It’s that time of the year when we review our Q1 2025 performance: the good, bad, and ugly.

Here are the raw Q1 performance data:

- January: +2.42%

- February: -1.23%

- March: +12.68%

- Q1 2025: +13.87%

The S&P 500 returned -4.59% during the same period.

But before we dive into the review, I want to pitch our Macro Ops Collective.

The Collective is the most unique group of traders, investors, and entrepreneurs on the Internet. Our central goal is to become consistently profitable in any market regime while having a ton of fun.

The MO portfolio officially closed the year with a +50.4% return. We’ll soon publish our year-end review, which will discuss our painful mistakes and total blunders, what we’ve learned, and what we’ll try to do better in the year ahead. So keep an eye out for that.

If you’d like to join our Collective as we tackle 2025 head-on, click here.

Let’s get after it.

If you look at the quarter-end returns, you’d probably think it was an “easy” quarter. We held a few core names, didn’t trade much, and sat on our hands. Where’s the drama?

But underneath the decent performance are tons of worries, psychological hurdles, and a constant, nagging fear that I need to trade.

I’ll dive deeper into these themes, but first, let’s review our quarter’s best equity performers. We’ll cover our futures positions in Part 2.

Three Stocks Drove Q1 Returns

As I mentioned earlier, we didn’t trade much during the quarter. We held a few core equity positions and added to our core group of futures and forex trades. Three equity positions drove our Q1 returns (with average portfolio weighting):

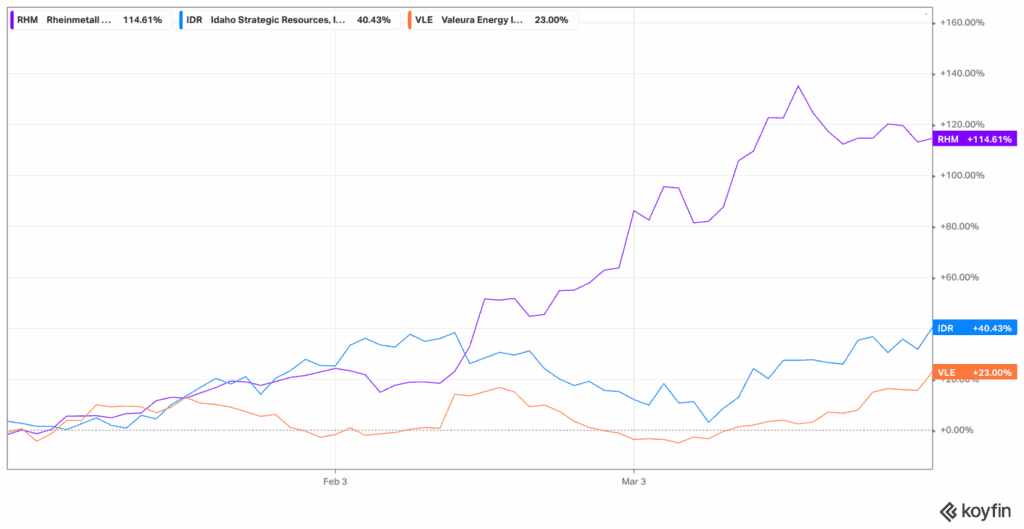

- Rheinmetall AG (RHM.AG): 8.92%

- Idaho Strategic (IDR): 3.68%

- Valeura Energy (VLE.TO): 8.95%

These three positions represented 22% of our net asset value (NAV). RHM was our most significant winner, returning 114.61% during the quarter. IDR returned 40.43%, and VLE returned 23%, respectively (see below).

Rheinmetall AG (RHM.AG)

We first bought RHM in January. My thesis at the time was (emphasis mine):

“Trump will demand Germany/EU to spend more on their defense and military (i.e., rely less on the US) and that RHM is the best-positioned company to meet that future demand.

