“If there’s one thing I’ve learned from interviewing 25+ CEOs and operators, it’s this: culture, incentives, and management teams really matter.”

Ben Claremon is the portfolio manager at Cove Street Capital and hosts one of my favorite investing podcasts, The Compounders Podcast (listen here). Ben spends his time reading, thinking, interviewing, and investing in the world’s best “Compounders”. These are companies that consistently generate above-average returns on capital for decades.

I picked Ben’s brain for 90 minutes on topics like:

- The most impressive CEO Ben’s interviewed

- Lessons from hosting The Compounders Podcast

- Ben’s Proprietary Management Assessment Framework

- Profitability vs. Growth

Ben is in the spotlight for this week’s 3 Big Things (3BT).

3BT distills my podcast episodes into bite-sized summaries. Each piece features:

- One Conversation (Stocks, Psychology, Markets)

- One Framework (Mental Model, Analytical, Behavioral)

- One Idea (Long or Short)

Alright, let’s dig into my podcast with Ben Claremon.

One Conversation: Building The Ultimate Company

I asked Ben to build his “Ultimate” company. It’s the investor’s version of creating your own player in Madden or FIFA.

Check out his answer below.

- Industry: Manufacturing

- Business Description: Makes and sells mission-critical, small component pieces of a customer’s larger cost structure. Ideally, these parts are so vital they become embedded into the end product’s specification requirements. (Note: reminds me of Hidden Champions, one of my favorite business books)

- CEO/Founder: Alan McKim (CEO of Clean Harbors), Joey Levin (CEO of IAC), or Ben Gliklich (CEO of Element Solutions)

- Board Structure: Mostly independent board with an independent director

- Compensation: Not egregious

- Tenure: Yearly elections

- Prefer a Strategic Committee (exclusively focused on expanding moats)

- Compensation

- Short-term: Tied to growth rates and margins

- Long-term: 50% RSUs 3-4 year vesting / 50% ROIC or Total Shareholder Returns

- Insider Ownership: 5% or more (10% or more gets really exciting)

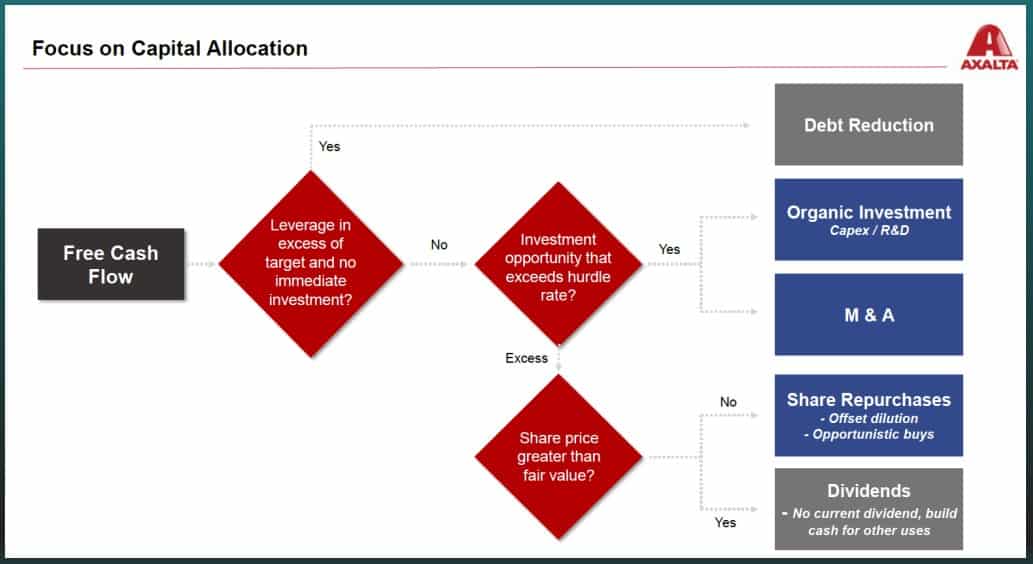

- Capital Allocation: Judicious (cautious, even) on “transformative” M&A deals and opportunistic use of buybacks/special dividends (not mechanical)

- Industry Structure: Either highly fragmented or highly concentrated (middle-ground is no-man’s-land)

Ben loved this exercise because it allowed him to see which investments in his portfolio most closely resemble his “ideal” company.

