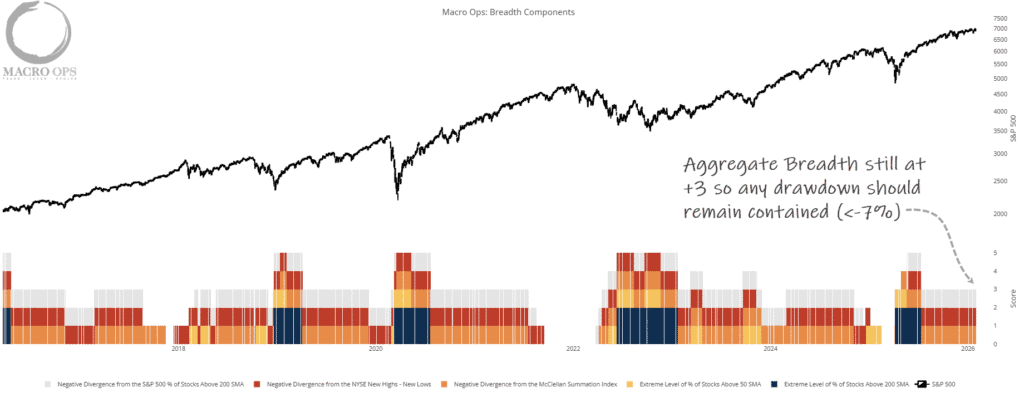

4. However, as we pointed out last week, the strong aggregate breadth and supportive internals suggest any selloff should remain relatively contained (sub -7%).

We shorted Qs and ETHUSD last week to hedge our remaining long exposure.

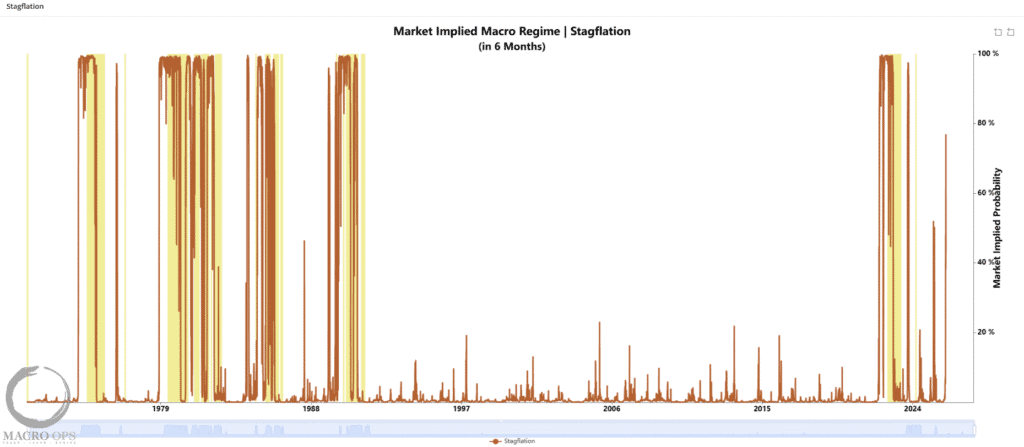

5. This is interesting… Our Market Implied Regime Indicator has risen to 80% for a Stagflation Regime—a reading over 90% has a 100% hit rate in forecasting a Stagflation Regime within 6-12 months. Stagflation is defined by an ISM of 53 or lower and a Sticky Price CPI exceeding 5%.

6. Now, as we’ve pointed out, we expect CPI to fall over the next 3-6 months due to the pure mechanics of falling shelter costs. But it’s interesting that we’re starting to see some of our inflation leads turn up, lending weight to what our regime indicator is projecting (click on charts to enlarge).

7. So we’ll continue to track things and see if our regime indicator passes above the 90% mark, ensuring an inbound stagflation regime starting sometime in the second half. Historically, precious metals have been the best-performing asset in a stagflationary regime, so PMs could become highly attractive again, especially if they spend the next 6+ months weeding out the weak hands.

