Michael Burry is an investing legend and Twitter favorite. His 13F filings dominate niche FinTwit discussions. But, true to his style, Burry’s portfolio is a hodge-podge of obvious value plays and “ick” factor bets. It’s why everyone loves him. He’s always fishing where the fish are, even if there isn’t another boat around.

This week, Burry released his Q1 2021 13F filing, which you can read here. The Big Short bet big on three industries …

- Healthcare

- Energy

- Transports

While also adding two massive short positions in Tesla (TSLA) and US 20+ Year Treasuries (TLT). These two shorts encompass ~52% of Burry’s entire US portfolio. TSLA alone is a 40% position!

But beyond the TSLA short headlines, there are a few takeaways from Burry’s latest portfolio — like why is he long so much energy? What does he see in the transports space? And why did he invest in three small-cap healthcare companies?

We’ll try and answer these questions below. So crank the death metal, grab your drumsticks, and let’s get after it.

Burry’s (Latest) Big Short: Tesla Puts

Burry sent Twitter into a feeding frenzy when his 13F reported a monster 40% short position in Tesla via put options. Burry bought ~8,000 put options on Tesla, giving him exposure to an 800K notional share amount for $534M.

We don’t know what strike price he bought them nor the expiration date, all critical in determining Burry’s time horizon for his short bet. But there are a few things we know. First, TSLA has one of the ugliest charts in Cathie Wood’s family of businesses (see below).

Plus, TSLA trades at a larger market cap than the entire auto industry combined. Yet, for some reason, the company can’t sell cars at a profit (which some would argue is an essential part of any auto company).

Finally, ARKK owns a lot of TSLA stock. As a result, should itsETF face a liquidity crisis (which Edwin Dorsey outlined here), it could trigger forced-selling to cover redemptions.

If you’re joining Burry on this short (like I am in my personal account), manage risk accordingly, whether that’s through stop-losses or outright put positions.

Let’s move on to Burry’s three big industry bets, starting with Healthcare.

Burry’s Healthcare Bets: MRNS, ARPO, & ZYME

Burry bought three new healthcare companies during Q1:

- Marinus Pharmaceuticals (MRNS)

- Aerpio Pharmaceuticals (ARPO)

- ZymeWorks, Inc (ZYME)

Remember, Burry’s a medical doctor by trade and stock picker by passion. As a result, he likely has a competitive edge over the average investor in this space regarding the potential efficacy of certain drugs.

Let’s see why Burry might’ve bought these three names.

Marinus Pharmaceuticals (MRNS)

MRNS is a ~$600M clinical-stage pharmaceutical company that focuses on developing and commercializing therapeutics to treat rare seizure disorders. The company’s leading drug, ganaxolone, helps with epilepsy and various depressions like postpartum depression.

Like most clinical-stage companies, MRNS has virtually zero revenue. Yet, last year the company generated $1.72M in top-line revenue while losing $68M in operating income. These companies are like call options or lottery tickets. You buy hoping the drug meets FDA approval and hits the mainstream therapeutic market.

Specifically, ganaxolone targets CDKL5 Deficiency Disorder (CDD). CDD is caused by the mutation of the cyclin-dependent kinase-like 5 gene, located on the X chromosome. The disorder affects females primarily with symptoms including scoliosis, visual impairment, sleeping disorders, and an inability to walk or talk.

CDD affects roughly 1 in 40,000 live births with no FDA-approved disease-specific treatments.

For those interested in learning more, you can read MRNS’s latest investor presentation here. The chart looks decent, too. MRNS is a ~0.34% position in Burry’s book (i.e., lottery ticket allocation).

Aerpio Pharmaceuticals (ARPO)

ARPO is a $55M biopharmaceutical company that focuses on developing and commercializing compounds that activate Tie2 for the treatment of ocular disease and vascular stabilization. The company is run by its founder and President, Dr. Joseph Gardner.

ARPO’s lead product, razuprotafib, is a small molecule inhibitor that has completed Phase IIb clinical trial for the treatment of non-proliferative diabetic retinopathy. It’s also completed Phase II trials for the treatment of patients with open-angle glaucoma/ocular hypertension.

