Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

Our New Show On Real Vision, The One Thing — AK, the host of our partner brand Fallible has a new show on Real Vision!. We’re super excited to work with these guys, Real Vision produces some of the best financial content out there. The pilot episode is called “The Crypto Conundrum.” If you are interested in bitcoin click here to watch!

Articles I’m reading —

Patrick O’Shaughnessy and team over at O’Shaughnessy Asset Management put out their latest quarterly report/research piece. It’s a great piece where they explore “factors within factors”, specifically looking at “peak yield” which is a company’s cumulative total buyback percentage since its peak share issuance. They then slice the funding sources for these buybacks into “capital pies” and combine it all with the valuation multiple at which the share repurchases took place. This more granular quantitative look at share buybacks gives them “alpha within factors” and improves upon just a plain vanilla quantitative use of buybacks as a factor.

It’s a short read and offers an informative look into where quantitative investing is going (here’s the link).

The New Yorker published a profile on Chinese Novelist, Yan Lianke, titled Yan Lianke’s Forbidden Satires of China, which was the best thing I read all week. The article gives an insightful, sad, and sometimes humorous look into China’s recent past and present.

There are some great lines in the piece. Here’s a few of my favorites.

Because information is so tightly controlled, generations of Chinese have been dream walking through life without realizing it, becoming zombies primed to live in accordance with state dictates. Waking up is unimaginable, because living in reality would require one to confront the atrocities of Chinese history, and to understand the catastrophe that the Party has visited on the country. To be Chinese, then, is to live under enforced amnesia, a medicated slumber of propaganda.

…

He surmised that Communism, by controlling every aspect of people’s lives, had infantilized generations of Chinese: “People’s sense of themselves as individuals atrophied, so much so that they lost common sense ideas of how to behave ethically without strict parameters.

And when asked about the current political situation in China, this was Yan’s response:

Yan shook his head and responded that it was beginning to remind him of the Cultural Revolution.

Entrekin’s (Yan’s publisher) eyes widened. “Surely it can’t be that bad,” he said.

Yan explained that, particularly since the removal of Presidential term limits, last year, he had sensed a gradual backsliding, especially when it came to issues of free speech. Not only has he frequently been prevented from publishing new books but publishers have also suppressed his backlist: “Anything that has the name Yan LIanke is indiscriminately removed from the shelves.”

There was a brief silence.

China is going through what will be a long and painful deleveraging. Throughout history, the backend of the debt cycle has more often than not, coincided with periods of extreme political regression, militaristic nationalism, and other fun stuff.

What if China is in the beginnings of another “Cultural Revolution” type period. What would that mean for markets, geopolitics, the prospects for war? Here’s the link.

The team over at Evergreen Gavekal recently shared one of my older write-ups on the tightening oil market and provided a great update to the thesis. I believe this is going to become a major macro thematic going into next year and will drive oil prices higher. It’s definitely worth reading to stay abreast on the theme (link).

Lastly, Greenwood Investors put out their latest investor letter where they shared some updates on a few of their favorite deep value names. Their stuff is always worth a read. Here’s a clip and the link.

Telecom Italia is trading at a valuation lower than a Russian telecom, and the country is being treated by investors today as a banana republic. We’re not going to get into a macroeconomic discussion here, but let’s just say we’re finding ourselves increasingly in disagreement with the “establishment” in Brussels which looks determined to prohibit independent government policy despite growing revolutions in nearly every country. Leading economic indicators in Italy are still positive and outperforming much of the rest of Europe, just as investors have decided they are not interested at any price. We have been taking advantage of this wide gap between sentiment and reality and price-agnostic selling.