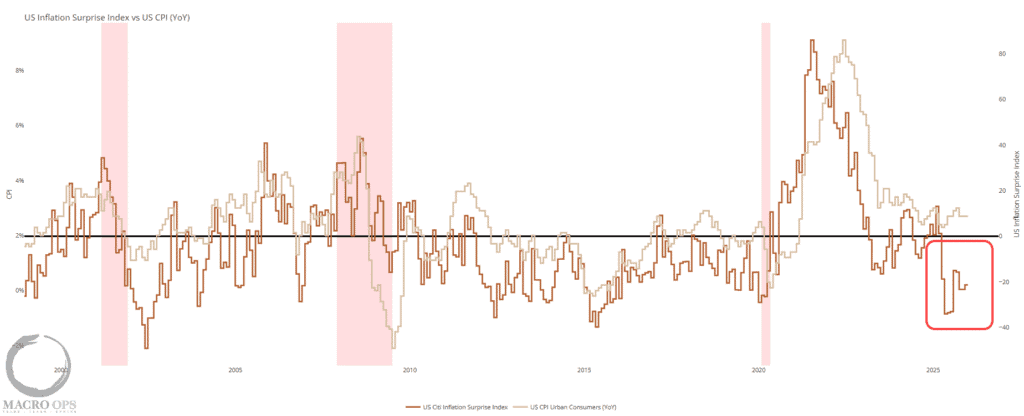

Citi’s Inflation Surprise Index continues to come in deeply negative, however, giving weight to our first-half disinflationary bent.

