Summary: Sentiment and positioning continue to slowly reset, though we’re still well above washout-level readings. Energy and rates are pressuring the broader indices, which look set to open the week with some downside volatility. Our models remain cautious — more downside ahead — but the primary bull trend is still intact. This is a correction, not a top. Inside: our Energy & Credit Shock indicator, AI’s real impact on labor markets, why inflation volatility matters more than its level, a bullish setup across the Ag space, and more.

A quick note before we dive in. We’re opening enrollment to the Collective this week — and we’re raising prices soon. Not as a gimmick. We’re keeping the community at a size where it actually works. If you’ve been on the fence, it’s time to jump!

MO Portfolio & Trades

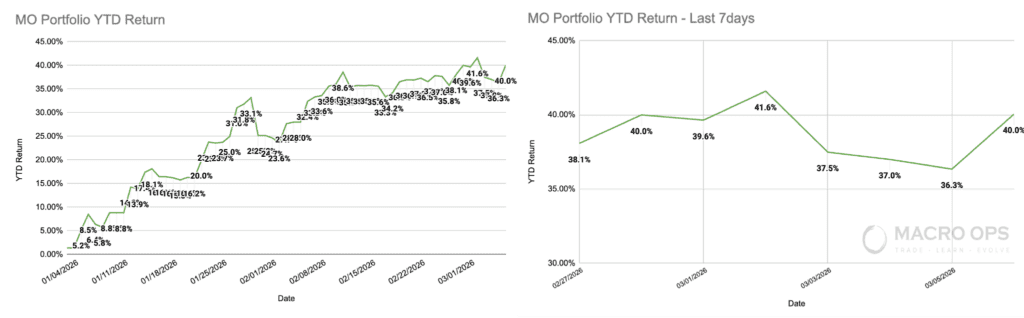

1. The MO portfolio gained +40bps on the week — though that number flatters the experience. We climbed to +41.6% on Tuesday, gave back to +36.3% by Thursday, and settled back at +40% YTD. Plenty of vol in between.

We cut the entire equity book last week. Waiting for clarity, starting fresh. Current positions: long oil futures and calls, long BBG commodity index, long KC HRW Wheat, short T-Bonds, short NQ futures.

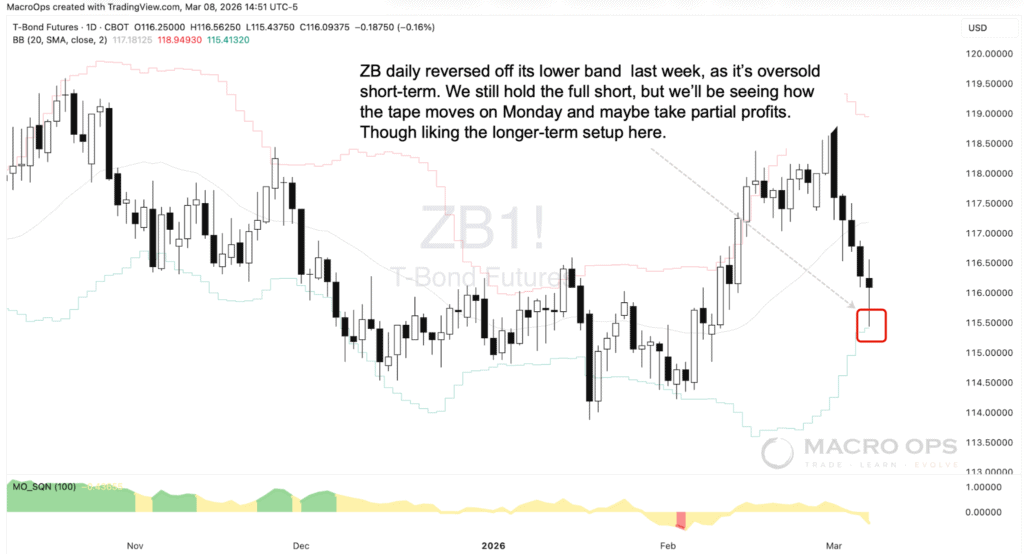

2. Last week we highlighted two Treasury trades — a bullish breakout in the front end and a short setup in the long end. The 2s were a bull trap; we stopped out. Still tracking it closely though, as it remains in a major compression regime. The short in the long end has played out well. It’s short-term oversold and sitting at its lower daily band. We’ll assess on Monday whether to take partials or let it run.

