A trick to get a sense of the overall level of bullishness is to ask who the burden of proof is on. If you pitch an idea, do other investors take your side immediately, or do they require evidence that your view is correct? If the answer is the latter, your idea is probably off-consensus.

~ Michael Fritzell, “Long-term Front-Running”

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at the increasing normalization of political violence, discuss why so-called “zombie” companies are back near all-time highs in the US. We then dive into data showing we’re about to enter one of the largest global restocking cycles ever, check out some charts showing rising global growth, improving COVID numbers, Bond VIX at record lows, a dem sweep this November, and end with a reup of a long stock pitch, plus more…

Let’s dive in.

***click charts to enlarge***

- This is the most concerning graphic I’ve come across in recent memory. Politico writes that “Among Americans who identify as Democrat or Republican, 1 in 3 now believe that violence could be justified to advance their parties’ political goals—a substantial increase over the last three years… In September, 44 percent of Republicans and 41 percent of Democrats said there would be at least “a little” justification for violence if the other party’s nominee wins the election.”

“Our frustration is greater when we have much and want more than when we have nothing and want some. We are less dissatisfied when we lack many things than when we seem to lack but one thing.” ~ Eric Hoffer, “The True Believer”

- Victor Schvets explains in his book “The Great Rupture” that this widening societal chasm is being driven by “technological changes on the one side and our dangerous addiction to debt on the other.” A dangerous coupling he calls the “Fujiwara impact (two hurricanes merging and reinforcing each other)”.

The below chart shows that 15% of US public companies can now be classified as zombies — companies where profits are less than the interest paid on their debts for at least 3-years (chart via the FT). Another symptom of a multi-decade debt binge (long-term debt cycle).

- While the above is disheartening we need to disconnect that part of our psychology when analyzing the broader market, since the market moves off of liquidity and relative values (stocks versus bonds). And the outlook for short-term economic growth and the stock market itself, remains quite bullish

Below is a chart from Jefferies showing that we’re in for a massive inventory restocking cycle. Jefferies writes:

-

- The surge in U.S. retail and housing demand has pushed inventories in these sectors to record lows.

- Manufacturing inventories are not yet at an extreme, but will likely decline further once retailers and home builders ramp up their orders.

- At the same time, businesses appear to be shifting from “just in time” to “Just in case” inventory management, which points to structurally higher l/S ratios going forward.

- All of this is likely to create the biggest restocking cycle on record. We expect inventory rebuilding to add considerably to growth over the next 2-3 quarters, creating a long tailwind for mfg activity and global trade.

- Goldman Sachs’ Global Leading Current Activity Index has rebounded to its highest levels since February 2018.

It behooves us to remember that right before COVID hit the world (excl. US) was coming out of a long and painful recession. The excess (again, excl. the US) has long been wrung out from the system. This, combined with the backdrop of record low rates, easy liquidity, and mounting fiscal stimulus, provides a very favorable backdrop for risk assets.

- More evidence of a sharp rebound in global growth. Korean exports (a strong leading indicator of Global EPS growth) are at their highest YoY point since Oct of 18’ and US New Orders/Inventory ratio just hit a 10-year high…

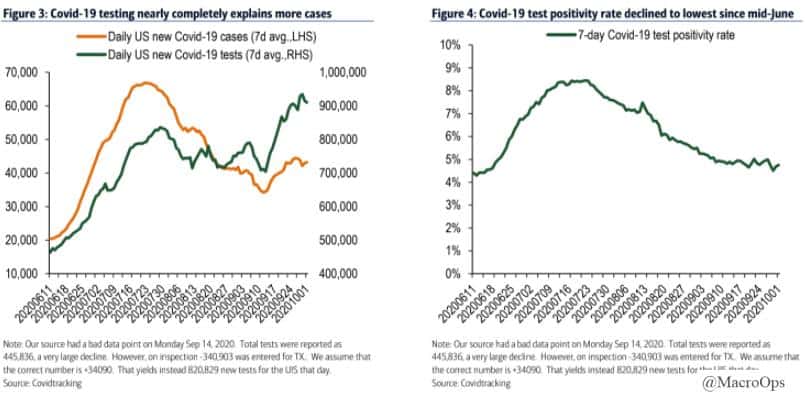

- If your one of the unfortunates who are glued to the news 24/7 you’d think we’re in for another devastating second wave of COVID cases this winter. But, the data continues to suggest that’s not going to be the case and that some level of herd immunity is establishing itself.

