You can either play the system or you can let the system play you. I like playing the system because it’s more fun and you win more. If you let the system play you, you can get very frustrated and very beat up. ~ Jim Paul, “What I Learned Losing a Million Dollars”

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at the SPX breaking new highs as well as Bear hearts, check in on what the Trifecta Lens is saying, cover a major rare breadth signal and what it means for small-cap performance, pitch the secular macro bull case that no one is talking about, cover Bitcoin stability, excess savings, the beginnings of a commodity bull cycle, and pitch a deep value tobacco stock, plus more…

Let’s dive in.

***click charts to enlarge***

- The SPX closed at new all-time weekly highs last Friday. This puts it above the “Broadening Top” pattern (if you draw thin lines) that the bears have been clutching too like fine pearls. It formed a weekly Doji candle, which is a neutral range bar. And that’s to be expected because as I pointed out to fellow Collective members last week the 3,550-3,600 represents multiple levels of resistance (top of multi-year pattern, upper weekly Bollinger Band, large round number etc…). But this is the price action you want to see if you’re a bull…

- In a world full of noise it pays to reduce complexity and KISS (Keep It Simple Stupid). Our Trifecta Lens Score is a +2 and the market is in a BullQ regime. Both bode well for further upside. The big drag on our TL model is sentiment/positioning, which is at -3 (green line in middle graph).

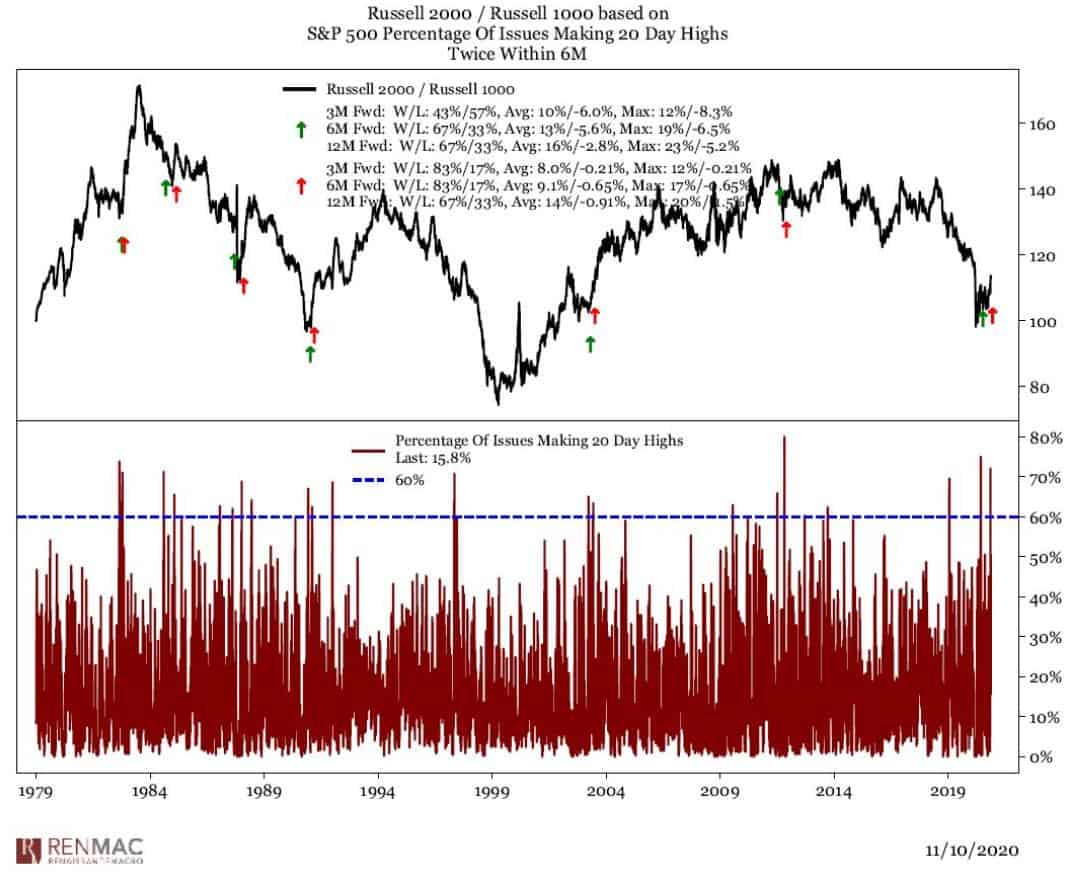

- The deGraaf Thrust Indicator triggers a bullish signal when over 60% of issues make 20-day highs. Last week triggered the second signal in under 6-months and marked only the 10th time in history that this indicator spiked over 70% (h/t to RenMac).