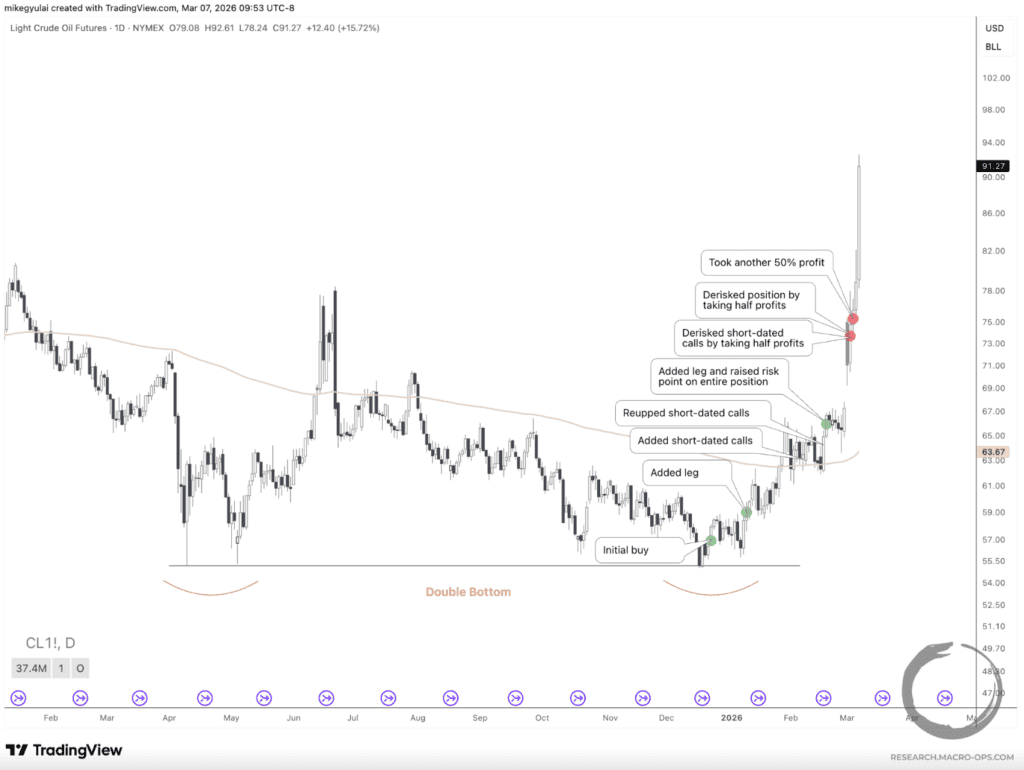

3. Our Lead Technical Analyst Mike Gyulai published a sharp note over the weekend covering the evolution of our long oil trade, among other things worth your time. [Read it here.] We’ve taken partials and continue to trail stops — but we’re still long futures and calls.

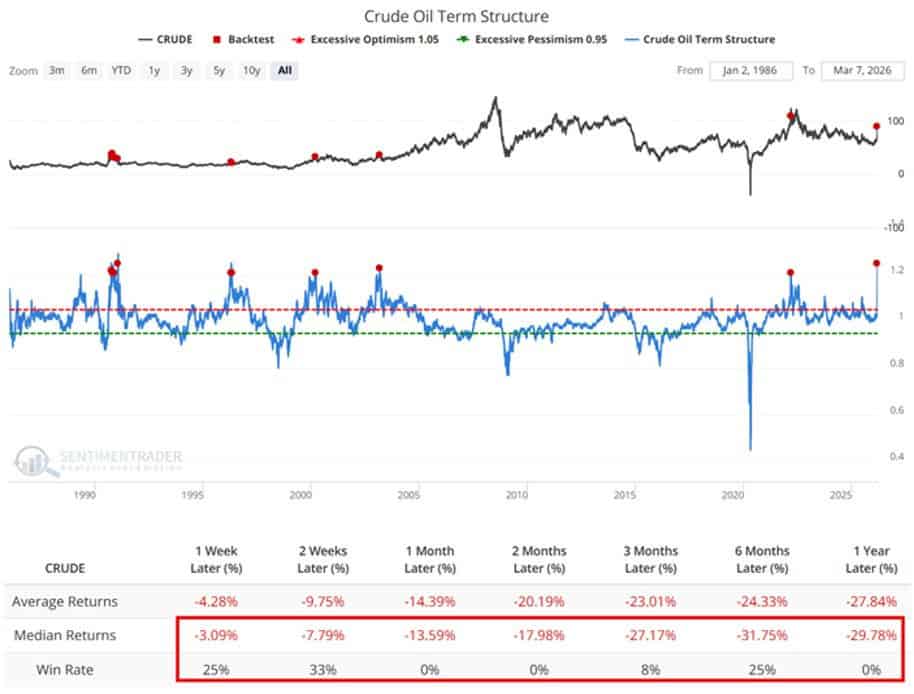

4. WTI is in extreme backwardation. Historically, that’s a signature you see at or near oil tops and it tends to bode poorly for forward returns. That said, we’re operating in an unusual, event-driven environment — basic historical comparisons need a helping of salt here (chart via @jaykaeppel).