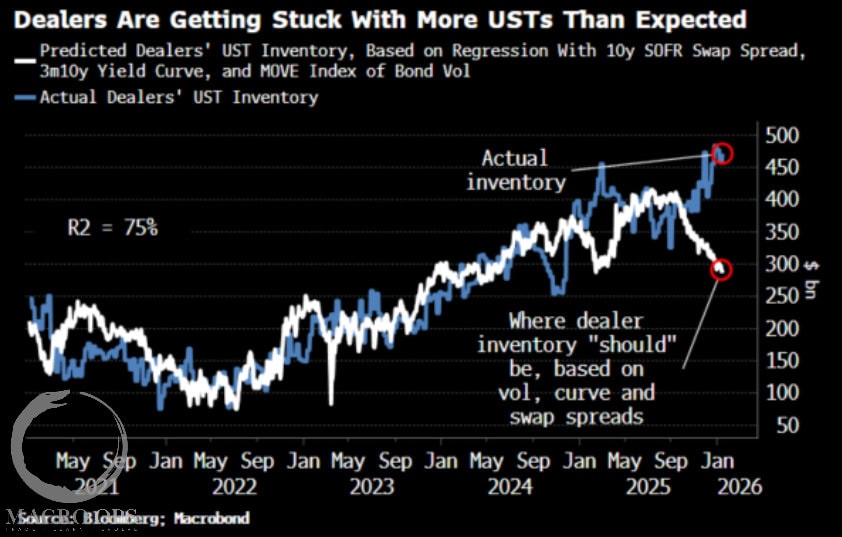

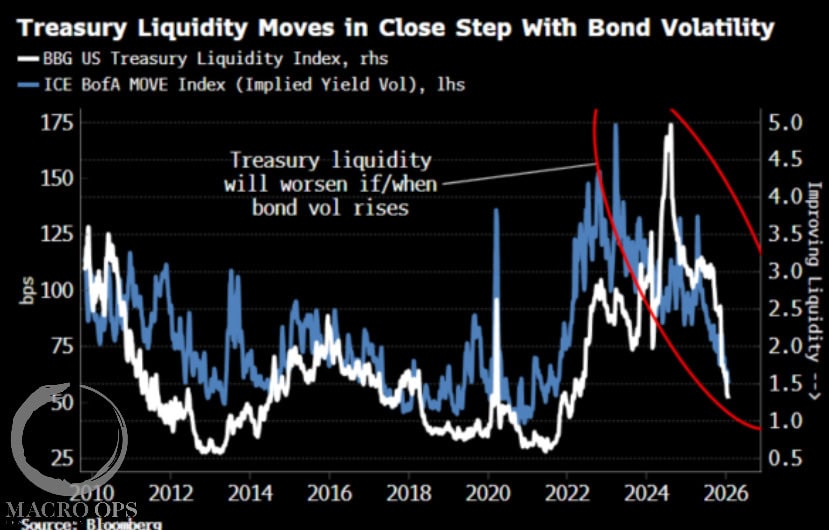

8. BBG’s Simon White put out a great note last week highlighting that dealers are becoming “reservoirs of risk” by carrying record equity leverage alongside nearly $500 billion in unsold Treasuries. And this balance sheet congestion is currently hidden by low bond volatility, but it leaves dealers at maximum capacity and highly vulnerable to any sudden market shock.

9. His concern is that if bond volatility spikes, these overextended dealers would likely pivot from providing liquidity to aggressively shedding risk. Which could trigger a forced, cross-asset deleveraging event where the rapid dumping of stocks, bonds, and metals leads to a cascading collapse in global liquidity.

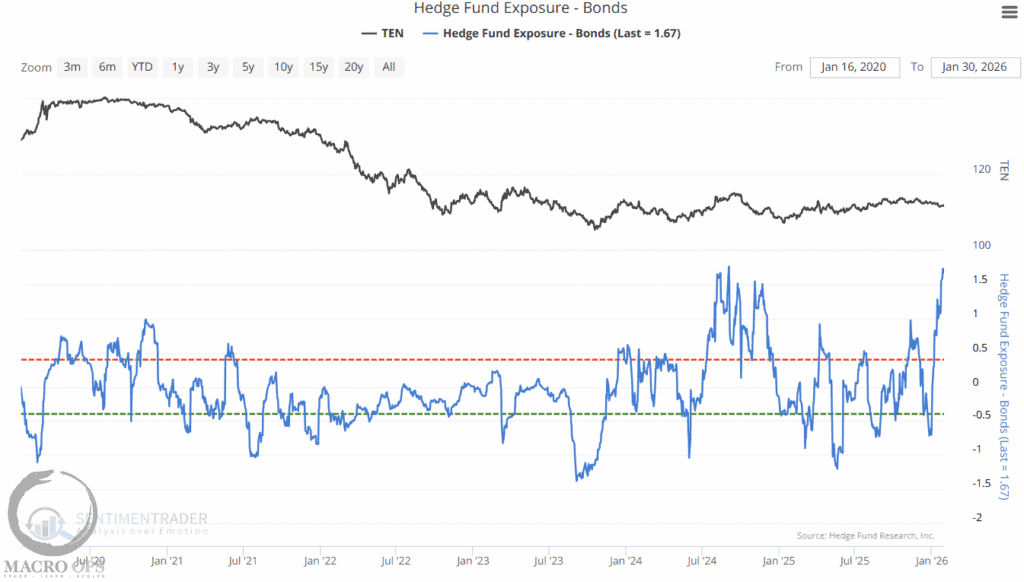

10. Speaking of bonds, Hedge Fund exposure to them is at record highs, according to SentimenTrader.

11. Last week, we highlighted the major compression regime in bonds on the monthly chart. We’ve been trading in and out of this one on the short side. Ultras have completed a large H&S pattern and have been consolidating in a 2-month rectangle below the neckline. My bet is that we see this one break lower soon.