Here’s a simple way to frame it: In 2024, Europe spent ~2% of GDP on national defense. Trump wants them to spend at least 3%. A 1% increase would result in an additional EUR 100B in annual spending until 2028 (see the graph below from RHM Investor Day).”

I outlined four reasons why I preferred RHM as the way to play this thesis:

- They’re the largest defense company in Germany and the fifth-largest in Europe.

- They’re quickly creating one of the largest military vehicle fleets globally.

- They were one of the leading defense partners for Ukraine.

- They have one of the most badass CEOs in the game (Russia/KGB tried to assassinate him at one point)

There’s a lesson here: If Russia/KGB tries to assassinate your company’s CEO, you just buy the stock. Those are the rules. Assassination attempts are worth at least 3-5x EBITDA.

In February, I wrote that:

“RHM’s operating profits should reach around EUR 3.6 billion by 2027, with EUR 1.4B in free cash flow. This puts the current valuation around 11x 2027 operating profits and 27x free cash flow.

It’s still not expensive, but it’s not obviously cheap. That is the sweet spot for some of the best-performing stocks. It’s the Trifecta Lens philosophy in action.

Take Eli Lilly (LLY), for example.

The stock never looked “cheap” – but it didn’t matter. It had (arguably) the strongest secular tailwind you could imagine: Lots of people are fat, LLY makes a drug to make people less fat without any effort, and people will pay whatever price to get less fat without any effort.”

RHM is more expensive today than when I wrote about it in February. We took partial profits in early April (mainly as part of our broader portfolio risk management rules), but still hold a ~6-7% notional position.

The stock trades at ~50x next year’s earnings, so there’s plenty of room to disappoint. But, if we’ve learned anything from Eli Lilly (LLY), it’s that these big secular themes can go longer than we can stay sane. European defense spending should only increase from here. There are even discussions about EU countries expanding their deficits to allocate more funds for defense.

We’ll gladly hold the rest of our position while the trend continues, but won’t hesitate to cut if the trend reverses.

Idaho Strategic (IDR)

I’ve written so much about IDR that I’m afraid it’s becoming my “Sacred Cow.” But that’s why I write these reviews – so you can hold me accountable. No stock is too sacred to sell.

Anyways, IDR returned 40.43% during the quarter, beating both the S&P 500 and the underlying gold commodity (see below).

If you haven’t yet, I encourage you to read my four latest IDR write-ups:

- IDR 2024 Earnings Recap

- Valuing IDR’s Rare Earth Assets

- Valuing IDR’s Gold Assets

- Knowing What You Own: Idaho Strategic (IDR)

The big idea is that IDR has increased significantly since we first started buying – but it’s still massively mispriced against its REE package, gold assets, and future production.

The company has the four most essential assets in mining in spades:

- Exceptional management team

- Tier-1 jurisdiction

- Fortress balance sheet

- Long runway for organic production growth

IDR’s REE asset could be worth its entire market cap, and they have a pathway towards 60,000oz in annual production. They have a waiting list of people who want to work for them and enough treasury notes to cover total liabilities twice over. You get all of this for ~$250M.

I spent a lot of time looking for new gold producers to add to our book. But none of them met IDR’s standards. And that’s a good thing. It means we’ve found a winner that we should add over time.

The stock briefly reached new all-time highs around $19.70/share before retreating to its current price of $16.65/share. I expect IDR to pull back as it digests its run before breaking above $20/share.

We haven’t sold a share this year, and the stock accounts for approximately 12% of NAV. But as always, can instantly change our minds and exit the entire position in a full risk-off environment.

Valeura Energy (VLE)

Valeura Energy (VLE.TO) is a $550M market cap Canadian oil producer with four producing assets in Thailand.

The company has $259M in cash and no debt. It recently reorganized its operations to unlock $400M in tax losses. At the historic 50% tax rate, the tax losses represent ~$200M in incremental cash flow.

Insiders own ~19% of the company, and VLE recently announced an NCIB to repurchase 7.4M shares (6.5% of the total).

