Our Collective members receive new investment ideas every week. Whether its a well-known (but forgotten) large-cap US company or an undiscovered Polish software enterprise. We provide our members with differentiated research on ideas they won’t get elsewhere.

The following is a snippet of our latest equity research on Fever-Tree PLC (FEVR). FEVR is a London-based tonic water and spirits mixer company. We believe it has the potential to generate Monster (MNST) and Celsius (CELH) like returns over the next 3-5 years.

If you’re interested in becoming a Collective member, click the bottom below!

![]()

The Collective is our full-kit soup-to-nuts service that provides research, theory, and a killer community that consists of dedicated traders, investors, and fund managers from around the world. We’ve been told that there’s nothing else like it on the web.

Anyways, here’s our latest write-up on FEVR!

——————–

Fevertree PLC (FEVR) has everything you’d want in a long-term, high conviction bet. The company’s led by its founders who own ~10% of the company. They make a differentiated, premium product in an otherwise forgotten market. They’re growing like a weed in new and existing markets. The balance sheet is one of the strongest I’ve seen. And they generate loads of free cash flow with little maintenance cap-ex required.

Of course, a business like this doesn’t come cheap — at least not often. Investors that scooped shares during the COVID lows sit on a near 2-bagger (200%+ return). Yet despite its rich valuation, FEVR is just getting started in its growth journey. The company’s solidified three key aspects of their business during the last 16 years: brand, distribution, and taste.

These factors will allow FEVR to push new products to market faster than their competitors with greater success. Customers will recognize FEVR’s premium product and (by default) associate their new products with that same stamp of quality. This opens the door for FEVR to attack similar markets like dark spirits, which account for 10x the size of their tonic market debut. In other words, there’s a lot of FCF left to harvest.

FEVR has a path to $700M in revenue and nearly $200M pre-tax operating earnings over the next five years. Getting there means they successfully stave off the (literally) hundreds of competing businesses vying for a seat at the mixer bar. At the current market price, investors can buy FEVR at 5x our 2024 revenue estimate and 18x our pre-tax earnings estimate.

Make Tonic Great Luxury Again

Tim Warrillow and Charles Rolls founded FEVR in 2004. Both men come from beverage/spirits backgrounds. Rolls helped revive Plymouth Gin while Warrillow specialized in luxury food/beverage marketing. Today they own ~10% of the company.

They started FEVR in the British Library while researching the history and ingredients to make a great tonic. The men spared nothing at the expense of finding the perfect ingredients for their tonic water. Their search for the best led to trips to the Congo (for quinine — more on this later) and Ivory Coast (fresh green ginger).

From the very beginning the men focused on quality, not price. Warrillow explains their interaction with local suppliers saying (emphasis mine):

“”And they in turn were excited, because we were going to them and saying ‘look, we are developing a new tonic water, and we want to develop the best. Don’t worry about the price – we just want to get the best ingredients that we can.’ Historically, the only time that anyone had talked to them about tonic was at a supermarket going ‘we want tonic water but we’re only prepared to pay you this amount for it.’ We were looking at it very differently.””

It wasn’t the ingredients that cemented FEVR’s success with customers. It wasn’t even their price point. It was the psychological framing that tonic actually matters when making your favorite cocktail. To many, tonic water is the last thing they think about when making a drink. FEVR wants it first.

Take their slogan: If three quarters of your gin and tonic is the tonic, make sure you use the best.

Rolls understands this given his background in luxury marketing. Take a boring (afterthought) product and create a luxurious appeal backed by the finest ingredients and highest quality manufacturing. Think about Patek Philippe’s watch marketing. The company’s famous “You never actually own a Patek Philippe …” instantly transforms a commodity (watch) into a luxury good (a Philippe watch).

That said I’m not rushing out and begging Bernard Arnault to buy FEVR and add it to his consortium of luxury goods. But FEVR is doing what other tonic companies aren’t: creating a luxury image around their otherwise commodity product.

