The Magna Mining (NICU) story is picking up steam. I’ve pitched it to nearly everyone I know. Most of the time they stop me after “so this is a mining comp–.”

While I’m seeing more write-ups on the company (s/o Unemployed Value Degen!), I’ve noticed they all miss the same thing: the importance of Jason Jessup and the NICU management team.

Make no mistake that NICU is a Bet The Jockey play. And that’s the best part. Jason and his team are executing the same playbook they used to help turn FNX Mining from $0.25/share to $15/share.

He’s doing the same thing with the same (arguably better) assets and same people.

So that’s why I’m sharing my initial NICU write-up. I sent this to our Collective members in September and bought a position in our MO portfolio, which is now ~12% of our book.

I hope you enjoy.

“I’m not selling a single share until we are a $1B company.” – Jason Jessup, CEO

Magna Mining (NICU.V) is a growing junior nickel developer with assets in the Sudbury region of Canada. It recently completed two transformational acquisitions and is on a path to reaching a market cap of $1B+ over the next few years.

NICU checks all the boxes at the mining company level and our Trifecta Lens criteria.

- Fundamentals: NICU is on the path to creating 3-5 producing mines within the decade with substantial free cash flow.

- Sentiment: Before this acquisition, NICU was a primary nickel play. Nickel is extremely hated thanks to cheap Indonesian supply and a cratering commodity price. Nobody likes nickel currently, and nobody is investing in nickel production domestically.

- Technicals: NICU chart is breaking out to new highs on the weekly and monthly time frames on major buying volume. It’s within $0.20/share of its all-time highs.

Before founding NICU, CEO Jason Jessup worked at FNX Mining, which went from $0.25/share to over $35/share in a decade.

Here’s the exciting part … Jason is creating FNX 2.0.

He’s hiring the same FNX Mining team, exploring the same geology, and executing the same FNX playbook of buying non-core assets from significant producers like Glencore, Vale, and KGHM. Management eats their own cooking and owns ~10%.

The value proposition is substantial. Post-acquisition, NICU will have 82Mt of 1.5% Nickel Equivalent (NiEq) or 2.71 billion pounds of resources for an in-situ value of ~$25B.

In a few years, they’ll have four producing mines generating over $300M in annual free cash flow.

All of this translates to nearly $2B in potential market cap.

It’s yours for today’s price of $150M.

The FNX Mining 2.0 Playbook

To understand NICU, we must first understand FNX Mining, one of the most successful and profitable mining ventures in the past two decades.

Terry MacGibbon, a former Inco mining executive, started FNX Mining in his basement in 1995. At the time, the stock traded around $0.25/share.

He had a simple strategy: acquire non-core nickel-copper-PGE assets from major producers in the Sudbury region.

The macro backdrop wasn’t that different from today, either (see below):

“It was not an auspicious start for a mining junior. The Bre-X scandal was discovered earlier that spring, causing many investors to stay away from the mining sector and put their money into technology shares. The dot.com boom was just beginning. In the fall of 1998, the price of nickel hit its lowest price ever – $1.76 (US) – when inflation was factored in.”

Undeterred, MacGibbon bought five former producing mines from Inco (his former employer): Levack, McCreedy West, Norman (later renamed Podolsky), Victoria, and Kirkwood … remember these names.

MacGibbon explained the reasoning behind buying these assets (emphasis mine):

“At the time, we knew there were smaller deposits in both mines that a junior could operate at a profit and that CVRD Inco needed that ore due to a shortfall from their other Sudbury Basin properties. The near term mining potential was very good. That is why we bid so aggressively for the assets.”

It’s a win-win situation. The major offloads non-core assets, the junior gets a deposit they can operate profitably, and the junior feeds ore into the major’s mill.

The result? McCreedy went from Care & Maintenance to production within a year. FNX reconditioned Levack by 2007, and the Podolsky mine was ready for commercial ore shipments by 2008.

FNX made a profit in its first quarter of production, and the rest is history.

The company merged with Quadra Mining in 2010, then acquired by KGHM in 2011 for $2.84B.

NICU has a similar plan.

How NICU Executes The FNX 2.0 Playbook

There’s so much going on with NICU that it’s hard to wrap your head around it all. The company released an initial PEA last year, acquired Crean Hill, released incredible assay results, acquired five KGHM assets, and updated its Crean Hill PEA …*breathes*

Let’s focus on the pre-acquisition assets and potential cash flow.

NICU has two primary assets:

- Crean Hill:

- Open Pit Indicated Resource: 16.76 million tonnes

- Underground Indicated Resource: 14.53 million tonnes

- Total Indicated Resource: 31.29 million tonnes

- Shakespeare:

- Open Pit Indicated Resource: 16.51 million tonnes

- Underground Indicated Resource: 3.83 million tonnes

- Total Indicated Resource: 20.34 million tonnes

For a total combined resource estimate of 52Mt (or 1.48Blbs NiEq).

