Markets work to surprise the majority of people, the majority of the time. This is because the average of everybody’s expectations is already embedded in price.

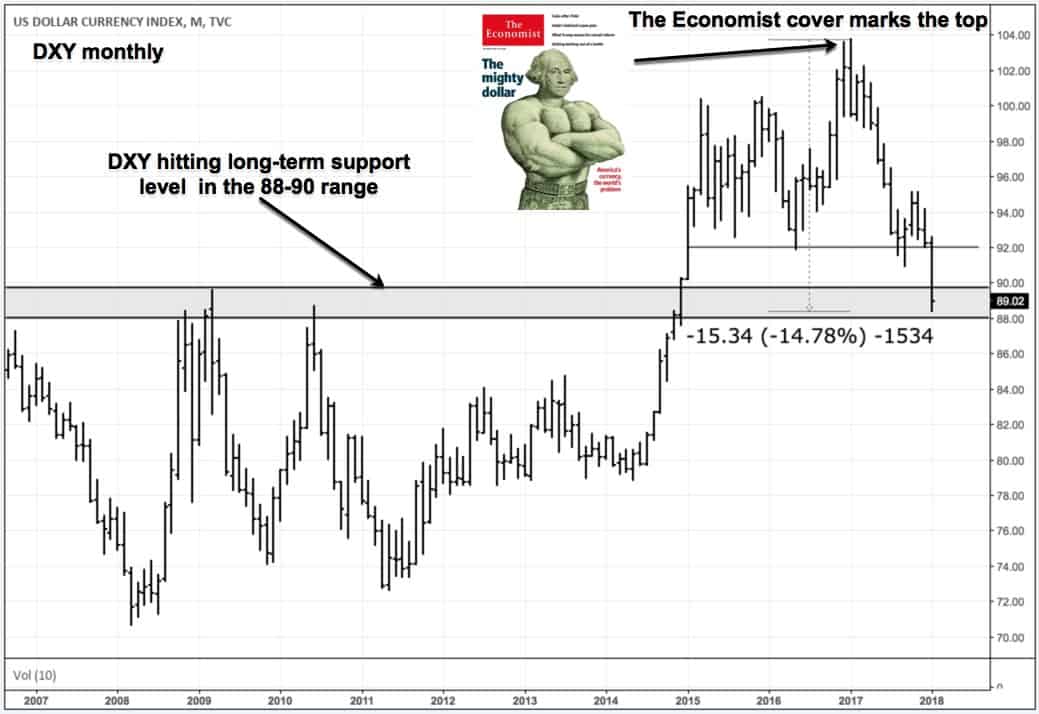

Nowhere is this more true, than in the currency markets. Consensus is the ultimate killer of currency trends. The chart above is a perfect example of this, where The Economist magazine cover marked the top of the US dollar bull market at the end of 2016.

The dollar has since fallen 15%. A move that hardly anybody was expecting.

This is why, when analyzing currencies, we need to adopt Percival’s rule of thumb and know “that expectations will be confounded.”

We often refer to the US dollar as the lynchpin of global markets. This is because global trade is done in dollars, commodities are priced in dollars, and the greenback is the world’s reserve currency and largest source of global funding… The path of the dollar affects nearly every other asset in some way, shape, or form. And if you can get a good handle on the dollar then you’ll have a good grasp on where commodities, emerging markets, and global liquidity are headed.

To start, here are the primary models I use to think about currencies in order to understand the driving narrative (currency markets are narrative driven) and supporting fundamentals.

- The Core-Periphery model: This model was used extensively by George Soros in his currency operations back in the day and discussed at length by economist Javier Gonzalez in his book How To Make Money With Global Macro. In this model, the US is the core and emerging economies are the periphery with other developed markets sitting in the middle. Long-term capital flows tend to cycle back and forth between concentration in the core, to strong flows to the periphery. The primary fundamentals of this model are relative growth numbers between the regions (ie, relative GDP growth and relative equity and bond market returns). When global growth is strong and broad based, risk is perceived as low, so capital flows out from the core to the periphery. The opposite holds true for when risks are perceived as being high. Put simply, capital flows to where it’s believed it’ll be treated best (ie, earn the highest stable total return relative to perceived risk). The US, along with other DMs, receives a premium over the periphery.

- Sentiment/Positioning: Like we discussed above, we want to operate off the rule of thumb that “expectations will be confounded”. So we always want to know what the popular sentiment is and how the market is positioned. To do this, we can look at anecdotal evidence such as magazine covers, news articles, and fintwit talk to get a feel for what narratives/belief are popular. And for positioning, we can look at the COT data and sentiment/positioning surveys like the BofA Fund Manager survey to see how investors are positioned.

