“We’re in the business of making mistakes. Winners make small mistakes, losers make big mistakes.” ~ Ned Davis

Summary: A short-term bounce in US equities is possible, but we remain neutral to bearish long-term. Dips should be traded, not invested in, as positioning and flows contradict the fear reflected in sentiment data, indicating more volatility ahead. In contrast, European indices are poised for a long trade. While our Macro Implied Regime model suggests a low recession risk in the next six months, macro data hints at increased risk by year’s end.”

Alright, let’s get to it.

1. We run two portfolios in our Collective: the MO Macro portfolio, which is up +10.3% ytd and is run by Brandon and me; and our Systematic Macro portfolio, which is run by Chris and is up +2.5 % ytd versus the S&P’s -5%. We alert all trades in real time for both ports within our Collective Slack. Chris puts out a weekly Market Overview where he updates what each of his systems are signaling for each market. You can watch the latest one here.

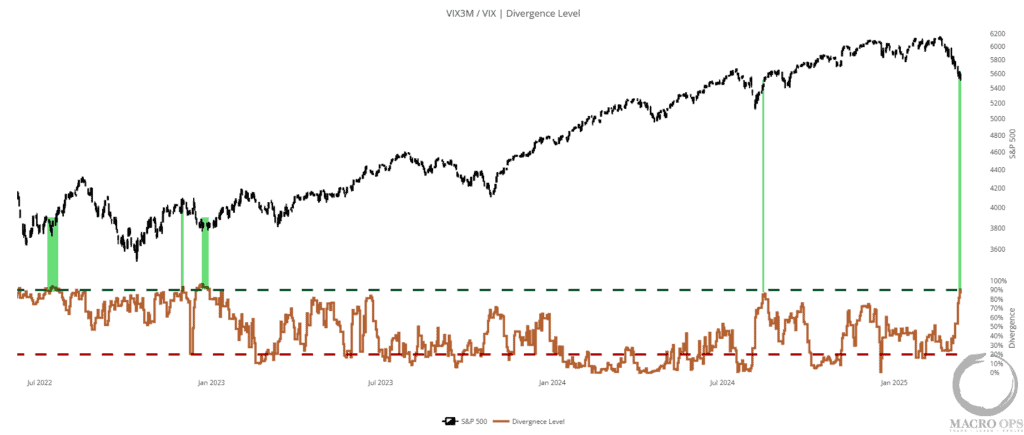

2. A short-term tradeable bottom is likely in… Here’s the VIX3m / VIX spot looked at on a divergence basis from the market. It triggered a buy signal this past Friday.

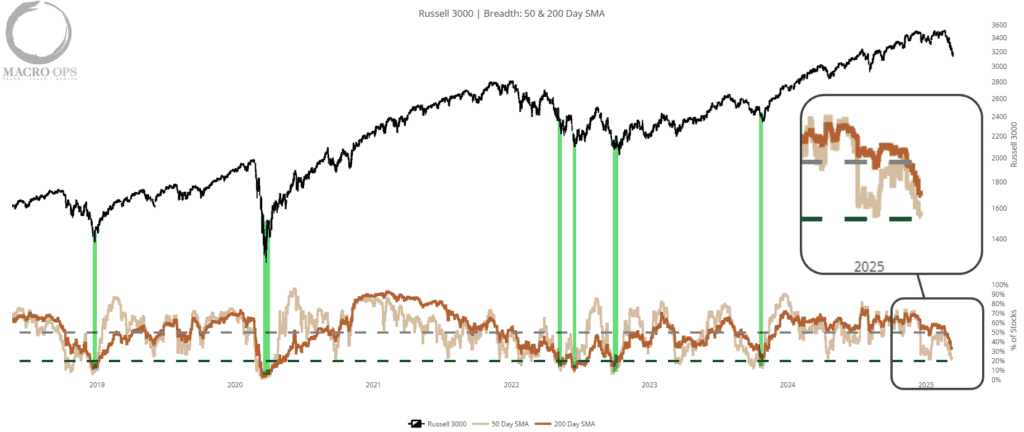

3. The percentage of R3K stocks trading above their 50dma dropped below 20% last week. But those above their 200dma are still above 30%. More significant bottoms tend to form when both are well below the 20% threshold.