We’ll be watching to see whether long-dated futures catch up to the front end (bullish) or if the front end catches down (bearish).

Trifecta Charts

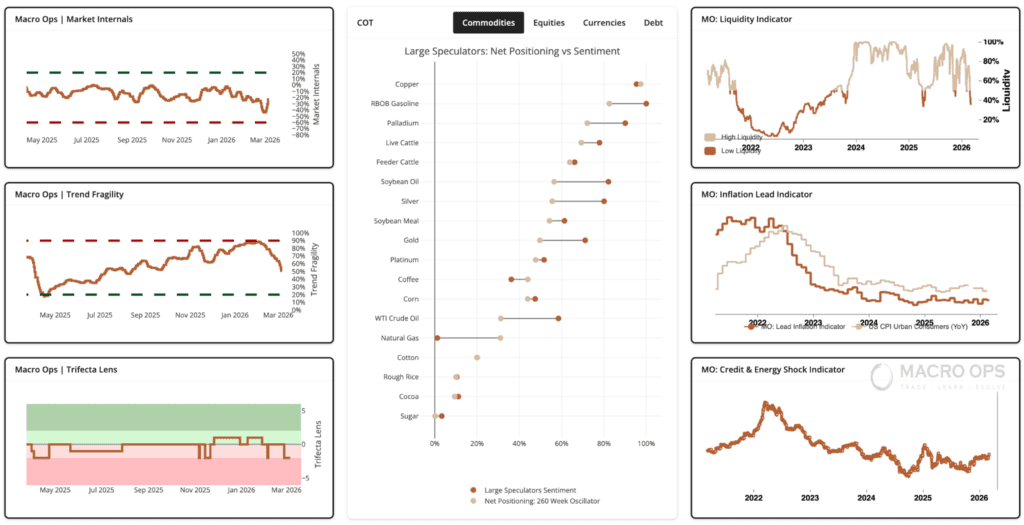

5. Some notable action in our core models last week, working counterclockwise from the top left:

Aggregate Market Internals saw a big jump WoW — still at a weak level though, but worth watching. Trend Fragility (our sentiment/positioning composite) dropped to 51% — a buy signal triggers on a cross below 20%. Our Trifecta Lens Score fell to -2, a level that historically precedes chop and downside vol in the indices. And our Liquidity Gauge collapsed to 39%, a level that historically points to poor forward 1-3 month returns.

