“There is no such thing as a high-probability trade. There are only high-probability situations, and even they fail often.” ~ Al Brooks

Summary: SPX continues to chop in its sideways consolidation while still firmly in a Bull Quiet as it digests the recent narrative tests. The path of least resistance remains higher, and we expect a bullish breakout soon. However, there are some key divergences/weaknesses we’re tracking closely and we won’t hesitate to flip our script should the data say to do so. Gold is showing a persistent institutional bid, which makes the long term trend solid, though shorter-term data suggests we’re due for a pullback soon.

Alright, let’s get to it.

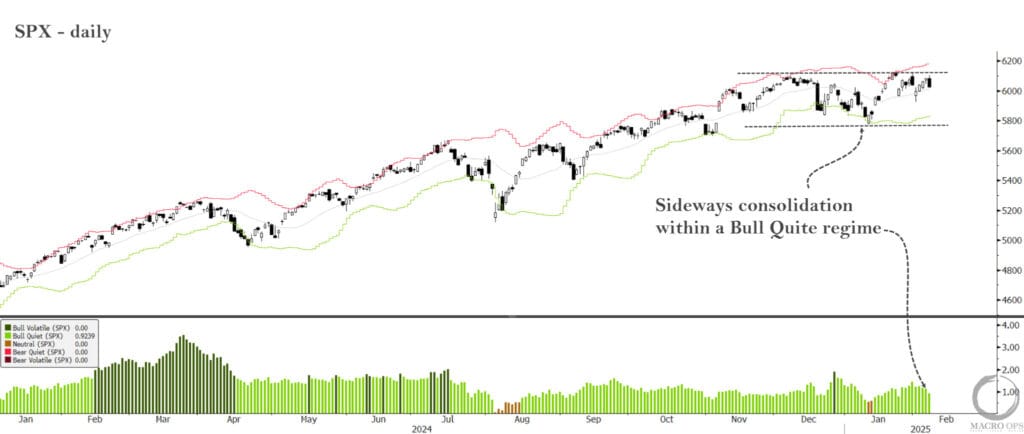

1. SPX continues to trade in a multi-month sideways consolidation within a broader Bull Quiet regime as it digests a number of narrative tests (Deepseek, Tradewar, etc..). So far, so good… and as we noted last week, these “regimes tend to punish shorts and reward disciplined longs.”

