Today’s Note and Stock Shopping List

Hope everyone is recovering well from their New Years celebrations and ready to dive back into markets for the year.

Just wanted to share with you some quick thoughts on the market, the dollar, and gold. And then at the end, I’ve got our Stock Shopping List with our favorite names that we’re looking to begin buying over the coming weeks.

Alright, let’s jump in…

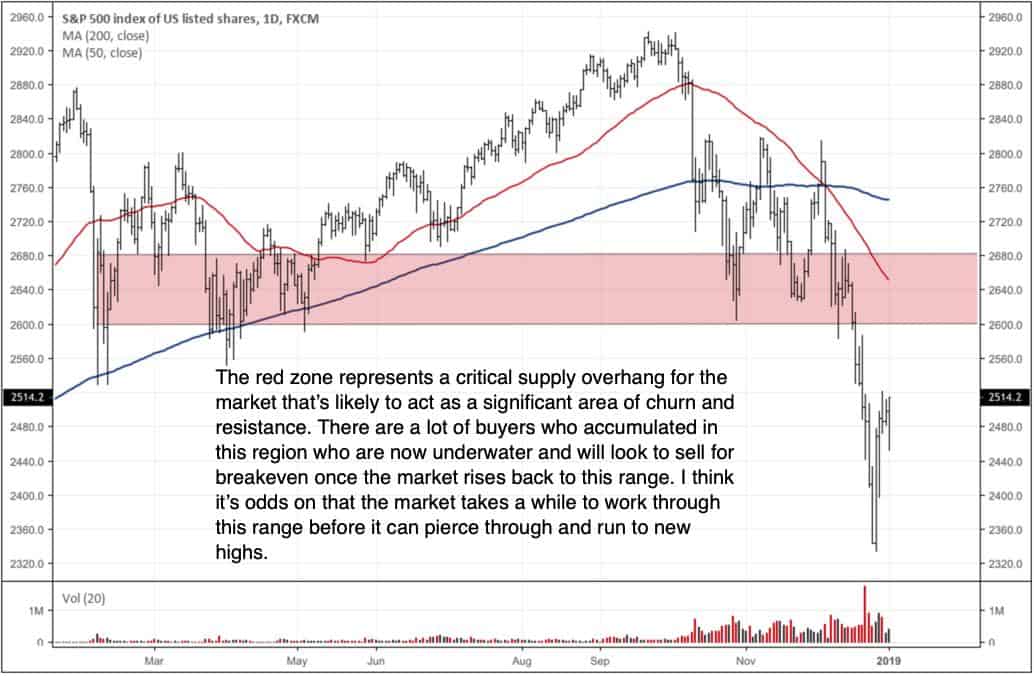

The S&P 500 is trading higher off a short-term bottom. We should see it run up into the 2,600+ range — its 50-day MA acting as an attractor (red line) — but as I note on the chart below, the market is going to bump into significant resistance here. There are a lot of players who bought into this range that are underwater and who will look to close out their positions for break even once price climbs back to these levels. This is called a supply overhang.

With large supply overhangs like this, it typically takes the market a number of attempts before it can break through and move to new highs. The supply needs to be worked off and so I’d expect to see a reversal around the 2,650-75 range followed by a selloff to recent or even new lows — double bottoms are typically the pattern we see after large selloffs like these.

This action will also help to reset that last bit of stubborn sentiment I pointed to in last week’s market update.

Last week, I tweeted this about gold.

Here’s a closer look at the chart. Gold is now at a major make or break inflection point (chart below is a weekly). If it’s turned away and closes lower for the week then that sets it up for a good sell signal.

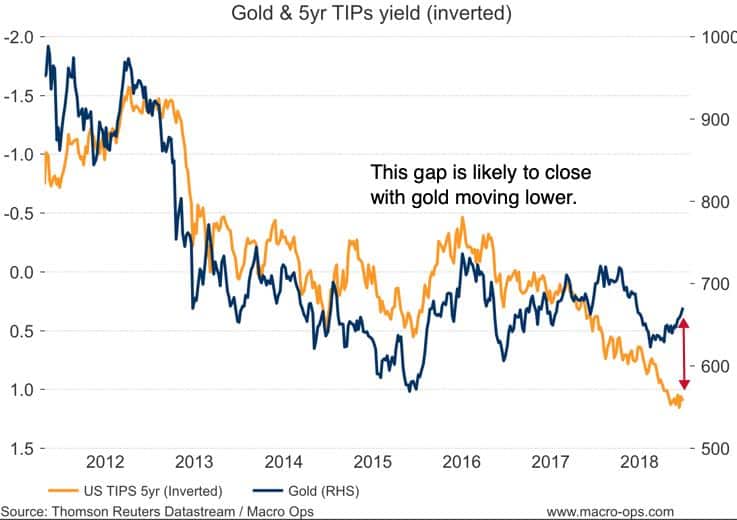

For those of you who are new to the group, I view gold as a reflection of global relative demand for USD assets (ie, the relative attractiveness of USD assets such as stocks, bonds, and the dollar versus the RoW). This is why gold trades in lockstep with relative equity momentum of EM vs. US equities.

