Most of the time Most mining companies are terrible investments with horrible governance, incompetent management teams, and no plan to build a real business generating actual cash flows.

We’re fortunate to have found three mining companies that are building real businesses with excellent governance, qualified and honest management, and actual cash flows … Idaho Strategic (IDR), Andean Precious Metals (APM), and Magna Mining (NICU).

I mention this because NICU announced another Sudbury-based land package acquisition this morning from NorthXNickel (NIX.CSE).

It’s the perfect example of what every mining company aspires to be (e.g., NICU) and what most mining companies are (e.g., NIX.CSE).

The TL;DR is that NICU fleeced NIX because they’re smarter, more focused, have a stronger balance sheet, and want to build a real company … not some lifestyle product.

There’s a saying, and I don’t remember where I read it or who said it, “Hell is a place where you see all the versions of yourself that you could be if you pushed yourself to the limits.”

Sudbury is that place for junior mining companies … except instead of hell, it’s NICU headquarters.

Here’s why this deal is so important.

NICU received CAD 53M in potential value for less than zero. Does this sound too good to be true?

Let’s get after it.

The First Question: What Did NICU Get And How Much Did They Pay?

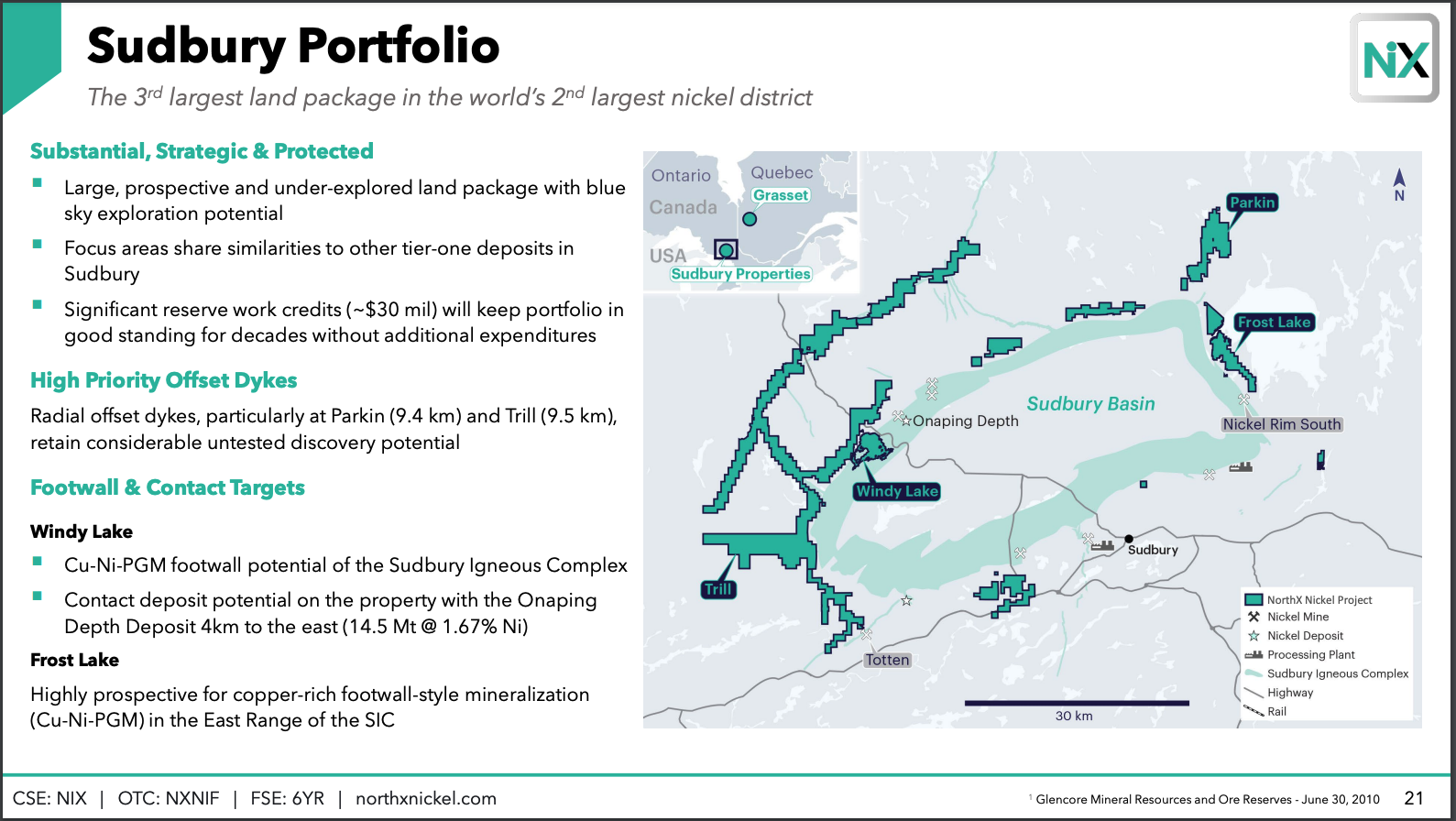

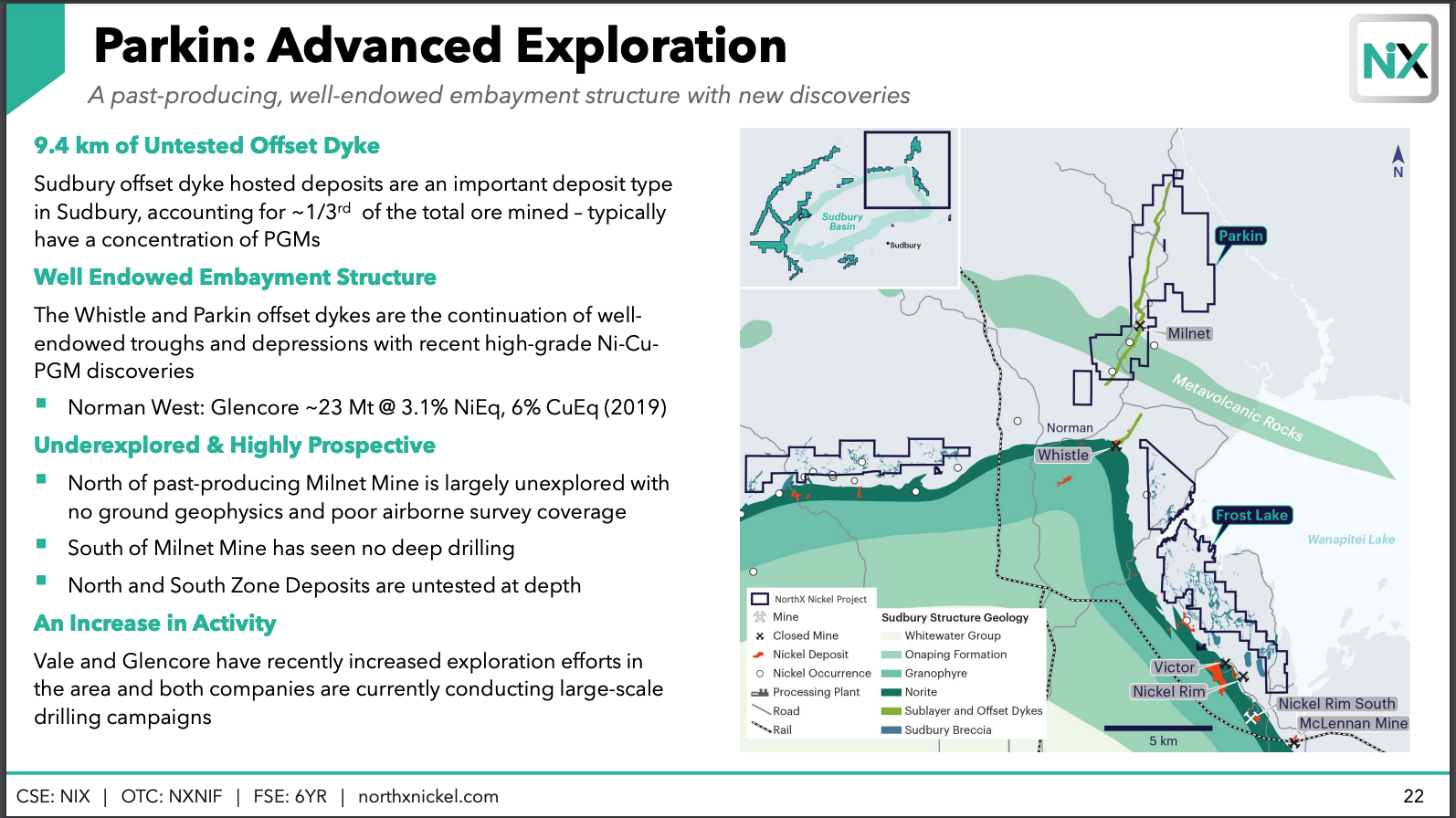

NICU paid CAD 1.00 (not a typo) to acquire two past-producing properties (Parkin and Wisner) and several exploration properties totaling more than 30,000 ha, mainly in the footwall of the Sudbury Igneous Complex (SIC) contact.

According to the company’s press release, Parkin hosts the historical Milnet mine, which produced 157,000 tons and graded 1.5% Ni, 1.5% Cu, and 6.2 g/t Pt+Pd+Au. It also hosts the high-grade Milnet 1500 Zone, which has drill hole intersections up to 4.1% Ni, 0.6% Cu, and 4.3 g/t Pt+Pd+Au over 8.0 meters.

Additionally, the Wisner property historically produced 295,000 tonnes grading 0.9% Cu and 4.1 g/t Pt+Pd+Au from the surface Broken Hammer Zone.

There’s more.

