I never lock myself down to investing in one style or in one country because the greatest trade in the world could be happening somewhere else. My advice is to make sure that you do not become too much of an expert in one area. Even if you see an area that is inefficient today, it’s likely that it won’t be inefficient tomorrow. Expertise is overrated. ~ Jim Leitner

In this week’s Dirty Dozen [CHART PACK], we go over the technical and sentiment/positioning backdrop of the broader equity market, we reiterate our intermediate bullish bias but point out that extremes in short-term extension make this market susceptible to a shakeout/consolidation, and finally, we end with a look at a budding trifecta setup in cotton, plus more…

–

**Note: Enrollment to the Macro Ops Collective is now open.

The Collective is our premium service that offers institutional-level research, proprietary quant tools, actionable investment strategies, and a killer community of dedicated investors and fund managers from around the world.

If you want to protect your portfolio in this new market regime, make sure you become a member.

**Enrollment will stay open until Sunday, June 4th at midnight CST.

You can learn more about the Collective and what it can do for your investing here.

–

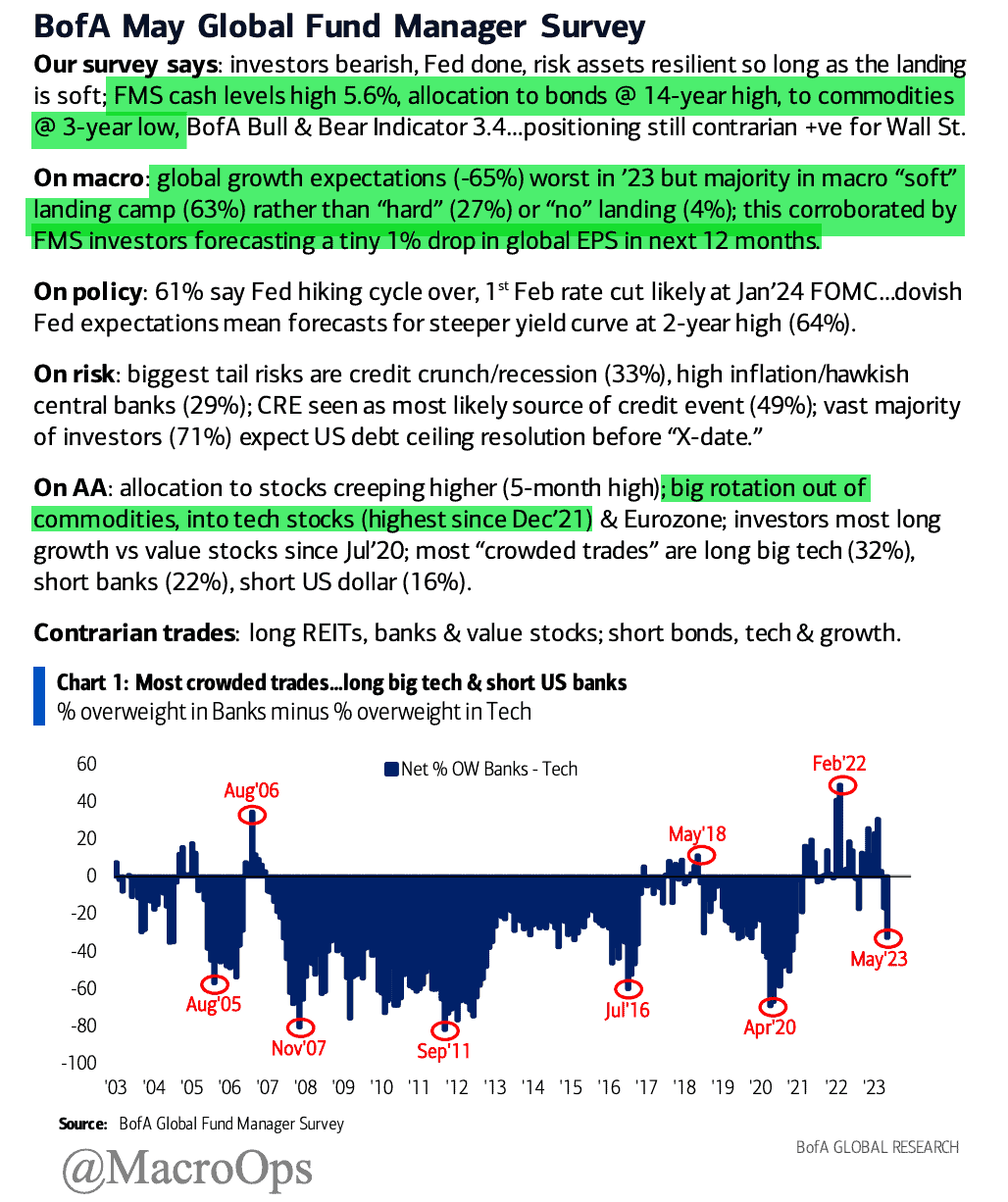

- The latest BofA Global Fund Manager Survey has some interesting tidbits… One that really stands out to me is how the majority remains bearish economic growth, but they also agree that a “soft landing” is most probable. Don’t forget that markets tend to hurt the most people most of the time, so it’s worth thinking through what that may look like (highlights by me).

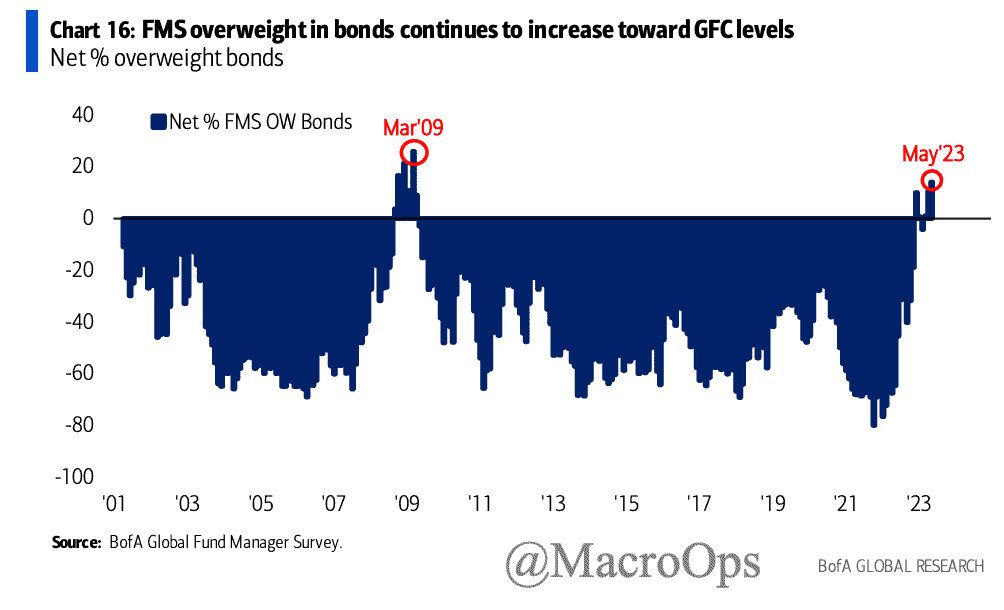

- A symptom of the bearish majority is that managers hold their highest overweight in bonds since the GFC (chart via BofA). That’s usually a good thing for stocks.

