I have a friend who has amassed a fortune in excess of $100 million. He taught me two basic lessons. First, if you never bet your lifestyle, from a trading standpoint, nothing bad will ever happen to you. Second, if you know what the worst possible outcome is, it gives you tremendous freedom. The truth is that, while you can’t quantify reward, you can quantify risk ~ Larry Hite

Good morning!

In this week’s Monday Dozen we check out short-term sentiment (still too bullish!), longer-term sentiment (getting pretty bearish), indications of a weakening US economy, credit stress, a long opportunity in the pound, a crowded consensus, and 250-years of stock and bond correlations…

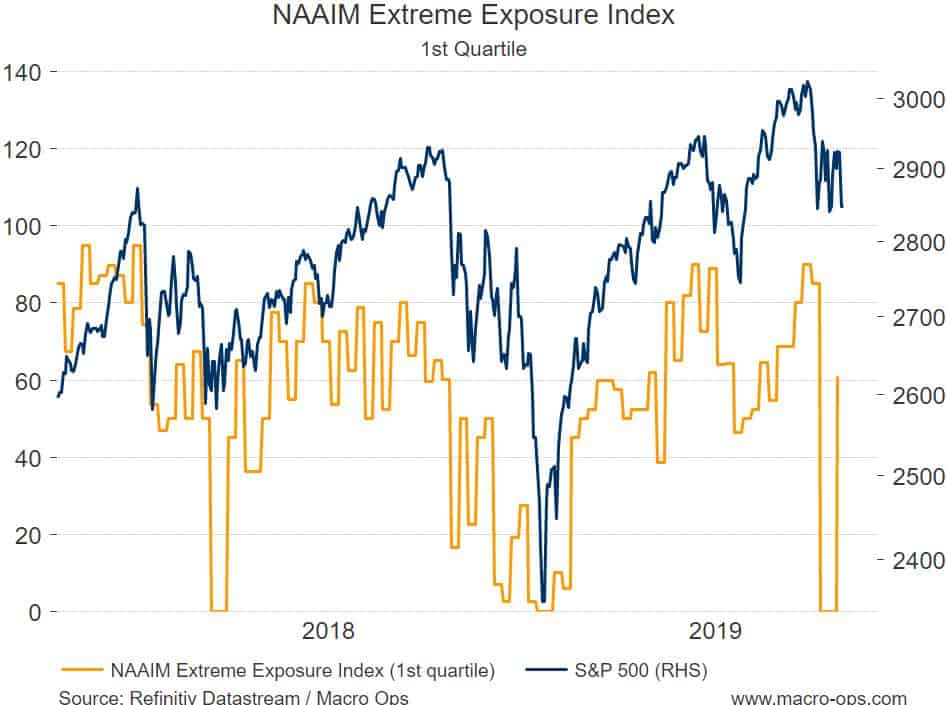

- When trying to gauge the durability of a potential market bottom we need to observe how quickly the dominant narrative flips. A sustainable rally needs to climb a wall of worry and general disbelief. When we see market participants quickly switch from bearish to bullish on a small bounce in price, it means that the market is likely to inflict more pain on the downside. Our NAAIM Extreme Exposure Index which measures the number of respondents who say they’re leveraged long the market saw a significant bounce this week. This along with my other sentiment/positioning indicators tell me we likely have more downside and chop ahead.

- With that said, the longer-term sentiment and positioning backdrop is potentially setting up for another significant bullish advance. The chart below via Sentiment Trader shows the 3-week average of AAII Bulls is near extreme lows, which in the past has often led to big gains over the following three months.

- The Philadelphia Fed Coincident State 1-month Diffusion Index bears keeping an eye on. This coincident index measures four state-level indicators for each of the 50 states. It recently fell to new cycle lows. In the past, similar weakness has often preceded a recession.

- The Conference Board’s Leading Economic Index (LEI) on the other hand, just made a new cycle high. The LEI has correctly signaled all eight recessions since its inception in 1959. It turns over and heads lower an average 10.5 months before a recession begins.

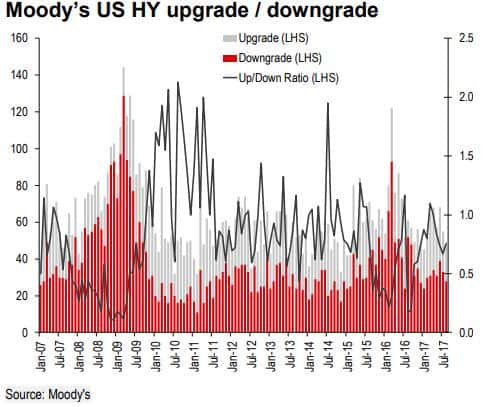

- Downgrades in high-yield credit are about average Note the uptick in downgrades in 07’ the preceded the GFC (chart via Moody’s).

