To bankrupt a fool, give him information ~ Nassim Taleb

Summary: SPX is going through a narrative test, and while we expect volatility in the near term, the broader trend remains intact. The USD continues to rampage against other major currencies despite the consensus impulse to fade the DXY. The labor market is showing cracks, while disinflation is becoming more pervasive. Bonds look to have bottomed, and we’re looking to buy. Plus, NVDA is on the precipice, and we might be going short.

Alright, let’s get to it.

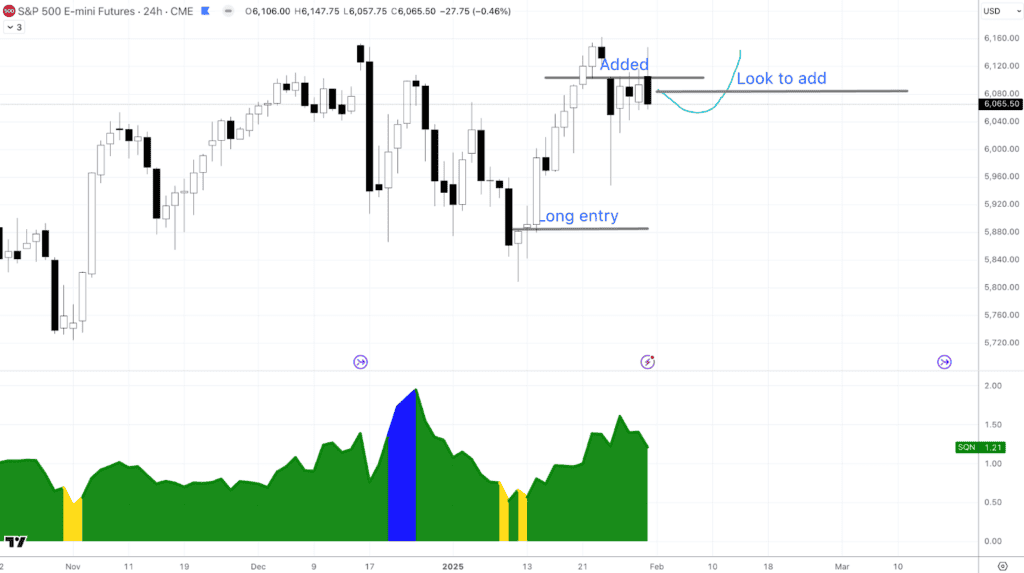

1. My partner Chris wrote the following in yesterday’s Sunday Setup that “with the recent tariff news creating uncertainty, there might be more weakness early this week. But if strength returns and this ‘best-looking sell setup’ fails, it’ll be our signal to increase position size and tighten stops. This is where I’ll lean in—capitalizing on the tendency of this regime to punish shorts and reward disciplined longs.”

I agree with Chris here. This doesn’t mean we’ll blindly go long this week. First, we need the market to confirm it’s survived this narrative test—meaning the dip gets bought. We’ll be waiting to see how things shake out.

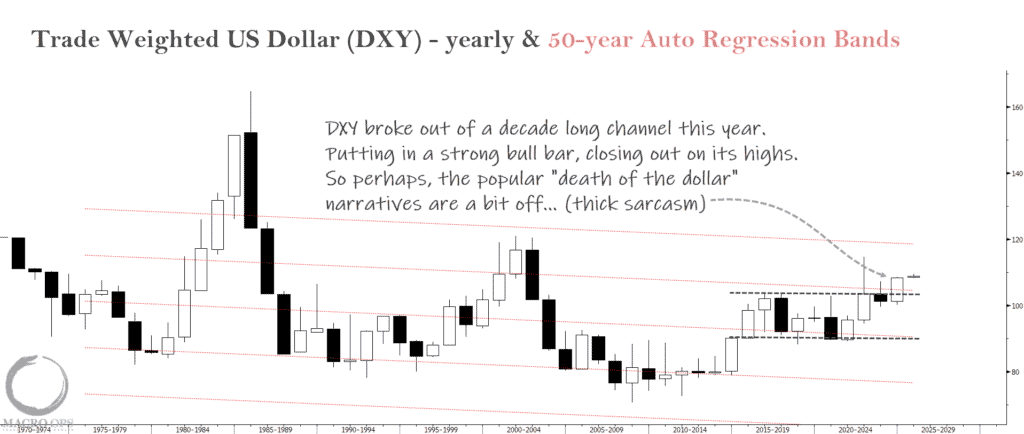

2. At the very start of this year, I wrote here in these pages that:

“This is one of the most important macro charts going into 25’, in my opinion. It’s a yearly candle chart of the trade weighted US dollar (DXY). It shows DXY decisively broke out from its decade long rectangle in 24’.

