Well, I was worth over one million after the close of business that day. But my biggest winnings were not in dollars but in the intangibles: I had been right, I had looked ahead and followed a clear-cut plan. I had learned what a man must do in order to make big money; I was permanently out of the gambler class; I had at last learned to trade intelligently in a big way. It was a day of days for me ~ Jesse Livermore, Reminiscences of a Stock Operator

Good morning!

We’ve got over a century of equity volatility, falling Capex, contracting margins, and traders in a near PANIC. Here’s your Monday Dozen Chart Pack.

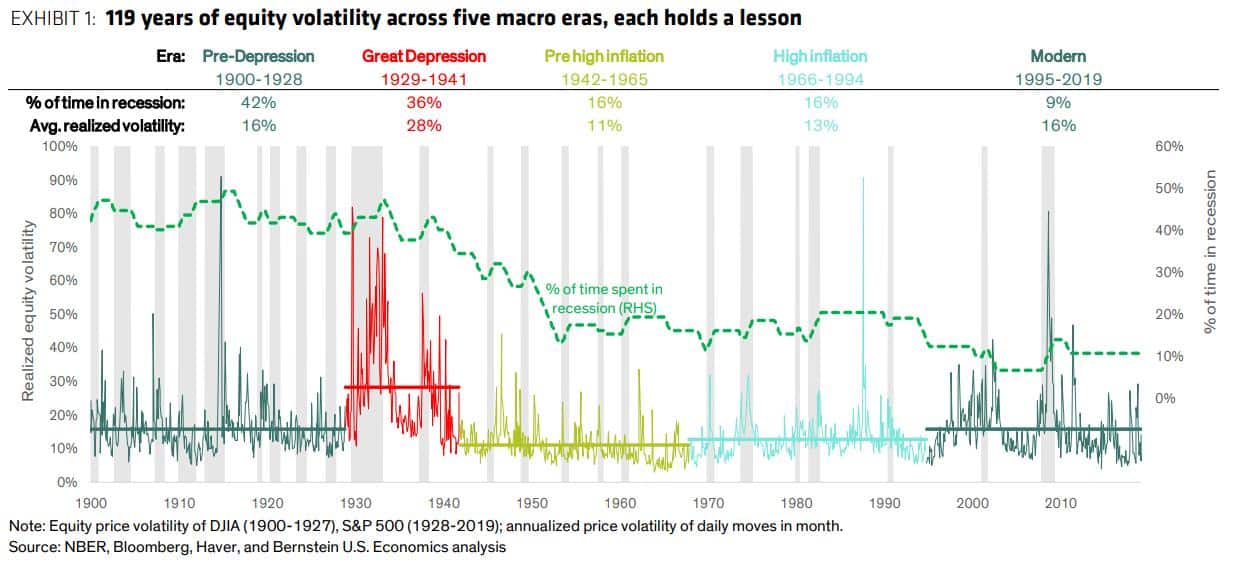

1. This is an awesome chart that I found floating around on the twitters. It’s from Bernstein Research and shows 119-years of equity volatility across five different macro eras. You can see that the percentage of time spent in recession (dotted green line) has trended lower and dropped considerably over the last century.

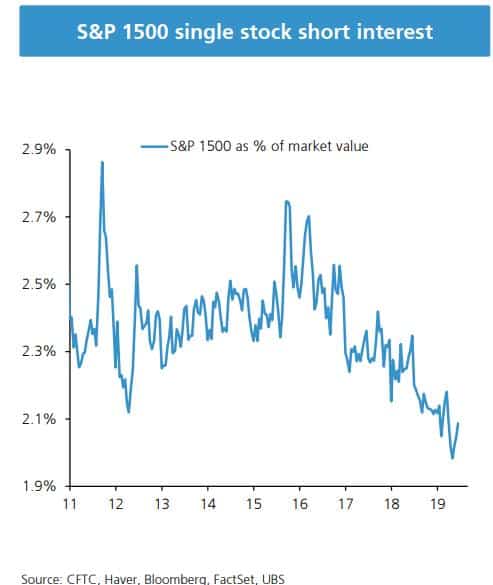

2. This chart from UBS shows how much single stock short interest has dropped over the last 3-years. Looks like people have kind of given up on shorting. Maybe it’s time to start increasing your short book?

