Private equity outperforms public markets. Unfortunately, most PE opportunities are for accredited investors (or high-net worth individuals). This means a majority of retail investors are unable to take part in these outsized returns.

Yet what if there was a way to bring private equity investing to the masses?

What if retail investors, small funds, etc. could access private equity opportunities at scale? What if you could replicate the strategy that helps private equity outperform public markets?

You can, and here’s the solution: apply a private equity investment strategy to public markets.

Thinking like a private equity investor is an edge in today’s short-term, next quarter mindset. Applying private equity principles to public market investing combines the best of both worlds. This gives every investor a chance at recreating that powerful strategy once reserved for high net-worth investors.

The Three Pillars of Private Equity

While thinking about the idea of private equity in public markets, we found recurring themes. We’ll call these our ‘Three Pillars’ of Private Equity in Public Markets. They are:

-

- Smaller is better

- Illiquidity Premium

- Long-term Thinking

Over the course of this section we’ll dive into these themes that a private equity mindset creates in public markets. Then, we’ll discuss ways to implement this mindset into your investment strategy.

I will warn you. This method isn’t for everyone. It requires a long-term outlook, a disregard for random stock price movements and a stomach for dramatic volatility.

Brief History of Private Equity

Let’s review the two types of PE firms we want to emulate. There’s Leveraged Buyouts (LBOs) and Venture Capital.

Leveraged Buyout Firm

As the name suggests, Leveraged Buyout Firms (or LBOs) use debt to purchase an existing business (either public or private). The leverage juices returns if things go well, but destroys capital in the event of a downturn.

LBOs sometimes use as much as 90% leverage to finance an acquisition. The goal for LBOs is an eventual sale (a.k.a., ‘exit’) three-to-five years down the road. These firms then try to improve the business through the income statement or balance sheet. Improving the business has two benefits:

-

- Increases cash-flow to the PE firm while they own the business.

- Presents the opportunity for a multiple re-rating when it comes time to sell.

Two high-profile examples of LBO Firms include Bain Capital and Apollo Global Management.

Venture Capital

Venture Capital Funds are another well-known PE vehicle. These funds invest in early-stage companies. These companies aren’t usually profitable. Some companies haven’t even generated revenue yet.

Venture funds invest (more-or-less) either the founder/CEO, or the vision of the company. Since there’s no profits, venture funds must learn to judge the quality of the CEO and the viability of an idea. These funds invest in either Seed or Series A rounds. Both rounds are the earliest times a company can invest.

Three examples of high-profile venture funds are Sequoia Capital, Insight Venture Partners and Adventur.es.

Here’s what we know: Private equity outperforms public markets.

We’ve already mentioned the three reasons why private equity generates higher returns:

-

- Smaller sized companies

- Illiquidity Premium

- Long-term Thinking

Let’s dive further into the investment strategy behind many private equity companies.

How Private Equity Firms Think

Private equity investors focus on four main areas when looking at potential investments:

-

- Downside Protection

- Three-To-Five Year Time Horizons

- Changing Management

- Buy To Sell

These four areas of focus fit nicely with our larger three criteria for higher returns. Applying these frameworks to public markets can juice our returns. Let’s break them down.

Downside is All That Matters

I know, this sounds confusing at first glance. Aren’t private equity firms known for massive leverage to juice returns? Yes, but as Munger likes to say, “invert, always invert.”

Private equity investors look for the strongest balance sheets. It is because they use leverage that they must look for the strongest balance sheets.

Leveraging an already levered company is like playing Russian Roulette. Sure you might hit it big with one or two names. But it only takes one name to topple the house of cards.

Three-to-Five Year Time Horizons

The standard PE model is to buy a company, instantiate change, and then exit for a multiple re-rating in three-five year’s time. This time-frame, three to five years, is important. The average public market participant can barely hold onto a stock for a year.

In fact, check out the data for average holding period by decade. The erosion in time horizon is stunning:

-

- 1960, eight years, four months;

- 1970, five years, three months;

- 1980, two years, nine months;

- 1990, two years, two months; and

- 2000, one year, two months

The average investor now holds onto a stock for less than one year. Here’s how insane that time frame is. Less than 1% of the business’ future value comes during that time. How then, is an investor supposed to realize the long-term benefits of a business’ cash flows? They can’t with that short of a time frame.

This is why time horizon matters. Three to five years is a minimum if an investor wants to reap the benefits of a cash-flowing business. Barring hard catalysts, these time frames should garner your entire investment decision.

