(Note: This is an excerpt from a note sent to Collective Members earlier today.)

I want to share some quick notes on this selloff, the trade war and potential risks, some portfolio updates, along with an earnings update from our value guy, Mr. Bean, on Construction Partners (ROAD) latest quarter.

Let’s start with the trade war.

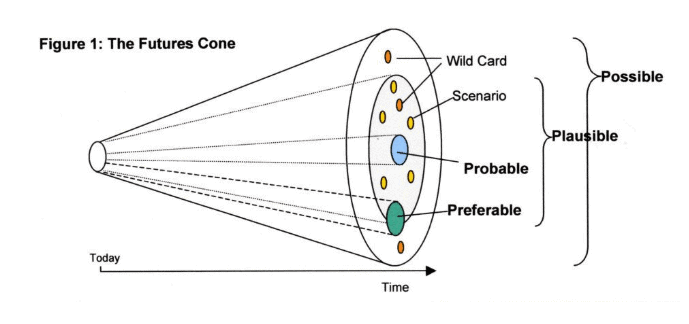

We often write about how the market reflects the aggregate range of reasonable opinions about what the future will look like (here’s a link to one of our writeups on the topic). In visual form, the concept looks something like this.

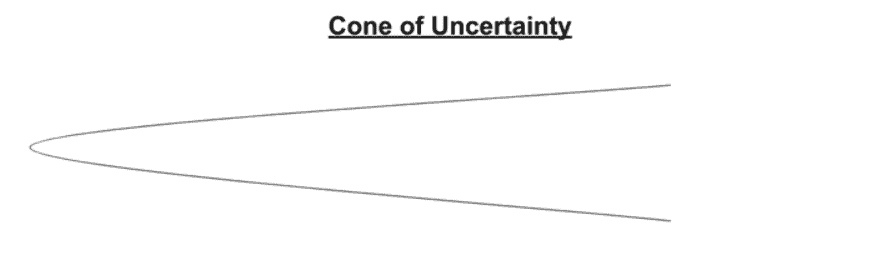

What happens when things like a trade war intensify is that the range of plausible outcomes expands. Uncertainty goes from looking like this.

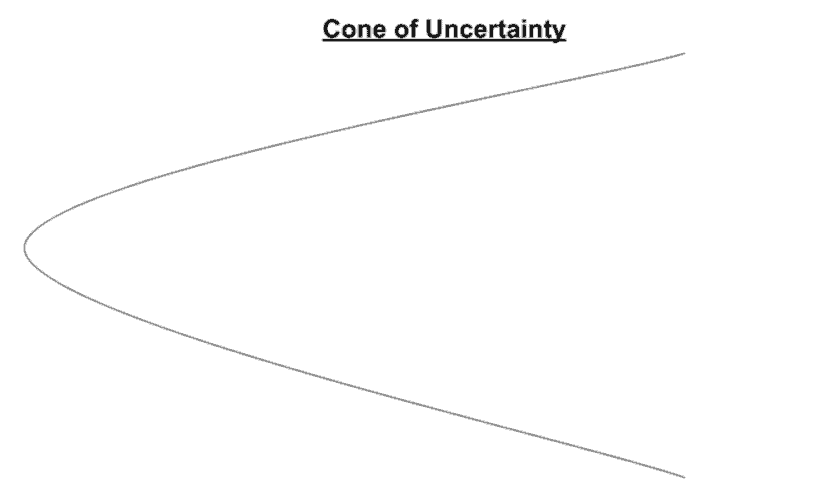

To looking more like this.

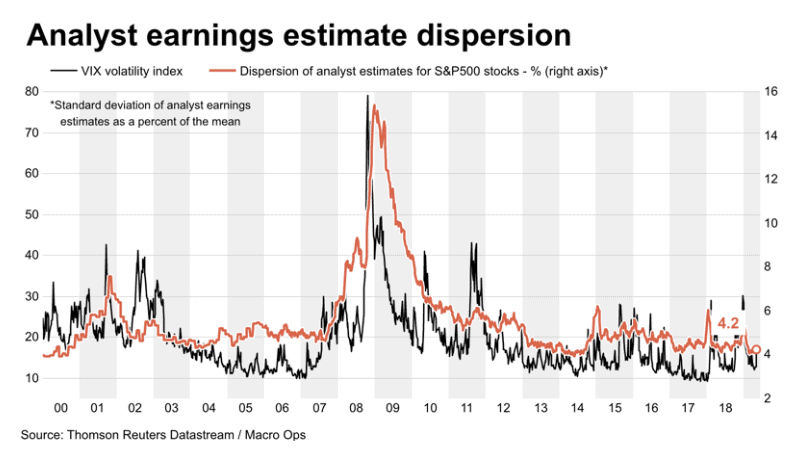

Uncertainty and volatility drive each other in a feedback loop as the market adjusts to new competing narratives as it seeks out a price that more properly reflects the new range of reasonable opinions. This is why analyst estimate dispersion tracks volatility. Both react to increased uncertainty over plausible and possible future outcomes.