Add another ~$43M in net cash, and you can buy this business for ~$12.35M Enterprise Value. Burry owns ~2% of the company, making it a 0.10% holding in his fund.

The company’s attacking a $2.0B adjunctive therapy market with a significant need for working therapeutics. 3M Americans suffer vision loss and blindness from Open Angle Glaucoma. Most sufferers receive Prostaglandin eyedrops, yet 50% of patients fail with the therapy.

ARPO’s value proposition is simple. The company assumes that patients will need ~20M prescriptions (Rxs) for adjunctive therapy by 2030. At 50% market share, ARPO would capture 10M Rxs at $150 per Rx, or $1.5B in 2030 US Sales. Assuming a bear case (20% market share and $100 per Rx price), ARPO would generate ~$400M in revenue by 2030.

You can buy this company for ~$12M Enterprise Value today, or 0.02x 2030E EV/Sales (you know, if you’re into that kind of thing).

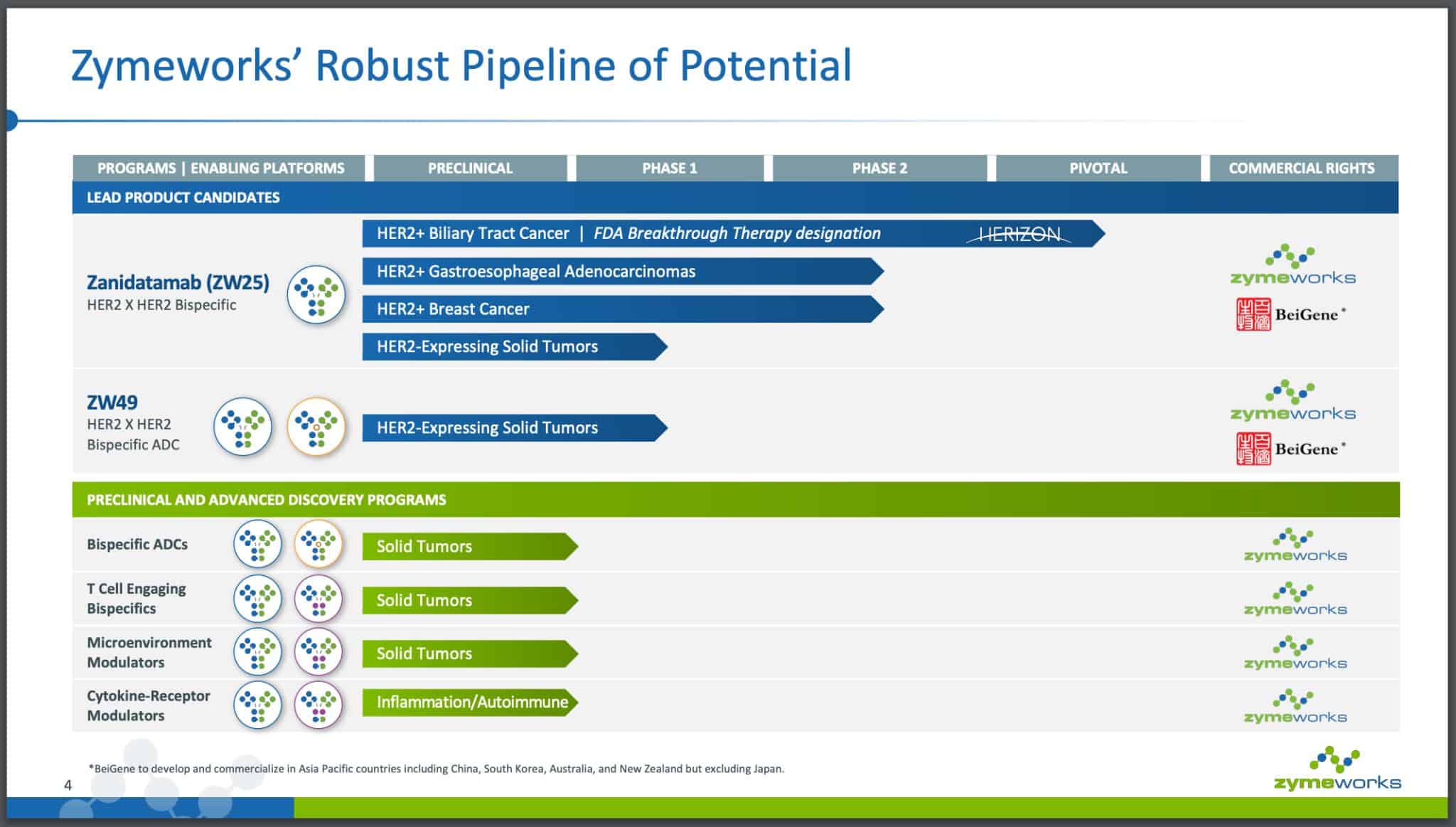

ZymeWorks, Inc. (ZYME)

ZYME is a $1.4B clinical-stage biopharmaceutical company that discovers, develops, and commercializesPermian therapeutics for cancer treatment. The company has two main drugs: zanidatamab and ZW49.

ZYME generated ~$40M in revenue last year while losing nearly $200M in operating income. The company has two drugs in the late stages of approval/early stages of commercial development (see slide below).

ZYME partners with other healthcare companies like Merck, Lilly, or Johnson & Johnson and sells its drugs through these partners. So far, the company’s received $217M from its total partnerships. ZYME estimates that they’ve got ~$8.6B left in revenue from these partners.

Check out the investor presentation here if you want to learn more.

Burry’s Energy Bets: OXY, HP, GOGL

Scion Capital added three new Energy names to its book:

- Occidental Petroleum (OXY)

- Helmerich & Payne, Inc. (HP)

- Golden Ocean Group (GOGL)

Let’s start with OXY.

Occidental Petroleum (OXY)

OXY engages in the acquisition, exploration, and development of oil and gas properties in the United States, the Middle East, Africa, and Latin America. The company is one of the lowest-cost producers in the Permian Basin and generated a record $1.6B in FCF during Q1 2021.

Here are a few more insights on OXY:

- Largest merchant caustic soda seller in the world

- Largest VCM exporter in the world

- 2nd largest chlor-alkali producer in the world

- 2nd largest caustic potash producer in the world

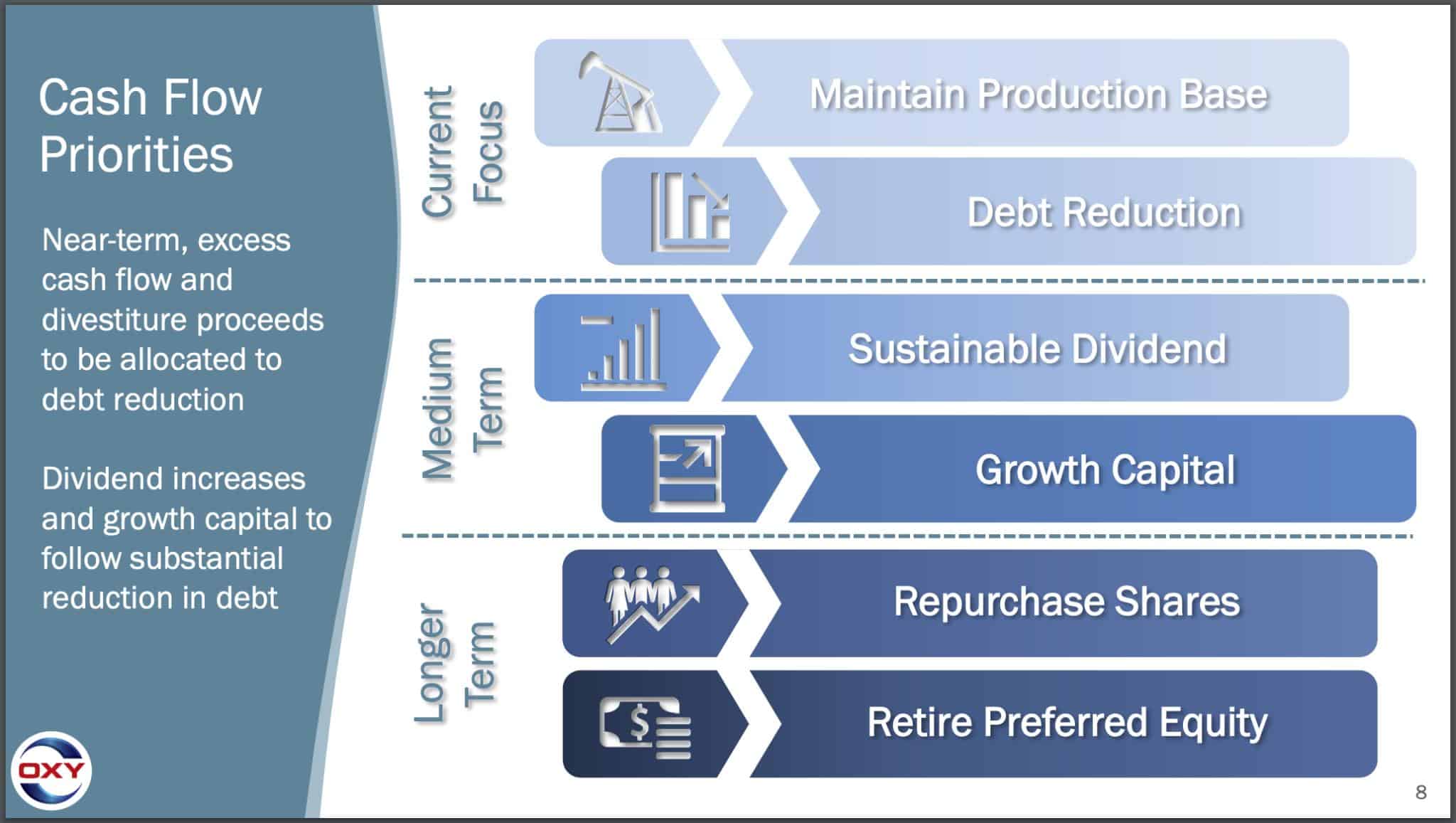

The OXY bet is simple. The company’s cash flow changes ~$215M for every $1 change in oil prices. As long as oil stays above $60/barrel, OXY will generate gobs of cash flow. With that free cash, the company has targeted short, medium, and long-term goals (see slide below):

Currently, OXY’s focused on reducing debt and divesting non-core assets. As of Q1, they’ve sold ~$8.7B in non-core assets. This lightens the balance sheet and generates cash to reduce debt. In addition, OXY’s long-term goals involve repurchasing shares and retiring its preferred equity.

The company’s expecting ~$21B in revenue, ~$10B in EBITDA, and $4B in FCF by 2022. If they hit those figures, it implies a current 7x EV/EBITDA multiple of 14% EBITDA yield. Plus, the chart shows a nice bull wedge with accumulating volume (see below):

Those interested in learning more can read OXY’s Q1 2021 slide deck here.

Helmerich & Payne, Inc. (HP)

H&P is the industry leader in US land drilling with operations in all major US onshore basins, South America, and the Middle East. The company is one of the only drillers with a net cash position on its balance sheet. Plus, it pays a ~4% annual dividend.

H&P solves three crucial pain points for E&P drillers:

- Drilling Rig Provider: H&P offers FlexRig driller, the market leader in drilling fleet

- Directional Service Provider: H&P offers a digital solution to automate decision-making and execution.

- Geosteering: Currently in testing mode

The FlexRig driller is crucial because it’s a plug-and-play solution for any E&P company. There’s one other E&P working on a product like FlexRig, but it would only work with that specific E&P’s wells. H&P’s technology is known as the standard throughout the drilling industry. It helps when you’re a ~100-year-old company.

E&P’s love working with H&P because they generally see four benefits:

- Overall returns and well economics can be improved

- Well productivity over the life-cycle can be improved

- Reduced production costs and field maintenance over well life-cycle

- Predictable, consistent outcomes and costs at reduced financial risk

Yet, the most impressive aspect of H&P’s business model is its balance sheet. The company is net cash positive, almost unheard of in the industry. Moreover, all its long-term debt isn’t due until 2025 while sporting a ~16% total debt-to-capital ratio.

H&P’s performance is tied to the commodity cycle. E&P’s drill when oil prices offer profit margins. Currently, the company is operating at 37% rig capacity with 111 rigs contracted out of the 301 available.

Rising oil prices = rising utilization rates = increased free cash flow. Either way, you’re paying ~2x revenues and ~20x (arguably trough) EBITDA for this business.