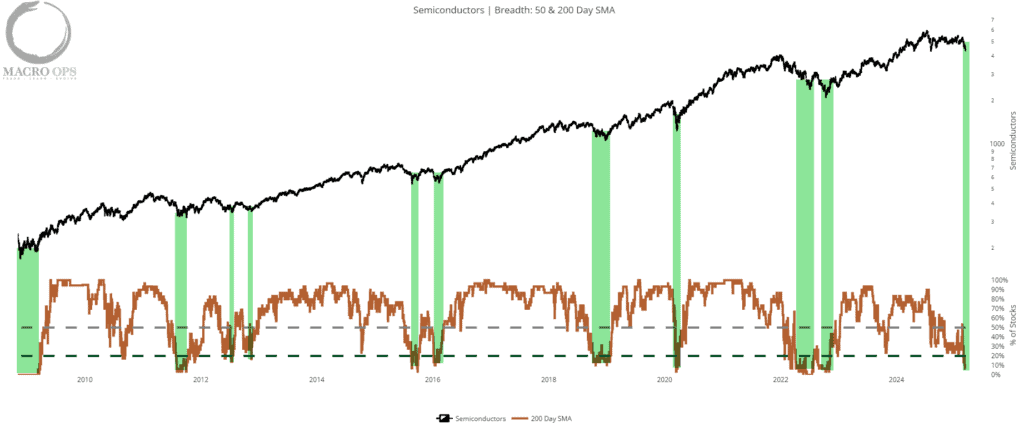

4. The percent of semiconductors trading above their 200dma dropped to 7% last week. Green highlights mark every time they’ve crossed below 20% over the past 15 years.