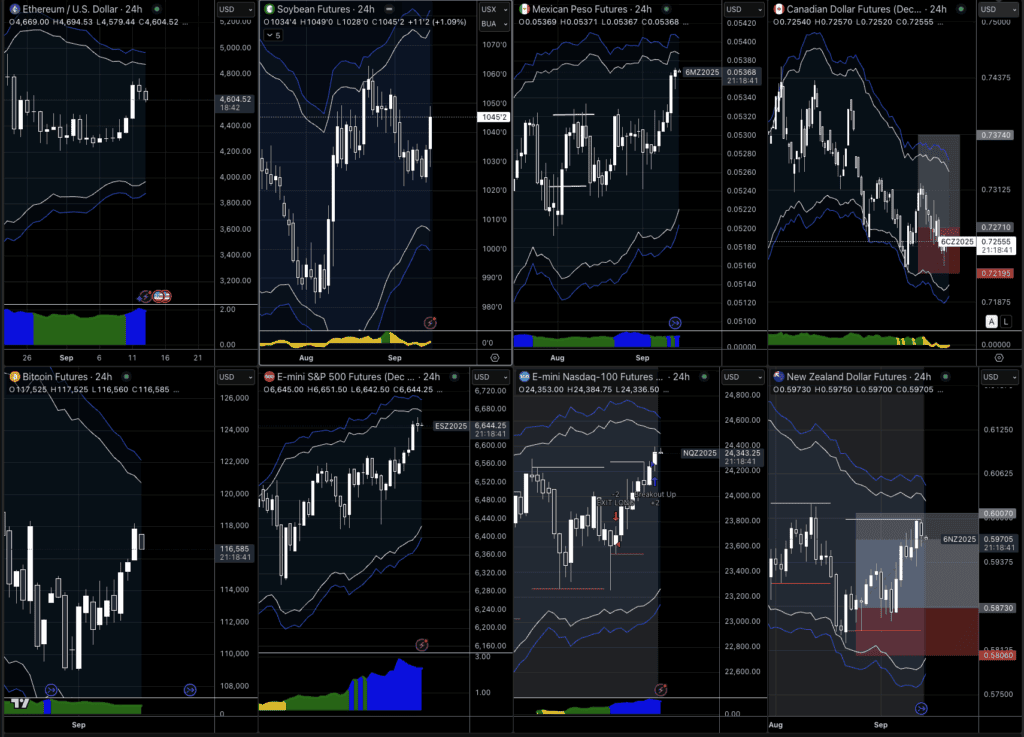

Chart I’m looking at —

Semiconductors (SMH) serve as a good barometer for the economy and as a leading indicator of risk sentiment for the overall market. Where semis go, the rest of the market tends to follow.

That’s why this chart should make you concerned.

I’m still long-term bullish on the US market but I don’t think the most recent round of volatility is over. The market will probably make new lows soon. This is primarily being driven by the recent jump in interest rates. More market vol is needed to settle the long end before this market can bottom and resume its trend to new highs.

Book I’m reading —

This past week I moved out of my cabin in the woods of Virginia and drove for three days across country to my new home, Austin, Texas. I was able to crank out a bunch of audiobooks on the drive and one of these that I enjoyed was Extreme Ownership by Jocko Willink and Leif Babin. Jocko and Leif were Team guys and share the leadership lessons they and other Seals learned from their time spent in combat. I served in Ramadi and worked with many of their teammates and always came away impressed with these guys.

The book is worth a listen (I actually recommend the audio over the written version since the authors read it themselves which helps add more weight to the stories they tell). It has some great life lessons and you’ll come away with some new ideas about what it means to be a leader. Here’s an excerpt.

The test is not a complex one: when the alarm goes off, do you get up out of bed, or do you lie there in comfort and fall back to sleep? If you have the discipline to get out of bed, you win—you pass the test. If you are mentally weak for that moment and you let that weakness keep you in bed, you fail. Though it seems small, that weakness translates to more significant decisions. But if you exercise discipline, that too translates to more substantial elements of your life.

Also, for you sci-fi fans, I listened to a fun audiobook titled We Are Legion [We Are Bob]. It’s the first in a trilogy (I just started the second book) and it’s an original and easy read (or listen).

Trade I’m considering —

Tencent (TCEHY) is trading at its most oversold levels, ever. I think we’re due for some ‘positive’ narrative surprises for EM and China stocks in particular. Tencent should benefit from this. I’m considering going long for a swing trade (ie, 1-2 months) once this recent bout of volatility completes. We’ll see, though… it really depends on what the dollar is doing; and yields.

Quote I’m pondering —

I kind of like uncertainty to some extent, because it’s a little bit of suspense and excitement and adventure… And you can learn a lot even if things don’t work out. But not everyone likes adventure. A lot of people seem to be against uncertainty, actually. In all areas of life. ~ Paul Buchheit

Markets are endlessly complex… learn to embrace uncertainty and become comfortable operating in various shades of grey or suffer at the foot of false certainty.

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.