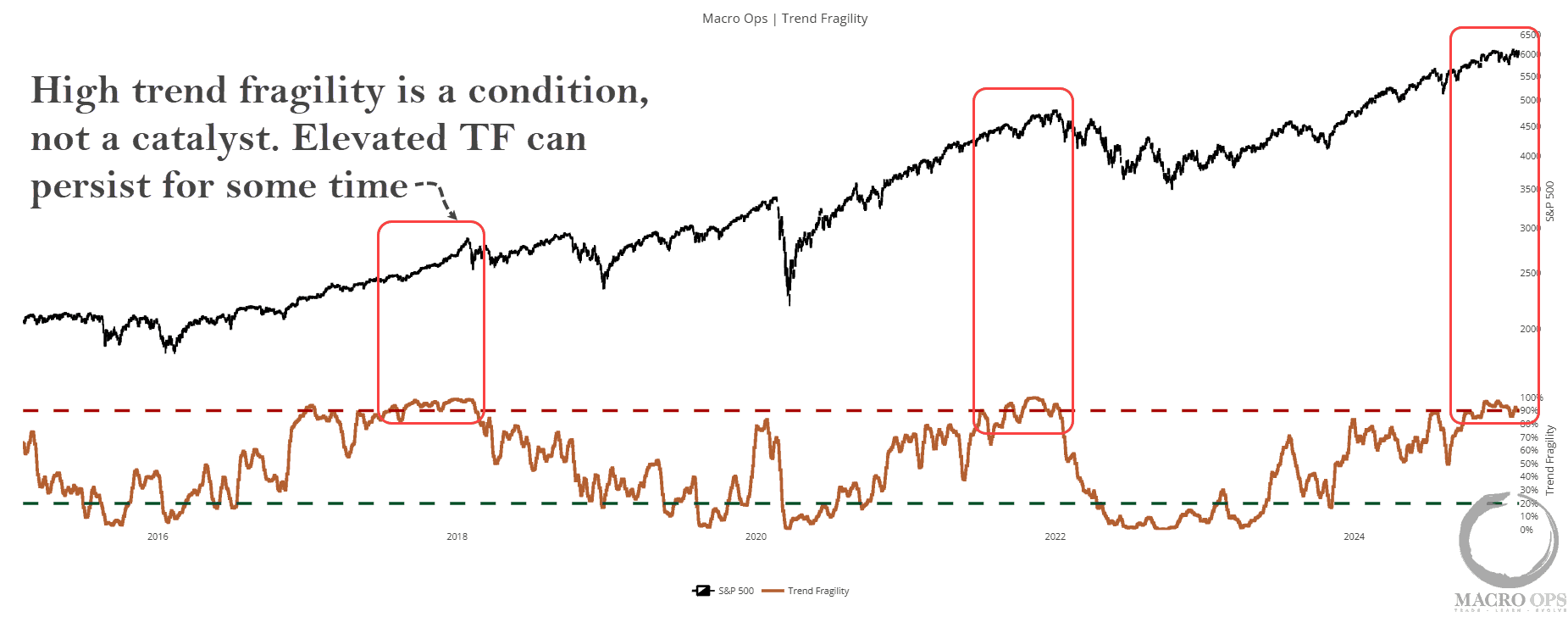

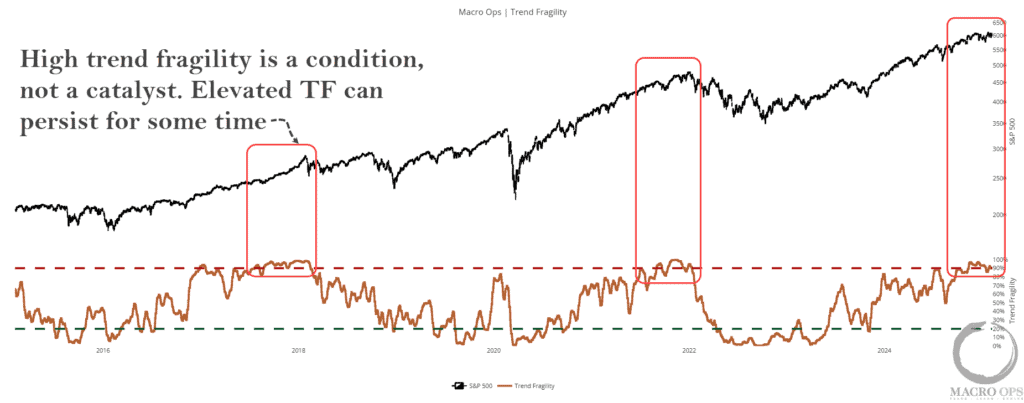

2. Let’s take a Trifecta look at this trend to see if we can triangulate what’s going on beneath the surface. Here we have our Trend Fragility score, which is elevated at around the 90th %tile currently. This is a composite sentiment and positioning indicator that’s showing high levels of bullishness at the moment.

However, this data point is a condition and not a catalyst. And these conditions can sometimes persist for quite a while (note the high reading for the second half of 17’.

