Every quarter I like to scan through the latest 13F filings of my favorite value investors. While I don’t closet-index their portfolios, I sometimes use their ideas as springboards for further research into areas that interest me. Every now and then I’ll invest in something only to find out there’s other big name investors buying the stock as well. Fox Corporation (FOX) is a recent example of this.

According to his latest 13F, Seth Klarman has around 12% of his fund in FOX. The fund’s investment is split between FOX and FOXA shares. Let’s see what Klarman likes about the business.

Disclosure: I am long FOX around $32/share

Company Background

FOX was spun-off from 21st Century Fox in March of 2019. The company began its journey as a public company at around $40/share. Due to spin-off selling dynamics, the stock dropped ~25% to below $30/share. Mr. Market has FOX wrong at the current price.

The thesis is simple. FOX is a great business that generates billions in free cash flow and has one of the best captive audiences in the game. The company’s run by incentivized management and generates most of its revenue from live events (sporting / politics). There’s little debt, loads of cash and hidden assets (NOLs). At today’s market price, you can buy FOX’s core operations for 9x EBITDA while getting their entire TV station line-up for free.

A Baby Out With the Bathwater

Cord-cutting is all the rage. Subscription TV packages are the future. Nobody cares about cable anymore. While that may be true for most television content, it’s not so when it comes to live events.

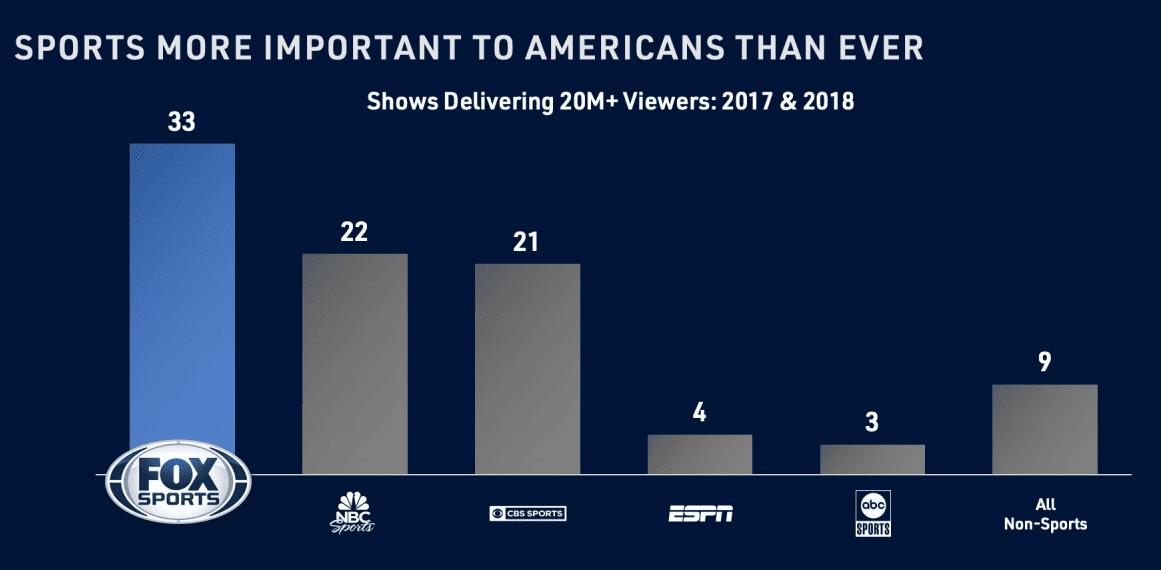

FOX’s assets are centered around real-time, live news and sporting events. These are events where you want to watch as it’s happening. You want to be in the know. While advertising impressions have declined for pre-programmed shows, live-event advertising remains strong. Check out the graph from FOX’s investor slide deck:

A key question to ask ourselves at this point is, “Will sports be as relevant 20 years from now as they are today?” I think the answer is yes. In fact, 88% of the top 100 telecasts nationally are sports related. This is up from 25% in 1998. FOX also delivers more sports content than any other provider. They have 33 shows that deliver 20M+ viewers annually. The next closest is NBC Sports with 22 shows.

The company’s secured rights for every aspect of their sports content through at least 2022. MLB and FIFA are locked in till 2028 and 2026 respectively. There’s a long runway for growth within the FOX Sports segment of their business.

Die-Hard, Captive Political Audience

Whatever your political leanings, it’s impossible to refute FOX News’ industry dominance. The FOX News bundle (which also encompasses FOX Business) reaches 200M+ people every month. It’s not just their reach, but the cult-like following with which their viewers stay glued. Almost everyone has that one grandparent that only watches FOX News.

