This week, we have Part 2 of our Portfolio Update.

We cover precious metals, Intermap Technologies (IMP), ClearPoint Neuro (CLPT), and two more miners (Andean Precious Metals and Fenix Resources).

Like the prior report, we discuss strategies for adding to current positions, stop-loss rationalizations, and notional size goals.

Check out Part 1 of my Portfolio Update series here if you haven’t already. I discuss oil (futures and VLE), our war/Trump hedge (RHM), and our two favorite mining stocks (IDR and NICU).

One last thing (I promise!).

I want to let you know about our Macro Ops Collective.

The Collective is the most unique group of traders, investors, and entrepreneurs on the Internet. Our central goal is to become consistently profitable in any market regime while having a ton of fun.

The MO portfolio officially closed the year with a +50.4% return. We’ll soon publish our year-end review, discussing our painful mistakes and total blunders, what we’ve learned, and what we’ll try to do better in the year ahead. So keep an eye out for that.

If you’d like to join our Collective as we tackle 2025 head-on, click here.

Let’s get after it.

Precious Metals: The Spice Must Flow

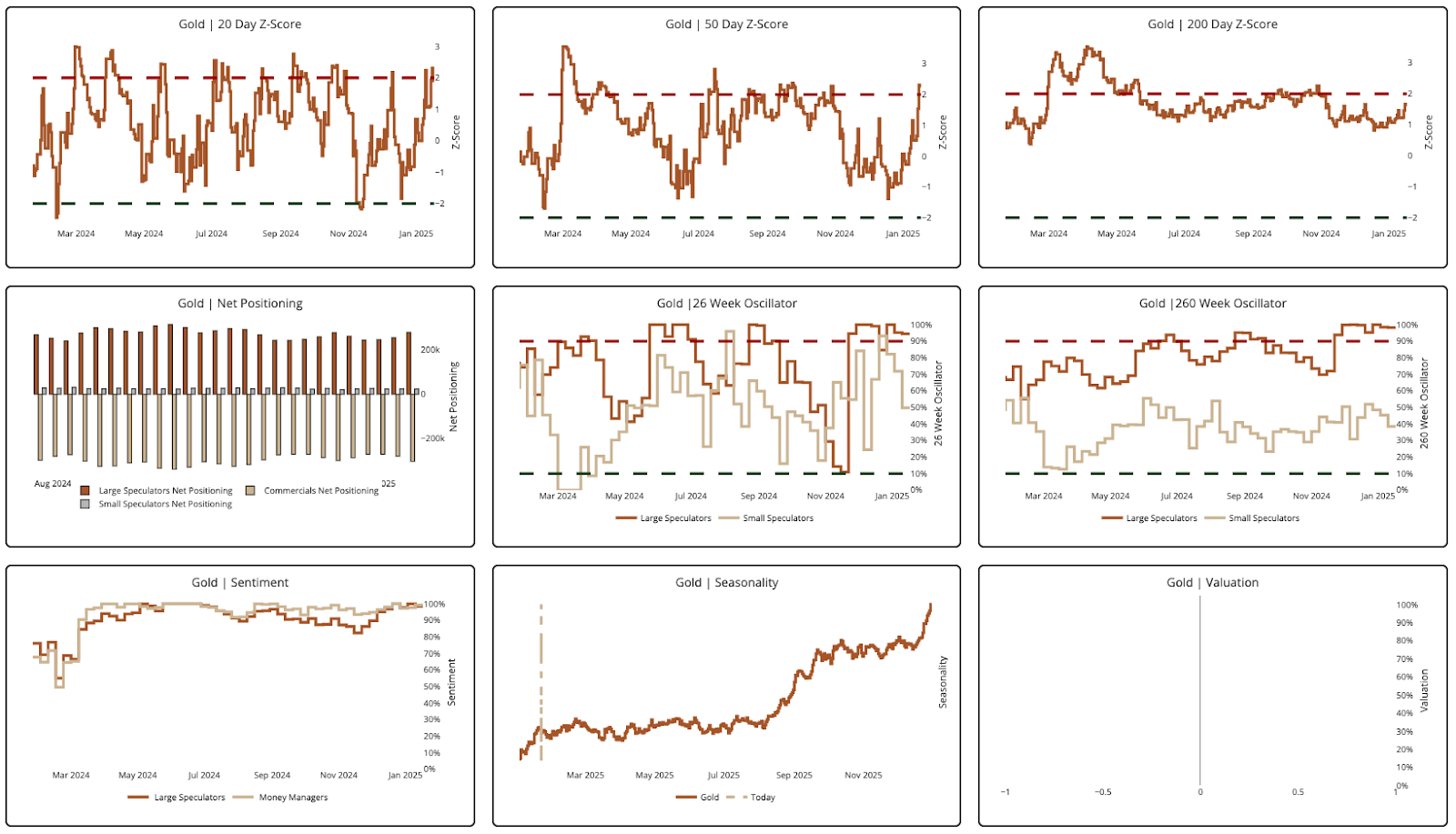

Let’s start with gold, which appears overextended by almost every metric. Here’s the most recent HUD data (see below).