- @RenMac points out that when this signal triggers twice in six months it often marks a turning point in favor of small-cap/large-cap and cyclical/defensive relative performance.

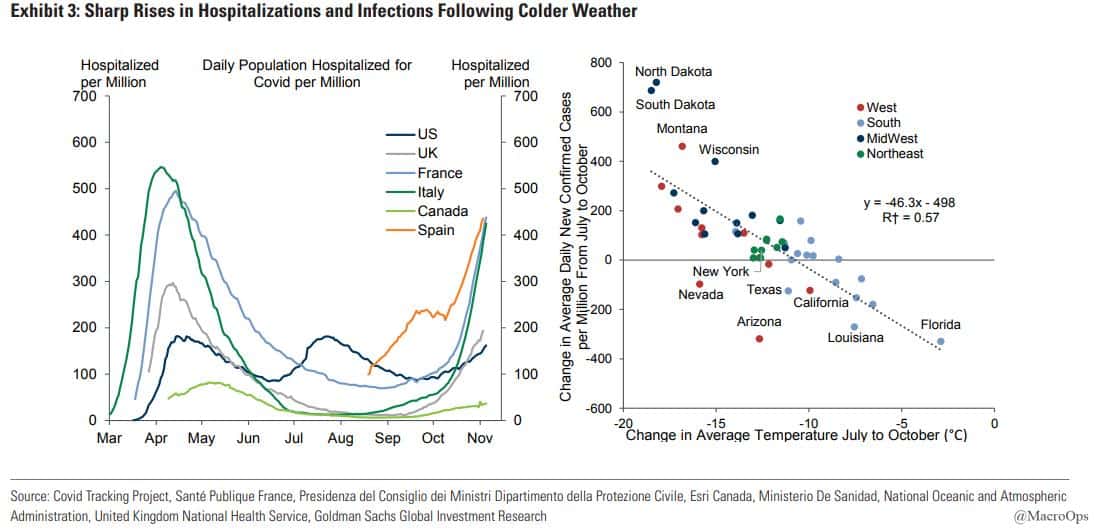

- The near-term bearish case is that the market is setting up to trap the bulls on a false breakout just in time for the COVID narrative to take over in the winter and lead to more shutdowns and a positioning washout. Things are going to get ugly in the coming months as temperatures cool. At the current trajectory, much of the US is set to breach ICU capacity within the next 60 days.

I think that with vaccines and more stimulus on the way the market may be able to look through this. But… it’s certainly a scenario that we have to entertain.

- Analysts continue to set a low hurdle for the market to clear. Jesse Stine shared this earnings estimate graph last week and wrote:

“Banks/Analysts playing major games post Covid. As always, CEO’s and CFO’s have SO many levers to pull to beat estimates. MASSIVE beats in Q2.Into Q3 earnings, analysts expected -20% EPS. Results: +2% lol. Q4 looks like another joke. They may be setting us up for Q1 Biden rug pull.”

- I shared these charts from UBS back in September. They’re part of the compelling longer-term bull case that nobody is talking about, so I figured I’d share them again.

The chart on the left shows the population growth by cohort (35-55 and 65+) on a YoY basis. As you can see, the 35-55 age group is inflecting higher while retiree growth has peaked and is set to rapidly slow. This is important because the younger cohort tends to own more equities as a % of investment versus the 65+ group which is more heavily weighted towards less risky assets.

The chart on the right shows the correlation between the growth difference of the two cohorts (gold line) and the equity risk premium (blue). If this correlation continues to hold then we should see the equity risk premium — which is currently well above its long-term average — narrow significantly. And since the Fed is unlikely to let yields rise, that means higher equity valuations are in order.