Changes in Management or Operations

One of the greatest advantages private equity has over public markets is their ability to initiate change in management. This is a big reason why private equity returns generally outperform broader public markets.

Even if an investor has great ideas to turn a company around, he won’t be able to build a big enough position to do anything. That is, if she’s investing in larger companies. As we’ll see later, the size of the company can make activism a possibility even for smaller investors.

They Buy To Sell

Harvard Business Review’s article on private equity hints at the “secret” sauce behind PE’s outsized returns. Are you ready? PE firms buy with the intention of selling at a higher price. I know, radical thinking, right? Here’s a snippet from the article (emphasis mine):

______________________________________________________________________________

“But the fundamental reason behind private equity’s growth and high rates of return is something that has received little attention, perhaps because it’s so obvious: the firms’ standard practice of buying businesses and then, after steering them through a transition of rapid performance improvement, selling them. That strategy, which embodies a combination of business and investment-portfolio management, is at the core of private equity’s success.”

______________________________________________________________________________

Buying to sell flies in the face of conventional value investing principles. Value investors should invest in compounders, right? Well, not entirely. Remember, our goal is to not lose money. It’s not to only invest in compounders. Three to five year time horizons should be our bread and butter. If we can hold onto a business after that, its icing on the cake.

The Solution: Private Equity Investing in Public Markets

So, how do we combine the best of both public and private markets? Before diving into the strategy, we’ll investigate three men already practicing this very idea. Dan Rasmussen, Adrian Warner and David Barr.

Verdad Capital: Small-cap, leveraged Value Stocks

Dan Rasmussen runs Verdad Capital, an investment fund dedicated to private equity-style investing in public markets. Dan’s strategy is simple. He invests in small-cap, leveraged firms. Diving deeper, Dan looks for the following characteristics:

-

- Companies trading <6x EBITDA

- 3-4x Debt/EBITDA leverage ratios

- Value tilt

According to Verdad’s research, this type of strategy produced an annualized return of 25.1% from 1965 – 2013. That’s not bad!

Verdad prefers public markets over private markets for a few reasons. First, they’re able to invest in cheaper companies while using appropriate leverage. Second, public markets offer greater transparency and trust than private markets. This makes sense as public markets have GAAP accounting, short sellers (to keep you honest), SEC requirements, etc. Private markets have none of that.

Finally, investing in public markets is cheaper than equivalent private market transactions. These savings are passed down to LPs (limited partners) in the way of lower fees (AUM or performance).

For more information on Dan’s strategy, check out his podcast interview with Patrick O’Shaughnessy

Avenir Capital: Private Equity Investing in Australian Stock Market

Adrian Warner is another public equity investor implementing private equity strategies. Before starting Avenir Capital, Warner spent 20 years in Australian and US private equity.

Now, he’s using that experience in public markets. Warner laid out his fund’s strategy in an interview with MOI Global.

During the interview, Warner presented three areas he thinks are vital for private equity investing in public markets. All emphases are mine.

1. Focus on the downside

“There’s a great deal of emphasis on worrying about what can go wrong in any investment, which I consider quite a healthy starting point, and fixating on avoiding permanent loss of capital. That’s probably the first element of private equity we work really hard on bringing over to the public markets.”

2. Strong emphasis on fundamentals and bottoms-up research

“[You should] remove yourself from trying to second-guess stock prices and focus on what you see as the underlying or intrinsic value of an asset and look to invest only in those situations where you can buy at a very material discount it. This bottom-up approach, which is highly consistent in private equity, is essential to what we do.”

3. Absolute, long-term returns is what matters

“There are no benchmarks in the short term, no liquidity or daily pricing of assets. The focus is very much on what you can buy an asset for now and what you think you’ll be able to sell it for three, four, or five years’ time. You don’t worry too much about what’s going to happen to the price in the short term. This absolute long-term return focus is very powerful, but a lot of the public market industry is trapped in the relative benchmarking mindset, which can be very damaging to focusing on the long-term return, in my view.”

I highly recommend listening to the interview or reading the transcript. Avenir’s investment strategy can be summed up in one sentence: Investing with a long-term time horizon, running a concentrated portfolio and evaluating investments as if we are buying the whole company.