You have all the ingredients of a pullback:

- Overbought on 20D, 50D, and 200D moving averages

- Increase in Large Spec net positioning to even higher levels

- Large Spec positioning over 90% on 26 and 260-week periods

- Sentiment at all-time highs

But then you look at the chart …

And you think, “There’s no way I should be bearish this thing. It’s breaking out, in an uptrend, in a Bull Quiet regime. Alex would kill me if he found out I turned bearish.”

Okay, that last part is the voice inside my head.

But Alex would be right. Yes, the CoT data flashes caution. But the tape, which never lies, says “all good.”

When in doubt, go deeper.

And by deeper, I mean the gold mining ETFs. Let’s start with the GDX daily chart (see below).

It’s bullish. You have a failed breakdown below the 50D and 200MA with an immediate regain of both moving averages at the infamous “double cross.”

Now step back and examine the monthly chart (below).

I see an 11YR cup and handle pattern, with the handle firmly in a Bull-Quiet Regime. Again, this is bullish.

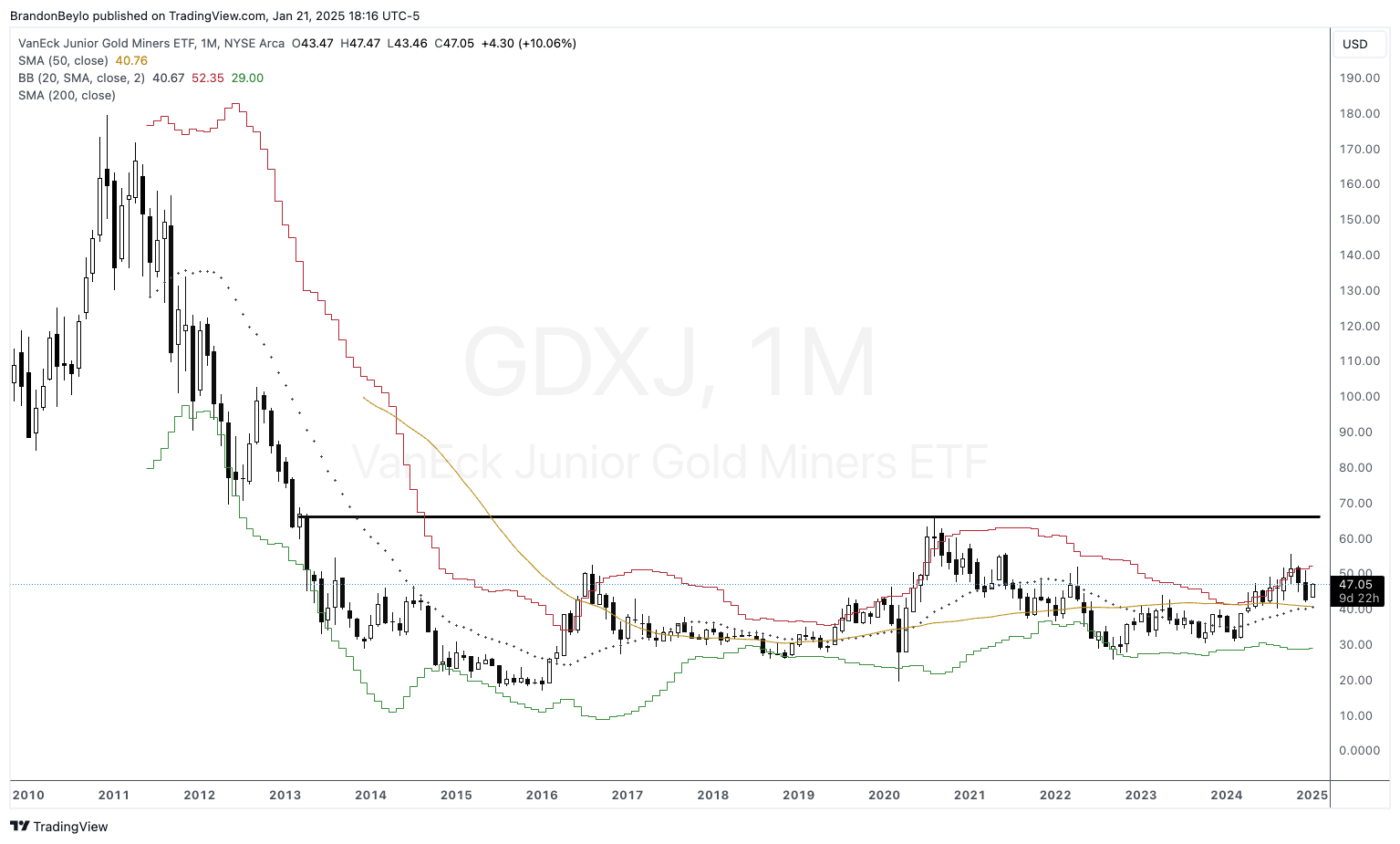

You also see the same pattern on GDXJ (below).