Your (Bad) Flavor Is FEVR’s Opportunity

Tonic and mixed drinks got by on subpar flavor because nobody challenged the top competitors. Everyone cared about the price of the tonic. To Warrillow and Rolls, this created “an extraordinary gap in the mixer category, specifically tonic water.” The reason? Warrillow explains (emphasis mine):

“Whereas premium spirits had been growing and growing all around the world, and consumers were becoming ever better educated, ever more interested, and paying more money for good-quality spirits.”

In other words, people were willing to pay more for spirits but weren’t given the opportunity to pay more for their tonic. It’s the opposite of Amazon’s approach: go in and undercut everyone’s margins until you’re the last man standing. FEVR’s pitch was “you want to pay more for a better-tasting tonic. We’ll give it to you.”

These subpar flavors and low prices lasted because top producers had no competition. Warrillow explains (emphasis mine):

“The mixer category had remained dominated by one global brand, who had really revelled in the fact that they had no competition for generations. Really the only battle they had been fighting was with the own-labels in the supermarkets, and so they had just spent all their time cost-engineering, with no real regard for quality or flavour. So there we were thinking ‘this is absolutely extraordinary: people are spending more money on a great spirit, yet they have no choice but to drown it in this increasingly artificial mixer.'”

FEVR entered an industry with complacent competition and a differentiated mindset: focus on flavor, not price.

The company’s secret sauce is the use of the ingredient “quinine”. According to FEVR’s website, “Quinine is the key ingredient that creates the gentle bitterness in tonic water.” It’s taken from Cinchona Ledgeriana trees (aka “fever trees”).

During their travels to the Congo, Warrillow and Rolls found one of the only remaining fever tree plantations in the world. It’s this ingredient that distinguishes FEVR’s product. And it’s something competitors have tried to replicate with chemicals, and failed.

The result? 13 years after launching its flagship product (Indian Tonic Water), FEVR is now the premier choice for spirit brands. The company holds 28% share of the UK retail mixer market. This is astounding because FEVR is a premium brand. Not only do they dominate the premium category, they command massive share in all retail mixer spending.

The result? 13 years after launching its flagship product (Indian Tonic Water), FEVR is now the premier choice for spirit brands. The company holds 28% share of the UK retail mixer market. This is astounding because FEVR is a premium brand. Not only do they dominate the premium category, they command massive share in all retail mixer spending.

As I write this FEVR is the #1 best-selling tonic water on Amazon despite a $2+ premium over their next-closest competitor. The reviews are also impressive. FEVR has 4K+ reviews with an average rating of 4.7/5 stars.

Check out one consumer’s review (emphasis mine):

“This is absolutely the best tonic water I have drunk in my entire life. I used to be a great G&T fan in my younger days, but I switched over to gimlets, because something happened to tonic water over the years: It ceased to contain actual quinine. This tonic water has quinine, and that truly makes a difference in the taste. Somehow “commercial” tonics just can’t replace the taste of quinine with their chemicals. I haven’t used it with gin since I found this product (my bottle of Tanqueray ran out sometime ago, and since I still had vodka in the freezer, I used that instead), but the vodka tonics I made were wonderful–and I’m not a big vodka fan. What I was happy to discover is that it tastes good on its own, over ice and with a squeeze of lime. I will be buying this again.”

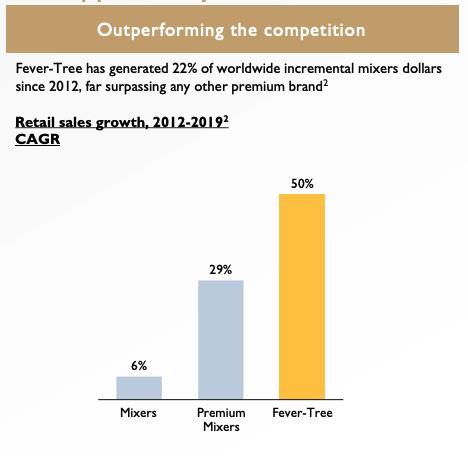

People notice the difference between real quinine and fake chemical copycats. And this difference shows in the company’s sales figures. Since 2012, FEVR has generated 22% of the worldwide incremental mixer dollars.

They’ve sported a 50% retail sales growth CAGR from 2012-2019. During that same time premium mixers did 29% CAGR and regular mixers 6% CAGR.

