I’m also a firm believer in predicting price direction, but not magnitude. I don’t set price targets. I get out when the market action tells me it’s time to get out, rather than based on any consideration of how far the price has gone. You have to be willing to take what the market gives you. If it doesn’t give you very much, you can’t hesitate to get out with a small profit.~ Linda Bradford Raschke

Good morning!

In this week’s Monday Dozen we look at the historical magnitude of the current tech bubble, the incredible financialization of our economy, the best-performing assets year-to-date, the end of an era, and much much more. Let’s begin.

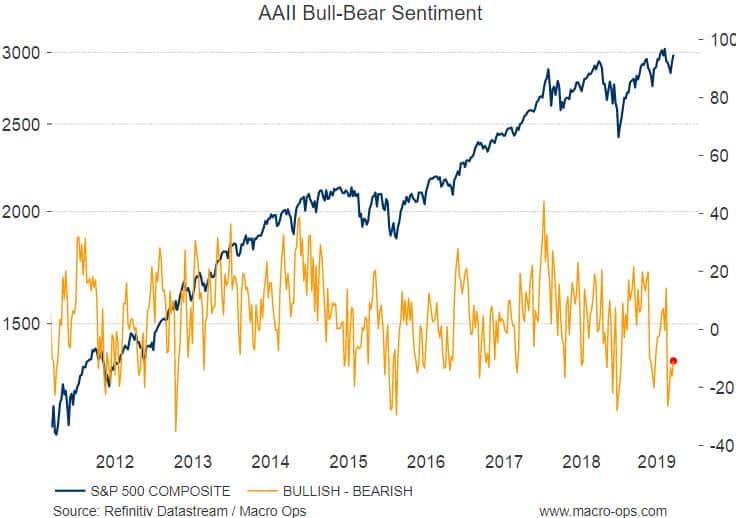

- The S&P is within spitting distance of all-time highs but investors aren’t buying it. AAII Bull-Bear sentiment remains in the gutter. This is bullish and makes it odds on we see new highs in US equities very soon.

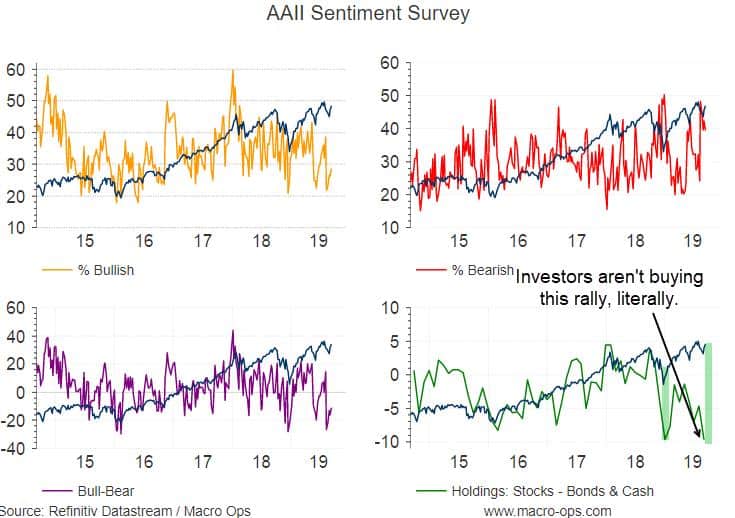

- Here are the subsections of the AAII survey broken down. See the chart in the bottom right-hand corner. Investors are holding their lowest levels of stocks relative to cash and bonds since January of 13’. This can mean two things (1) there’s a lot of potential fuel to drive this coming bull leg higher or (2) there’s trouble ahead because we need investors to eventually start buying in.

- At least one would think so because how much longer can this lopsided equity demand trend continue?

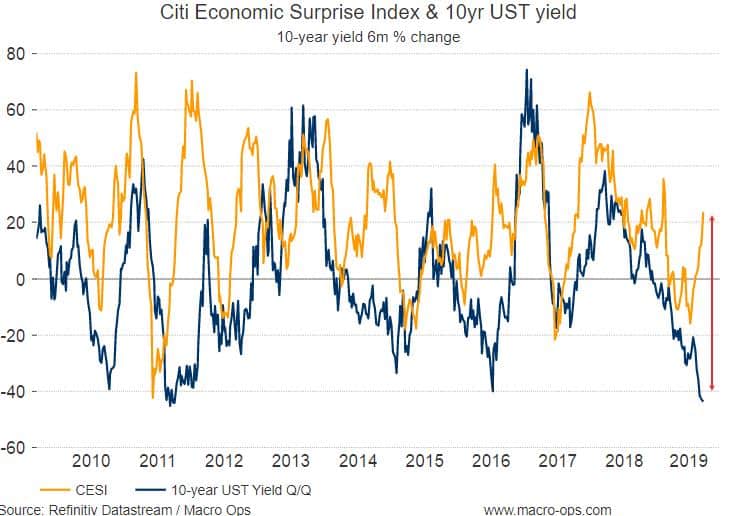

- If equities are about to rally like I think they will then crowded bond longs may be in for a world of hurt. The US Citi Economic Surprise Index (CESI) just turned positive for the first time in nearly 150 days. Bondholders, MIND THE GAP….