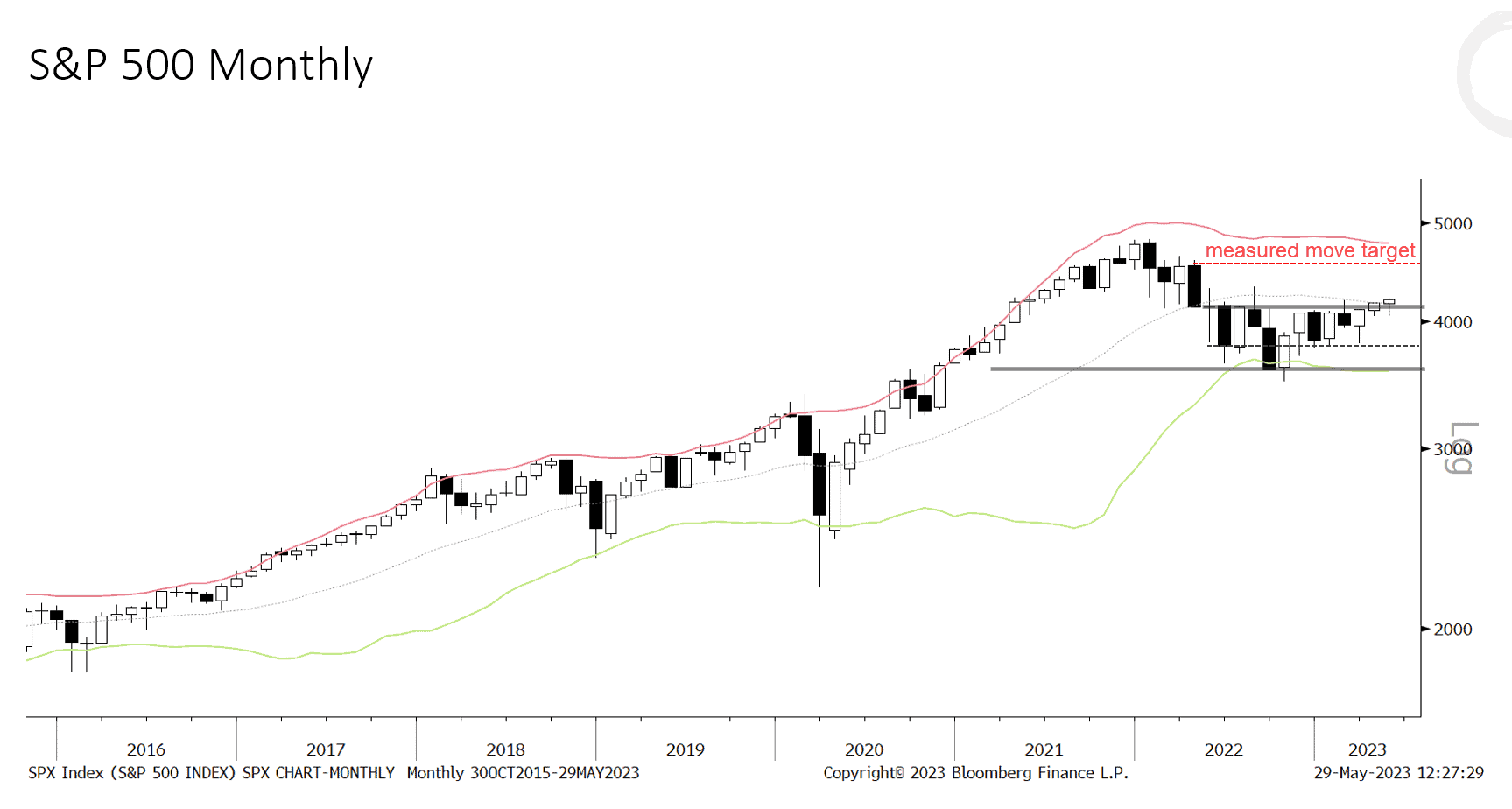

- There are only two more trading days left in the month of May. Barring a strong bearish reversal it looks as though the SPX will end the month with a bull and confirmation breakout bar from its 10-month trading range.

The April high (around 4,550ish or about 9% higher) is the measured move target for this breakout.

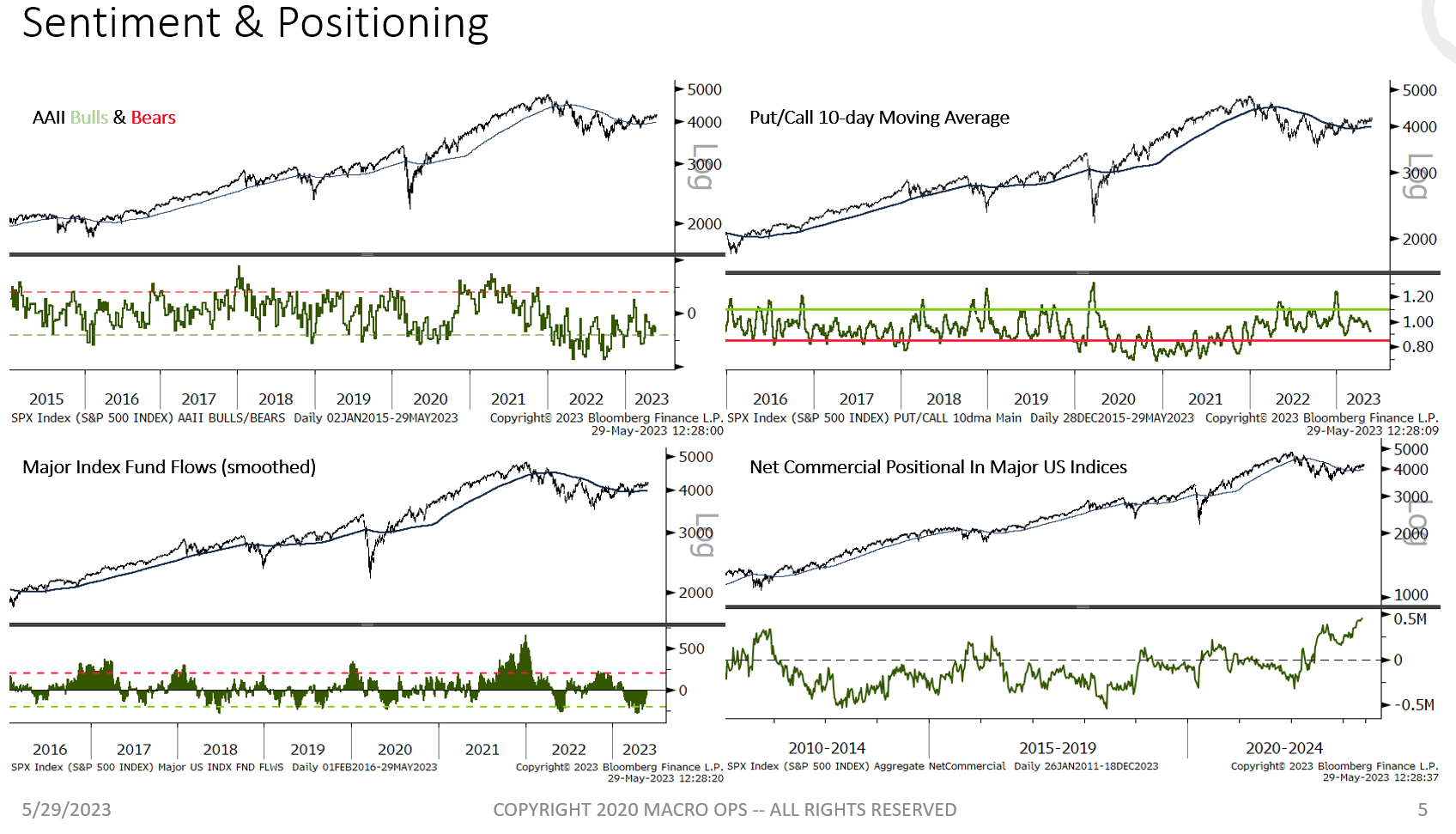

- One of the main reasons we flipped bullish back in Oct 22’ (link here) is because of the extremes we saw in bearish sentiment and positioning (read how sentiment drives prices here). This bearishness has been sticky despite the increasingly constructive tape (see charts below). This is why we’ve been and continue to be constructive on the continuation of this intermediate bull trend.