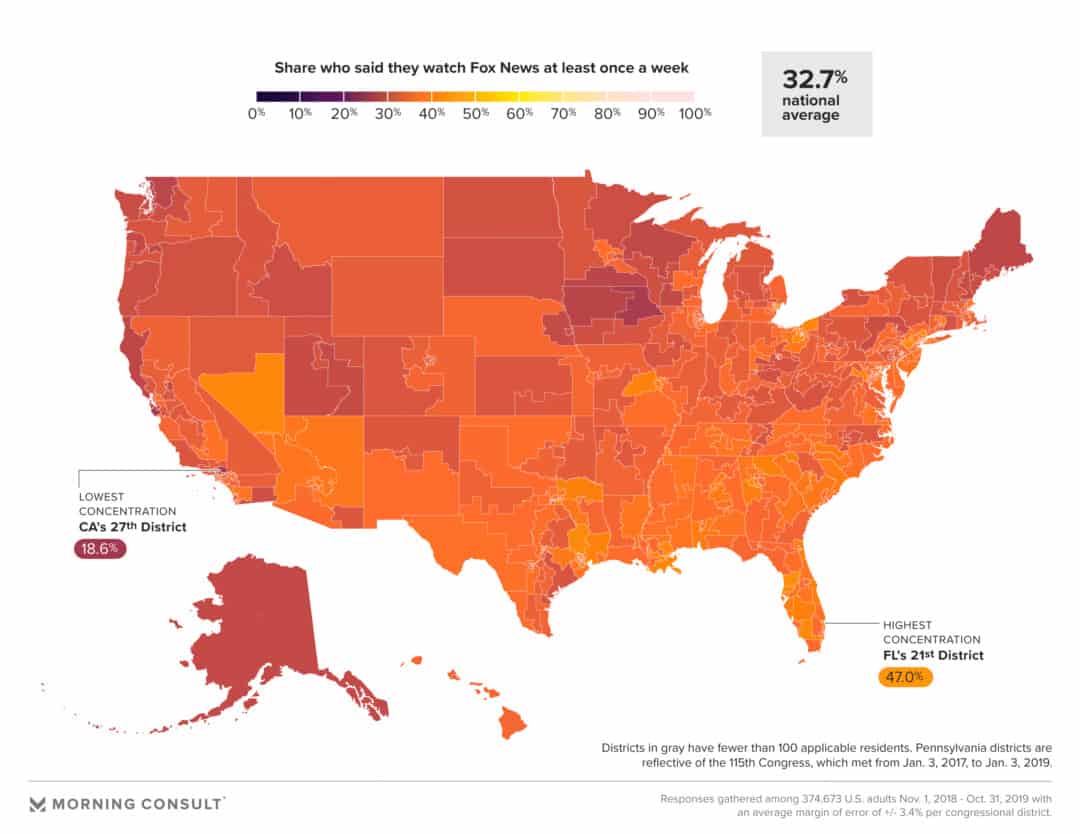

As of 2018, FOX News achieved 17 consecutive years of owning the #1 spot for primetime and total day viewership. What’s also interesting is FOX News leads in demographic areas that are contrast to it’s right-leaning bias. Check out the map on the right:

As of 2018, FOX News achieved 17 consecutive years of owning the #1 spot for primetime and total day viewership. What’s also interesting is FOX News leads in demographic areas that are contrast to it’s right-leaning bias. Check out the map on the right:

The big catalyst for FOX News’ growth and captivity is their perceived level of trust within the community. According to a Brand Keys Research Study, 87% of those polls said they trusted FOX News. This beat out PBS at 86%. Also, a 2016 USA Today poll found that 26% of people surveyed trust FOX News as a news source.