The RoW is currently seeing slowing economic growth while growth in the US remains relatively strong. This higher growth is driving higher real rates in the US. The below chart shows the widening gap between the inverted yield on TIPs (the real yield) and gold. We should see this gap close with gold going lower.

I’ve also commented in the past about how platinum often leads gold. The current gap between the two metals should be concerning for gold bulls (red lines is platinum and black is gold).

One thing to note is that January tends to seasonally be the strongest performing month for gold (chart via Commodity Seasonality). You don’t ever want to trade off seasonality alone but it’s something to keep in mind. I think after the unusually strong December month for the yellow metal that perhaps that performance was pulled forward. In any case, let’s watch gold closely. A weak weekly close will set it up for a high R/R short opportunity.

And then we’ve got the dollar.

Last week I noted (link here) how the divergence between gold and the dollar and how gold often leads the dollar at turning points. The key word there is often, as in not always. That relationship may or may not hold this time around. So stay open minded and flexible.

The EURUSD might be seeing a key reversal day today. We’ll need to see if it holds into the close. The aussie is also making new lows against the dollar. Ultimately, we want to be short both pairs against USD.

The reasons why we want to be long the dollar against the euro and the aussie are pretty much the same for both. When looking at currencies we want to look at: rate differentials, growth differentials, relative equity momentum, and positioning.

Capital flows to where it believes it will earn the highest risk-adjusted return. Both Europe and Australia have large exposure to China — which just printed its first contraction in PMI since May of 17’ — while the US economy is more insulated to slowing Chinese demand.

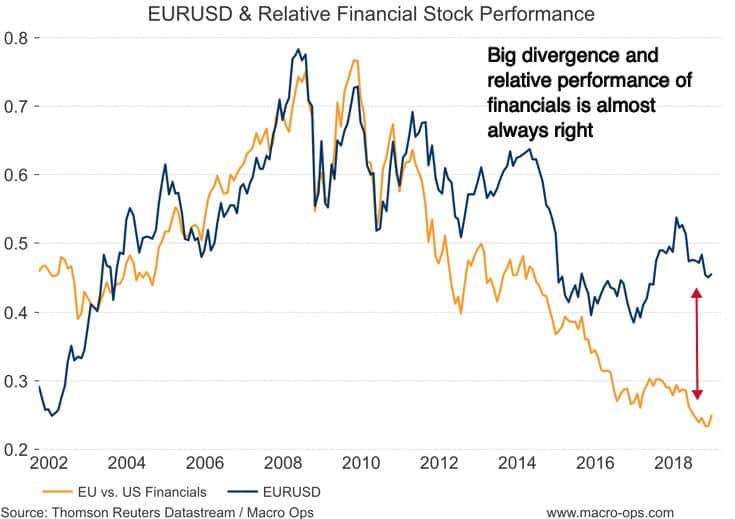

Looking at the euro (though same holds true for the aussie) we can see that relative financial stock performance between the US and Europe favors a much lower euro. Financials trade off growth and rate expectations which is why this is a key indicator to track for currency pairs as the relative financial stock performance almost always leads.

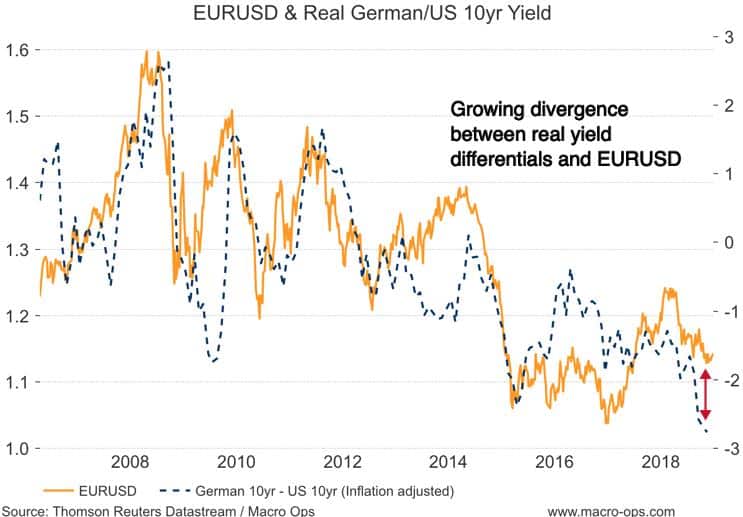

The most important rate differential to track is the real (inflation-adjusted) 10yr yield. The current difference in rates also suggests we’ll see a much lower euro.