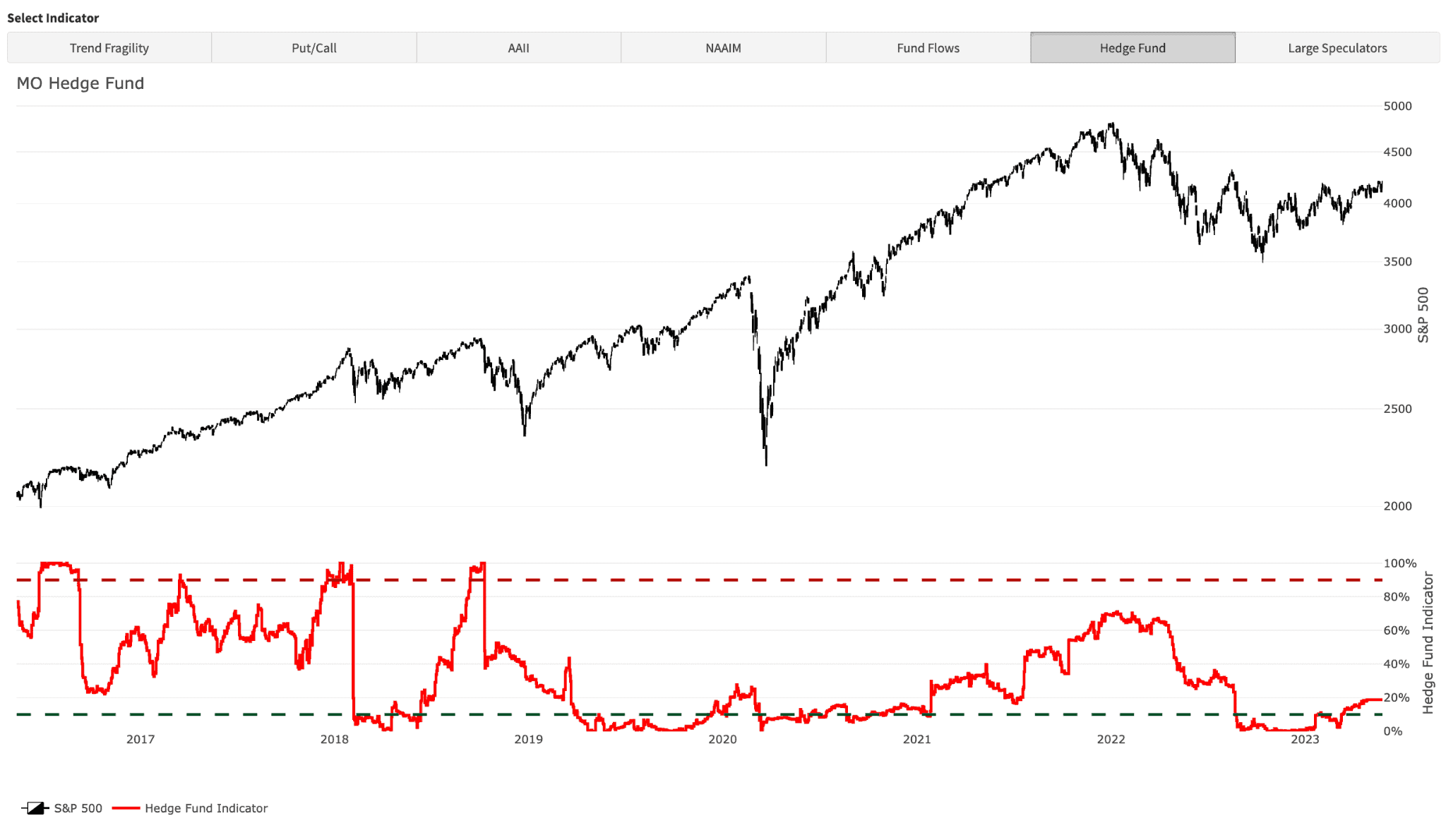

- To further hammer that point home take a look at hedge fund positioning, which remains below its 20th percentile. This is the group that tends to be wrong the most at market turning points and I don’t doubt that will be the case this time as well.