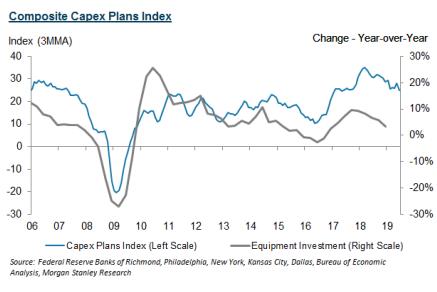

3. Capex is a critical component of the Levy-Kalecki Profits Equation. Morgan Stanley’s composite Capex Plans Index fell again in June, back to levels last seen in mid-17’.

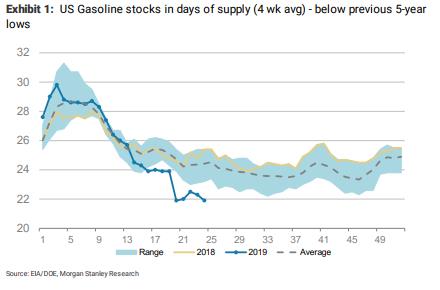

4. US Gasoline stocks, measured in 4-week average of days of supply, has fallen well below previous 5-year lows (chart via MS).

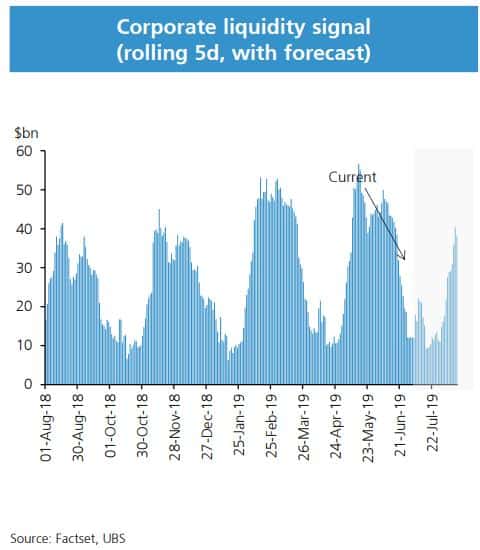

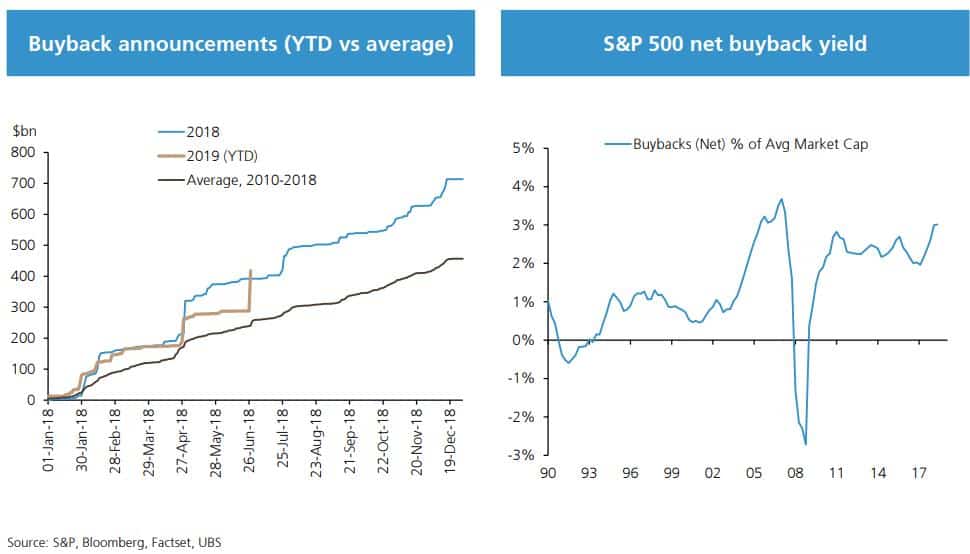

5. This chart shows UBS’s rolling 5-day Corporate Liquidity Signal (aka, buybacks). The net destruction of shares (more shares being taken off market through buyback and M&A relative to new issues) continues to be one of the most dominant drivers this bull cycle. It’s important to keep an eye on where net buybacks are trending.