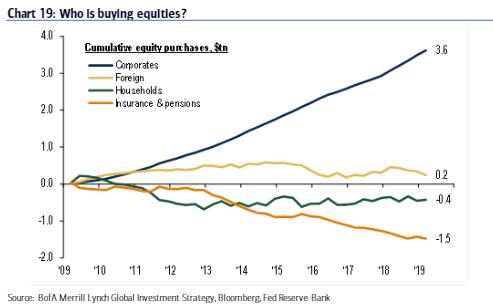

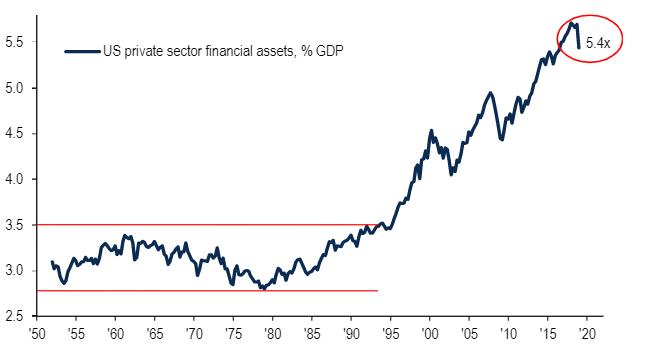

- When I reference the financialization of the economy, this is what I’m referring to. This is why investor confidence is so critical to the economic cycle. The financial asset tail now wags the economic dog (chart via BofAML).

- While I’m expecting a large pullback in bonds (jump in yields) over the coming months, I ultimately think US yields go lower. All the way to zero. Demographics are the reason why. We’re seeing the Japanification of the world.

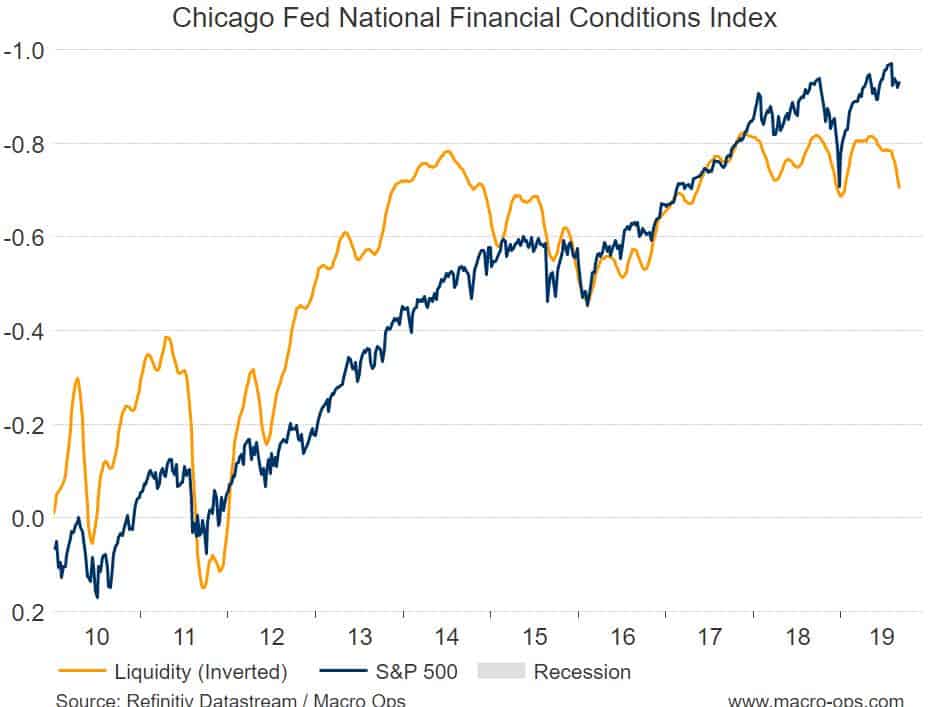

- The majority of my liquidity/fin-stress indicators are healthy and giving little cause for alarm. But, the Chicago NFCI is close to hitting multi-year highs (chart is inverted). I think we’ll see this turnaround but if it doesn’t then we’ll want to pay attention. Note the strong correlation between the NFCI and the SPX.

- Raise your hand if you came into 2019 predicting Greek stocks and bonds to be amongst the best performing assets globally. If your hand is up then you’re a liar :). Also, notice there’s quite a lot of European assets in the top 10 which is funny because they’ve been universally shunned by investors.