They’ve sported a 50% retail sales growth CAGR from 2012-2019. During that same time premium mixers did 29% CAGR and regular mixers 6% CAGR.

The company benefits from this growth while charging a premium over its mainstream competitors. In the US for example, FEVR charges $1.29 more per-bottle than their competitors (see on the left).

Let’s dive deeper into their financials.

Narrative To Numbers: FEVR’s Financials

The company splits its sales into four segments (% of sales as of 1H 2020):

- United Kingdom (UK): 46%

- United States (US): 26%

- Europe: 20%

- Rest of World: 8%

In 1H FEVR generated $129M in sales, $60M in Gross Profit and $27M in operating income.

FEVR sells their beverages through on-trade and off-trade channels. Think of on-trade as restaurants, bars, etc. Off-trade comprises online and retail sales (grocery stores, liquor stores, etc.).

Given the COVID lockdowns, FEVR’s UK on-trade sales plummeted 61% YoY. Much of Europe remained on lockdown during 1H 2020, which accounts for ~45% of FEVR’s total European sales. Despite the on-trade woes, FEVR’s off-trade business took off.

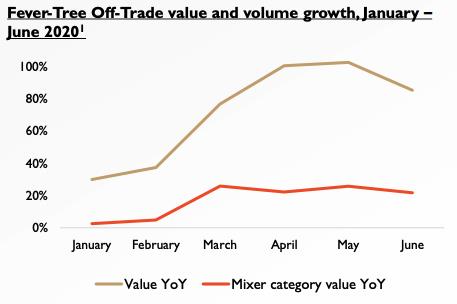

The company grew its off-trade sales in its two largest markets (UK & US) 24% and 30%, respectively. In fact, FEVR’s value and volume growth grew >100% during April and May in the US (see chart on left). And in the UK, FEVR grew its value share 38% and now commands 37.6% UK value share.

The company grew its off-trade sales in its two largest markets (UK & US) 24% and 30%, respectively. In fact, FEVR’s value and volume growth grew >100% during April and May in the US (see chart on left). And in the UK, FEVR grew its value share 38% and now commands 37.6% UK value share.

FEVR is also taking off in its RoW category. The company’s now the largest tonic brand in Canada with 34% value share. And it’s the fastest growing mixer in Australia.

Their European segment also saw massive valeu share gains in Germany, Belgium, Italy and France.

The company’s strategic advantage lies in the strength of its balance sheet. While other mixers and tonic companies shelter and hoard cash, FEVR is spending it to grow their brand. For instance, the company launched its first-ever national TV ad campaign in the UK and introduced new Premium Soda products.

In the US the company launched its own Amazon store-front and introduced its new Sparkling Pink Grapefruit tonic. This increased awareness led to a 73% increase in Google Searches for “Fever-Tree” in the States. They also have distribution agreements with some of the largest retailers in the US: Walmart, Kroger, Target, etc.

FEVR’s Future: Larger Markets & Greater Mindshare

The company made its name in the tonic water space. Yet that accounts for 6% of global premium spirits sales. In other words, FEVR has a long way to go in disrupting the premium spirits market. Their next target: dark spirits. According to Warrillow, dark spirits are 10x the TAM of tonic water.

What’s their plan? Do what they did in tonic water: provide the best-tasting product in a market dominated by price conscious incumbents.

Here’s Warrillow’s thoughts on attacking the new space (emphasis mine):

“The quality of mixers available for these dark spirits is pretty poor and pretty limited,” says Warrillow, “so that’s why we’re quite excited about the development of our dark spirit range, which includes a smoky ginger ale, a spiced orange ginger ale, a ginger beer, a cola, and more. That’s an enormous opportunity. Now we’ve got a brand that I think can really help communicate that message more quickly. And the dark spirit companies are saying, ‘If you’re going to do this, we’d like to work alongside you.”

That last part is important … “Now we’ve got a brand that I think can really help communicate that message more quickly.”