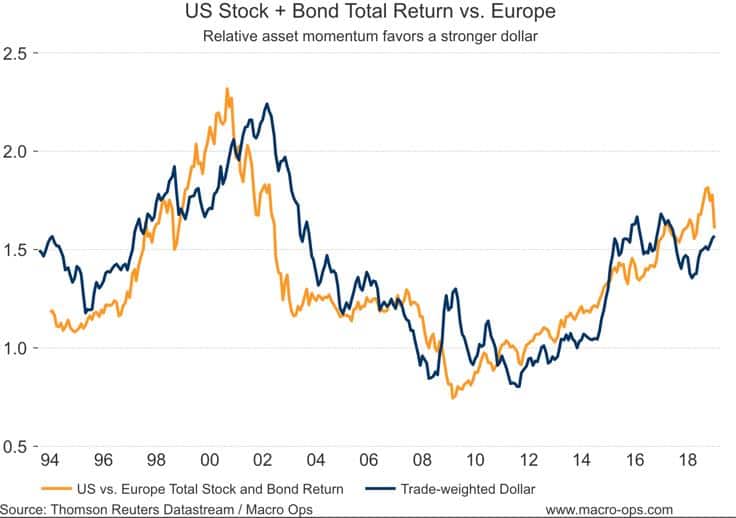

Relative total stock and bond performance favors a much stronger dollar versus the euro.

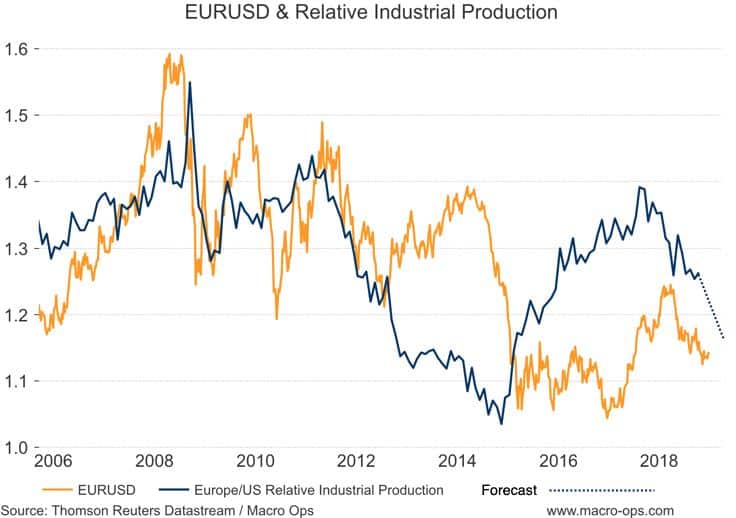

And the trend in relative economic growth favors a much lower EURUSD pair.

The short-term bear case against the dollar is just that positioning and sentiment remain somewhat crowded to the long side, though much of this has been worked off and is now less of a headwind. And then, the gold divergence which I mentioned above and which is hardly an iron-clad heuristic.

Technically, EURUSD remains in a tight coil resting on significant support in its 200-week moving average. This is around the spot 1.13 level. If we see a weekly close below this level then I think it’ll be high-time to load up on short EURUSD. But, until then, we’ll patiently watch the dollar pairs from the sideline.

Now onto our Stock Shopping List.