“We’ve spent the last few years making fun of the degens ranting on about the dAeTH oF thE uS DolLAr as a global reserve currency. It’s exactly that type of based sentiment that sets the stage for monster rallies.

“24’ was a BIG breakout year for the USD. We might be in for a big USD bull trend here.”

USD price action to date strongly confirms the above. I read that the general consensus is still to fade the USD here. That means more short covering to fuel the bull move.

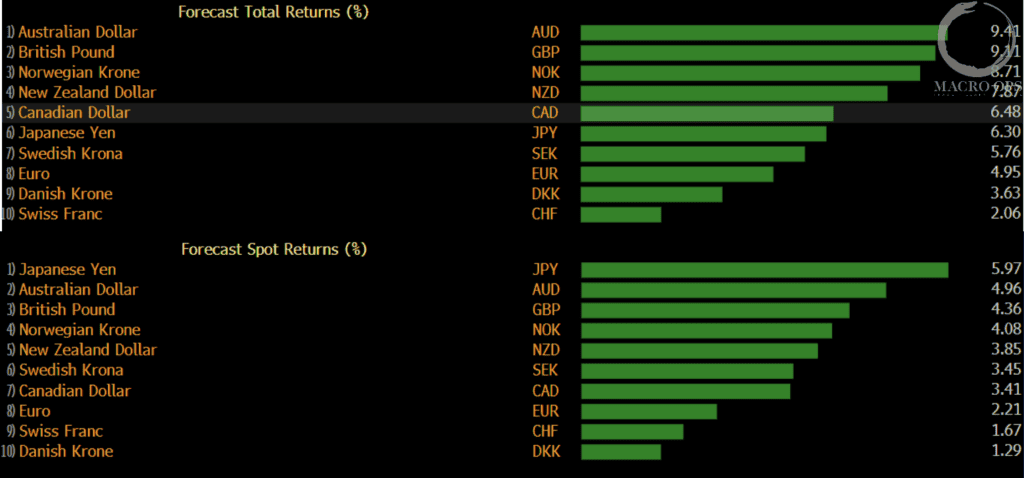

3. Here’s the BBG consensus average forecasted spot and total returns for major currencies against the dollar in 25’. All expect a bearish USD.

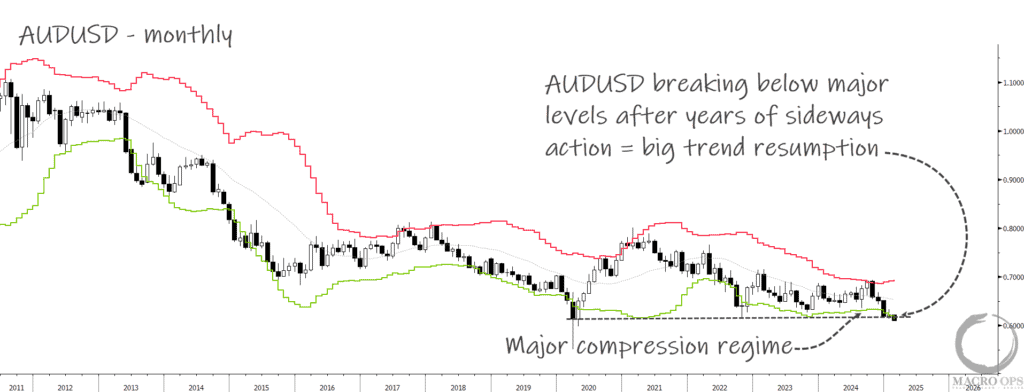

4. For over six months, I’ve been writing about the major compression regimes in key macro assets (USD pairs, crude, BTCUSD, precious metals). Many of these compression regimes are in the process of resolving. In other words, they’re breaking out to start what will likely be big trends.

Here’s AUDUSD busting through the bottom of its large monthly Bollinger Band squeeze. This is a chart you want to be looking for spots to get short.