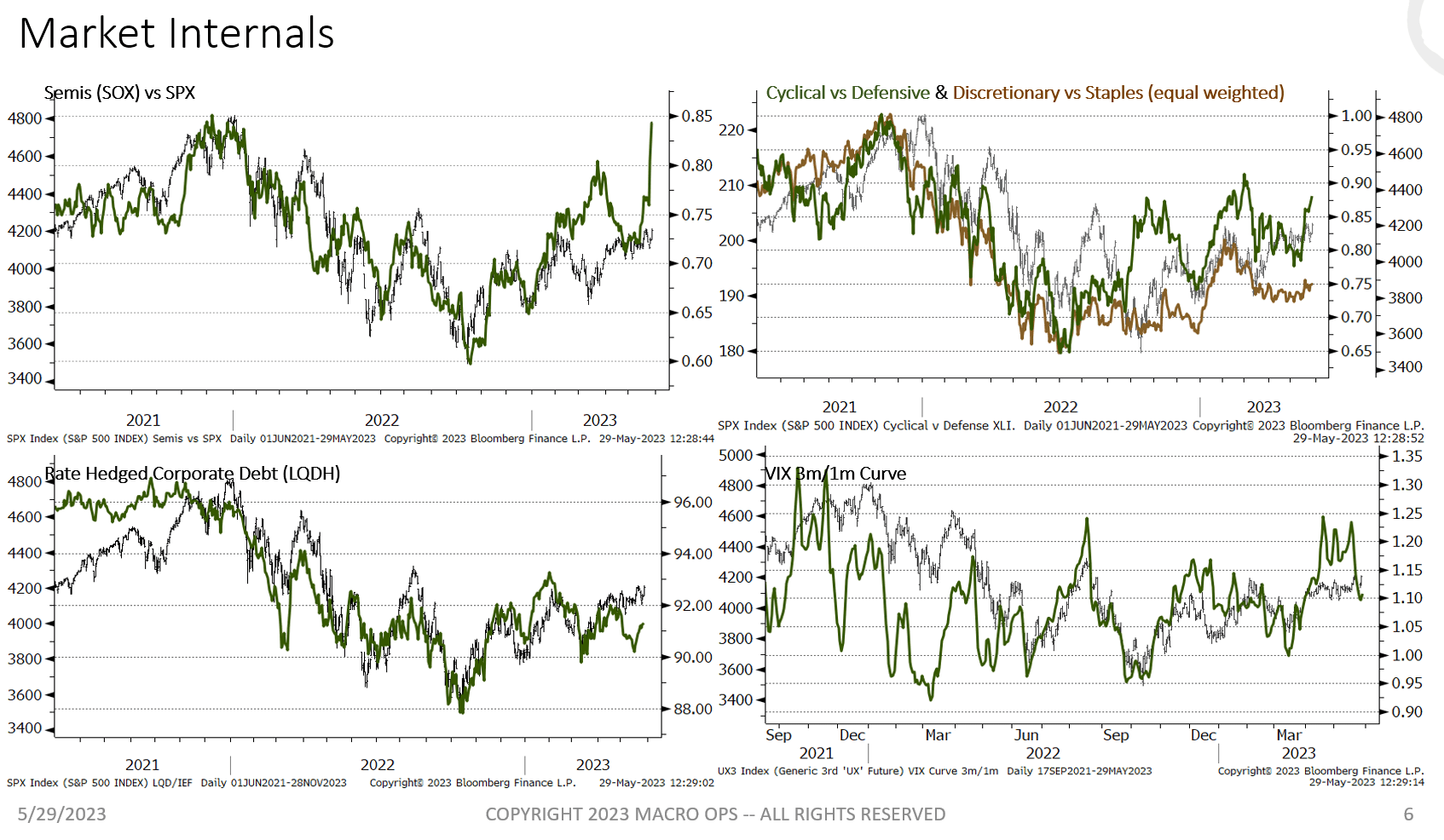

- Market internals also continue to support the intermediate bull trend in stocks.

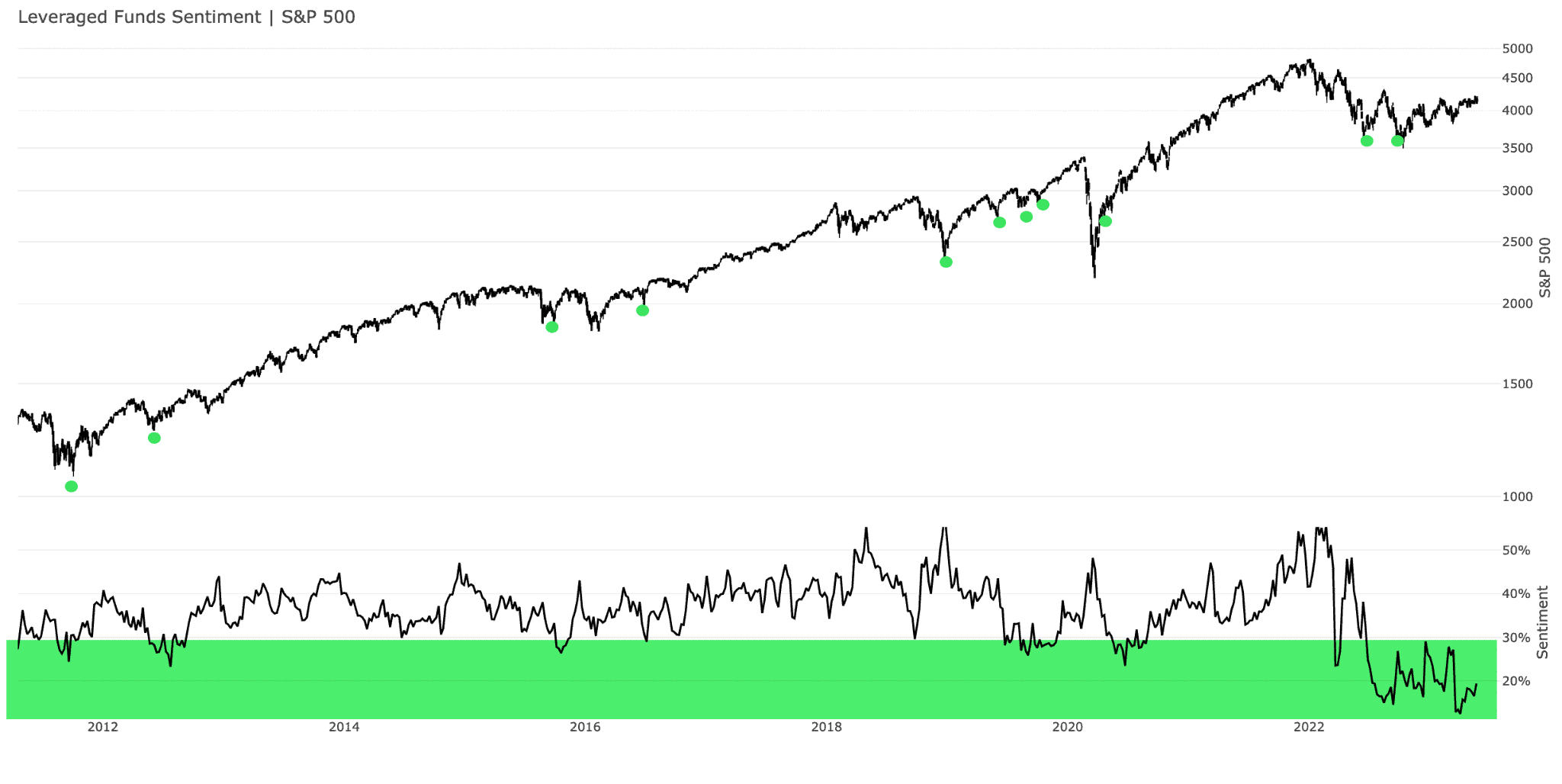

- Our modified CoT gauge of leverage funds again shows persistent extreme bearishness. This is not what tops are made of but are what bottoms look like.