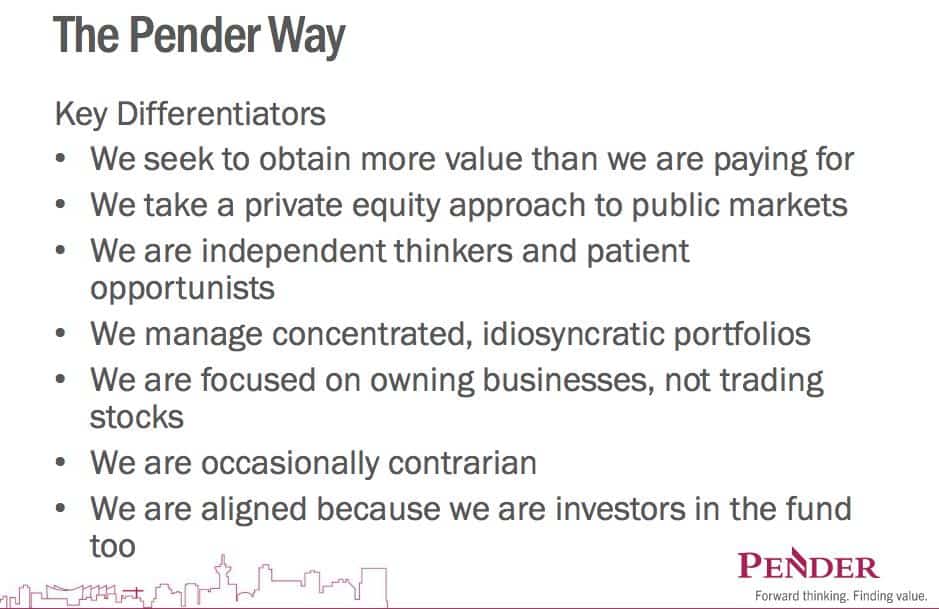

PenderFund Capital Management: Private Equity Approach in Canada

David Barr is President and Portfolio Manager of PenderFund Capital Management, Ltd. In 2018, Barr released a slide deck outlining the fund’s public market strategy. Here’s a few snapshots of my favorite slides:

“The Pender Way”

PenderFund focuses on three drivers for long-term value creation:

-

- “Scuttlebutt” research and due diligence

- Work with investee companies

- Drive a liquidity event or exit

Barr does all these things inside public markets. But he’s not engaging with mega, blue-chip companies. He’s going to the smallest corners of the markets. The small and micro-caps.

According to Barr’s deck, he prefers small caps because of large target markets and long runways for growth:

We know the strategy works, and we’ve seen examples of other investors doing it. Now let’s flesh out the key pillars to the underlying strategy.

Fleshing Out The Advantages (The Three Pillars)

Now it’s time to dive into the Three Pillars of our private equity strategy. We’ll expand on each pillar so that you understand why it matters and how we apply it to public markets.