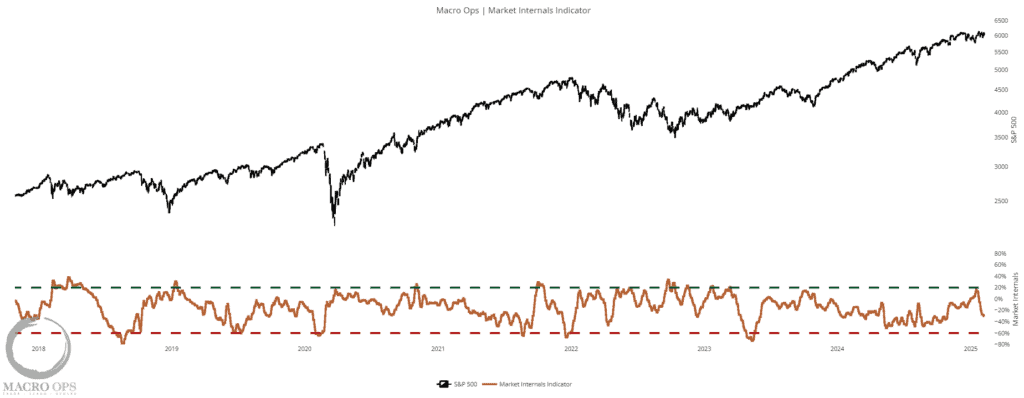

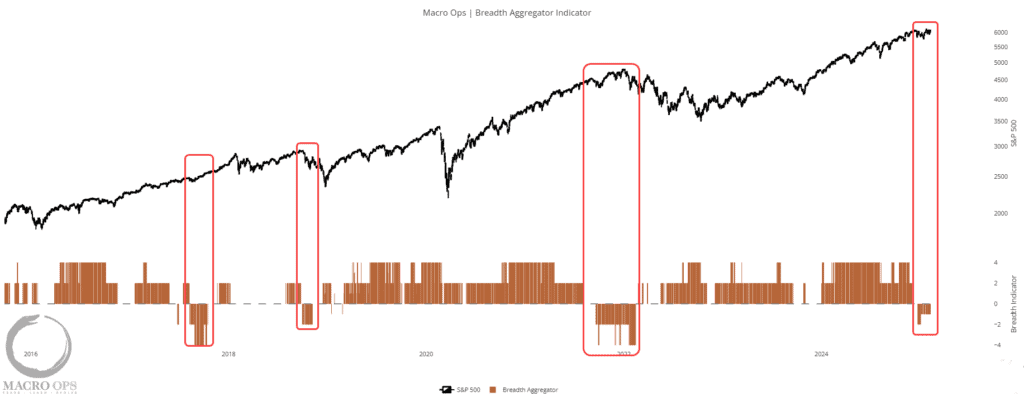

3. Our Internals Aggregator has been dropping like a rock these past two weeks. It’s still in neutral territory, so there’s nothing to act on at the moment. But this is something we need to continue to track.

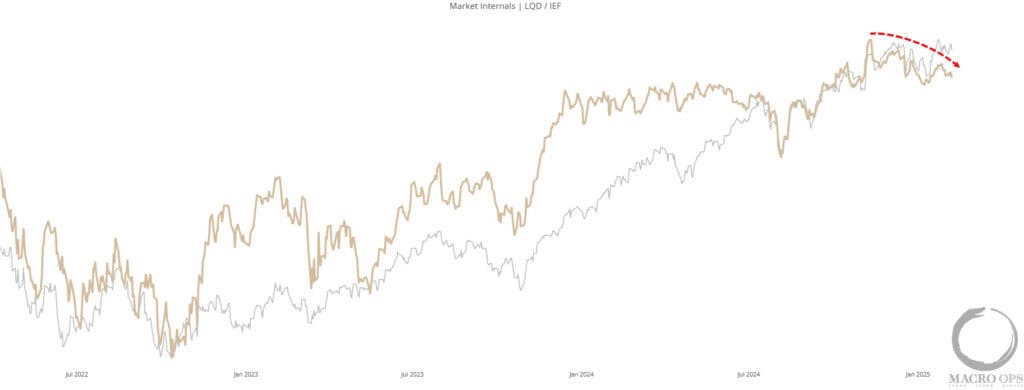

4. The weakening internals has largely been driven by the poor relative performance in semis. But we’re also starting to see credit begin to diverge lower as well.

5. Our aggregate breadth indicator shows that while breadth has improved off its lows since the turn of the year, it remains weak. Similar to internals, this isn’t reason enough to be bearish. Just something to keep an eye on. We’d want to see this flip positive with any bullish breakout from the current trading range.