What’s The Point? Brand Loyalty & Advertising Dollars

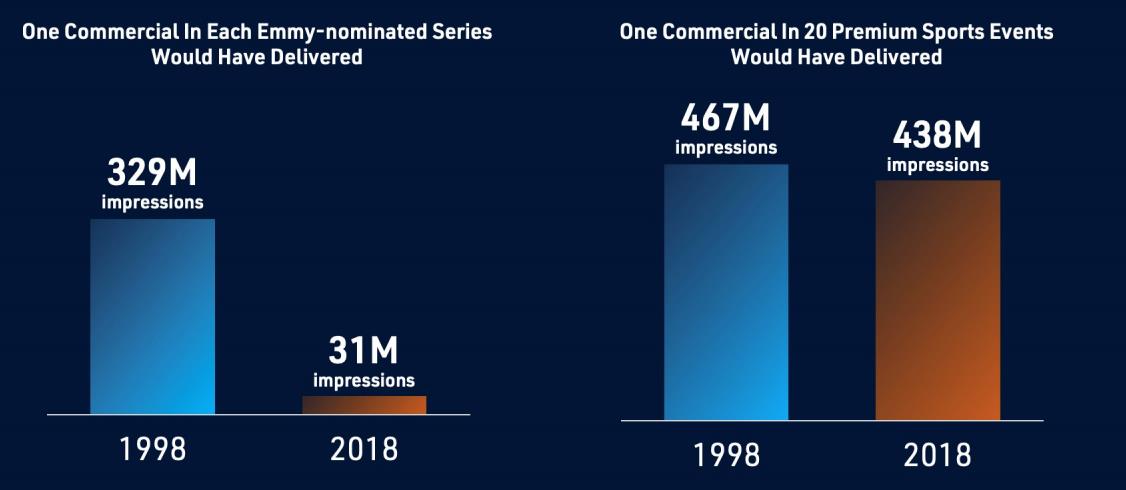

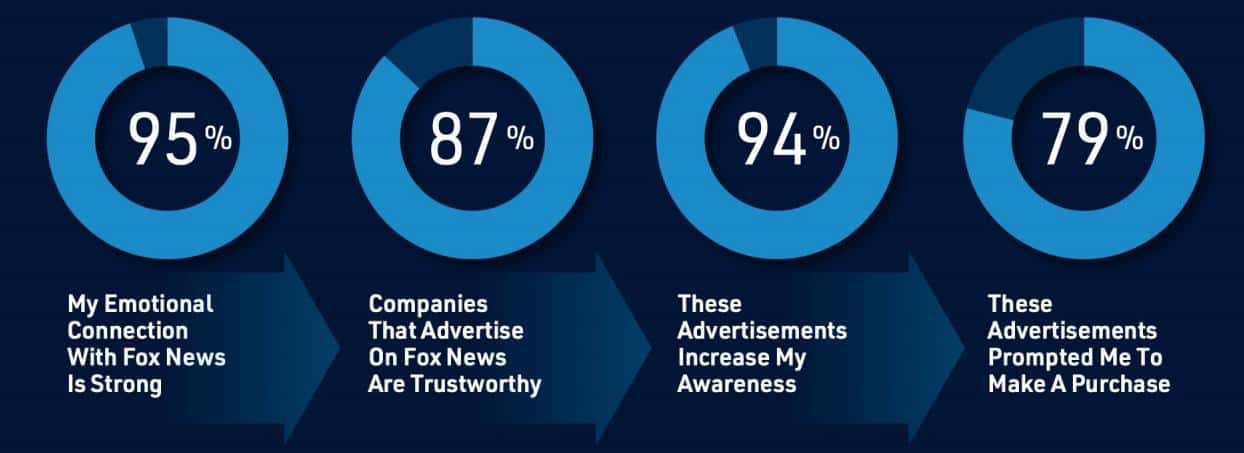

When it comes to bang-for-your-buck advertising spend, it’s tough to beat FOX’s audience. The slide below reveals FOX’s largest competitive advantage:

An emotional connection is impossible to quantify, but it’s one of the strongest moats for news stations.

This moat — a deep, emotional connection — can’t be bought, either. Even if you give someone $20B (FOX market cap) to try and replicate that connection, you’ll fail. These connections take decades to build.

You don’t get a similar emotional connection from CBS, PBS or ESPN. CNN is the closest competitor when it comes to emotional connection. Yet despite being the closest competitor, CNN’s trust rating is 12%.

Turning Emotions into Profit

FOX generated over $10B in revenue in 2018 and did $11.3B in 2019. EBITDA came in at $2.38B and $2.64B respectively. That’s a 23% EBITDA margin! The company also generates close to $2.4B in annual FCF. At current market price that’s a 13% FCF yield.

Mr. Market is currently valuing the company’s cable business — arguably the best cable business in the world — at a little over 9x EBITDA. 9x EBITDA for FOX’s cable assets is attractive enough on its own merit. But with owning FOX stock, you get a lot more. The company also operates 28 TV stations across the United States.

These TV stations generate over $470M in annual EBITDA. At $32/share, the market’s valuing all 28 TV stations at $0. So 9x EBITDA bought you the cable business, giving you 28 cash-flowing TV stations for free. Plus, FOX’s cable assets are more resistant to the cord-cutting/streaming service. That’s not a bad deal.

The Next Five Years

FOX is well positioned to grow revenues and EBITDA over the next five years. I don’t see their audience losing the emotional connection. And with the 2020 Presidential Campaign heating up, TV ad revenues should shoot through the roof. If the company grows it’s top-line at a modest 5% annually over the next five years, you’re looking at over $14.5B in revenues and $3.4B in EBITDA.

If we apply a 15x multiple on 2023 EBITDA, which doesn’t seem like a stretch given the brand power of their assets, we get around $56/share. That’s nearly 70% upside from current prices.

Strong Balance Sheet with Hidden Asset

Unlike most spin-offs, FOX isn’t saddled with a mountain of debt. They have $19B in current assets ($2.5B of liquid cash) and only $6.7B in borrowings. Most of that debt isn’t due until after 2029.

FOX also has over $4B in hidden assets in the form of deferred tax credits. The company deferred close to $400M in income in 2019. At that rate, FOXs deferred assets should last up to ten years.

Risks

There are things not to like about FOX. The Murdochs pay themselves hefty compensation packages (most of which are through stock rewards). There’s also some share class structure that prevent shareholders from engaging in activism with Rupert Murdoch owning most of the voting-power Class B shares. And we can’t forget the cord-cutting bonanza that’s sent most cable stocks plummeting (I’m looking at you, CBS).

It’s investments like FOX that make me think about my favorite Joel Greeblatt quote:

“My biggest positions aren’t in companies that I think I’ll make the most money on. They’re in the companies where I don’t think I’ll lose money on.”

The current price (9x 2019 EBITDA), strong balance sheet ($3B in cash vs. $6B in LT debt), healthy cash flow ($2.4B) and incentivized management give us confidence that our odds of losing money with FOX are low.