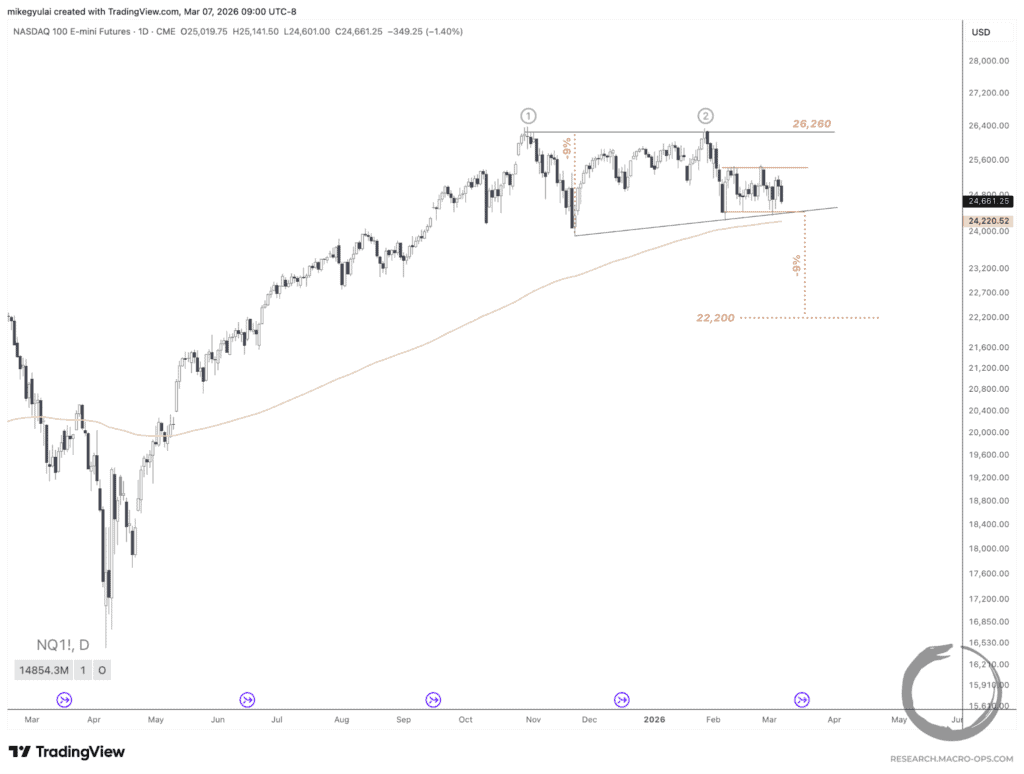

6. Last week, I shared the double-channel chart on ES-mini, suggesting a likely breakdown from its 2-month sideways range and a selloff toward November lows before a proper washout bottom. Mike G echoed this with NQ — a break below recent congestion gives it a measured-move target of -9%, or roughly 2,200.

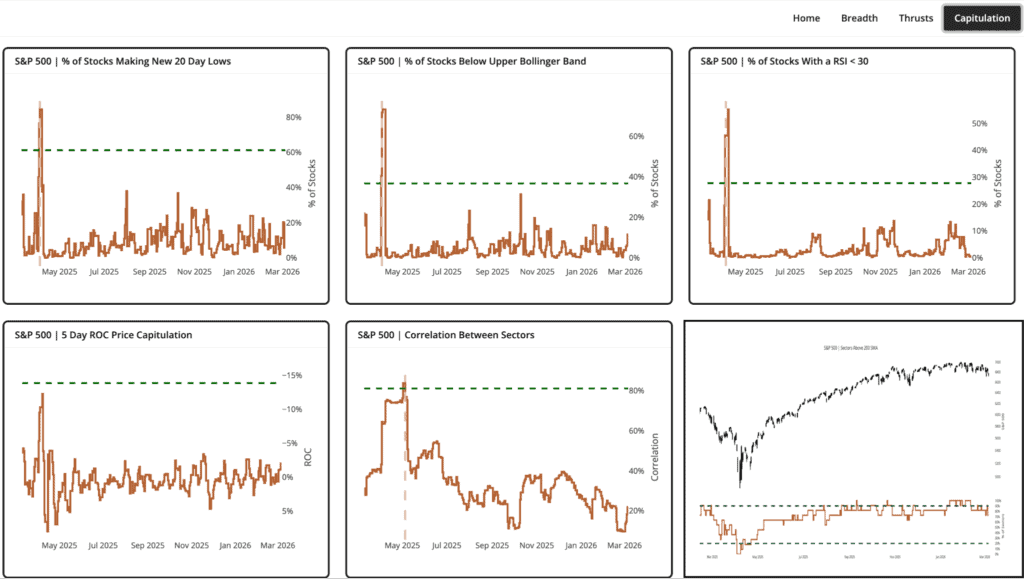

7. Our base case is not a cyclical top. The primary trend models remain supportive. That said, I think a larger extended sideways range — 6 months or more, volatile — is a real possibility. Either way, we’ll be tracking the Capitulation tab in our HUD to help identify a bottom.