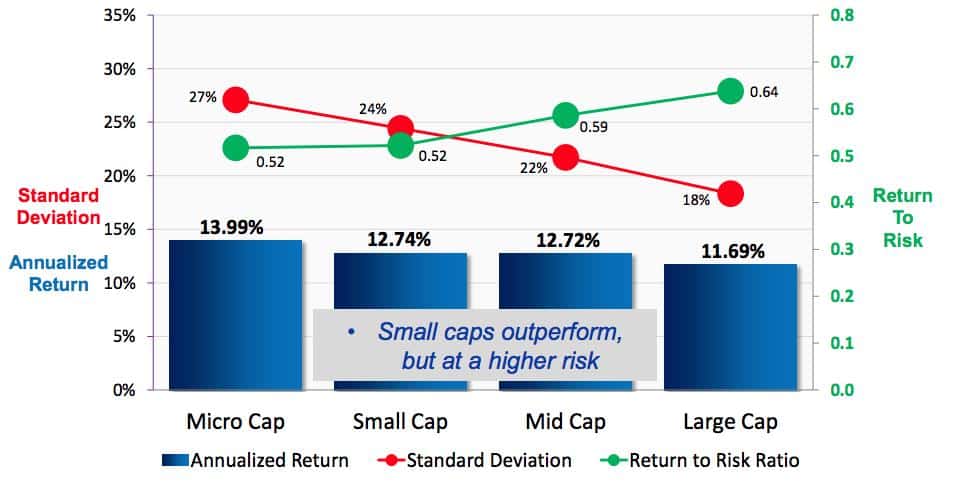

Size Matters: Smaller Value Companies Win

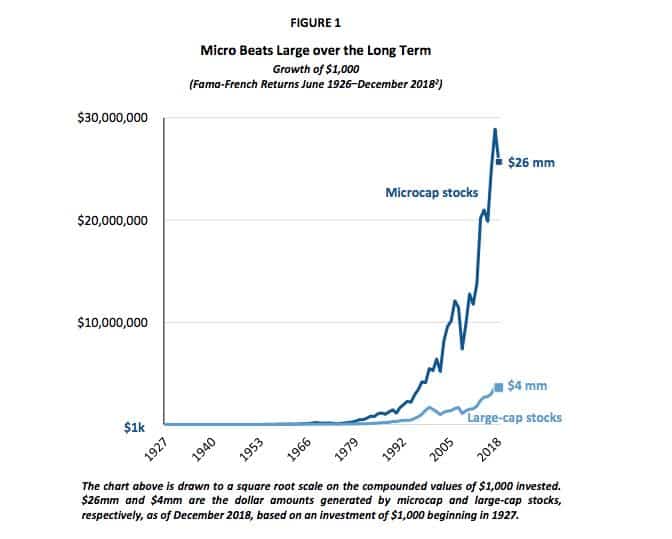

The data is clear. Smaller companies outperform larger companies in public markets. And no one analyzes the smaller-company edge better than Roger Ibottson.

According to the famous slide deck, Liquidity as an Investment Style, micro-cap stocks outperformed every other size between 1972-2013:

As the data shows, this isn’t the most optimal strategy. Using size as the lone factor increases the standard deviation of returns and reduces the return to risk ratio. We can do better (and we will).

Further research by DGHM & Co., backs up Ibottson’s claim. Between 1928 – 2018, microcap stocks compounded $1,000 into $24M. Large caps during that same time frame? $4M.

Further research by DGHM & Co., backs up Ibottson’s claim. Between 1928 – 2018, microcap stocks compounded $1,000 into $24M. Large caps during that same time frame? $4M.

It’s evident that the smaller we go, the greater the chance for outperformance. But we’re not done. There’s one more layer we can add to this criteria to really boost potential returns.

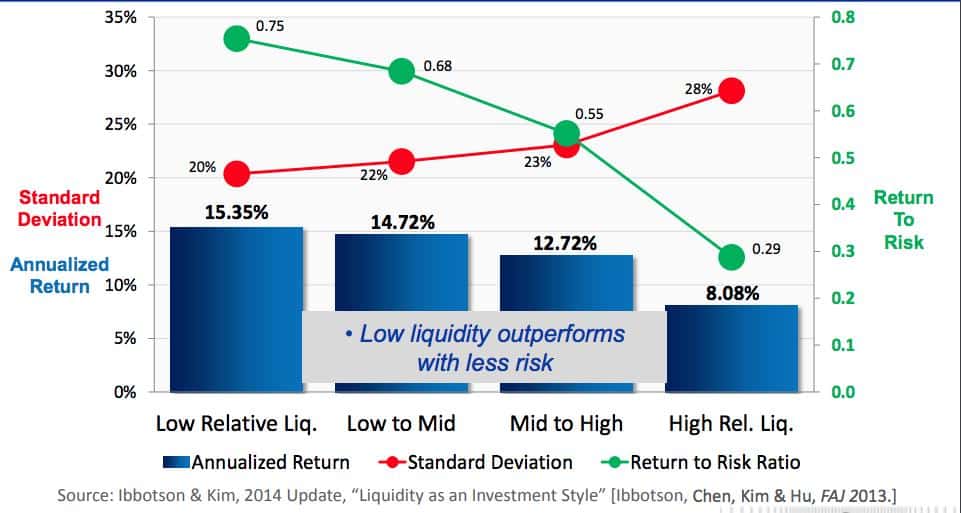

Illiquid Stocks Perform Better

We know smaller is better. But we can do better than that. According to Ibottson (and private equity theory), it’s illiquidity that drives outperformance.

There are three things that stand out on this chart. First, low liquidity outperforms high liquidity by nearly 10% per year.

There are three things that stand out on this chart. First, low liquidity outperforms high liquidity by nearly 10% per year.

Second, the return to risk ratio is 0.75 for the least liquid investments and 0.29 for the most liquid.

Finally, the standard deviation for illiquid stocks is 20% compared to 28% for high liquidity stocks.

In other words, illiquid stocks generate higher returns with less risk. That doesn’t sound too bad! But, when we combine the above features — small size and illiquidity — we get 1 + 1 = 3. This is our optimal strategy (see photo below):

Illiquid micro-cap stocks generated 16.3% annualized returns from 1972-2013. This far surpasses any other investment category.

Long-Term Thinking as an Edge

As we discussed earlier, many PE firms have three-to-five year time horizons. This is important because value creation doesn’t happen overnight. A large part of most PE strategies involves shaking up management. Sometimes changing the entire course of the business. To assume those long-term efforts will pay off in less than a year is foolish.