The breakdown in trade talks and the tit-for-tat that is now taking place with Beijing recently stating they will raise tariffs on roughly $60bn worth of US imports after June 1st, is widening that cone of uncertainty and will continue to drive volatility higher until (a) the US and China make convincing progress on a deal or (b) the market reaches a price level, that along with sentiment and positioning, better reflect the expanded range of probable outcomes.

We talked in this week’s Brief how this ‘readjustment’ also happens to coincide with our indicators clearly showing stretched levels of bullish sentiment and complacent market positioning — as these events often tend to do. This will make the readjustment particularly volatile.

We should see the market bounce over the next week or so, seeing as how oversold it is on a short-term basis. But I want to reiterate that this rally should be sold into, not bought.

It’s likely we see this down-leg continue until the percent of stocks trading above their 50-day moving average moves near the 20% level (green area below).

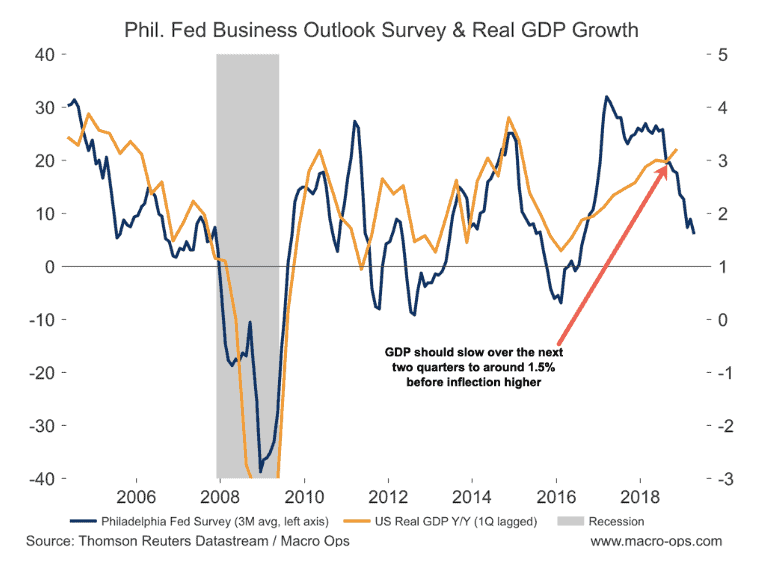

The major risk here is that the ensuing bout of market volatility feeds into the real economy and dampens consumer behavior enough that it tips us into recession. This is the whole “financialization of the economy” risks we’ve talked a lot about. The market “tail” now wags the economy “dog” which is why we saw such crappy data in January/February with retail sales falling through the floor. Consumers got spooked by the Nov/Dec market selloff and pulled back in their spending.

Considering the inflated GDP print last quarter that was due to a buildup in inventories and where growth in the US is headed now, the economy is skating on increasingly thin ice. A market shock could be the thing that plunges it through. Not saying that’s going to happen. But it’s certainly worth keeping in mind.

Moving on to our portfolio.

We’re taking profits and closing out the rest of our long Facebook (FB) position. Growth stocks should continue to get needled in this new regime, as I talked about in our most recent MIR. On that same note, our value plays are holding up much better than the broader market which is a good sign we’re seeing a rotation out of growth and into value happening.

We also got stopped out on our Gaia Inc (GAIA) trade yesterday. The bullish thesis is unchanged but that thesis is kaput until the market starts agreeing with it. In hindsight, I mismanaged the trade by sizing too large at 1% risk with too tight of a stop. My conviction behind the trade skewed my better judgment and as a result, our portfolio is the poorer for it. I plan on putting out a more extensive review of the trade soon.

Construction Partners (ROAD) came out with earnings recently and crushed it. Here’s Mr. Bean’s comments on the report (link here). ROAD is roughly 10% of our portfolio. I want to eventually build it into a 15-20% position.

Precious metals have been getting a bit of a bid the last few days. From a technical standpoint, they aren’t completely out of the woods yet. We need to see a higher swing low before I feel comfortable adding to our silver and AngloGold (AU) positions. There’s risk we see the dollar pop here which would likely stop us out of our starter positions.

Also, keep watching oil. It’s bouncing around its 200 and 50-day moving averages but, as we talked about in the Brief, positioning is stretched and due for a reset.

That’s all I’ve got for now.