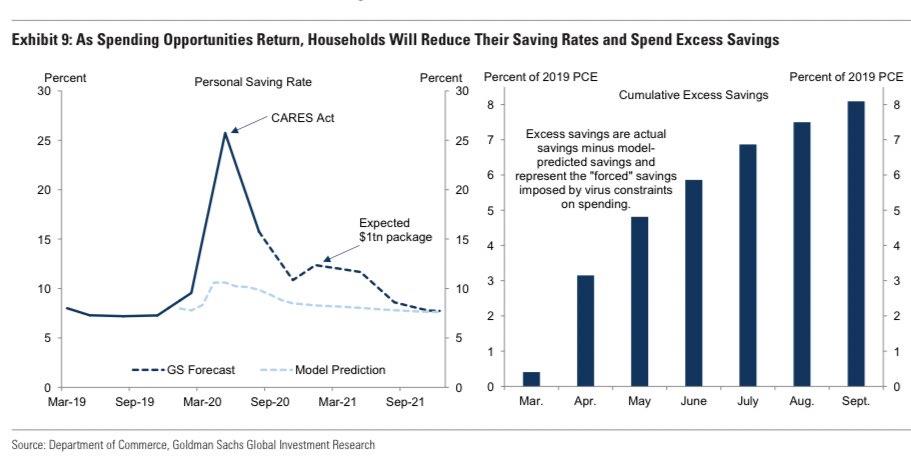

- In addition we have repaired consumer balance sheets and excess savings. The following is from GS, “households are likely to lower their high ‘forced’ saving rates, and to spend down some of the excess savings that accumulated during the pandemic .. We expect this to trigger a mid-year consumption boom that lifts .. annualized GDP growth to +7% in Q2 ” (h/t Carl Quintanilla).

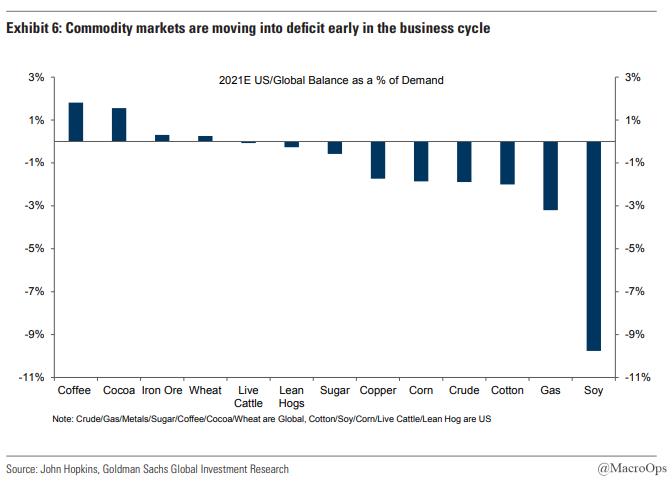

- The reflation-rotation trade may or may not take a breather as the COVID narrative comes back in force. But one way or another it’s going to kick into high gear soon. Capital Cycle dynamics and loads of government money — not to mention Wealth S-curve dynamics — all but ensure it.

Read the following from GS:

“The volatility in commodity markets in recent weeks is a reminder of the damage that lockdowns can do to commodity—especially oil—demand. But what is far less visible is the fact that structural under-investment in commodity-producing sectors over many years has meant that even the faltering recovery so far is generating a deficit in major commodity markets with inventories drawing. Given that inventories are drawing this early in the cycle, we see a new bull cycle for commodities emerging in 2021 as demand recoveries meet restrained supply (Exhibit 6).

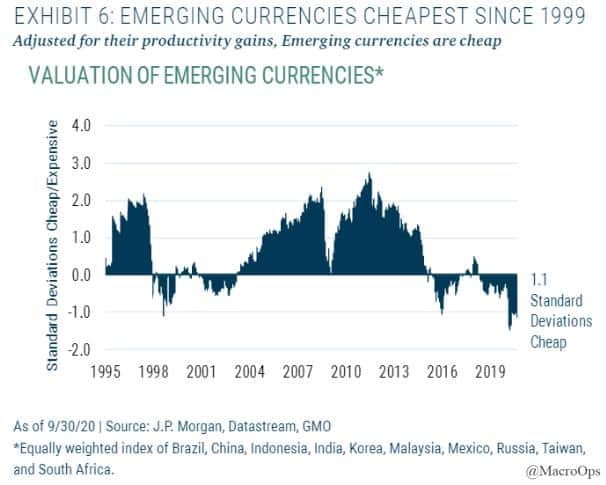

- I keep saying it but I like EM going forward. Its equities and FX are dirt cheap as GMO points out in its latest report (link here). MXN is still my favorite.