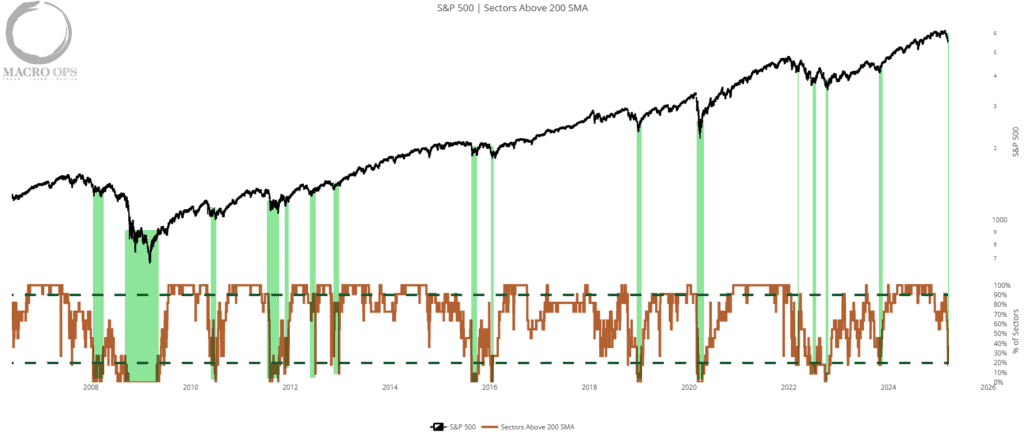

5. The percentage of S&P 500 sectors trading above their 200dma also dropped below 20% last week.

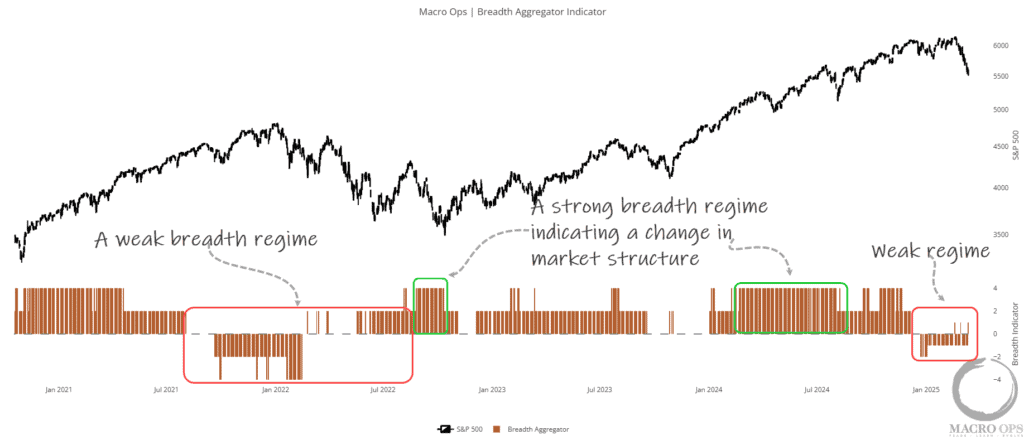

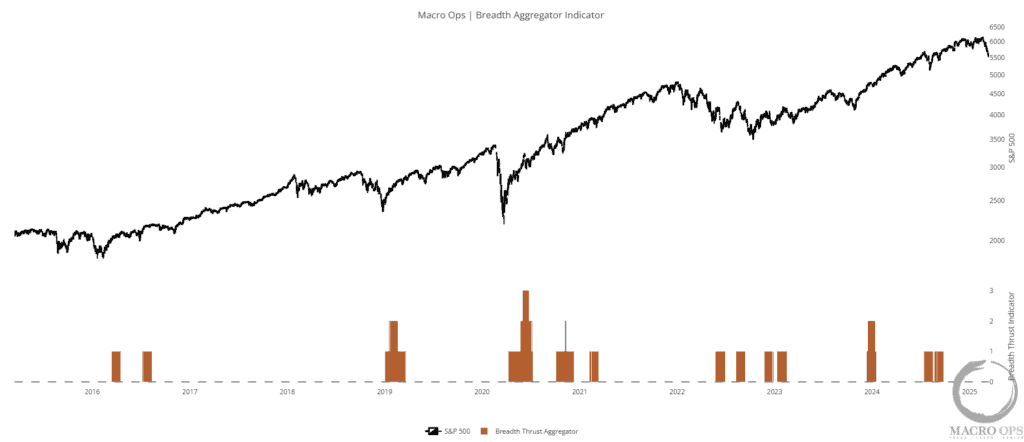

6. So we’re seeing an increasing amount of oversold levels across both price and breadth. But… this just means that the forces of mean reversion will start to exert some positive pressure on price over the short-term. For us to turn bullish on the market — at least for anything greater than a short-term trade — we need to see a shift back to a strong breadth regime and preferably one accompanied by some breadth thrusts, indicating the bulls are back in control.

7. As of now, our operating belief is that, at best, we’ve entered a large, volatile sideways trading (topping?) range that will play out for a number of months. And at worst, we’re entering a new market regime with significantly more downside ahead.