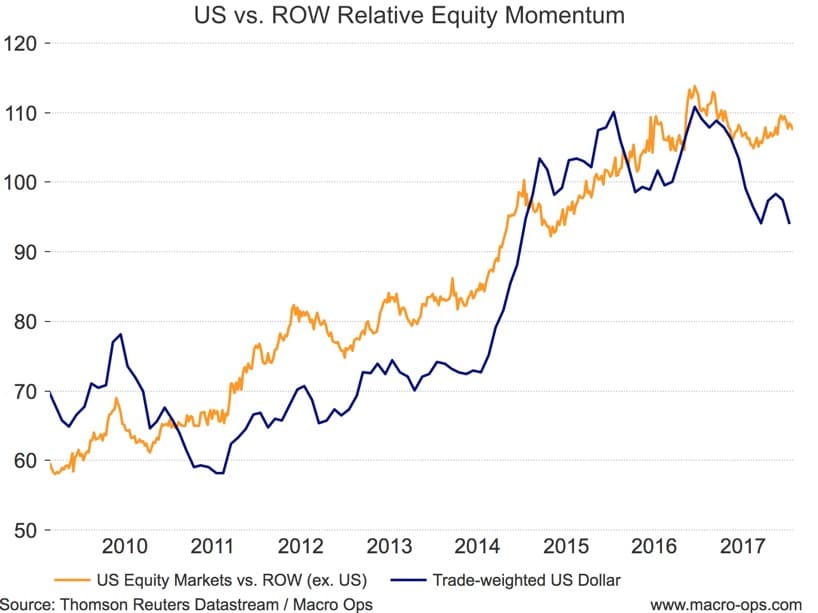

- Trend and Total Return: Once a currency gets going it has a tendency to persist for long periods of time. This is because currency flows are largely speculative, meaning they chase market returns around the world. And when capital flows into a country where the equity/bond market is outperforming on a relative basis, these flows then strengthen the underlying currency. Now you have an outperforming equity/bond market + a strengthening local currency (lowering local inflation and boosting real returns). This ups the total return for foreign investors, thus attracting more flows and creating a positive feedback loop. So when analyzing currencies we always need to look at relative market performance, because currency pairs tend to track relative stock/bond market performance over time.

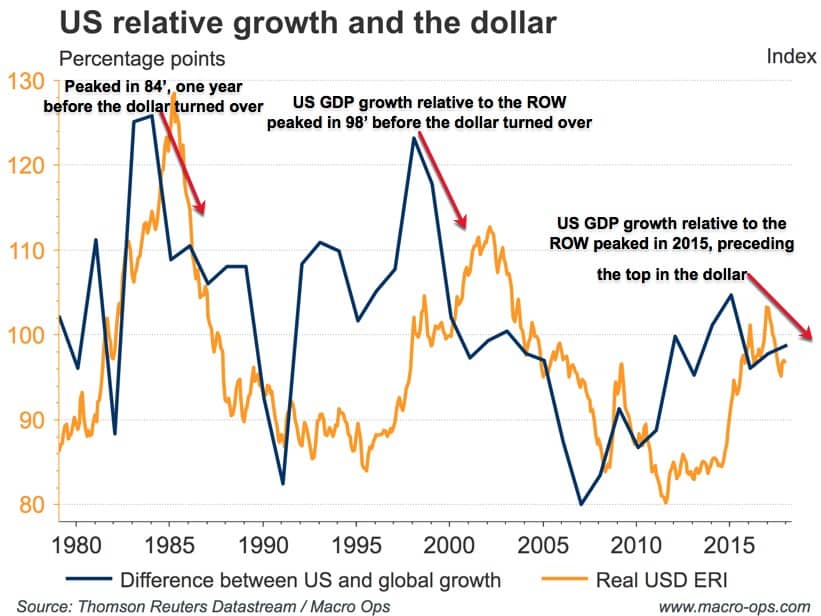

To begin our analysis of the dollar, let’s take a look at relative GDP growth between the US (the core) and the rest of the world (periphery). Relative gdp growth is important because growth affects everything from investor behavior, inflation and interest rate expectations, and perceptions of risk.

The chart below clearly shows the relationship between US GDP growth relative to the rest-of-the-world (ROW) and the subsequent trend direction in the dollar.