This chart from BofA shows that the European countries who were most severly affected by COVID early this Spring are largely being spared now, and vice-versa.

- In addition, rising cases in the US can entirely be explained by more comprehensive testing. Both the test positivity rate, hospitalizations, and deaths continue to trend lower.

- In the hierarchy of markets, credit sits near the top. Credit leads equities, so it pays to pay attention to the commercial bond space. On that note, BofA pointed out in a recent report that we’ve seen $18bn in net upgrades over the past two weeks compared to $538bn in downgrades in late March/early April.

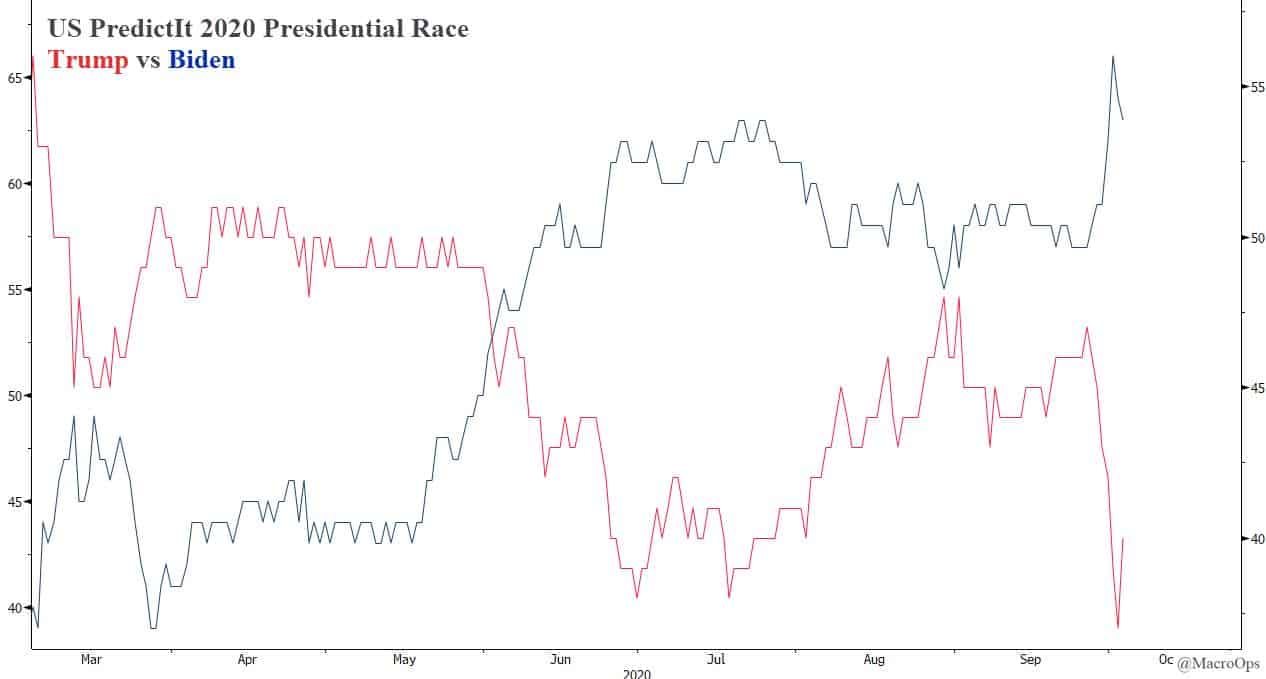

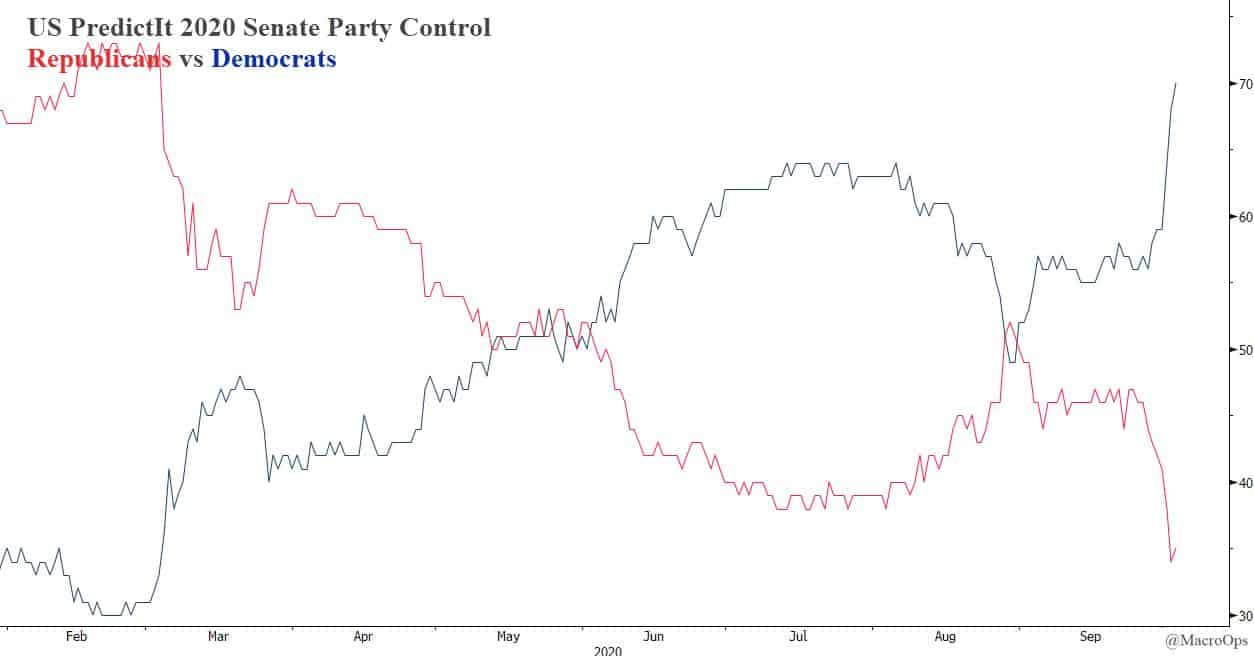

- I made a political prediction in a Market Note sent to fellow Collective members over the weekend. I’m predicting a Biden/Dem sweep this year. The reason is basic demographic and eligible voter pop numbers, plus a few other key things. According to the betting market, this isn’t a contrarian take. PredictIt is pricing in a blue wave…