Macro

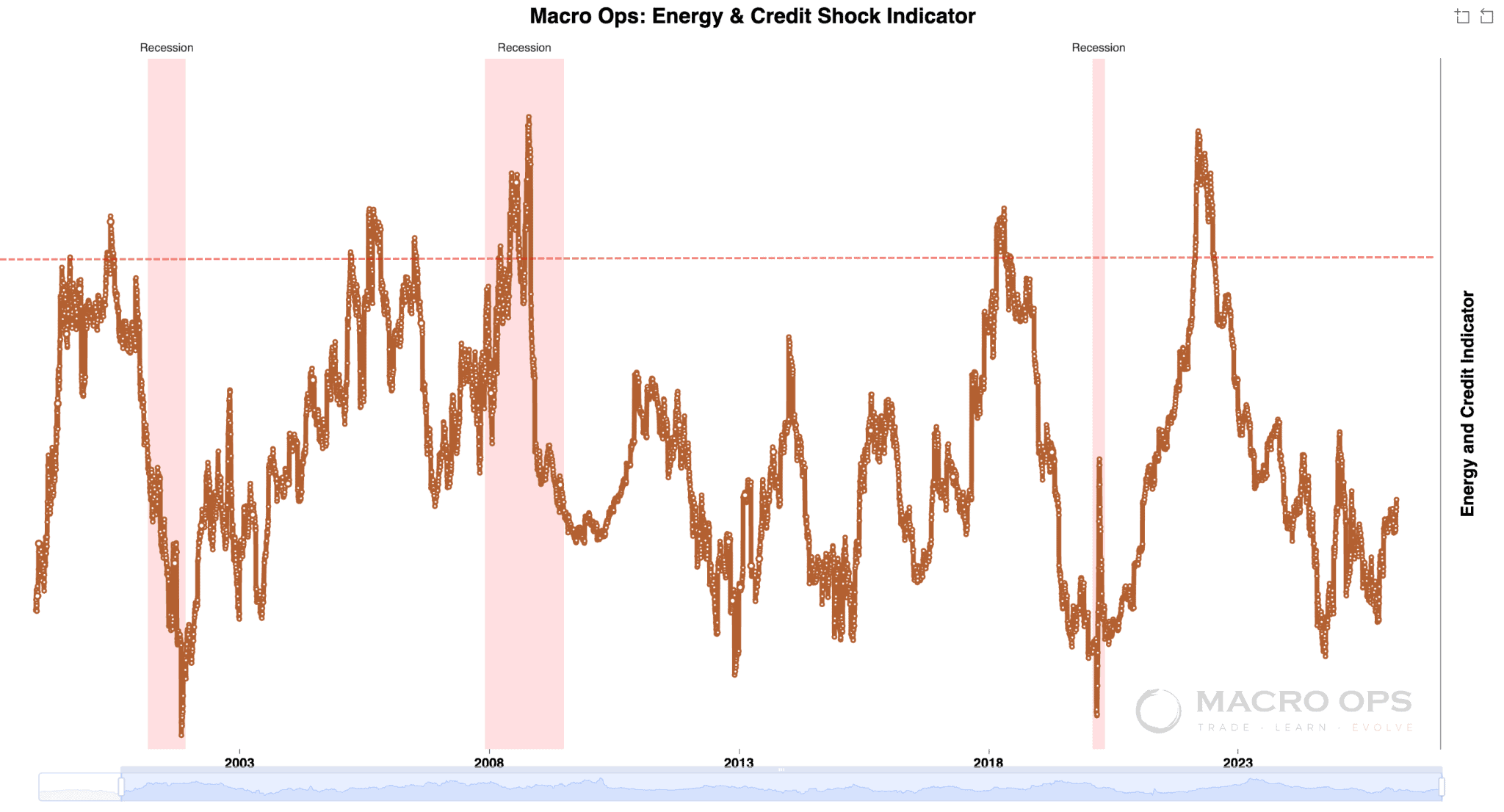

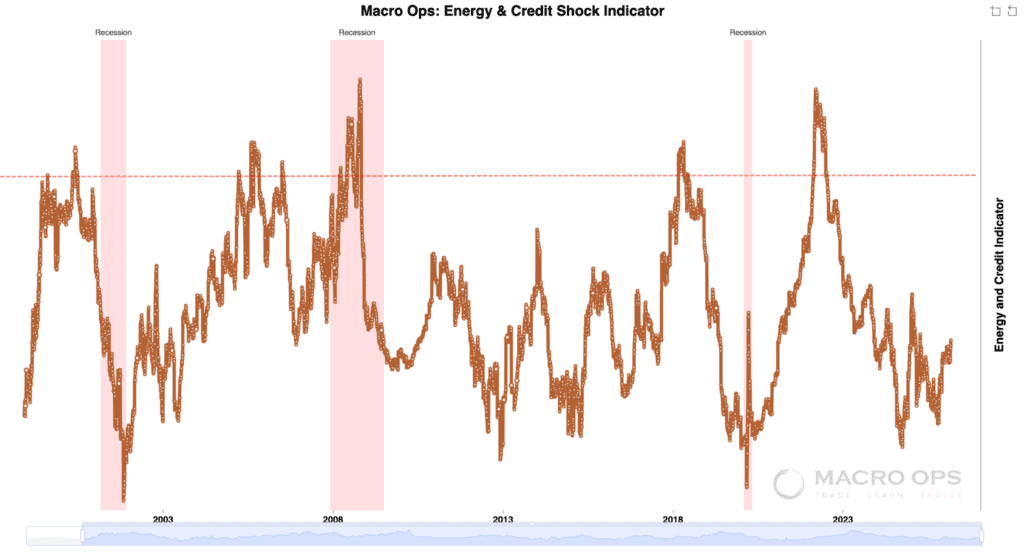

8. PTJ once said every recession since 1970 has been preceded by a 100% YoY rise in the price of oil. Sans COVID, he’s right. Our Energy & Credit Shock Indicator illustrates this cleanly. We’re fine right now — but this thing can move fast.