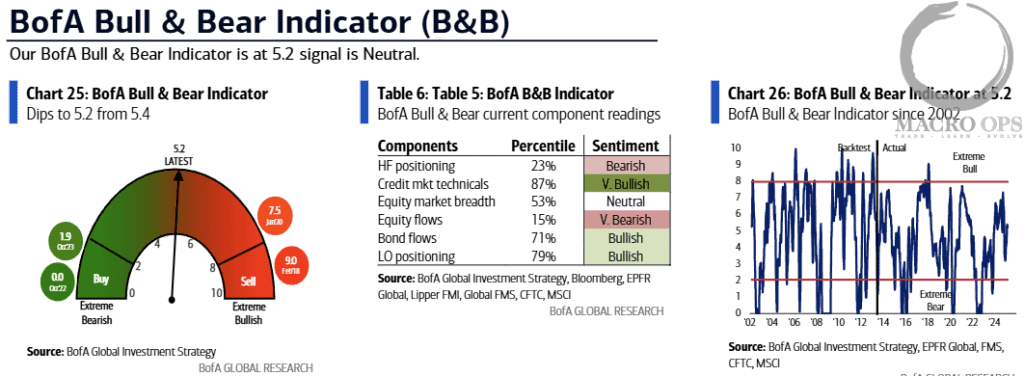

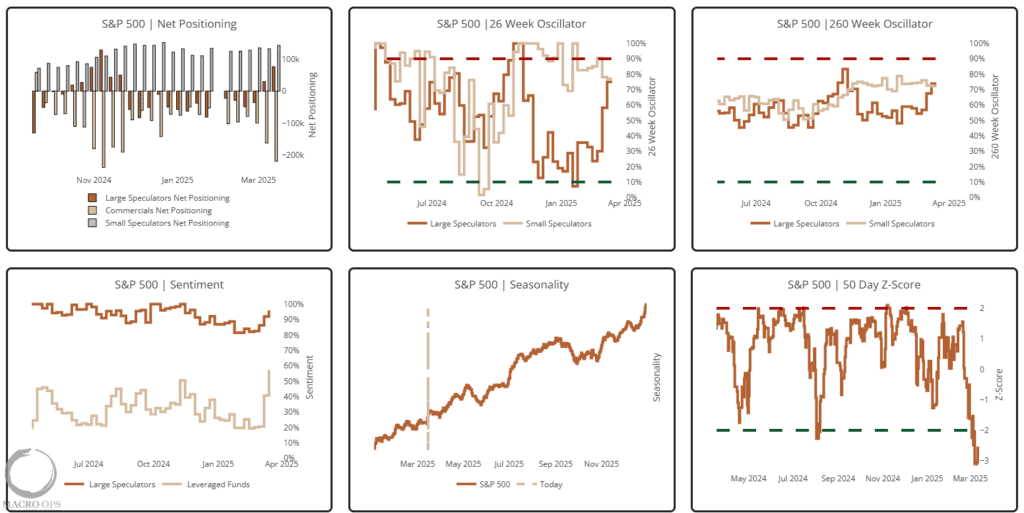

One worrying point is that while some soft survey measures of sentiment (AAII for example) are showing max bearishness, actual positioning data and flows, such as the BofA Bull/Bear below, CoT for the SPX and NQ, and Total Put/Calls, are either neutral or quite long/bullish.