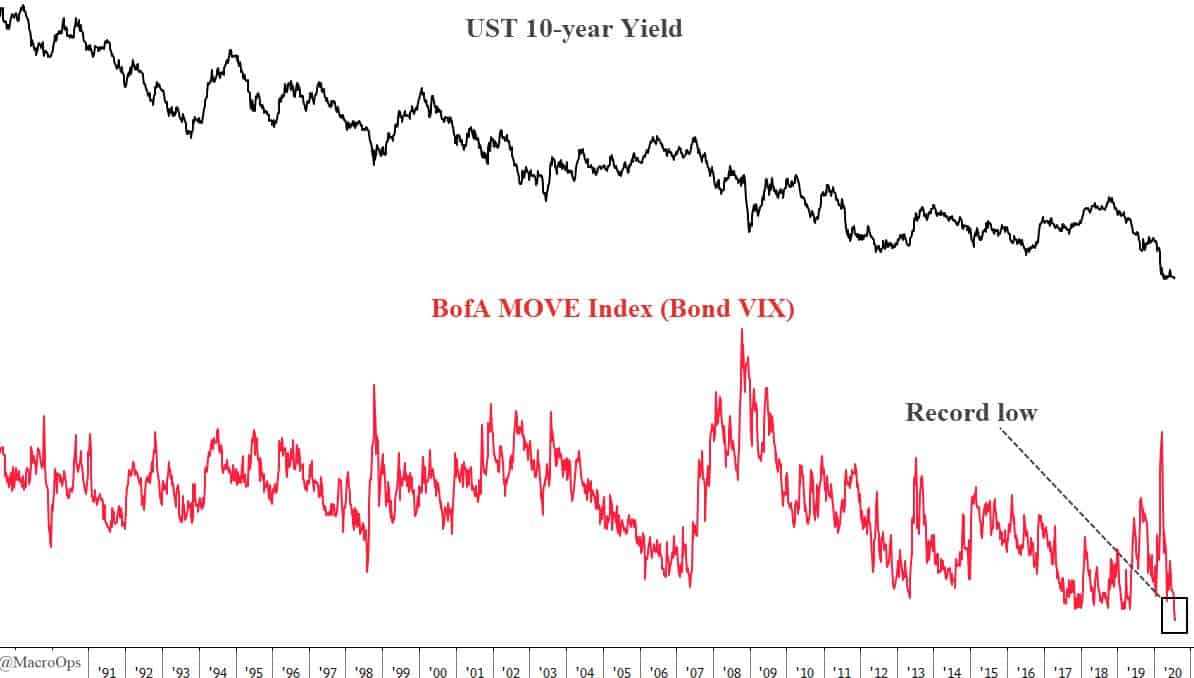

- I find this interesting… On the backdrop of rising political disunity, rebounding growth, improving COVID data, and high odds of a dem sweep, we find bond volatility at an all-time record low.

Now I know that’s largely due to expectations set by the Fed. But, you gotta think we at least see somewhat of a bear steepener play out here. Especially if we get a CARES 2 deal done soon…something I think is very likely.

- Very few will probably notice but the Nikkei 500 just hit an all-time high.

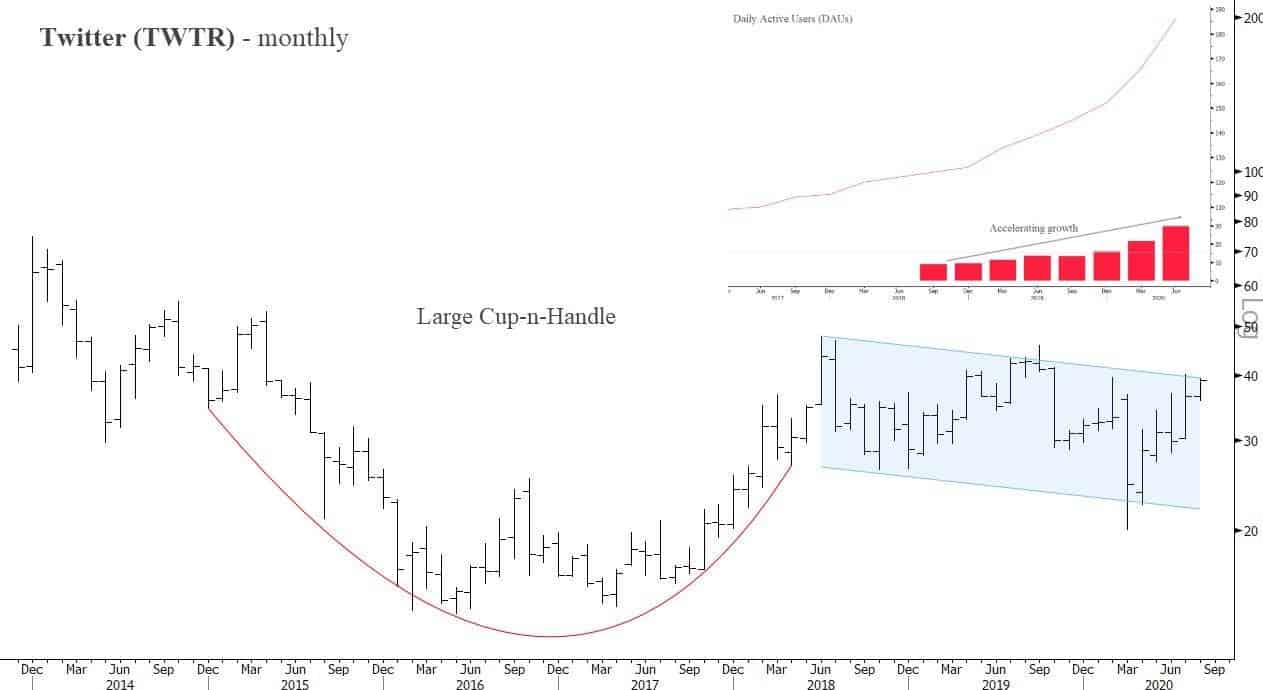

- Back in August I shared the below chart of Twitter (TWTR) on a monthly basis forming a massive cup-n-handle. Well, it has since broken out. We’ll be sending out a note later today to Collective members alerting a DOTM trade we’re putting on. Keep an eye out for that!

Stay safe out there and keep your head on a swivel.