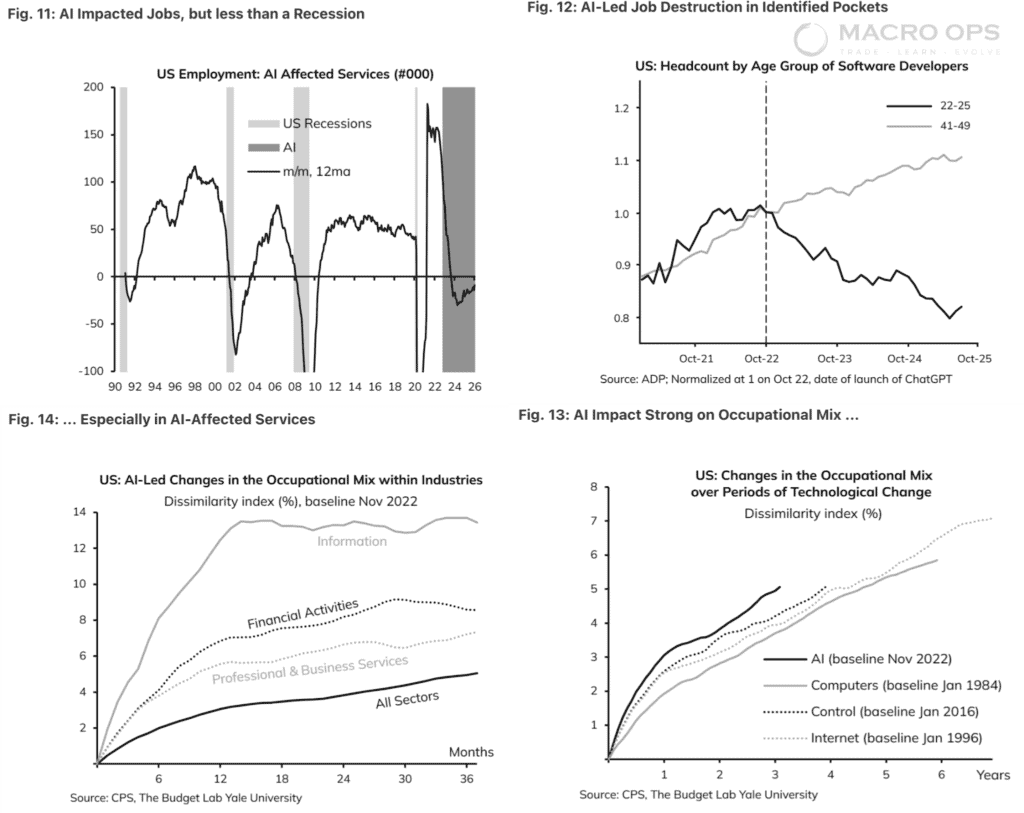

9. LB Macro put out a great post this week on AI’s economic impact so far. Their take: AI isn’t destroying the labor market — at least not yet. What it’s actually doing is something subtler and probably more consequential: reshaping it faster than any prior technology wave. Entry-level cognitive jobs are getting hit. The composition of employment is shifting at a pace that dwarfs previous tech cycles. The destruction is contained for now, but the reallocation is very much underway.

10. I mostly agree — for now. But we have to maintain real cognitive flexibility here. This isn’t a normal environment, and AI is not your average technological revolution. Charts like the one from JPM below need to be watched and respected. Don’t get complacent.