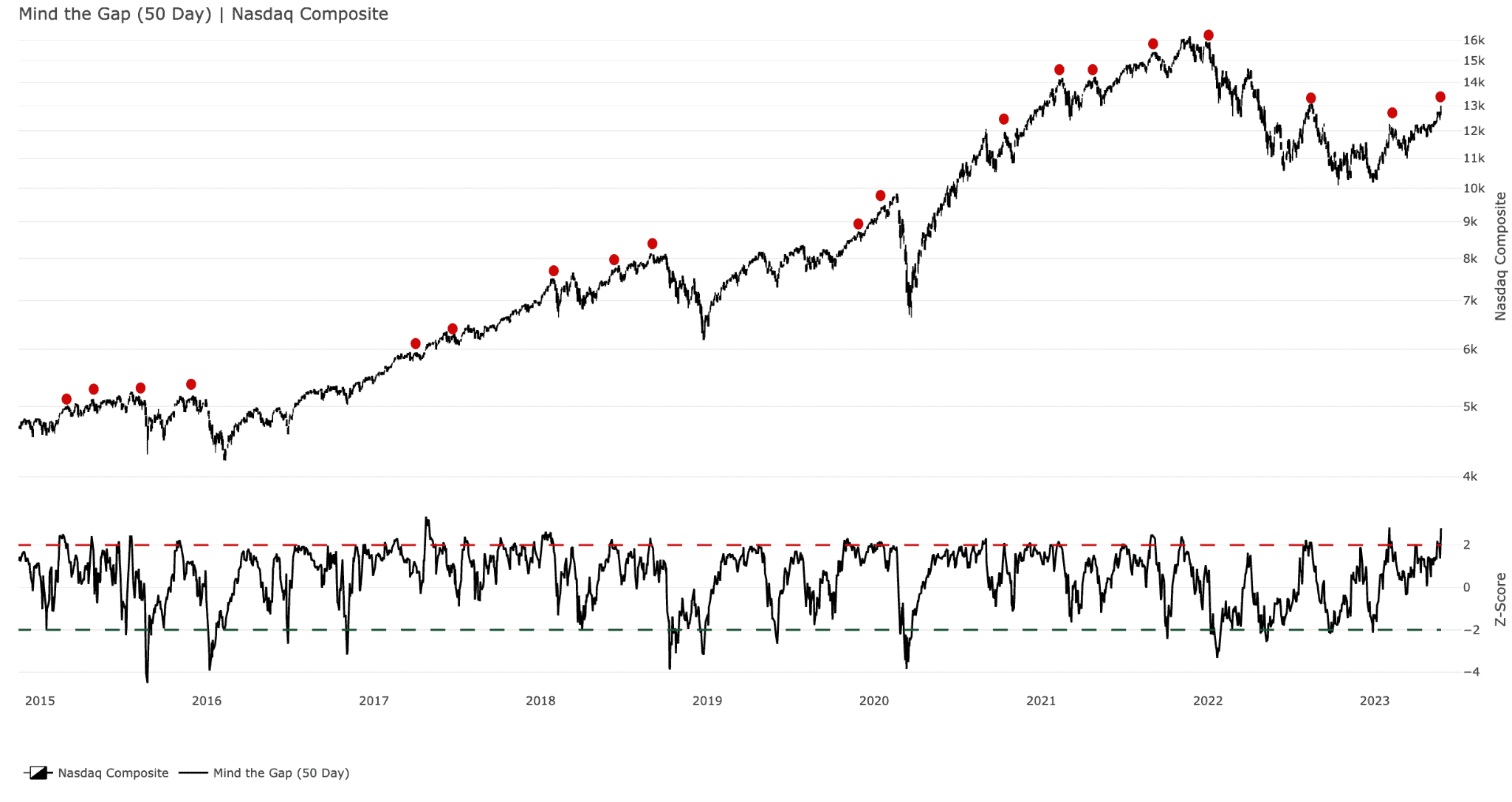

- But… while we are bullish the intermediate trend in stocks we have to be aware of short-term extremes in the tape. The Qs are currently over 2.5std above their 50-day moving average. Red dots mark past instances.

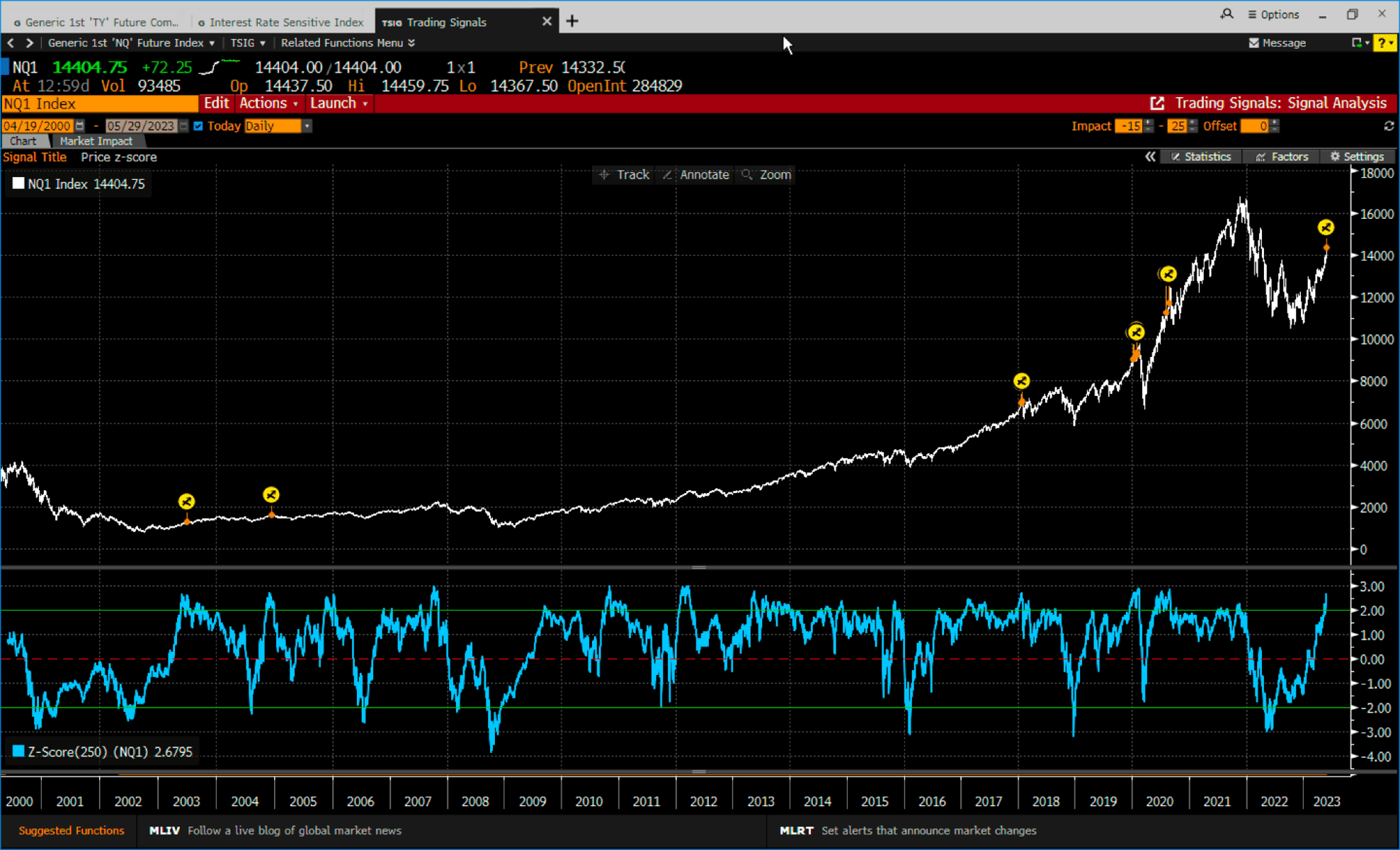

- Three forces are always at work within the tape (1) trend (2) momentum and (3) mean reversion. Here’s another way of looking at the current extreme overbought levels in the Nasdaq. The blue line shows the z-score of the price. The yellow dots mark all instances where it rose above 2.5std.