What would your “Ultimate Company” look like?

One Framework: Ben’s Proprietary Management Assessment

Ben developed a Management Assessment Framework in 2019. You can download the 58-slide PDF deck here.

Cove Street distilled the Framework into seven key components, which we’ll share below. We’ll also include a few bullets on why they matter.

Compensation & proxy statement analysis

Compensation and the proxy statement reveal critical information about management motivations and incentives. For example, it answers questions like:

- What is the company’s long-term bonus measurement?

- How much stock do insiders and the board of directors own?

- Is management incentivized to grow revenues, expand margins, or increase market share?

- How much of the CEO’s compensation is tied to stock price performance?

The goal is to answer the question: how aligned is the management team with common shareholders?

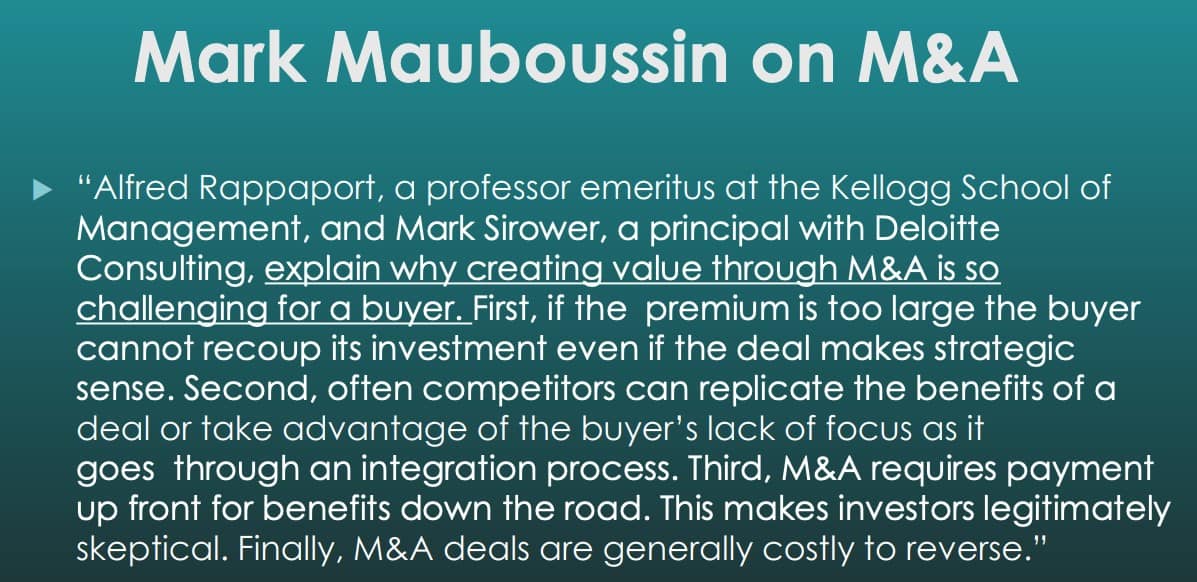

Scrutinizing prior M&A

Empirical data shows that most of the value in an M&A deal goes to the seller. That’s a harsh reality for any CEO to overcome.

And for CEOs with a history of M&A deal-making, a ruthless examination of prior deals allows an investor to answer the following questions:

- How did previous deals impact FCF, ROIC, and margins?

- How diversified did the company’s revenue stream become?

- What types of deals were they (roll-ups, bolt-ons, tuck-ins, etc.)

- What happened to organic revenue growth post-deal?