Those interested can read the company’s Q1 2021 Investor Presentation here.

Alright, let’s bring it home with financials.

Burry’s Transports Bets: STNG, GOGL, GNK

The final bet Burry made this quarter was buying transports, specifically:

- Scorpio Tankers (STNG)

- Golden Ocean Group Ltd. (GOGL)

- Genco Shipping & Trading (GNK)

Tankers are not buy-and-hold investments. Instead, you buy most extensive when the getting’s good, and exit before daily rates collapse and operating losses skyrocket. Now is one of those times where the getting’s good, and we’re seeing it reflected in tanker stock charts.

Let’s start with STNG.

Scorpio Tankers (STNG)

Everyone knows STNG at this point. It’s the poster-child for tanker stocks, thanks mainly to Harris Kupperman (aka Kuppy). The company transports petroleum products worldwide through its fleet of 135 wholly-owned, chartered-in tankers.

STNG boasts the world’s most extensive product tanker fleet yet sports an average age of 5.2 years per tanker. As a result, a younger fleet can handle more hauls and requires less maintenance capex.

Nikoloas Sismanis wrote a long thesis on Seeking Alpha, which you can read here. Sismanis notes three drivers of future performance (from the article):

1. Historically low order book

“The slower the rate that the global fleet grows (supply) against the (growing) industry demand, the more favorable the pricing power for a big player in the industry such as Scorpio.”

2. ECO fleet will outshine peers

“The company’s young and modern fuel-efficient vessels will benefit given their lower GHG emissions, while older, less efficient vessels may undergo retrofits or be scrapped.”

3. Robust short-term TCE projections

“Management’s TCE guidance remains robust, with rates likely to improve moving forward given the A) season winter uptick from heating oil demand, B) wide NW Europe-Far East naphtha arbitrage and C) conclusion of refinery maintenance which was completed over the last 12 months.”

STNG’s stock chart looks ready to rip, too (see below).

Golden Ocean Group Ltd (GOGL)

GOGL owns and operates dry bulk vessels in the spot and time charter markets and transports bulk commodities, such as ores, coal, grains, and fertilizers. As of today, GOGL had 96 ships in its fleet.

Higher demand for grain and coal means higher TCE rates. And that’s what these tanker bets are all about: TCE breakevens.

GOGL’s thesis is simple. If the company generates a ~$21K – $24K TCE, it’ll do ~$285M to $390M in cash flow. That’s a 22% and 30% yield, respectively. The cash flow gets crazier if you assume January 2021 peak levels ($495M cash flow).

The company also sports industry low cash breakevens. For example, its NewCastleMax and Capesize ships have a $12,860 breakeven while Kamsarmax and Panamax ships do $8,560.

GOGL recently bought 18 new ships for a total of $752M at what looks like an industry trough in Capesize vessel prices.

Besides 2020, GOGL has grown revenues each of the last five years from $188M in 2015 to $610M in 2020 while generating ~30% gross margins/10%+ EBIT margins. The stock currently trades for ~4x NTM sales and 5.6x normalized earnings.

Finally, it’s got a killer monthly chart (see below).

If you want to learn more about the company, check out its latest investor presentation here and write-up from Titsdor Investor Holdings here.

Genco Shipping & Trading (GNK)

GNK is a dry bulk carrier that transports iron ore, coal, grains, steel products, and other dry-bulk cargoes. It charters its vessels primarily to trading houses, including commodities traders,, producers; and government-owned entities.