When growth in the core outpaces growth in the periphery (as it did from 09’-16’), capital concentrates in the core and drives the US dollar higher. When growth in the periphery outpaces the core, capital flows outwards leading to a lower dollar.

It’s important to note that it’s the trend in this relative growth that matters. Growth in the core (US) is almost always lower than that of high growth emerging markets. But US growth gets a premium over EMs. Which is why it’s the trend in relative growth and not the absolute levels that are important.

In mid 2016, beaten down equities in the ROW began outperforming the US. While at the same time, US relative GDP growth turned lower, and both sentiment and positioning reached extreme long consensus in the dollar. This led to the top in the dollar bull market.

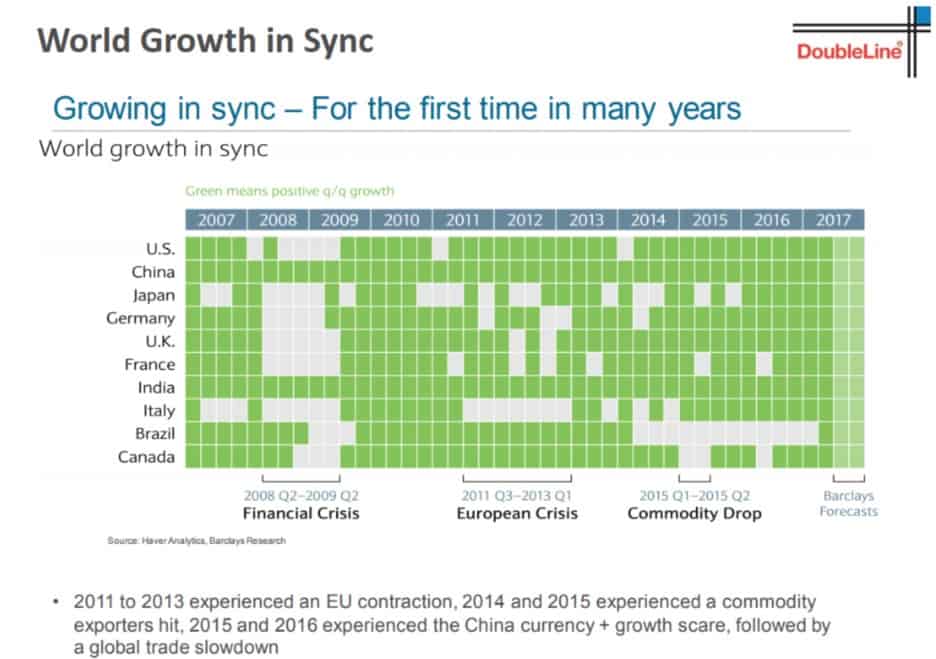

Currently, we find ourselves with conditions that are the opposite of those that created the dollar bull market.

Instead of narrow and tepid growth, we have a global economy that’s firing on all cylinders and seeing complete synchronized growth across the board (chart via DoubleLine).

To adhere to Occam’s razor then, it’s fair to assume that the dollar is falling because we’re in the goldilocks period of the market cycle where growth is strong and risk is perceived to be low. This is leading to capital flowing out from the core and to the periphery.

The budding narrative is as follows: The horizon looks clear and foreign markets offer better relative value to expensive US stocks and bonds.

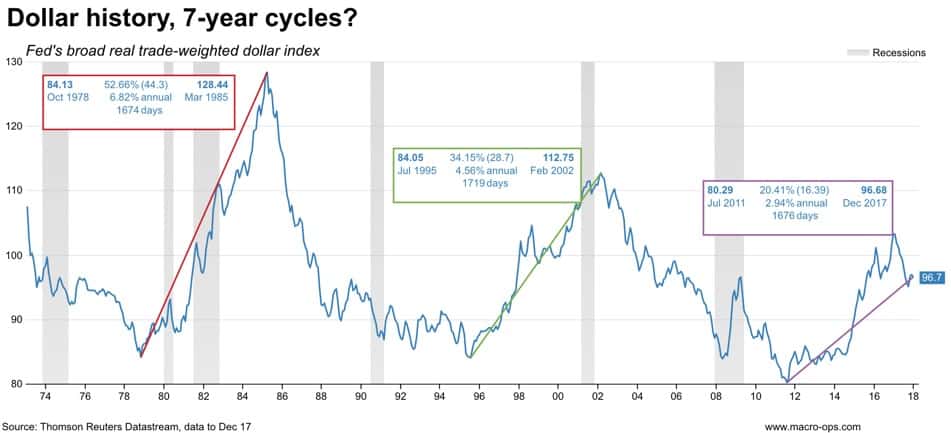

In addition, there’s a lot of capital concentration which accumulated in the core over the last 7-years. This capital is likely to be converted out of dollars and into other currencies over the coming year(s). This will put further downward pressure on the dollar and risk creating a bearish feedback loop.