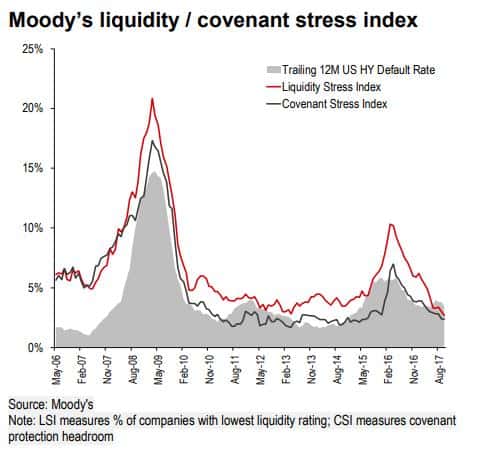

- And Moody’s Liquidity/Covenant Stress Index remains subdued.

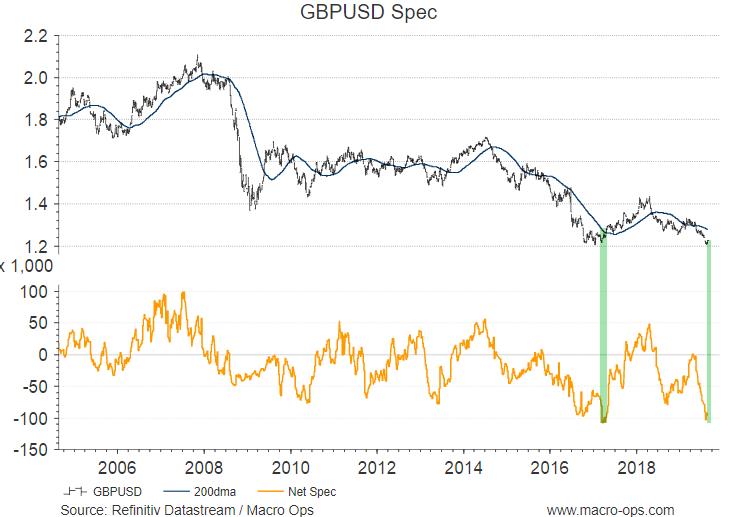

- The pound (GBPUSD) is bouncing off of long-term support (chart below is a weekly).

- Specs are very short.

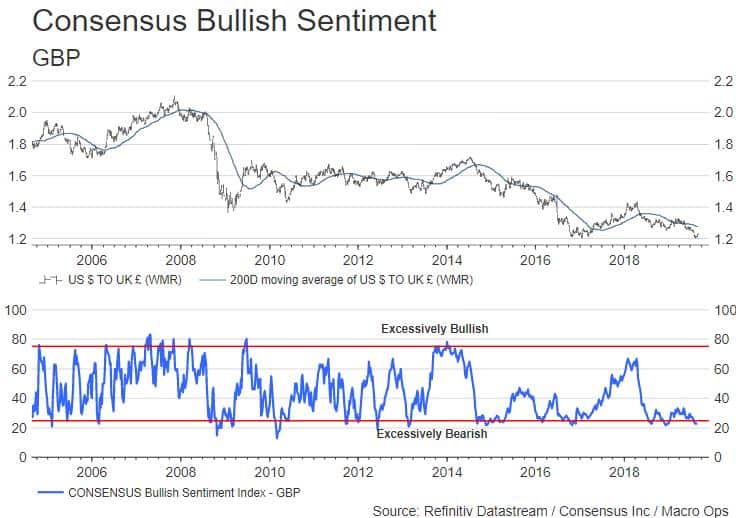

- And sentiment is very dour…

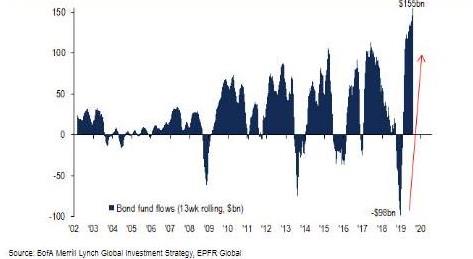

- The flows into bonds have been massive since the end of last year (chart via BofAML).

- We’re literally nearing the point where not a SINGLE soul thinks long-term interest rates will rise… Pay attention to the consensus narrative! (chart via BofAML)

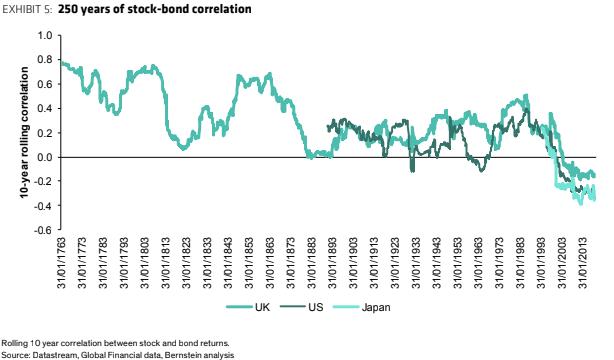

- This great chart from Bernstein Research shows that the correlation of stocks and bonds over the last 20-years is its most negative over 250-years of data. As Bernstein notes “This has been incredibly beneficial to asset owners and is a part of the reason why it has been so desirable to simply hold a passive 60:40 combination of equities and bonds… but if it was a function of the movement lower in inflation and real growth and changes in monetary policy then it might not be possible to rely on such a benign state of affairs continuing.”