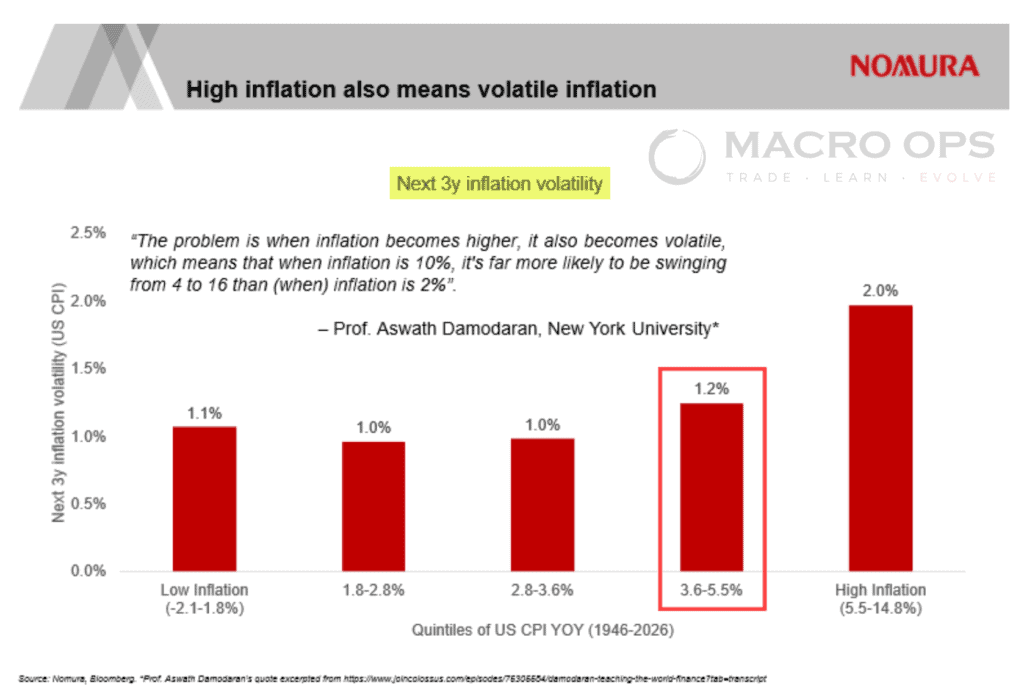

11. Research has shown it’s not the level of inflation that hurts risk assets — it’s the volatility of inflation. This chart from Nomura is a useful reminder: when inflation runs hot, it also tends to run wild.

Trade Setups / Topical Charts

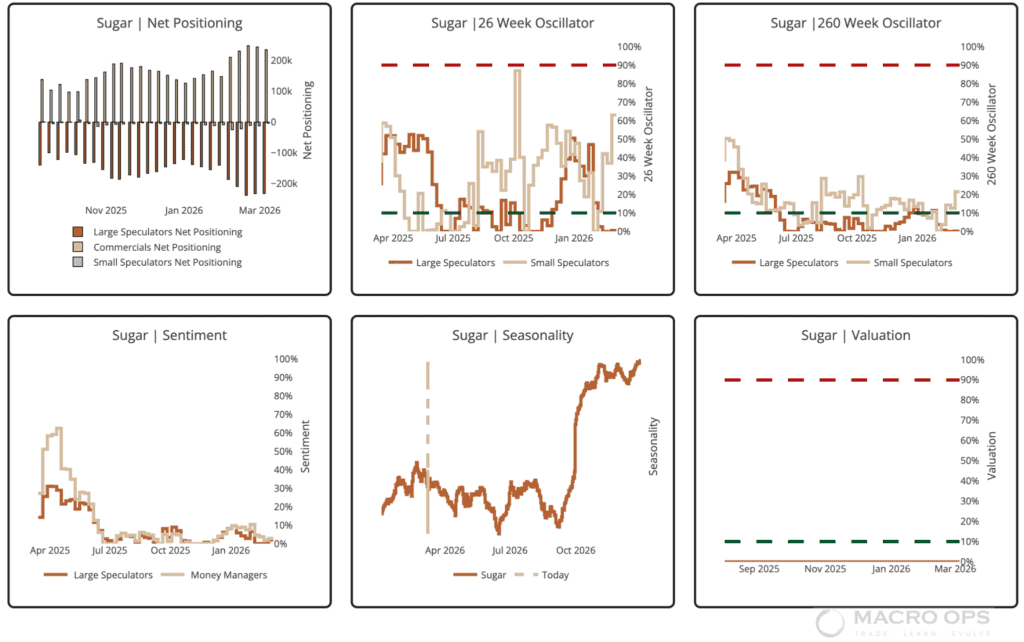

12. We’re in a cyclical commodity bull, and it’s following the standard playbook to a T: Precious Metals → Industrial Metals → Energy → Agriculture. We’re long Kansas City Hard Wheat, missed an entry on corn last week, and are now tracking a setup in Sugar.

Speculator short positioning recently hit its most bearish reading on record. Our sentiment indicators are sitting at the 0th percentile. Relative valuation is nailed to the floor.

13. I’ve been patient with Sugar — watching the one-sided positioning, waiting for a technical setup and some news failures to confirm. Now we have both.