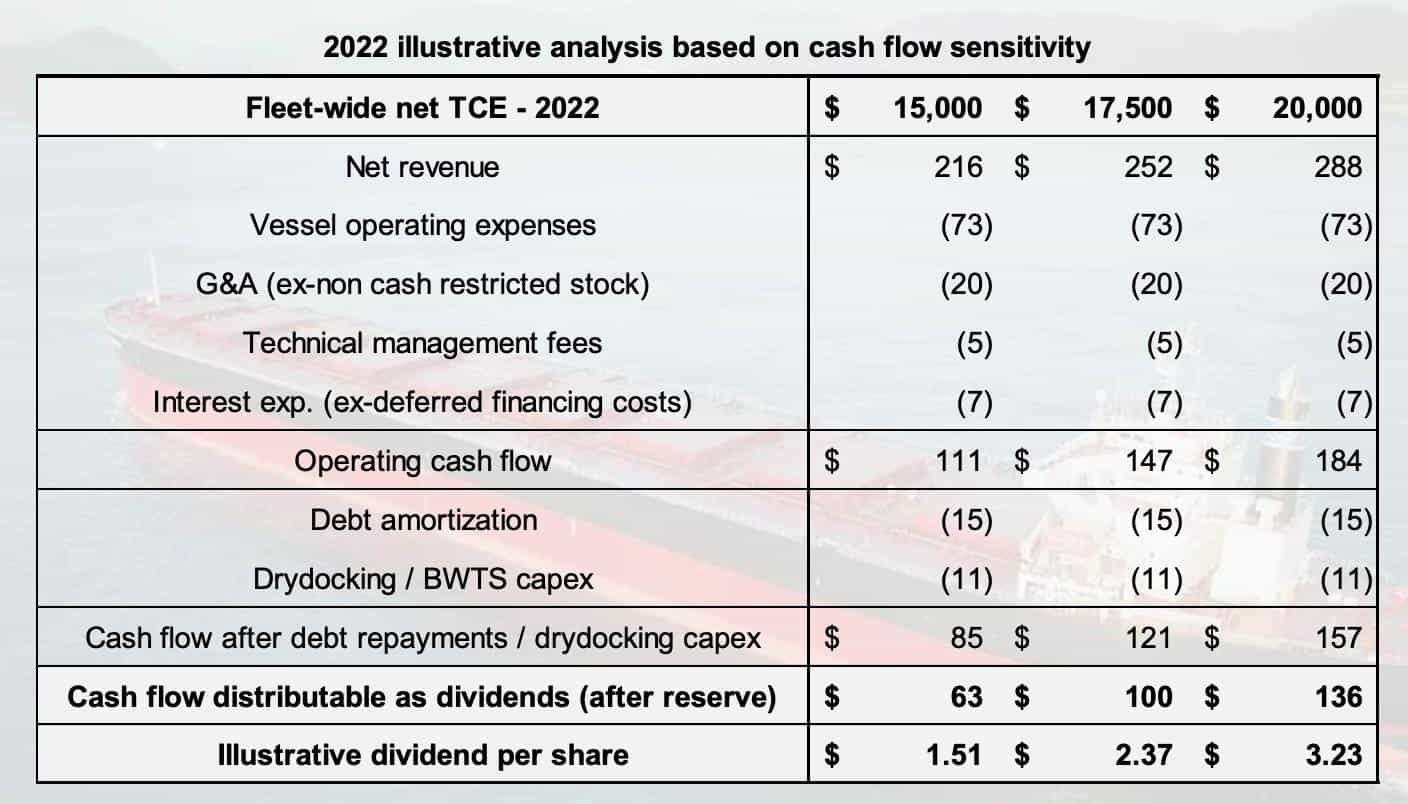

Like the two tankers above, let’s focus on TCE rates and breakevens. GNK is living in its highest TCE rate environment since 2010. The company has ~74% of its Q2 2022 rates fixed at ~$20.7K. Moreover, its Major Bulk vessels are doing $25K per day!

According to GNK’s latest investor presentation, each $1,000 increase in TCE adds ~$14M in EBITDA to the bottom line.

The company plans to do three things with this potential increased cash flow:

- De-lever the balance sheet

- Buy more ships

- Increase the dividend

Here’s how GNK’s revenues and operating cash flows look under three varying TCE assumptions:

The stock currently trades for ~$16/share. If GNK hits the mid-point of its estimate, you’re paying ~7x distributable dividends after debt repayments. That’s a 15% yield.

If you’re interested in learning more, you can read GNK’s latest investor presentation here.

Concluding Thoughts

The goal of this essay is to get you up to speed on the three biggest industry bets in Michael Burry’s portfolio. Think of this as the gateway drug into further research (if you find a name or two you like).

Michael Burry is (and always will be) my investing hero. If there’s one thing this quarter’s 13F taught us, it’s that he’s still buying “ick” names and still drumming to his own beat.