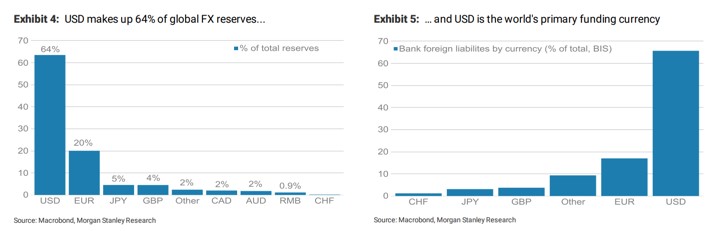

For example, the dollar currently makes up an unnecessarily large percentage (64%) of global foreign reserves, as shown on the chart below via Morgan Stanley.

Hedge fund manager, Ray Dalio, recently noted (emphasis mine):

The dollar’s role as the dominant world currency are anachronisms and large relative to what one would want to hold to be balanced, so rebalancings should be expected over time, especially when U.S. dollar bonds look unattractive and trade tensions with dollar creditors intensify.

Morgan Stanley commented on the vulnerability of the dollar in a note, saying (emphasis mine):

Our key point here is that foreign holdings of USD-denominated debt have increased, while foreign holdings of European debt instruments have declined. A similar dynamic has taken place for equities, where foreign ownership of US equities has more than doubled, which contrasts with trends in the foreign ownership of European equities. An important implication is that, should US assets lose their relative attractiveness (e.g., widening credit spreads, declining equities), then there could be a substantial amount of foreign-held USD-denominated assets for sale.

With the US deficit set to widen because of the recent tax cuts and expected increases in fiscal spending (coming infrastructure plan), we’re set to see a rise in the supply of USD assets at a time when investors are moving their capital out of dollars and into other markets.

That’s not the kind of backdrop that’s supportive of a stronger dollar.

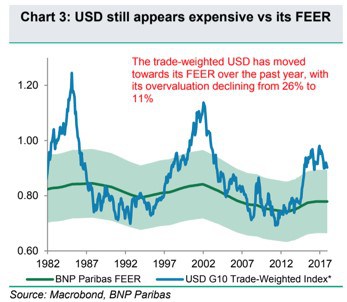

On top of this, no matter which means of valuation you use, the dollar is overvalued, especially against emerging market currencies.

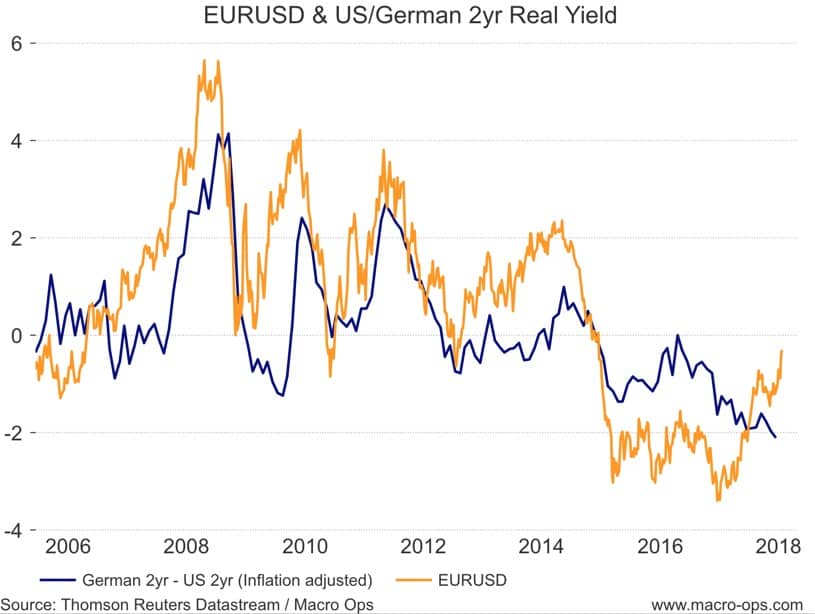

When looking at the dollar, we have to include the euro. The EURUSD pair makes up well over half of the trade-weighted dollar basket, so it has a large influence on where DXY goes.