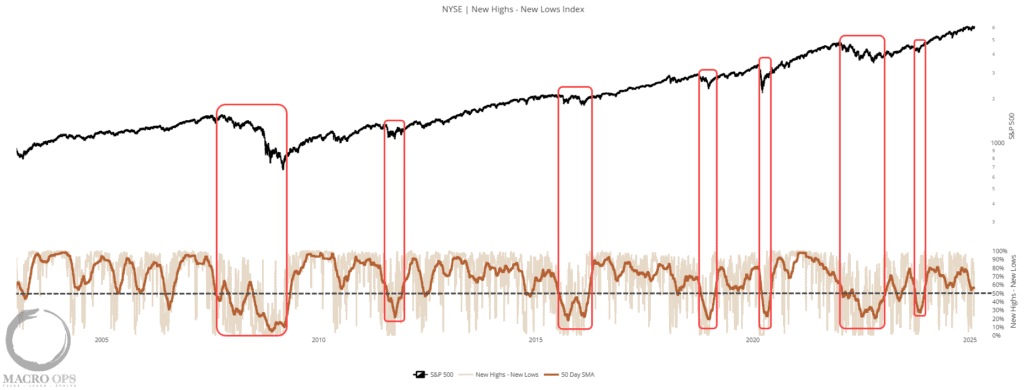

6. An example of one of the weak but still neutral breadth components is the NYSE New Highs-Lows Index. It’s been trending lower but remains above the key 50% mark.

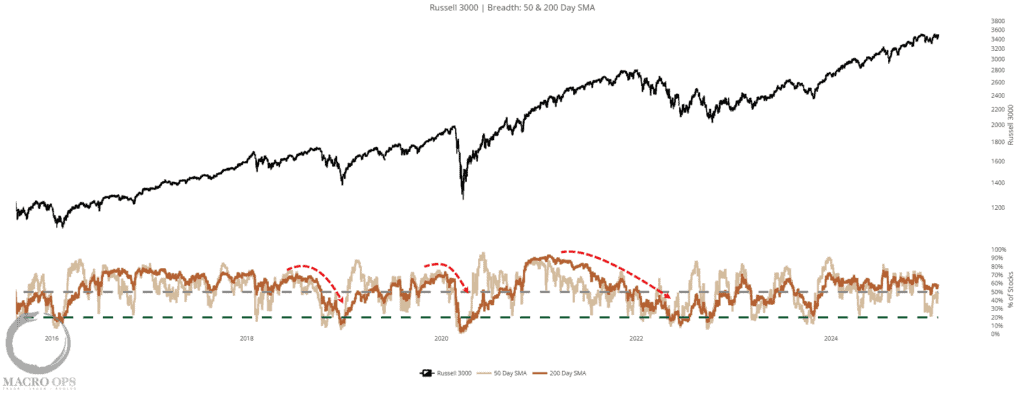

7. While the percent of stocks trading above their 50 and 200dma’s in the R3K index remains above key levels and is generally supportive of an eventual bullish advance from the current trading range.

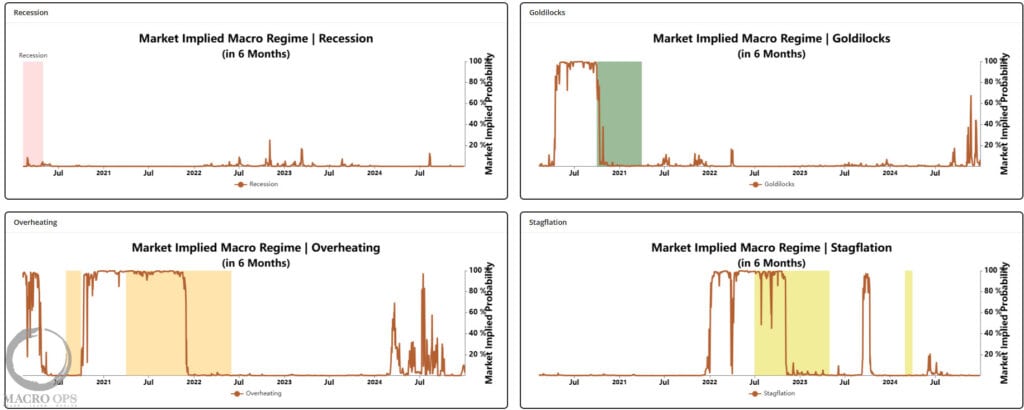

8. Our general read is that the market is digesting the major narrative tests of the past few weeks, while also waiting for the weight of inbound data to signal where things are headed. Our Market Impied Regime model is back to neutral across the board, after we saw a spike in the probability of a Goldilocks Regime earlier this year. This makes sense considering the uncertain policy environement we’ve transitioned into.