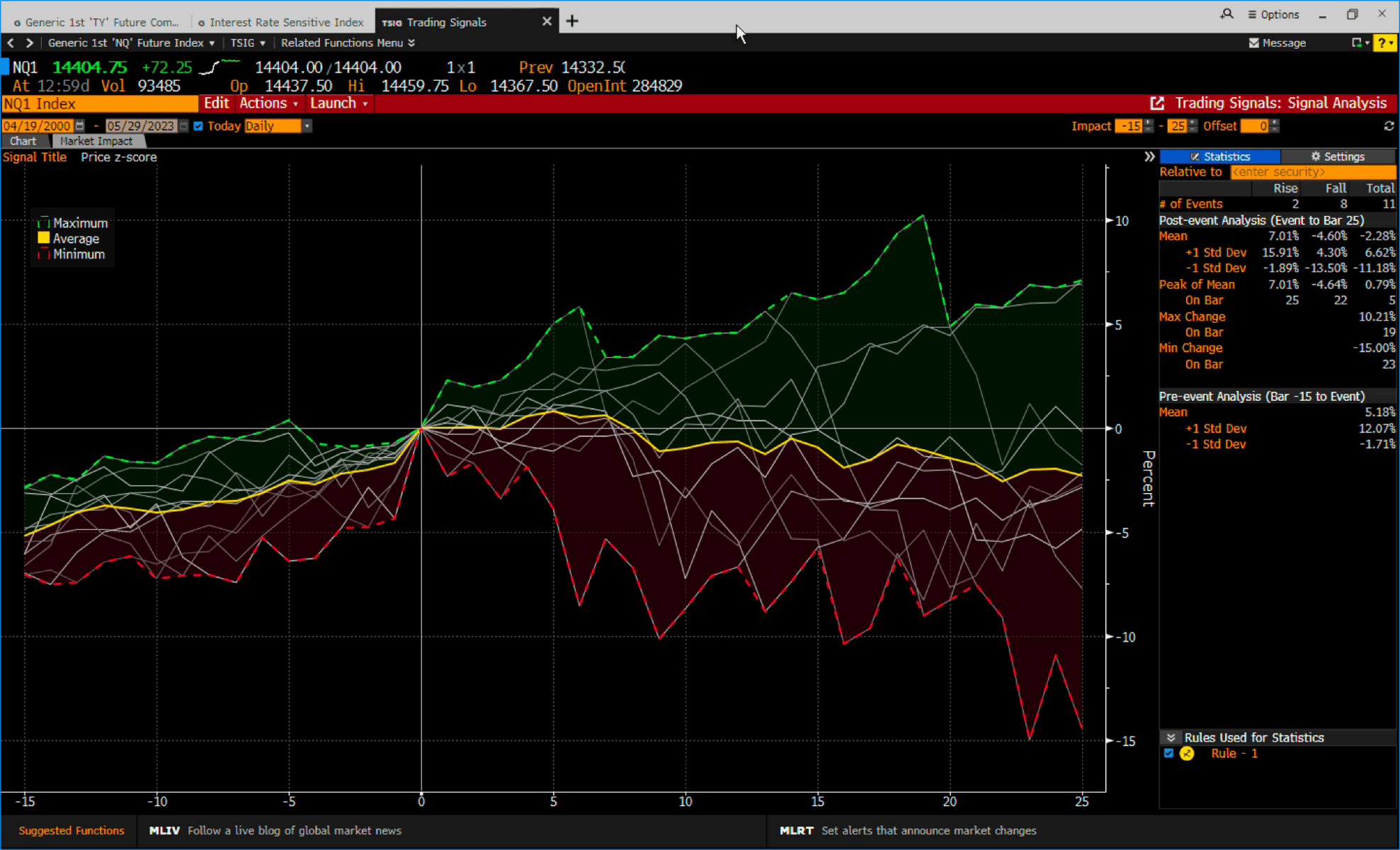

The graph below shows the follow-on returns over 25 trading days, with the yellow line marking the average, which in this case is -2.3%. So look out for mean reversion action over the short term.