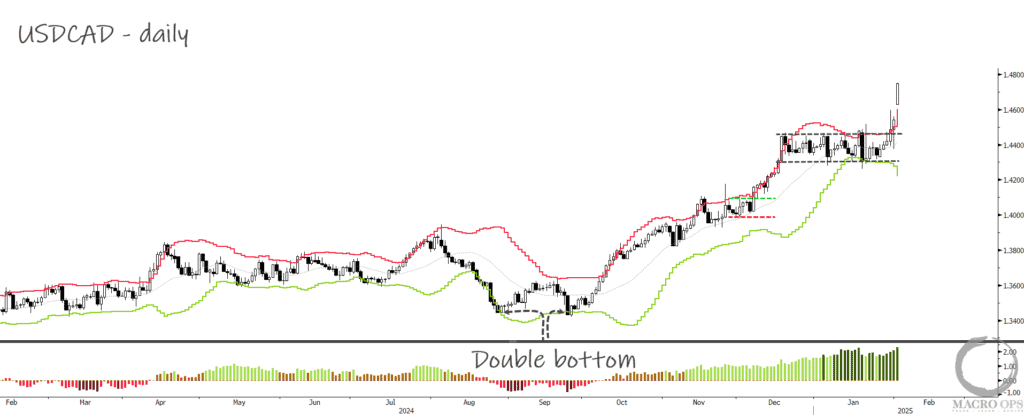

5. USDCAD is a pair we’ve been making the bull case on for the past few months (example here) and one we’ve been actively trading on the long side. Today’s bar gives us another continuation from a textbook rectangle congestion pattern.