9. We continue to be big precious metal bulls, particularly gold. Here’s a weekly chart of the yellow metal. It’s put in 6 consecutive weekly bull bars. This shows a large persistent institutional bid (think central banks buying). This is a long term trend you want to be long and buying on dips. We still think the PM bull is only getting started.

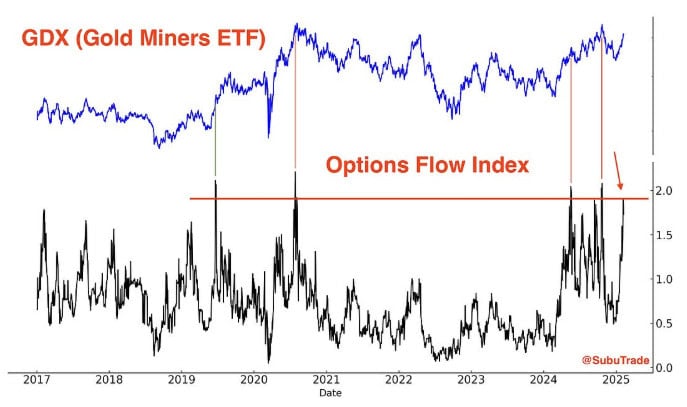

10. @SubuTrade has become one of my regular weekly Substack reads. He puts out some great work. His latest post, which you can find here, suggests we may see some short-term mean reversion in gold soon (we agree). We’re looking forward to this as another opportunity to add.

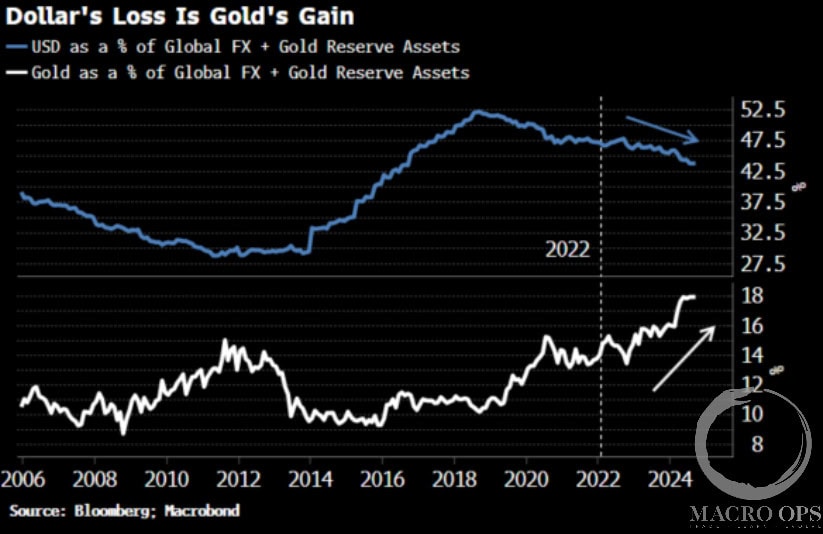

11. BBG’s Simon White shared the following recently “Look no further than the ascent of gold to see what happens when a shortage in viable savings assets is anticipated, from waning demand due to the US’s willingness to use its currency hegemony as a geopolitical stick, but now also through an expected lack of supply of such assets. In fact, official reserves of gold have risen by almost exactly the same amount as those of the dollar have fallen since 2022. A soft-for-hard asset swap. “

12. Speaking of soft-for-hard asset swaps, we continue to be big long term bulls on resource plays. Brandon shared the writeup on one of our holdings, Magna Mining, this past week, concluding: “NICU is truly unique. It has a world-class management team executing a playbook they created to generate 100x returns in the same jurisdiction, with the same assets, with 200-1,200% upside at potentially trough-level nickel equivalent prices.” You can read his piece here.

The MO portfolio officially closed things out with a +50.4% return on the year. The team and I will be publishing our eoy review soon, where we’ll dive into our painful mistakes and total blunders, as well as the things we’ve learned and what we’ll try to do better in the year ahead. So keep an eye out for that. And if you’d like to join our Collective as we tackle 2025 head on, just click here.

Thanks for reading.