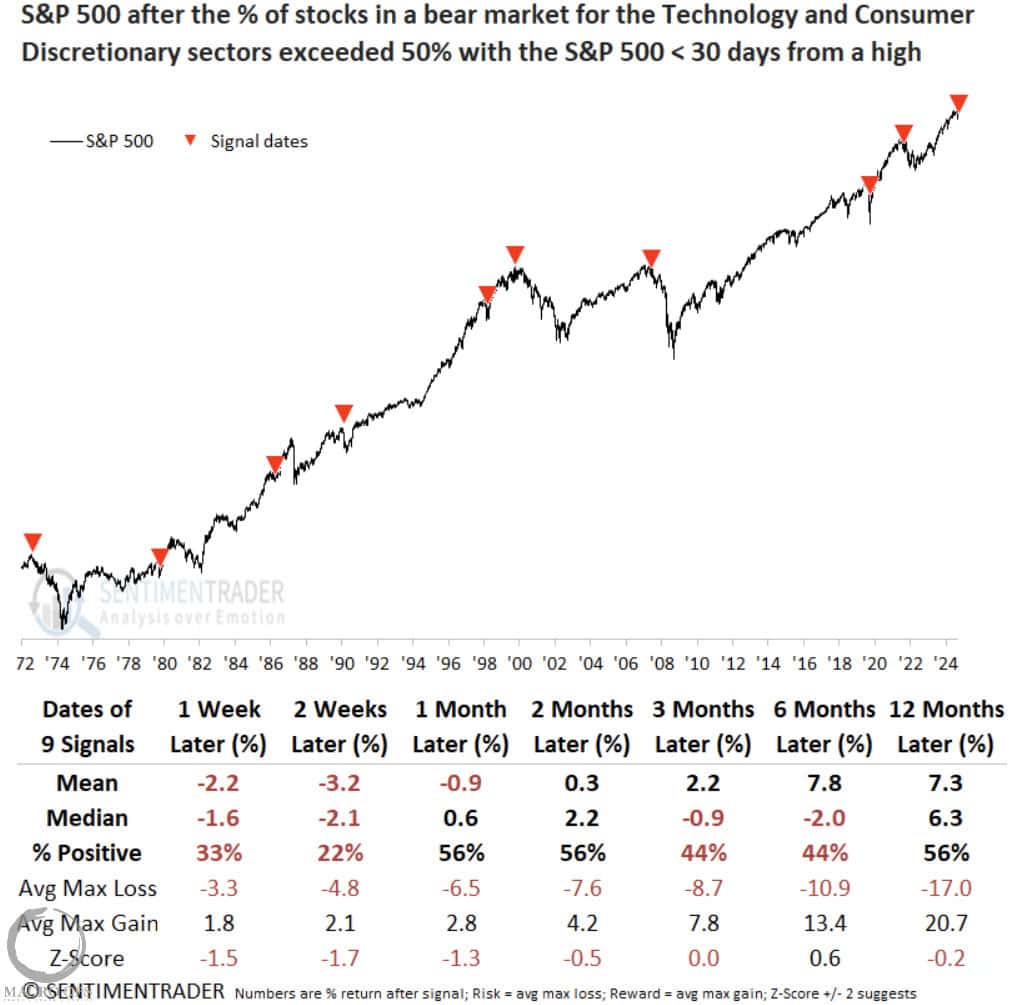

8. To that point, here’s an interesting study from SentimenTrader:

“When 50% or more of stocks in the Technology and Consumer Discretionary sectors closed in bear market territory with the S&P 500 within 30 sessions or fewer of a multi-year high, the world’s most benchmarked index exhibited unfavorable win rates and returns over the following six months.”

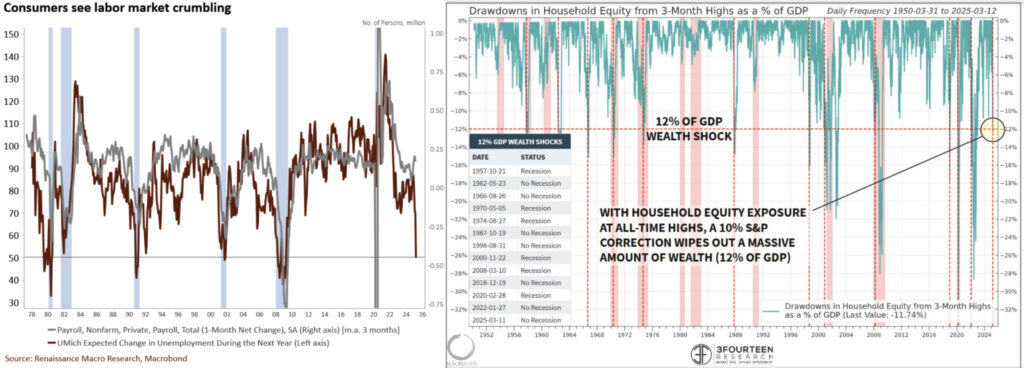

9. Here’s two notable macro charts shared last week, one from RenMac and the other Warren Pies. Warren tweeted:

“NEGATIVE WEALTH SHOCK…B/c households are massively OW stocks, the current 10% market decline has created a wealth shock equivalent to 12% of GDP…10% corrections are typical (53 since 1950)… But, wealth shocks are rare (13)…The economy is more vulnerable to a stock decline.