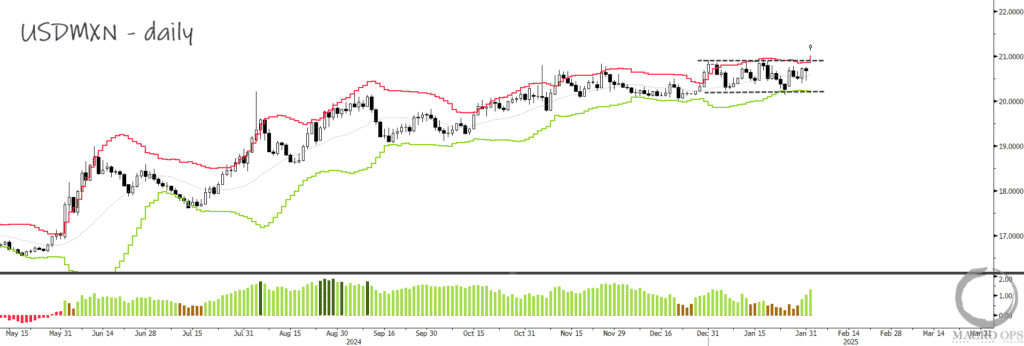

6. We just go long USDMXN on its breakout from this similar pattern.

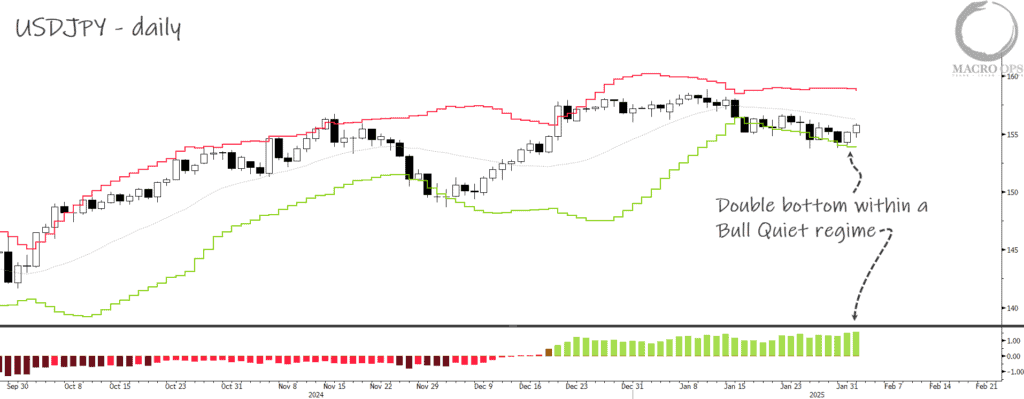

7. I have buy stops in on USDJPY to pull us in long on a move slightly above Wednesday’s highs.

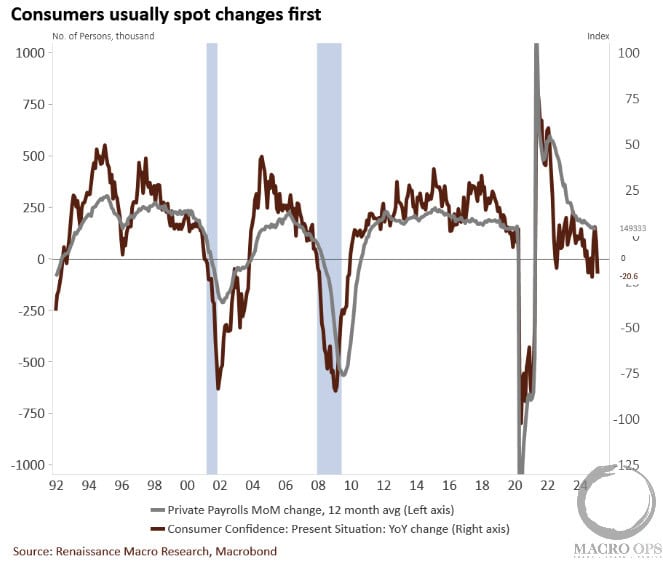

8. RenMacLLC shared the following this weekend “Consumers tend to spot changes in their local labor markets ahead of the published statistics. In January, the present situation sub-index of the Conference Board survey fell to a three-month low, down 20.6pts against last year. Not a welcome sign for future jobs growth.

“…Unemployment is low, but the job finding rate does not paint a picture of a particularly strong labor market. Both rates of job finding and hiring have gone a bit beyond where they stood immediately preceding the pandemic.”

I concur. While I don’t see an imminent recession, I do find it ironic that after nearly two years of a recessionist narrative consensus, the popular view has flipped to higher for longer at precisely the point when real cracks are starting to appear for the first time in ages…