NICU trades at ~$0.10/lb NiEq at its current $150M market cap from just these two assets.

Its peers trade at an average of $0.24/lb NiEq (see below).

However, NICU should trade above peer and comp averages. Here’s why.

Above Peers: Tier-1 Jurisdiction, High-Grades, Fully-Permitted, & Ore-Selling Agreements

NICU operates in Sudbury, Canada. Sudbury is probably the best mining jurisdiction globally.

It has a 130-year history of mining, multiple mining suppliers/vendors have their headquarters in Sudbury, there’s a growing population of talented labor, and it’s close to large North American markets with excellent infrastructure.

And when it comes to nickel mining, you can’t beat Sudbury. According to New Age Metals, the Sudbury basin contains 1.6B tons of material grading 1.2% Ni, 1% Cu, and 0.8g/t PGM.

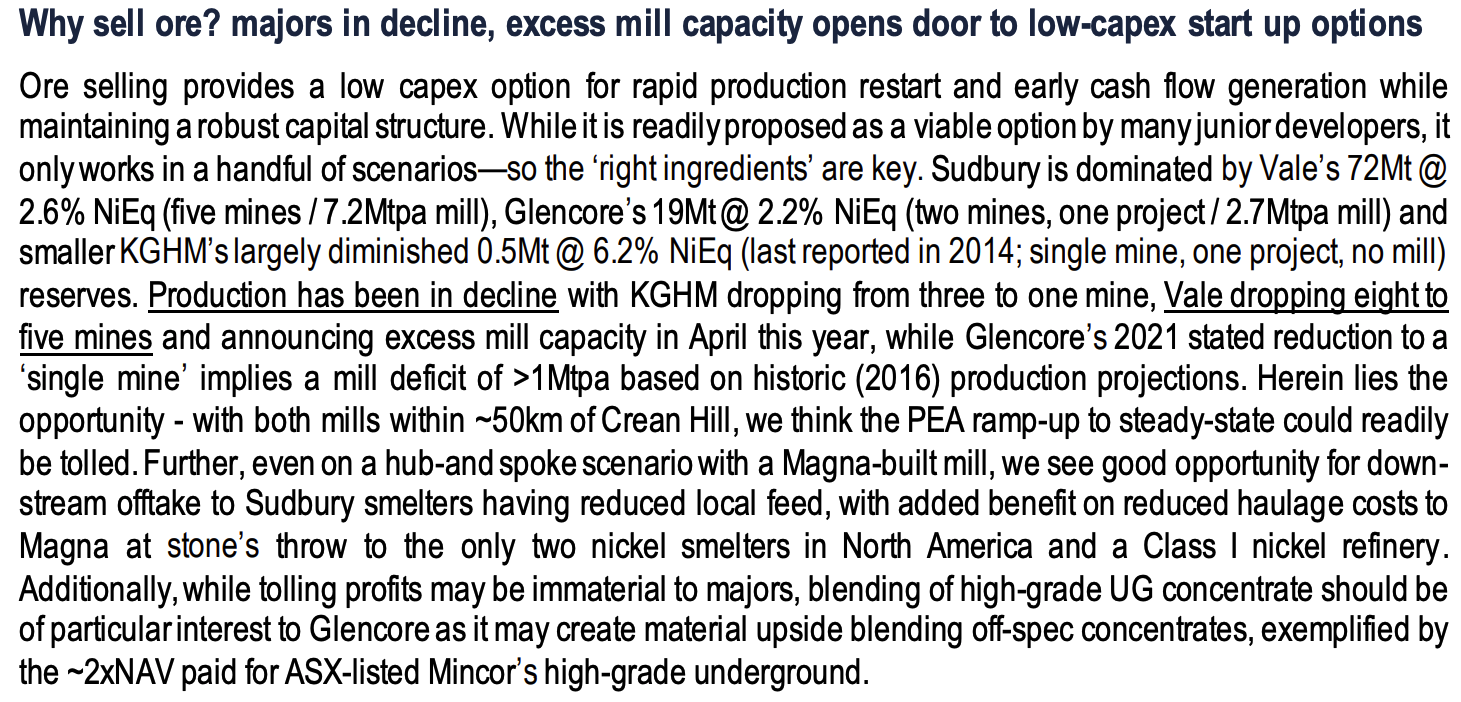

NICU is also unique because it is fully permitted with an ore-selling agreement with Vale.

Major mining companies like Vale and Glencore are increasingly eager to secure ore for their Sudbury mills due to declining production from their existing nickel mines in the region.

Companies like NICU can sign more favorable offtake agreements with the mills.