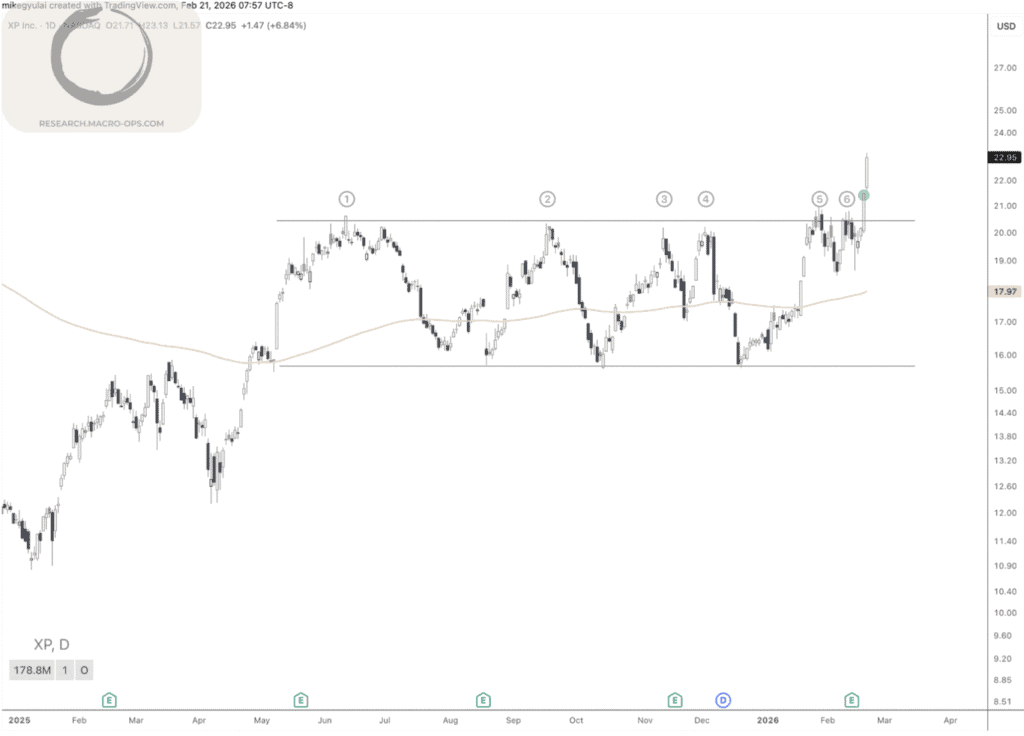

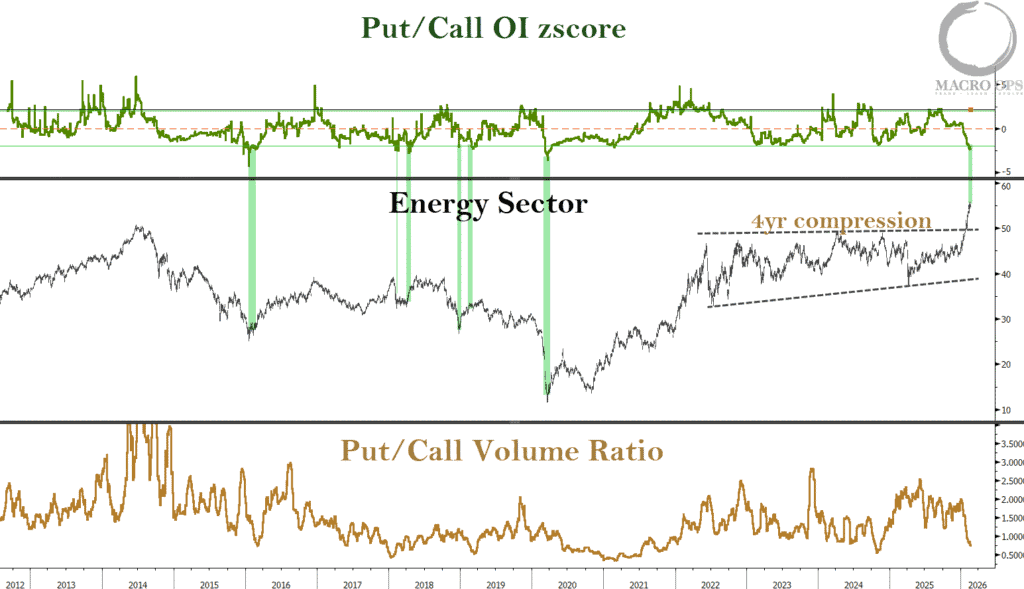

12. Over the past two months, we’ve steadily accumulated long energy positions, capitalizing on historic bearish extremes in crude sentiment and mounting sector relative strength. Chevron (CVX) has just broken out from a five-year compression rectangle with a decisive monthly bar. We’ll likely be adding this one to our port soon.

Join The Collective

Thanks for reading.