VLE outperformed the S&P 500 and Crude Oil during the quarter (see below).

Then oil crashed 20%+ in the first few weeks of April. So, we took profits in VLE and are happy to sit on the sidelines, monitoring oil’s price action before re-entering.

This is one of those instances where we still love the business, management team, and valuation, but sold to protect capital and reduce portfolio risk. I like saying, “It’s nothing personal, just risk management.” Remember – no sacred cows.

Does the company make money at $60/bbl oil? Sure. But that won’t stop the algos and momentum traders from selling it into oblivion. And if you know that, or have a feeling that will happen, why hold if you can put money to work elsewhere? You can always get back in.

Doing Nothing Is The Hardest Thing To Do

Four years ago, I wrote an essay called Boredom: An Investor’s Last Remaining Edge. My big idea was that (from the article):

“People say they want to make money in the stock market. But in reality, it’s far more complicated. Humans crave action.

Whether it’s running from a big cat in the African Sahara or buying that hot new stock your gym buddy can’t stop mentioning. In our brains: action = good, inaction = bad.

So much so that we’d rather harm ourselves than sit alone with our thoughts.”

Read that last part: “We’d rather harm ourselves than sit alone with our thoughts.”

That’s impossible, right? Nope. In 2014, social psychologist Timothy Wilson posed two questions:

- Do people choose to put themselves in default mode by disengaging from the external world?

- When they are in this mode, is it a pleasing experience?

Participants ranged from college students to the elderly (77+). In the first study, the participants did a 6-15 minute “thinking session.” No phones, no external stimulus. Alone with their thoughts.

The first study revealed that 58% of participants found it difficult to concentrate. 89% said their mind wandered during the 6-15 minute session. And ~50% of participants said they didn’t enjoy the experience.

How much do you enjoy doing nothing in your portfolio every day? Do you feel accomplished? Or do you feel lazy, like there’s something you should be doing, but can’t name it?

Anyways, Wilson added a third option: harming yourself. Back to the essay:

“Many participants elected to receive negative stimulation over no stimulation—especially men: 67% of men (12 of 18) gave themselves at least one shock during the thinking period [range = 0 to 4 shocks, mean (M) = 1.47, SD = 1.46, not including one outlier who administered 190 shocks to himself], compared to 25% of women (6 of 24; range = 0 to 9 shocks, M = 1.00, SD = 2.32). Note that these results only include participants who had reported that they would pay to avoid being shocked again.”

I love how Wilson couldn’t even hide his amazement:

“But what is striking is that simply being alone with their thoughts for 15 min was so aversive that it drove many participants to self-administer an electric shock that they had earlier said they would pay to avoid.”

Self-administered electric shocks are just another way of saying, “overtrading.” But I told you that I didn’t trade much during the quarter, so why did I still feel this “electric shock” pain?

There’s a mental shock investors receive when they’re not used to doing nothing. It’s not physical pain, but it affects you just as much. The shocks look like this:

- “There has to be a better stock out there than the worst one in my portfolio, I must find it now.”

- “I haven’t traded in a while and the market is going crazy, I must rebalance or take profits or cut losses.”

- “I haven’t made a new trade in months. Sure the stuff I own is working, but I should be doing something, right? That’s what I’m getting paid to do.”

Maybe your shocks sound different – but they feel the same. It’s the same crippling self-doubt around your process, your stock selection, and portfolio construction that usually creeps in whenever the market gyrates.

In markets, we hurt ourselves by acting when we should sit tight. Again, great ideas don’t appear often. When they do, we should buy as much as we can and sit on it. Then, do nothing.

Doing nothing is akin to Wilson’s students sitting in a room and not shocking themselves with painful stimuli. The majority of us simply cannot do it, whether due to boredom or negative self-reflection tendencies.

But you know what’s funny? It was our sitting, our doing nothing, that generated all of our returns in Q1. Fascinating how that works.

Quick reminder … If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the button below and sign up. We look forward to seeing you in our Slack!