- What were the average multiples paid for the acquisitions?

Finally, investors should question any deal from a management team with no history of M&A. That’s usually a sign that management is hiding slowing (or decelerating) revenue growth.

Buyback and dividend policies

The most critical factor for buybacks and dividends is frequency. Does management set arbitrary (read: mechanical) buyback policies regardless of valuation?

Additionally, does management give any thought to dividend policy? Or is it a flat rate anchored to GDP growth?

More mechanical policies mean less deliberate thought on capital allocation.

Search for management teams that aggressively buy back stock at depressed prices, sell stock at elevated prices, and/or issue special dividends when they have excess cash.

Tracking management objectives (TMO)

Does management set and hit stated goals or objectives? If so, it’s a good indicator that they understand the business deeply.

However, monitor the goals and objectives. Are they big, hairy, and audacious enough? Overly conservative plans are worthless (“we want to grow at GDP rate.”). But so are unreasonable objectives like “we produced 100 units this year, and our goal is to produce 10,000 units next year.”

Ultimately, you’re looking for consistency. A management team that does what it says it will do.

Does management talk the talk?

One of Ben’s signals for management is the language they use to discuss capital allocation and business strategy.

For example, Ben wants to hear “buzzword” phrases like: “Return on invested capital (ROIC),” “Creating Shareholder Value”, “Hurdle rate,” “Long-term,” etc.

Then check if management is incentivized to improve on these metrics (our first criteria).

Insider transactions

Nobody knows the inner workings of a company better than its management team. How do their insider transactions reflect that reality?

Are insiders hoarding shares like they’re Charmin during COVID? Or are they aggressively selling at elevated valuations?

Regardless of the signal (buy or sale), consider it with that person’s net worth. There’s zero signal in a $100M net worth CEO buying $100K worth of stock. But if a founder worth $100M buys $10M worth of stock on the open market? Take notice.

Generally, open market purchases have more substantial “signal” power than stock option awards/grants.

What has the stock done?

Investors will always judge a management team (or CEO/founder) by the total shareholder return during her tenure.

Check the five-year shareholder return on any new investment. How has management performed during that time? Have they beaten the index? If so, by how much? And if not, how significant is their underperformance? And is that underperformance industry or company-specific?

Caveat here. Any timeframe before five years is too soon to judge the quality of a management team’s decision-making abilities.

One Idea: Element Solutions ($ESI)

Element Solutions (ESI) is a global specialty chemicals company. ESI sells chemicals and materials for various electronics hardware and industrial applications. You can learn more about the company here.

ESI’s management team, mainly its CEO Ben Gliklich, drove Cove Street’s initial interest. Ben (from Cove Street) highlighted his impressions of management during the podcast (emphasis mine):

“I found his comments on how he’s building a culture to be really compelling. ESI has these five C’s: challenge, commit, collaborate, choose, and care.

The way he constructed those five C’s is incredible. He inherited this company which was a former Ackman SPAC. The company was not in good shape financially when he took the job, and the culture at that time wasn’t healthy.

Since then, he’s built a high-performing organization innovating for customers and successfully acquiring other businesses.

He felt like someone that had been running this business for 30+ years, even though he’s 38 years old.”

Gliklich became CEO in 2020, so it’s too early to gauge the value of his decisions. However, there are a couple of operational improvements to note since he took the role:

- Reduced average Cash Conversion Cycle from 112 days to 103 days

- Reduced Days Sales Outstanding from 76 to 69

However, as Claremon noted, most of the company’s improvements are qualitative (like culture). Things you can’t see on a balance sheet or income statement.

Wrapping Up: Where To Learn More

Thanks for reading, and I hope you learned something. Check out these resources if you want to learn more about Ben, his Investment newsletter, other podcasts, etc.:

- Ben Claremon on Twitter

- Cove Street Capital Website

- The Compounders Podcast

- Ben Claremon Podcast Appearances outside Value Hive (here)