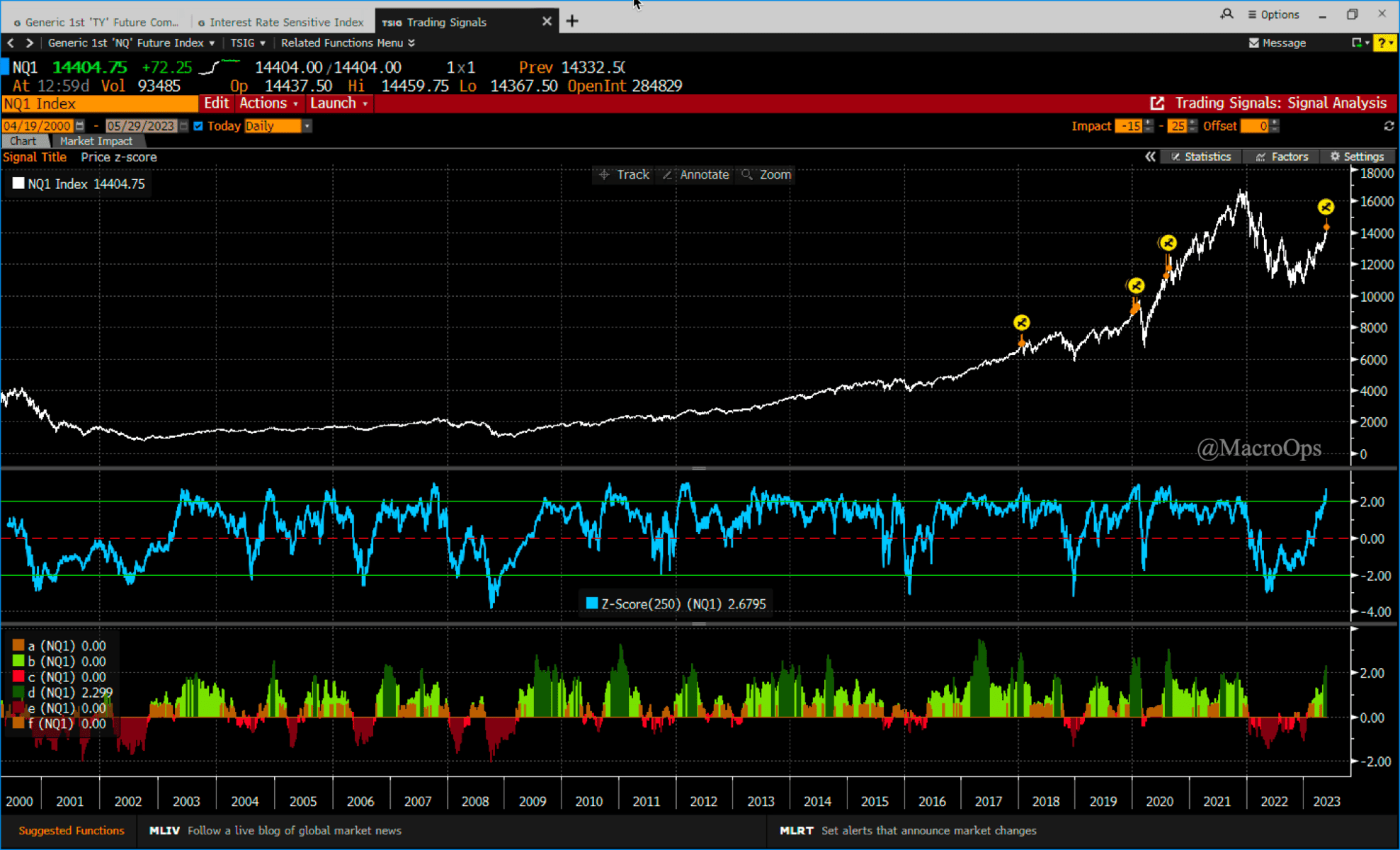

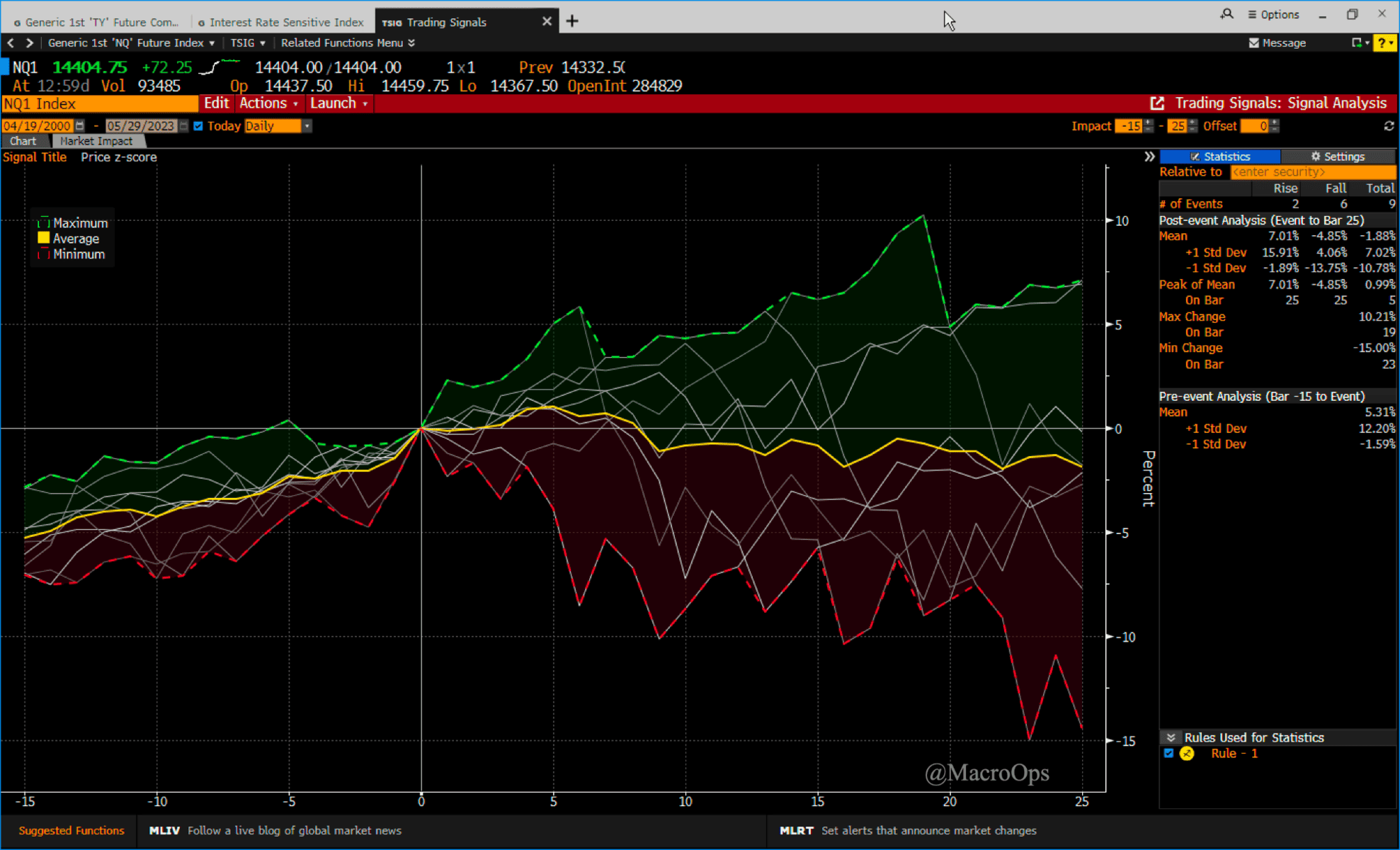

- We can further filter this down by including the SQN level, which is also near historical extremes.

There’ve been eight instances where the NQ z-score crossed above 2.5std and the SQN was in Bull Volatile above 2.5. Six of those saw negative returns over the following month.