6. This is one reason why we continue to be positioned net long the overall market.

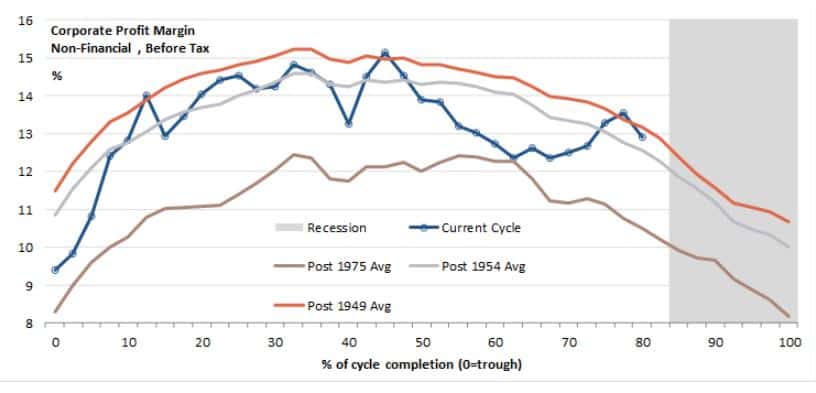

7. This chart shows the current US Corporate before tax profit margins based against previous cyclical trough relative to past business cycles. We can see that margins are contracting but if this cycle is like past average ones, from a profit margin standpoint, then recession is still a ways off (chart via Societe Generale).

8. With average debt servicing costs for US companies at depressed levels, the force driving contracting margins is primarily labor costs.

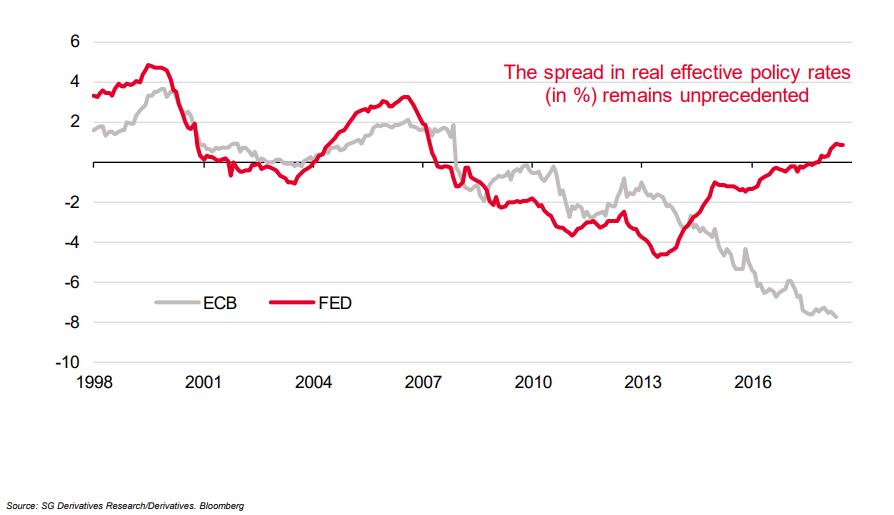

9. The current spread in real effective policy rates between the Fed and the ECB is unprecedented (chart via Societe Generale).

10. Total speculative USD position. Lots of air to be let out of this trade. I’m short and looking to get more so (chart via GS).

11. This chart shows the number of 25bps hikes/cuts delivered every year relative to the amount of 25bps cuts already priced in over the next 12-months (chart via MS).