According to a 2023 SCP Research report, Glencore’s Nickel Rim South mine is transitioning to “care and maintenance” by spring 2025, with a >30% decline in total NiEq (nickel equivalent) production in Sudbury by 2026.

Other majors like KGHM and Vale have also reduced mine production and are hungry to feed their mills. (see below).

So those are NICU’s pre-acquisition assets. There’s a 250-500% upside from Crean Hill and Shakespeare.

The following KGHM assets are icing on the footwall (mining investors will get the humor attempt).

NICU’s Recent Acquisition of KGHM Assets: FNX 2.0!

NICU bought five non-core assets from major producer KGHM:

- McCreedy West Copper Mine

- Levack Mine

- Podolsky Mine

- Kirkwood Mine

- Other exploration assets (Falconbridge footwall, Northwest Foy, and North Range & Rand)

We’re assigning a $0 value to the “Other Exploration assets” as they’re still too early to get resource estimates. Instead, we’ll focus on the four past-producing mines.

NICU financed the deal with C$7.3M in cash, $2M in NICU shares, and C$24M in deferred payments.

There are three reasons why this deal is so significant.

First, Jason and his team know these assets better than anyone else. They worked in these mines during the FNX days. They see the value there and know how to restart each mine and quickly maximize cash flow.

Second, the McCreedy West copper mine turns NICU into a copper producer play. The market values copper producers much higher than nickel developers. So NICU should get a P/NAV re-rating.

Third, NICU can use the cash flow from McCreedy West to finance the production ramp at Crean Hill. This eliminates the need to dilute shareholders or incur debt.

As of 2023, McCreedy West produced 317.6Kt of 1.59% Cu and 2% NiEq. NICU plans to ramp production at McCreedy from 317Kt/year to 720Kt/year.

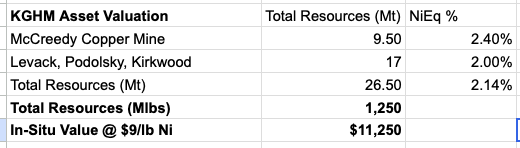

The other reason I love the acquisition is that it adds another 1.25 billion pounds of NiEq to NICU’s resources—$11 billion in in-situ value at $9/lb nickel (see below).

NICU’s valuation estimates are on a NiEq price-per-pound basis (see below).

The company has ~800% upside at its closest peer valuation of $0.46/lb NiEq at the current market cap.

So far, we’ve discussed the company’s resources, its in-situ valuation, and why NICU should trade at a premium to its peers for its current resource base of 2.7Blbs NiEq.

But we don’t get paid on in-situ value. We get paid from cash flow. Let’s examine the company’s potential annual cash flow as they ramp to 3-4 producing mines in 3-4 years.

3-4 Mines in 3-4 Years

According to CEO Jason Jessup, the current NICU plan seems to be:

- Ramp McCreedy West from 317Kt/yr to 720Kt/yr

- Use McCreedy West cash flow to finance the ramp of Crean Hill

- Restart Levack, Podolsky, and Kirkwood

- Use cash flow from McCreedy, Crean Hill, and Levack/Podolsky/Kirkwood to finance Shakespeare mine production and mill

So, by 2028, NICU could have four producing mines while constructing Shakespeare and its own mill.

I’ve talked to a few NICU investors about the next 3-4 years and have a rough, back-of-the-napkin model. You can see it below.

This model contains many assumptions. It’s rough; take it with a grain of salt. All I’m doing is trying to capture the potential earnings power of NICU’s four mines once they ramp production to a steady state.

If the above model is directionally correct, NICU will generate ~$300M in operating profit annually. That’s not including future free cash flow from Shakespeare.

I hope you see how absurd the value proposition is at the current market cap. For instance, NICU trades at 2x fully-ramped McCreedy West free cash flow.

So you’re paying 2x cash flow for one producing copper mine and getting Levack, Podolsky, Crean Hill, Shakespeare, and the other exploration assets for free.

The company should fund these expansions from internally generated cash flow (see above plan). That means little dilution over the next 3-4 years, which explodes IRRs.

Acquisition multiples for mid-tier nickel producers in tier-1 jurisdictions range from 4-8x cash flow. That puts NICU at a $1.8B valuation at the midpoint of 6x cash flow for a 1,200% upside.

These cash flows, multiples, and in-situ valuations aren’t extreme, either. If anything, NICU should trade at premiums to market averages for in-situ and cash flow valuations.

Conclusion: A Clear Path To One Billion Dollars

There are tons of risks with this thesis. But they’re all external risks that every mining company experiences (depressed nickel prices, global recession, Indonesian flooding supply, etc.). NICU is truly unique. It has a world-class management team executing a playbook they created to generate 100x returns in the same jurisdiction, with the same assets, with 200-1,200% upside at potentially trough-level nickel equivalent prices.