You can see on the chart below that the euro has completely retraced the breakdown from its previous multi-year trading range. If price holds this month, it would mean that this was a major multi-year bear trap.

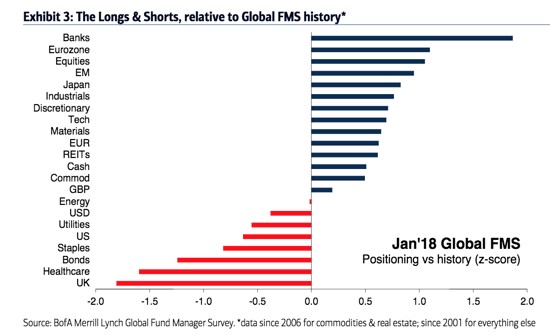

Sentiment and positioning in the euro and European assets have ticked up, as shown in the chart below via the BofA FMS.

Spec COT positioning is stretched and is now a headwind over the near-term.

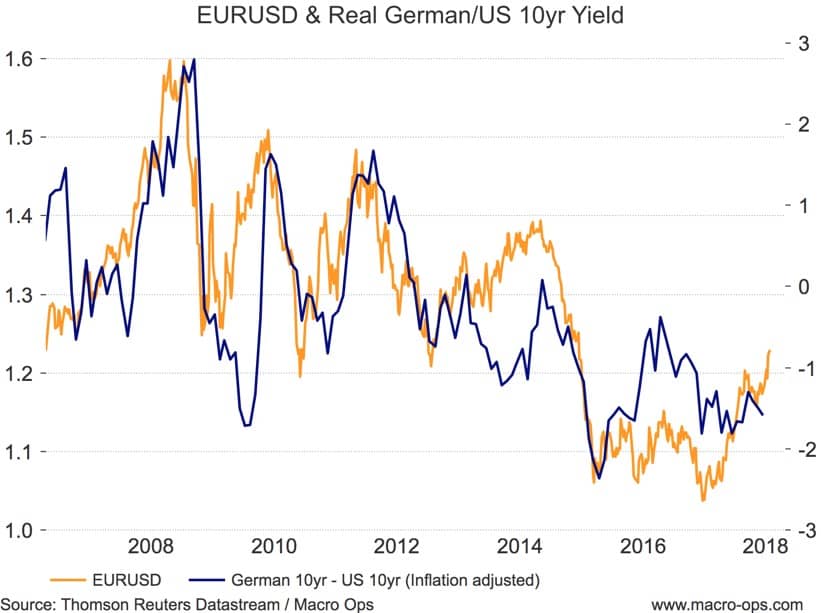

The real yield differential between the US and Europe hasn’t supported the move up in the euro. But the market is driving the EURUSD pair higher on the expectations that European rates have more room to move up from current levels, than US rates do.

In fact, the dollar is currently a top-4 yielder out of the G10 (chart below via DB).

While yield differentials are important, currencies can move against logical yield relationships for long periods of time. And it’s the expectations over future yield differentials that tend to matter more than the current spreads.

The most important chart for the dollar in my opinion is this one. The S&P versus emerging markets. Even with US stocks going on an endless tear, EMs are performing even better.

If EM outperformance continues, it’s going to attract more capital flows which will help to drive the dollar lower.

A falling dollar creates a number of positive tailwinds for EMs besides raising foreign investor’s total returns.

It leads to higher commodity prices, which benefits commodity producing countries. And it leads to lower funding costs (many EM corporates and countries borrow in USD, so a lower dollar equates to lower debt costs).

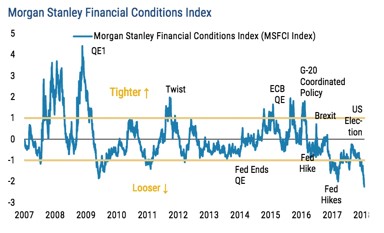

With liquidity as loose as it is today, there’s little on the near-term horizon that could significantly reverse these dollar bearish flows outside of a major shock that raises investor’s perceptions of risk. Sentiment and positioning is now bearish the dollar but far from extreme levels that tend to mark significant reversal points.

I don’t expect the dollar to continue falling straight down. Many DM-USD pairs appear to be stretched over the short term and are nearing significant resistance levels. So we’re likely to see a pullback soon. But as traders we have to respect the tape and acknowledge the possibility that the dollar bull market which started in 11’ is now over.

If this is the case, it will have big implications for markets moving forward.

If you want to stay up to date with our latest US dollar coverage then check out our Macro Intelligence Report (MIR) here.