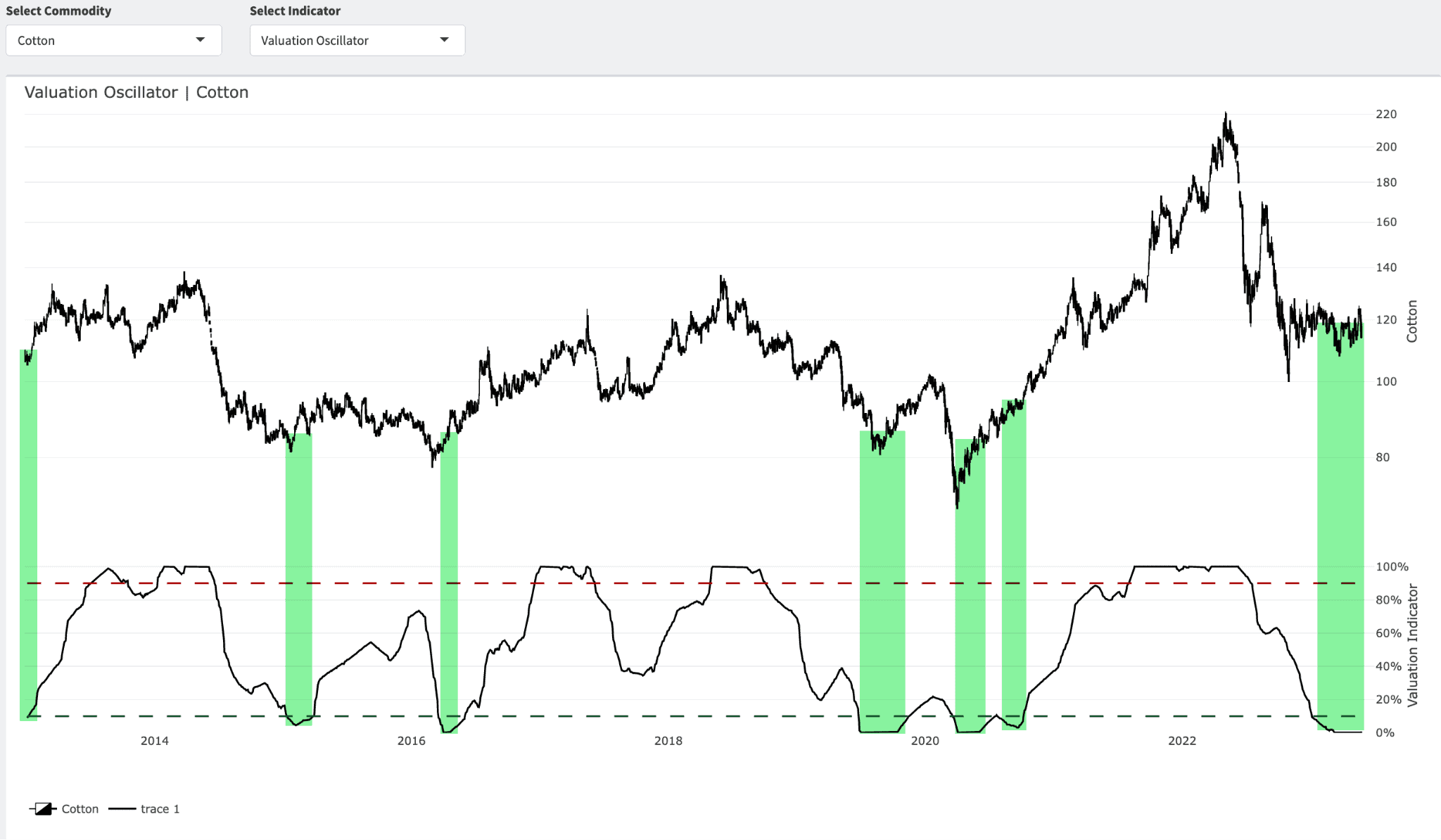

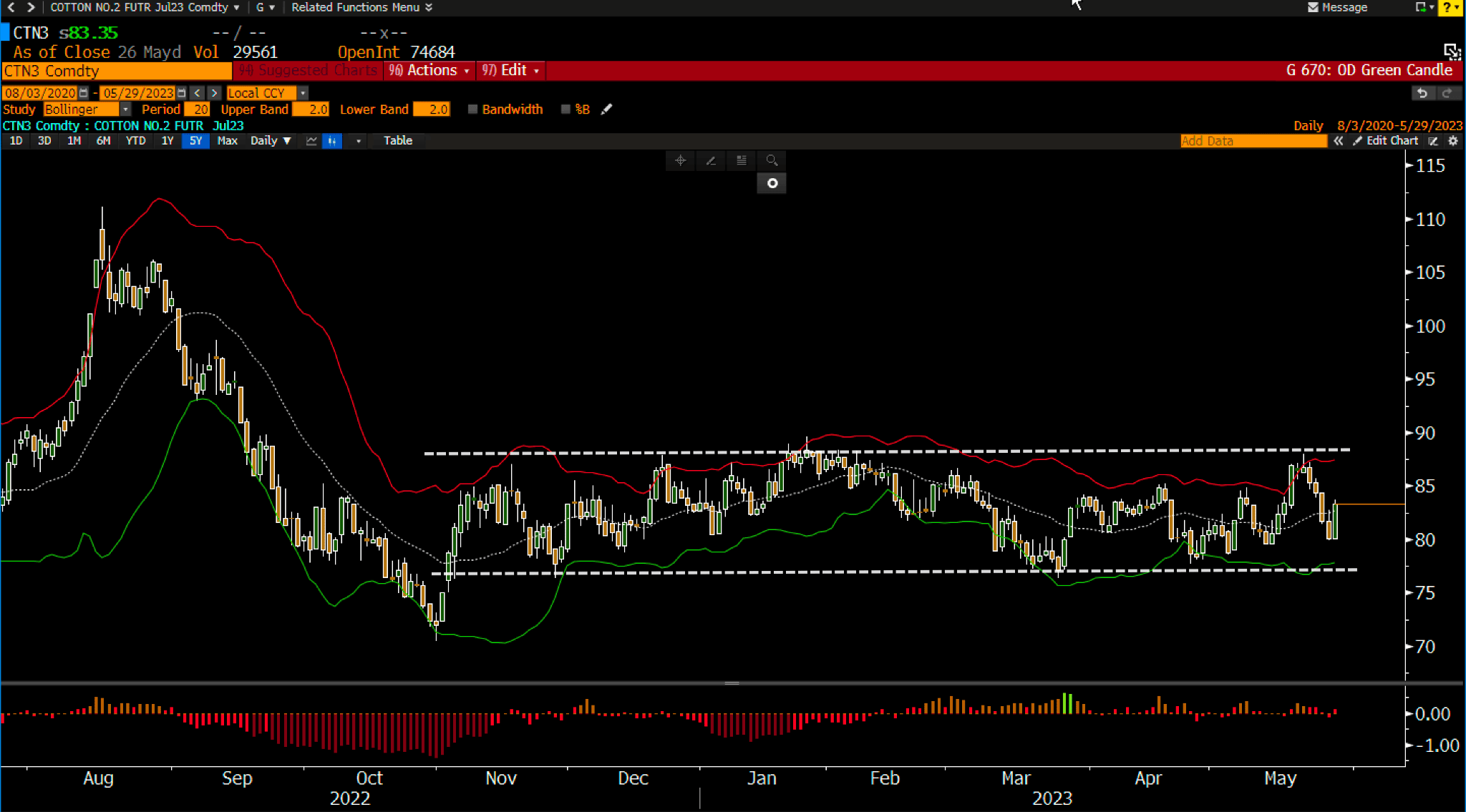

- One trade that we’re watching closely for a technical entry point is cotton. It has a trifecta setup forming. Our valuation oscillator is currently in the 0th percentile. Note how past low valuations marked or preceded major bottoms.

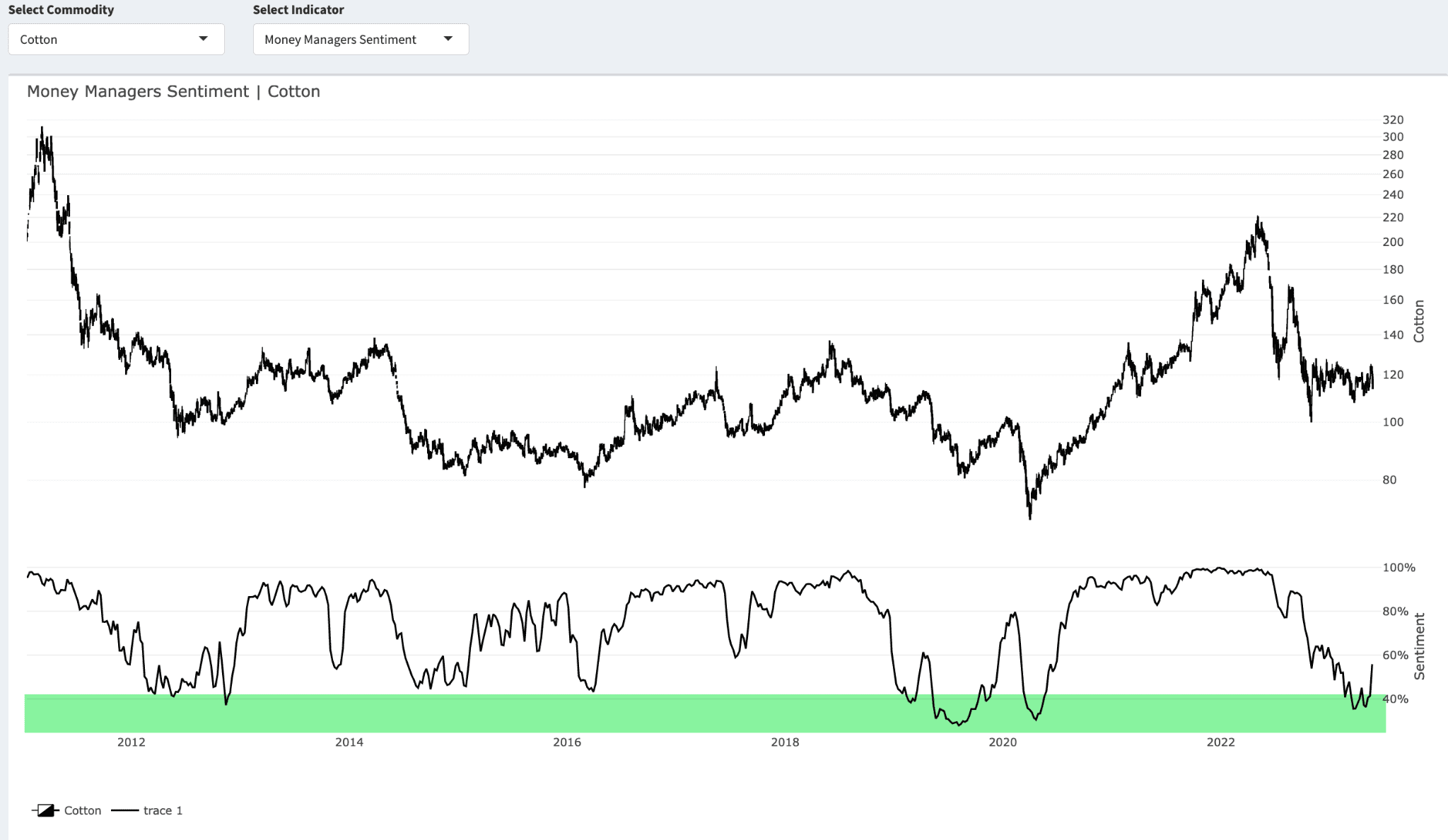

- Sentiment and positioning are also very bearish. Our gauge of Managed Money sentiment shows that it’s turning up from a historically low range.

The chart is in a 7-month rectangular trading range so there’s nothing to do at the moment but watch and wait for a breakout.

Thanks for reading.

Stay frosty and keep your head on a swivel.