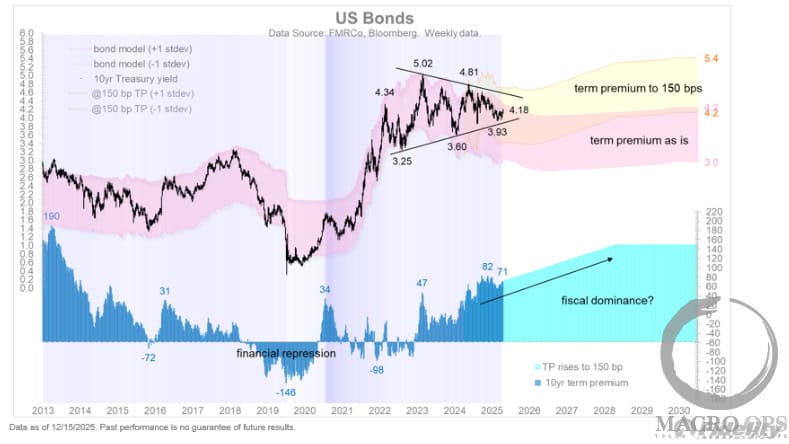

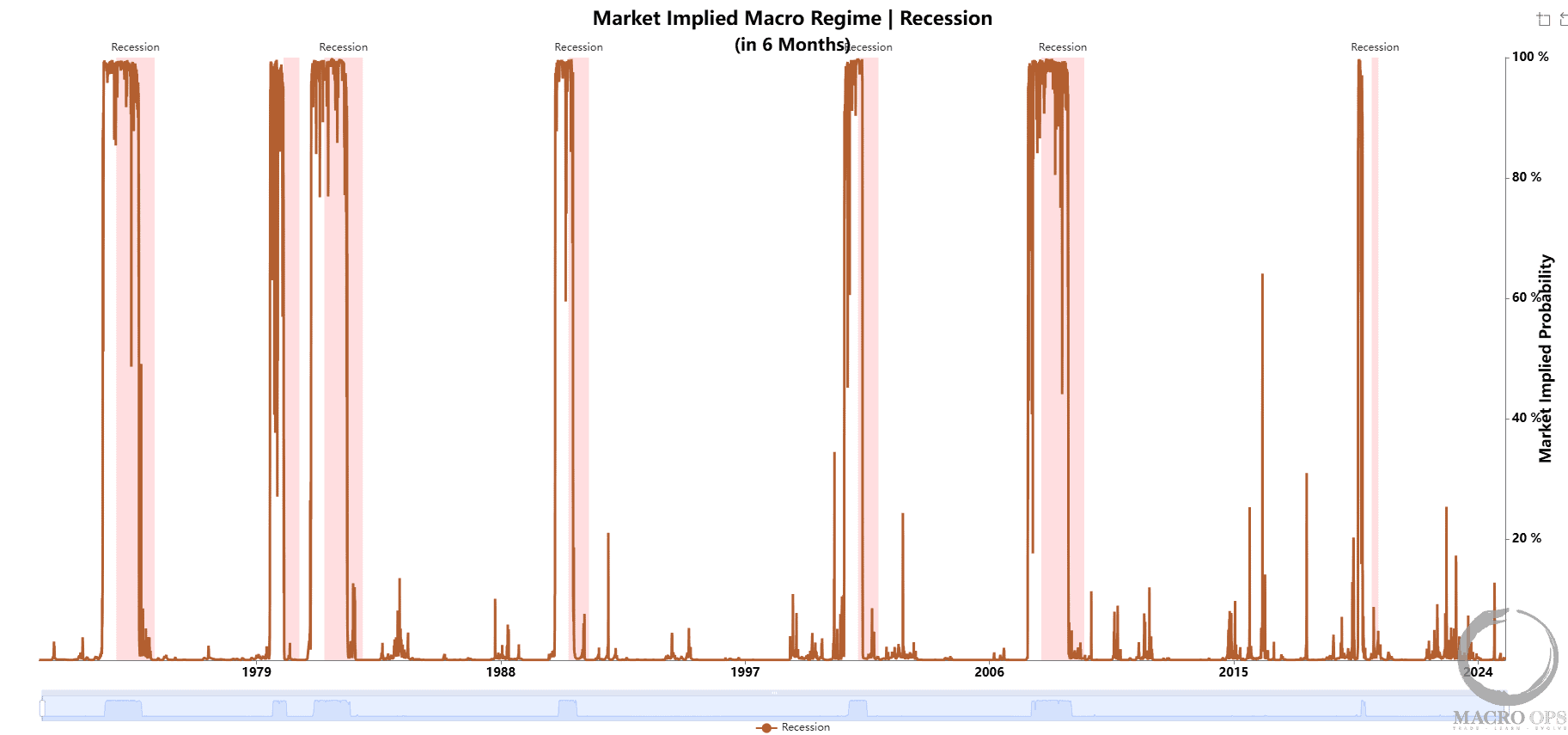

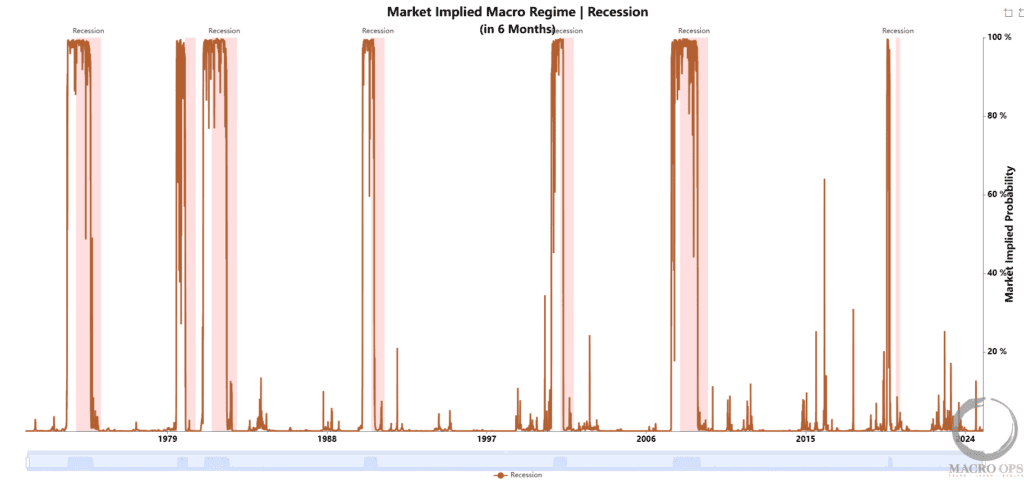

10. The macroeconomic landscape is growing more worrisome, with the possibility of a recession in the latter half of the year increasing. While our Market Implied Macro Regime chart currently shows only a 5% chance of a recession in the next six months, this outlook can change rapidly.

.