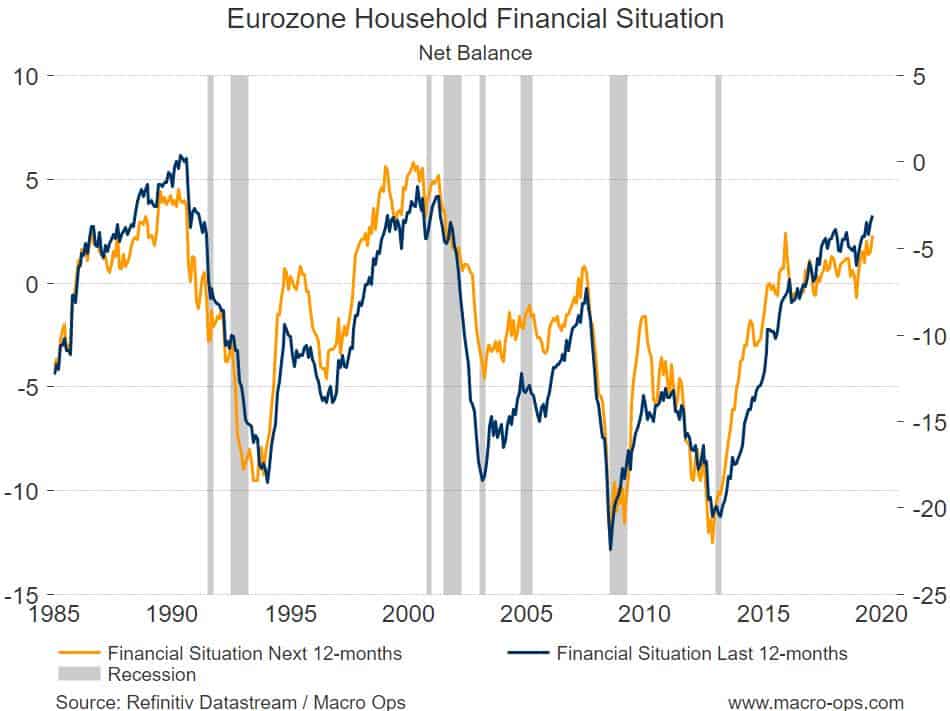

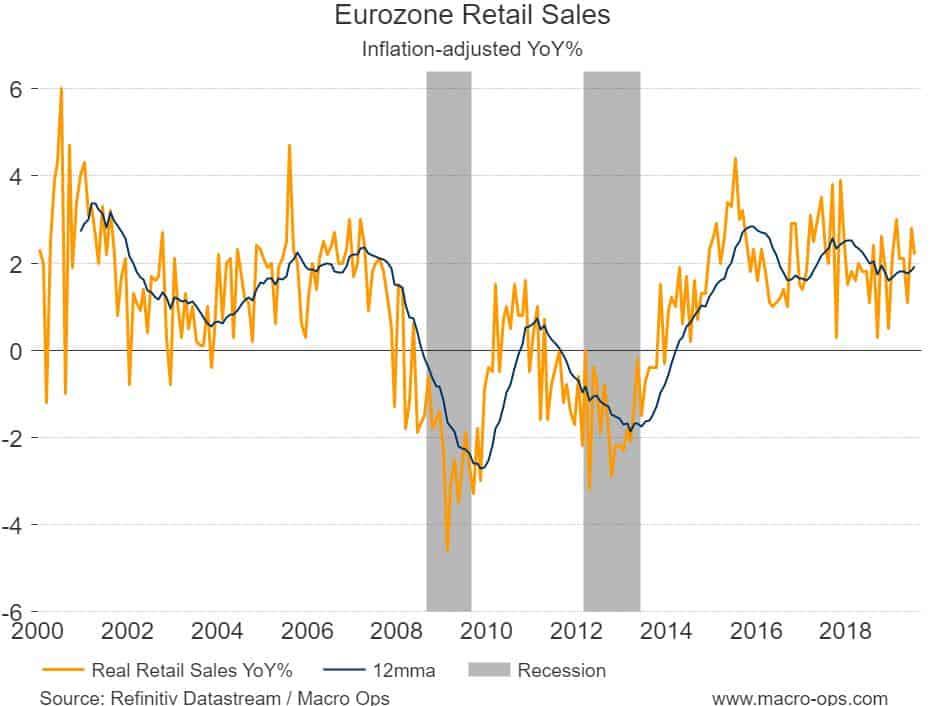

- There’s been constant negative coverage of the European economy over the last year with the manufacturing recession in Germany and fears over Brexit and all that. But it doesn’t look like anybody has told the European consumer. European households appear to be the most optimistic about their financial situations in a very long time.

- And inflation-adjusted retail sales are still growing at a healthy clip.

- The FAANG HODL trade may be nearing its end as things are looking a bit… much? This chart from BofAML shows that Tech as a share of profits vs. prior bubbles is at historic extremes.

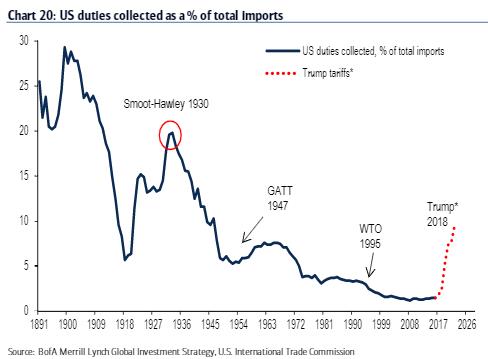

- The end of an era. Deglobalization is going to reshape the world in ways we can’t even begin to imagine. This trend is only just beinning and will play out for a looong time.