But there’s another reason why PE investors need long-term time horizons. Illiquidity. Unlike public markets, if an investment goes south, PE investors can’t quickly sell. They’re stuck with their business, for better or worse.

Thus, illiquidity encourages a greater emphasis on the balance sheet and durability of a business. We can recreate all three of these advantages in public markets.

Creating an Investment Strategy Around our Three Pillars

We’re now ready to create an investment strategy aimed at capturing private equity premiums in public markets. The strategy is simple in its construction, but brutally difficult in execution. Let’s dive in.

Before you do anything, shrink your universe of stocks to microcaps and the most illiquid stocks you can find. I focus on stocks trading at market caps at or below $50M. Of those stocks I look for ones with the least amount of average trading volume.

After you’ve done that, focus on boring business. These are businesses that aren’t susceptible to technological change. Businesses that are small cogs in a larger machine. Think of electrical component manufacturers, valve producers, cyclical companies, etc. The more boring the better. Remember these companies are small. If they’re in a fiercely competitive technology sector, how much confidence is there that they can outspend on R&D?

Narrowing down our stocks to boring businesses we then focus on the balance sheet. Verify that the balance sheet is clean and bullet-proof. Favor current assets over long-term assets (unless its an asset play where management’s liquidating PP&E).

We want to buy companies with little-to-no debt. Remember, we’re thinking like PE investors. It’s hard to leverage a company with an already leveraged balance sheet. This doesn’t mean we’re going to use leverage — but we must think within that same framework.

Finally, from this subset of small companies with great balance sheets, focus only on the most illiquid names. I measure illiquidity by average annual share turnover. The calculation looks like this:

-

- 10 day average volume x 252 (number of trading days) / total shares outstanding

The smaller the percentage the better.

Once you get to this point, you’ll have a small list of potential investments. You can do one of two things. You can invest in a basket of microcap and illiquid stocks. Or you can take a more concentrated approach. It all depends on your risk tolerance and portfolio goals.

If you’re using this as a diversification tool within a larger, factor-based portfolio, a basket approach makes more sense. If you’re looking to change course or develop a true, private equity-type strategy — concentrated picks might be the move.

Let’s chat about risk management for a minute. Stop-losses aren’t as reliable in microcap investing given the wide bid/ask spreads. Keep this in mind as you’re deciding on which iteration of this strategy is right for you: basket or concentrated.

Risks of a Private Equity Strategy

Yes, this strategy works. And yes, you can generate significant outperformance. But it doesn’t come without its share of risks. Illiquid, micro-cap investing shares the same risks as the general market. Yet there’s three risks that are unique to an illiquid, micro-cap strategy:

1. Liquidity Risk

A PE strategy applied to public markets brings about liquidity risk. In other words, you might not be able to get out of a stock when you want / need to. In illiquid, micro-caps, there’s not always a complimentary buyer/seller on the other end of the trade. This also works the other way. It may take weeks or even months to establish a full position in an illiquid name.

Are you willing to sit in a position knowing full well you might not be able to get out of it in quick time?

2. Capital Constraints

The second major risk, if you want to look at it like that, is capital constrainment. An illiquid, micro-cap strategy works for small account sizes. The larger you climb the AUM ladder, the fewer companies you’ll be able to invest in. It breaks down to simple math. A $200M fund cannot invest in companies with $5M or less market caps.

3. Increased Volatility

I want to preface this by saying, no, volatility is not investment risk. Yet it is personality risk. Let me explain. An investment strategy is only as good as the person implementing it. So, if you can’t stomach random gyrations in share price, this strategy may not be for you. But, if you understand that share price isn’t indicative of intrinsic business value, you’ll welcome the volatility.

Illiquid micro-caps experience bouts of extreme volatility for several reasons. First, one investor can move the market. It may not be for fundamental reasons. Maybe his daughter needs a new car. Or the investor needs to pay for her vacation. In this space, we’re dealing (for the most part) with retail investors.

Concluding Thoughts

Thinking like a private equity investor in public markets is powerful. Through this lens, we can create a strategy that provides the best of both private and public markets. We leverage the alpha from illiquidity and smaller-sized companies, while retaining higher liquidity than conventional private equity offerings.

This strategy is backed by decades of research confirming its absolute outperformance over broader indices. Here’s the beauty of the strategy. You don’t have to implement it across your entire book. You can create a subsection of your portfolio dedicated to this illiquid, micro-cap space. In doing so, you increase portfolio diversification and expected long-term returns.

_______________________________________________