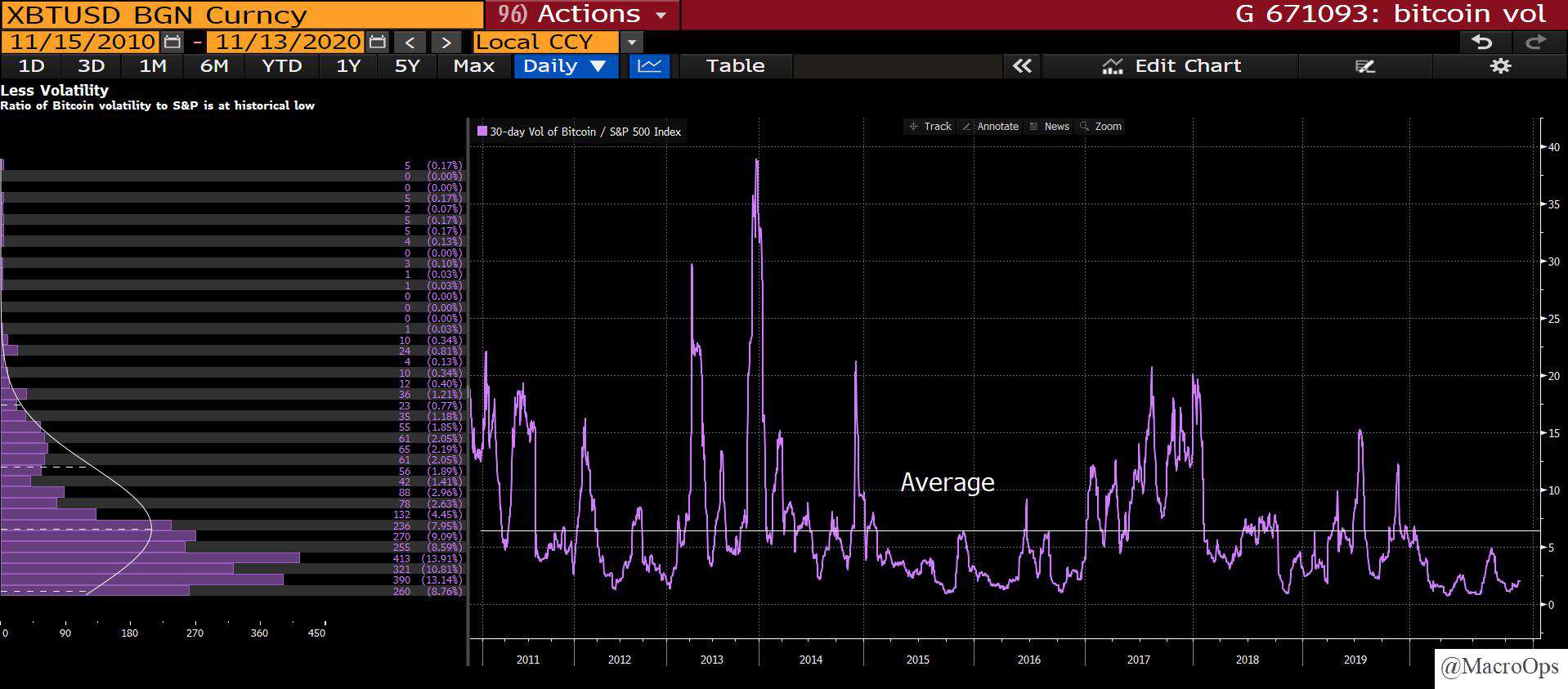

- I’ve been writing for months now that the new bull market in Bitcoin is going to be driven by institutions and not retail. This is important because it means much steadier hands as well as deeper pockets.

Ye Xie, writing for Bloomberg last week, made some key points, noting “Billionaire investor Stanley Druckenmiller explained this week why he owned some bitcoin in an interview with CNBC:

‘Bitcoin could be an asset class that has a lot of attraction as a store of value to both millennials and the new West Coast money — and, as you know, they got a lot of it. It’s been around 13-years and with each passing day it picks up more of its stabilization as a brand.’

“What’s interesting is that the volatility of Bitcoin relative to the S&P 500 has dropped to historical lows this year, one of the most tumultuous periods in recent memory.”

Interesting indeed…

- I love plays that have multiple positive drivers. Tobacco company, Altria Group (MO), fits this bill.

We’re in a macro environment that is slowly going to start favoring the value space (finally!). MO is a stalwart with an iron-clad balance sheet that trades at 9x FCF, has an 8.5% divvy, and is in an industry that has the best long-term track record. Also, the technicals are cherry with the stock bouncing off its 200-month moving average (blue line). A level that has acted as a support every time in the past. And it’s put in a large double-bottom. It might be time to take a puff…

Two Roads Diverged In A Wood And I – I Took The One Less Traveled By, And That Has Made All The Difference. ~ Robert Frost

Stay safe out there and keep your head on a swivel.