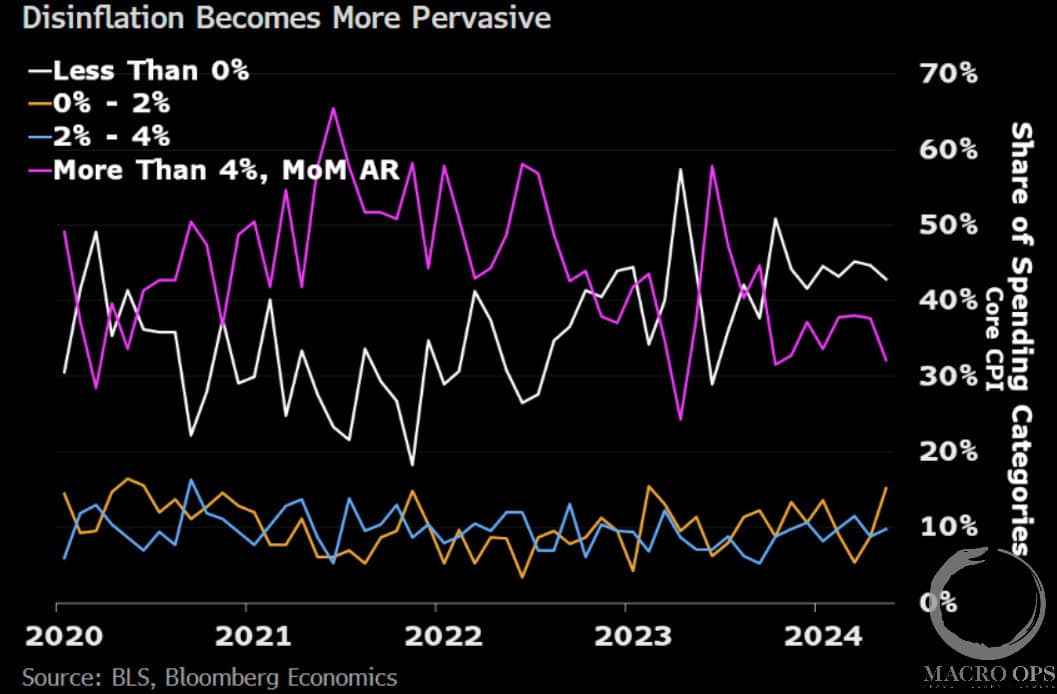

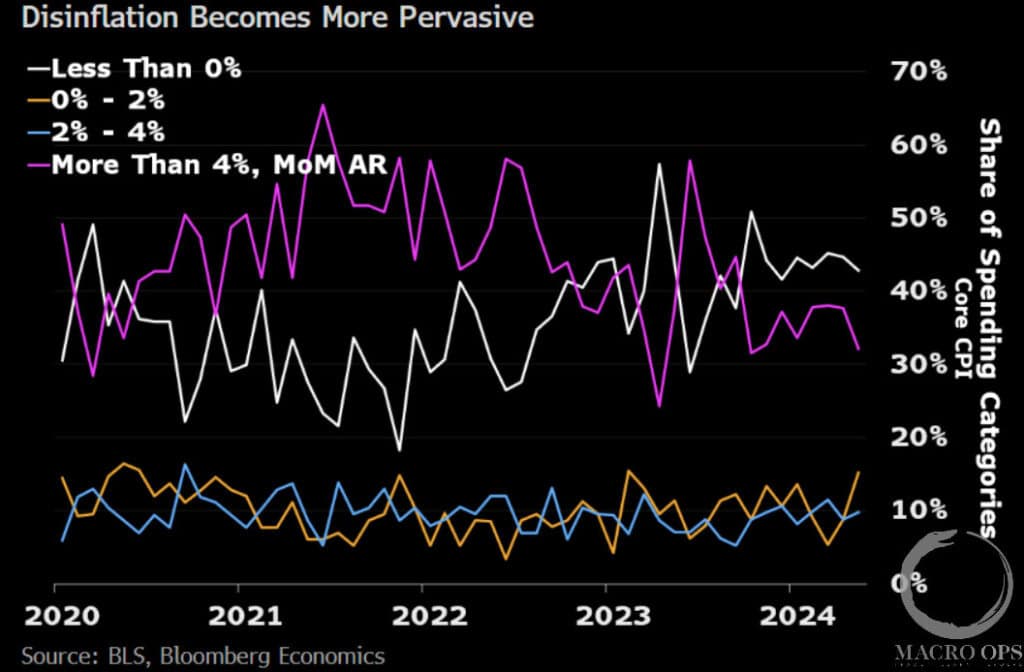

9. BBG chart showing that, contrary to popular belief, disinflation is becoming more pervasive, not inflation…

10. From BBG “If the White House goes ahead with threats on Mexico, Canada, and China, it would increase the average US tariff rates on all goods imports to more than 11% from 3%. This remains below Trump’s campaign pledges to put 60% tariffs on China and 20% on all other partners — but it would be a more aggressive approach than we envisaged as a tentative base case before he took office.”

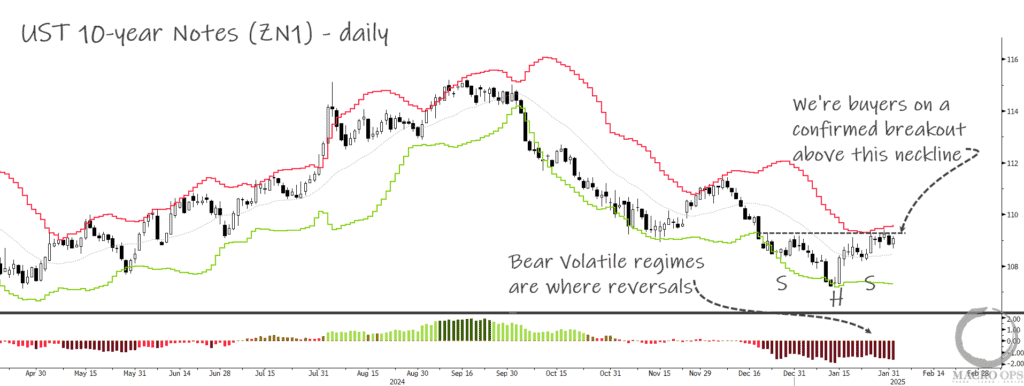

11. 10yr Notes are in a Bull Volatile regime (which is where key reversals occur) and is close to completing an inverted head and should bottom. Long bonds seem to me like a very anti-consensus trade. We’re buyers on a confirmed close above the neckline.

12. Even after NVDA’s recent selloff, they are still a roughly $3trn marketcap company trading over 25x revenues. To put this absolutely insane valuation into perspective, NVDA would need to grow its revenues more than 11x, while keeping its marketcap steady (meaning its stock price trades sideways), just to come down to the long-term average tech P/S ratio of 2.3x.

Nothing like that has ever remotely happened in the stock market’s history for a company of NVDA’s size.

They’ve put a double-top on the monthly chart. We remain in a larger bull market, so this is not a high-conviction short. But I’m willing to plunge in small size on a close below the recent swing low.

The MO portfolio officially closed things out with a +50.4% return on the year. The team and I will be publishing our eoy review soon, where we’ll dive into our painful mistakes and total blunders, as well as the things we’ve learned and what we’ll try to do better in the year ahead. So keep an eye out for that. And if you’d like to join our Collective as we tackle 2025 head on, just click here.

Thanks for reading.