11. On the single equity side, the team and I are primarily focused on real asset exposure (miners, producers, etc…). Here’s a name we’ll likely be buying a starter position in soon, Sylvania Platinum (SLP:LSE). Brandon wrote them up last year (link here).

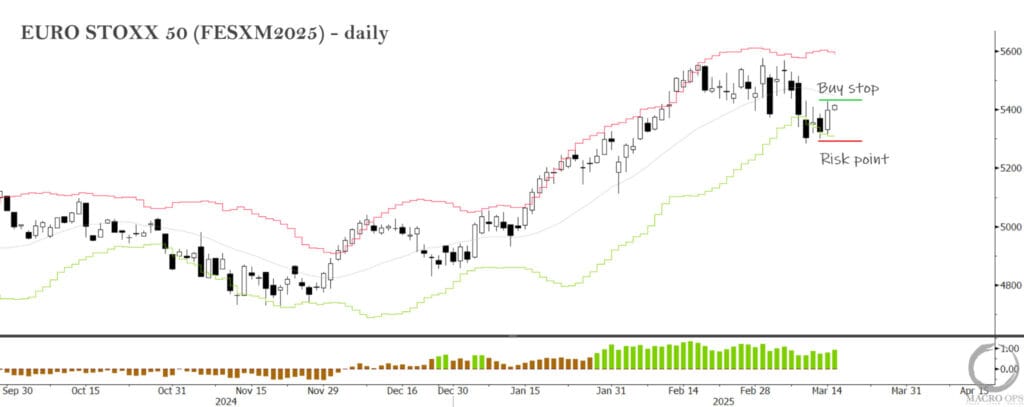

12. Buy Europe over US… Last week we noted the failed breakout setup forming in EURO STOXX 50. Friday gave us the signal to put in a buy stop to see if the market can pull us in long.

Join The Collective

Thanks for reading.