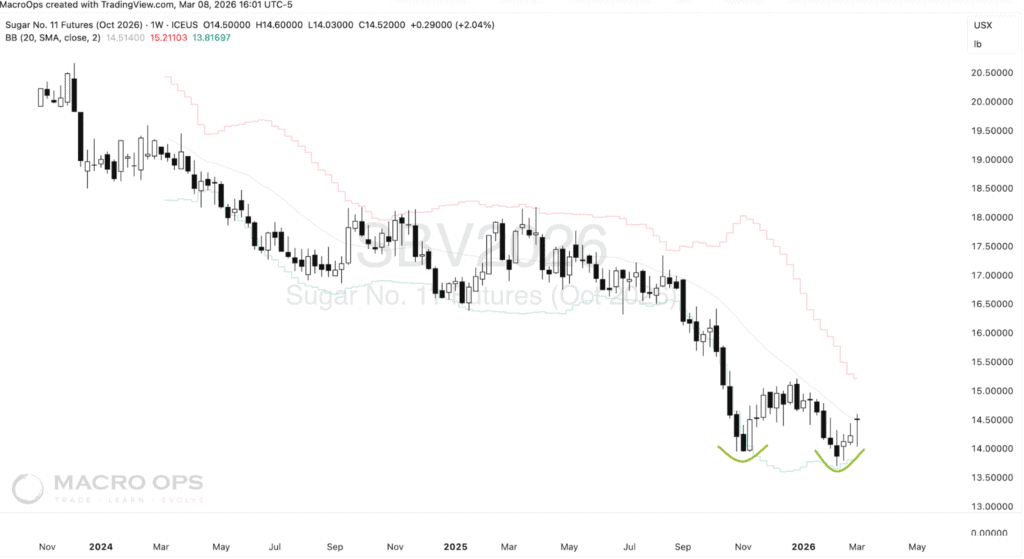

The October chart shows a double bottom on both weekly and daily timeframes. We’ve had a series of bearish news failures over the past week. And Sugar is heavily influenced by ethanol prices, which jumped last week. We’re looking to get long this week.

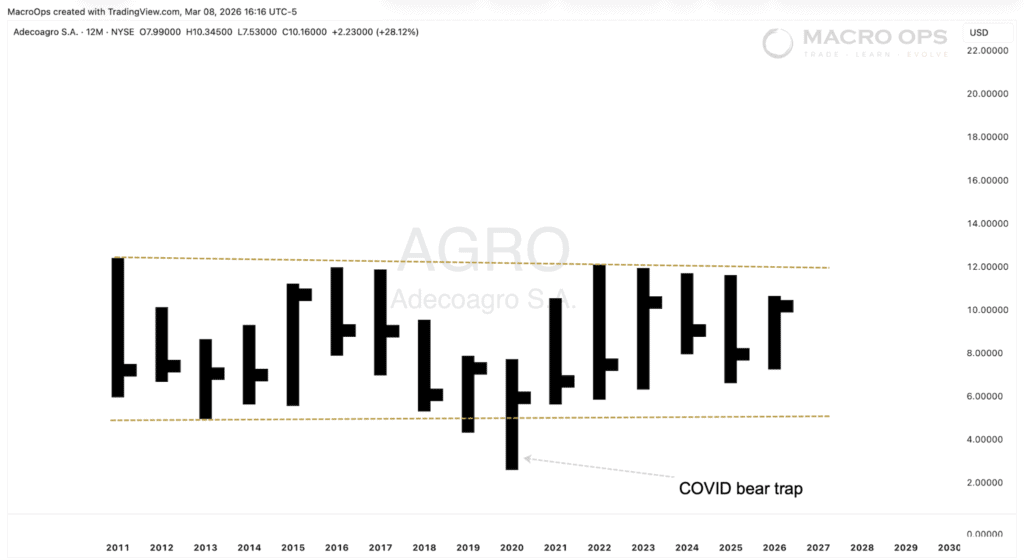

14. On the equity side, Adecoagro (AGRO) surfaced as an interesting way to play this. They operate primarily in Argentina and Brazil — low-cost producer of sugar and ethanol, with significant corn and soybean exposure. Highly sensitive to the No. 11 sugar contract. The stock has traded in an $8 sideways channel for its entire life as a public company. It jumped last week. No trade yet — but I’d be interested on a clean breakout above $11.50.

One more thing before you go.

The Collective is where we do the real work — live portfolio, full model access, the HUD, Mike G’s technical notes, Brandon’s deep value dives, my macro takes, a dashboard of our proprietary tools, and a community of serious investors and traders who are actually devoted to getting better. It’s not cheap, and it’s about to get less cheap. We’re raising prices to keep the community at a size where everyone gets real value out of it. If this resonates with you, now’s the time.

Thanks for reading.