FEVR has built a brand as a premium, great tasting mixer. In turn, the company can leverage its massive distribution network they built creating the best-tasting tonic water to churn out premium dark spirits mixers. It’s not that different from Lamborghini getting into the SUV market. They (Lamborghini) built the brand that it is today. Doing so allows them to create another ancillary product where people assume it’s the best in its class.

The beauty of FEVR’s business is they don’t compete with whiskies, gins or vodkas. They complement those products. That means as long as people keep buying (and paying up) for expensive spirits, FEVR will have a market for their mixer.

It’s also important to note that taste really matters in this business. And FEVR has the best-tasting product on the market. There’s an element of flavor lock-in with FEVR’s products much like customers lock-in to either Coke or Pepsi. I’m not saying FEVR has as good a business as Coke. But once a customer, bar or restaurant finds a product that tastes great and mixes well with drinks, why switch?

This idea — taste lock-in — led me to an interesting podcast with Linda Bartoshuk, PhD. During the podcast, Dr. Bartoshuk explained why our brains love certain tastes. Turns out the brain creates “templates” of flavors and tastes we enjoy. These templates remind us of what we like and guide our preferences over time (emphasis mine):

“Absolutely, and also you learn the mixture sensation. That is one of the beautiful things our brains do is to record information about what we’ve eaten before, and those are saved almost as templates in the brain. So, for example look at bacon. You eat bacon it’s got protein in it it’s got fat in it those are two things that your brain perceives as really good so it’s gonna make you love the flavor that comes with bacon. Now that flavor is actually a composite, it’s a lot of salt, it’s a variety I mean dozens of different volatiles make up the smell and the flavor of bacon. You put those altogether and they produce a template, a certain sensory signature that’s stored in your brain, and the next time you eat bacon you’re gonna recognize it very quickly.”

Given that FEVR’s product quality (and therefore, taste) is significantly better than the competition, consumers who drink FEVR tonics will create templates based on FEVR’s taste. This means FEVR becomes the go-to tonic because consumers know they’ll get the best-tasting, highest quality tonic.

Taste lock-in and a premium product translate to high margins and strong free cash flow. FEVR’s generated (on average) 50% gross margins and 30% EBIT margins. The company’s grown cash from operations at a 33% 5YR CAGR. In turn, FEVR enjoys near 100% free cash flow conversion.

The balance sheet is loaded with $170M in cash against $42M in total liabilities. This allows the company to pay out dividends, which have increased from $1.84M in 2015 to $23.84M in 2019.

Risks, Valuation and Tape Reading

FEVR competes in a very competitive market. The company’s founders have mentioned on various podcasts that there’s >100 competing brands and products. And when you’ve got major brands like KO and KDP with their seemingly unlimited resources, it’s a real threat.

There’s also the risk of revenue growth declining. We’ve seen this in the last three semi-annual reports with revenue growth compressing from 35% to -11.2%. COVID certainly played a role in the last two figures, but it’s worth mentioning given the current valuation.

Finally, a major risk is the company losing its access to its quinine source in the Congo. Saying the Congo is a volatile place to do business is an understatement. Should FEVR lose its only quinine source in the Congo it would lose a vital part of what makes its drinks taste so good.

Despite these risks, we see a path towards $700M in 2024 revenue and nearly $200M in pre-tax cash flow. That would mean FEVR would have to grow revenue (on average) 16% per year while maintaining 27-28% EBIT Margins.

FEVR’s online business will benefit from COVID 3-5 years from now, and it’s on-trade (bars, restaurants) sales should return to normal levels by 2024. That means you can buy FEVR today for 5x 2024 estimated revenues and 18x 2024 pre-tax cash flow.

Finally, FEVR is attempting to breakout of an 18-month long basing pattern (see below):

While we’re hoping for lower prices, we won’t hesitate to take a starter position should the company breakout in the coming weeks.

Concluding Thoughts

Nothing is guaranteed in investing. The only thing we can do is try and tilt the odds of success in our favor. And history tells us it’s a good idea to bet on founder-led companies that make a product people love in a market hemorrhaged with cost-cutting and poor quality. Add to that a business model that prices its product at a premium and generates substantial free cash flow with little maintenance cap-ex.

FEVR is the type of business that tilts the odds of success in our favor.