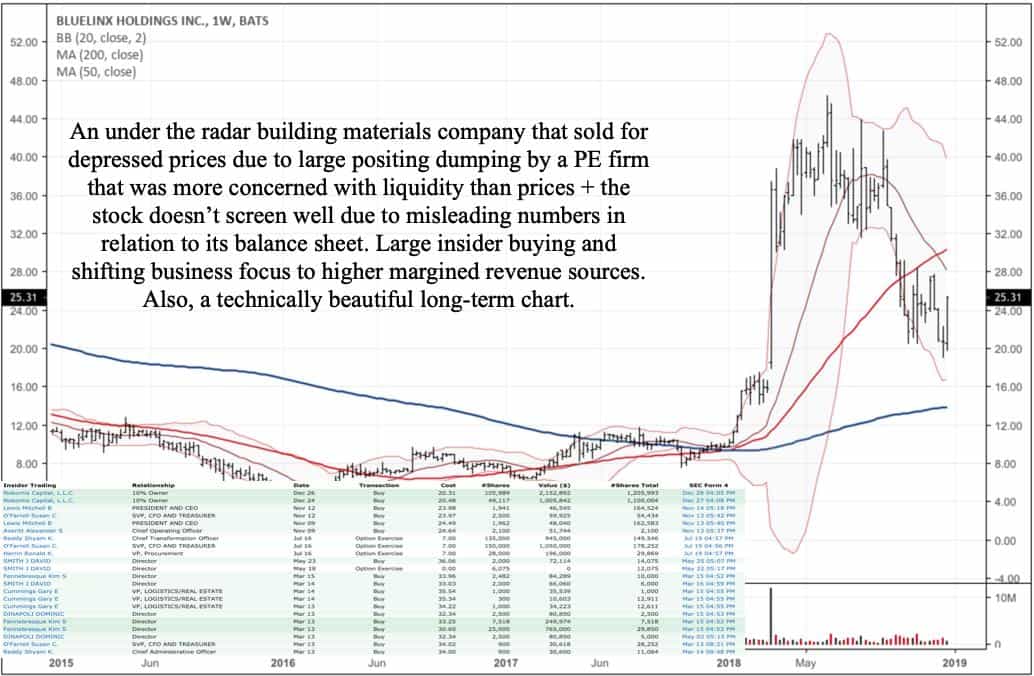

BlueLinx Holdings (BXC)

The best risk/reward opportunities are typically found in stocks that don’t screen well. This is due to the rise of quants along with the free and wide access to a plethora of various screeners and algorithmic stock ranking systems available to any and all. Because of this, any obvious quantifiable mispricing quickly gets repriced in the market. Long gone are the days when buying a stock just because it has a low PE made you money.

Now, the best opportunities are in stocks that are mispriced because their true value is distorted and disguised by the popular GAAP accounting numbers and ratios that people typically look at. If you’re interested in reading more on this then check out our Value Investing Manifesto.

BXC is one of these stocks.

The company is a wholesale distributor of building products with distribution centers across the Eastern US. Previously, BXC served as the captive distribution arm of Georgia Pacific (GP) which is the country’s largest producer of plywood. In 2004, BXC was spun out of GP by a private equity buyer who did what PE firms do, they saddled the company with lots of debt. This wasn’t great timing of course, with the housing crash just around the corner and all. And in 2017, the PE firm was forced to liquidate its holding in the company at bargain prices.

The stock is underpriced because it doesn’t screen well. The GAAP balance sheet likely understates the value of the company’s real estate to the tune of a couple hundred million dollars while also overstating its leverage.

Here’s the following from Matt Sweeney of Laughing Water Capital on the opportunity in BXC (with emphasis by me).

While buying from a seller that is not concerned with price is a good place to start, by itself this is not

sufficient for investment. We were further attracted to the business because of its misleading GAAP

balance sheet, which we believed under-stated the value of the company’s real estate by almost $200M.

Importantly, the company had been monetizing their real estate through sale-leaseback transactions,

which allowed the company to paydown debt. While the mechanical screeners that rule the markets were viewing the company as levered ~8x, we believed the company had already reduced its leverage to ~6x, and could be theoretically almost debt free if they simply continued to monetize their real estate.

More important than this theory however, is the reality: they just don’t need all of the land they have.

Because the company started as a part of GP, their footprints were designed to accommodate storage of plywood and other sheet goods. Storing plywood requires a lot of space for a small amount of margin, and is thus not a good business to be in.

Additionally, a look at BXC’s product mix vs. public competitors showed significant room for margin

expansion through moving into more value-added aspects of the building supply distribution business.

Combining the above elements, I felt that BXC was significantly mis-understood by the market, and that

there were multiple ways to win in the years to come.

What I did not consider was that BXC would announce a merger with a competitor that has a highly

complementary business and footprint only months after our purchases. Shares more than doubled on

the news, driving BXC into a top 5 position for us. While it may be tempting to just take the money and

run after a move of this magnitude, reviewing the transaction indicates that the combined company may

be cheaper now in the low $30s than it was below $12 just a few months ago. This is a business where scale matters, and the opportunity to take costs out of the combined business and drive revenue through consolidating the footprint to more fully utilize square footage, leveraging purchasing power, leveraging administrative resources, and cross-selling complimentary products is very real. It is not difficult to envision scenarios where the combined company can generate $8 to $12 in free cash flow per share looking out a few years, which when combined with a likely de-leveraging of the balance sheet leads to the potential for significant additional upside.

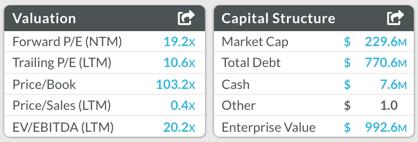

An expanding business that’s moving into higher margined products combined with the benefits of increasing scale make BXC an attractive company. The opportunity is made even richer when you also consider the pace of deleveraging in the balance sheet (lower debt makes the equity worth significantly more) and a business that should be generating $10+ in free cash flow in the coming years. The stock is currently only trading at $25…

Insiders think the stock is a steal at current prices and have been loading up on it — typically a good sign. And from a technical perspective, the chart looks great. It’s broken out of a large base and has now retraced to the lower band of its weekly Bollinger Band.

For more info on BXC you can read this dated but still relevant write-up from Adestella Management on the company (link here).

To be continued…