The purchase includes the Blezard, Frost Lake, and Creighton South properties. According to the press release, the Blezard and Creighton South properties cover portions of the footwall environment near the known Blezard and Creighton contact deposits, which have measured and indicated resources of 7.9 million tonnes grading 1.0% Ni, 0.7% Cu, and 6.2 million tonnes grading 4.5% Ni, 3.3 % Cu, respectively.

Here are some slides from NIX’s latest investor deck highlighting the Sudbury assets (see below).

Surface samples from The Blezard have returned assays of >4% Cu.

I told you they’re buying all of this for CAD 1.00.

But that’s not entirely true.

NICU will assume all liabilities attached to the Broken Hammer Project Mine Closure Plan, which includes filing financial assurance with the Ministry of Mines for ~C$481,629 due at closing. They’ll also assume the general liabilities associated with the other assets and properties.

However, NIX will provide NICU with CAD 500,000 cash at closing to cover the Broken Hammer Project Mine Closure Plan.

Instead of paying CAD 1 for these assets, NICU will receive CAD 18,370 to take them off NIX’s hands!

I’ve seen worse deals.

The Obvious Question: Why Would NIX Sell On These Terms?

Earlier, I said that NICU is what every other mining company wishes it were. This is what I mean.

NIX paid NICU to take these Sudbury assets off its balance sheet. Why would any management team agree to that deal?

I see a few reasons.

First, NIX isn’t a real company. It’s a lifestyle company. For example, the company promotes two flagship assets: Sudbury (which NICU just bought) and Grasset (NIX’s cornerstone asset in the Abitibi/Quebec region).

It’s a ~10-hour drive between assets.

However, NIX’s headquarters are in Vancouver … which is 3,169km (1,985 miles) from the company’s two assets.

That’s not to say management teams cannot successfully operate distant mines (APM owns a US gold mine with its headquarters in Bolivia, for example).

But compare that to Magna Mining CEO Jason Jessup. Jason has lived in Sudbury his whole life, and all his professional work experience involves Sudbury-based mines and mining companies.

The dude eats, sleeps, and breathes Sudbury.

Who has the edge in understanding the intrinsic value of these assets? Probably Jason.

Second, NIX is a pico-cap company at <$3M market cap. They have ~ CAD 1.5M in cash with no debt. But they’re burning ~ CAD 1.87M per quarter.

They didn’t have the resources to pursue both assets, so they bet on Gasset.

NIX’s CEO explained the sale (emphasis added):

“Our core focus is on the exploration and development of our 100%-owned Grasset nickel sulphide project, located within the highly prospective Abitibi Greenstone belt in Quebec. The sale of our Sudbury property portfolio streamlines NorthX’s efforts and resources on Grasset, what we view as one of the most attractive undeveloped nickel sulphide projects in Canada.”

I’ll translate … “We’re screwed and need more capital through an equity raise. But we’ve already increased the share count 20x since 2021. I know! Let’s offload our Sudbury asset and say we’re a pure-play in the Abitibi complex. Pure plays are sexy, right?”

Again, compare the two balance sheets. NICU has ample cash after over-subscribing its last equity raise. They have no debt and strategic investors like Dundee on the cap table.

Jason could also buy these assets cheap because we are in the trough of the nickel cycle.

Nickel trades at $15,500/t or the same price in 2003. Like most commodities, nickel has periodic parabolic moves higher but generally trends around $21,000/t (see chart below).

My job isn’t to forecast future nickel prices. That’s too hard. My job is to understand why management teams make certain decisions and judge whether those decisions are smart.

Jason bought these NIX assets at peak nickel despair/hatred.

This is the opposite of what most mining management teams do: buy at peak commodity prices and peak love/adoration because they “think” that’s what shareholders want.

To recap … NICU got paid ~ CAD 13K to own even more of Sudbury because:

- NIX isn’t a real company; it’s a lifestyle corporation … they don’t care about maximizing shareholder value or generating future cash flows.

- NIX management team lives 2,000 miles away from their Sudbury assets and (likely) doesn’t understand the intrinsic value of what they own (i.e., the right asset in the wrong hands).

- NICU bought these assets at cycle lows in nickel prices.

The Final Question: What Could These Assets Be Worth?

The short answer is I don’t know. But we don’t need to worry about the future value because we’re (NICU shareholders) getting paid to own them.

These assets have liabilities, but NIX is paying CAD 500K to cover them. Additionally, I trust that Jason and the team wouldn’t buy assets with more liabilities than future intrinsic value/cash flow potential.

So, while it’s false precision to estimate future value today, we can see what NIX originally paid for these assets (see below).

“Pursuant to the Asset Purchase Agreement, Archer will acquire the Nickel Assets from Wallbridge in exchange for 198,635,786 Archer Shares (each, a “Consideration Share”) at a deemed value of C$0.27 per Consideration Share for a purchase price of approximately C$53.6 million.”

Two years ago, nickel traded for around $24K/t. We’ll probably see those prices again. In that case, NICU was paid CAD 13K to add CAD 54M in value to its balance sheet.

Fantastic work by the Magna Mining team.

This is what a real mining company looks like.