This could mean two things: spot gold drifts sideways or down for a few months as it cools from overbought levels, or gold miners finally outperform the underlying commodity. Or both?

The point is that gold and the miners are in the early stages of a long bull market.

We’re positioned well either way.

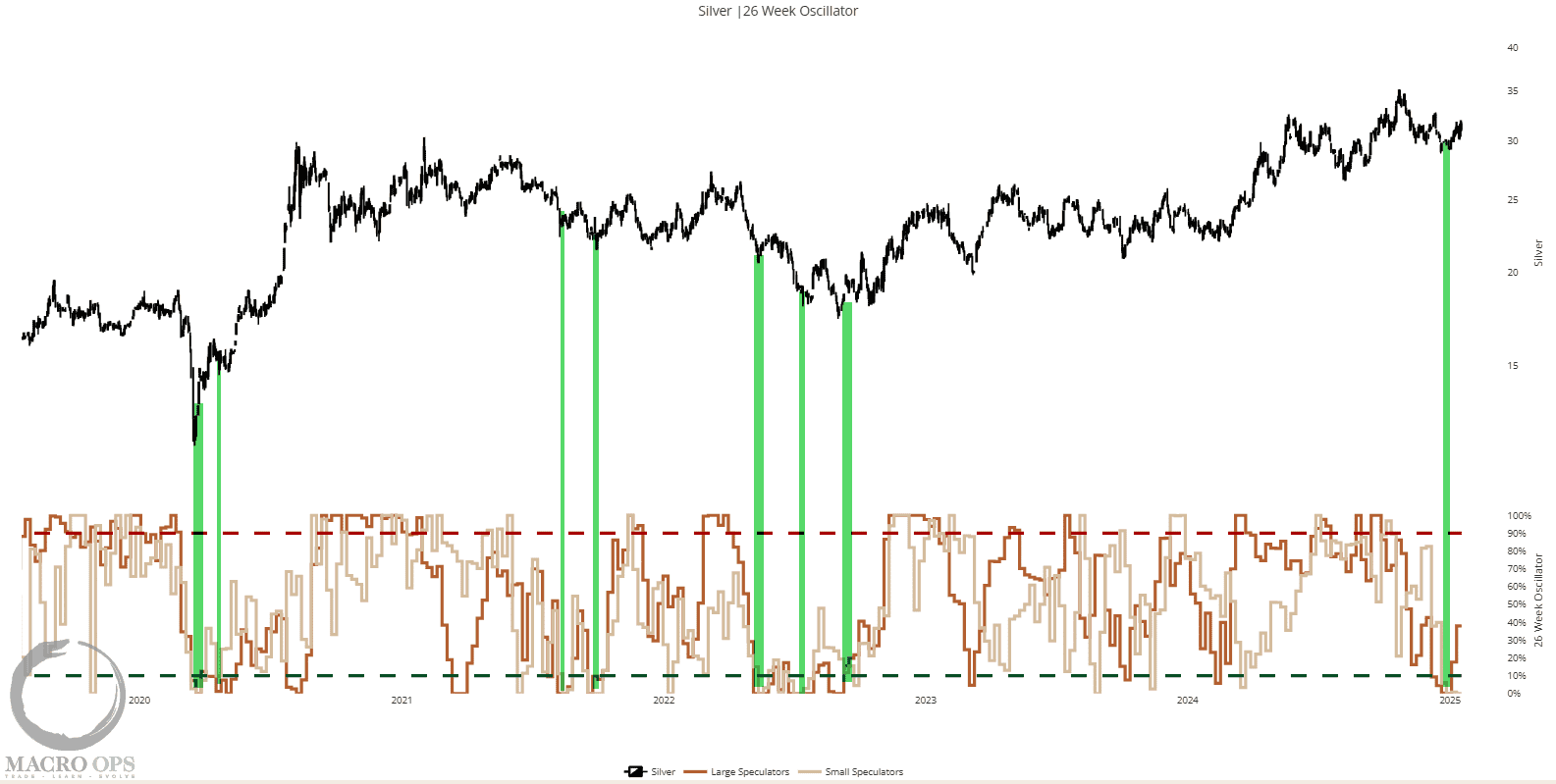

Onto silver.

Alex did a great job highlighting the bullish silver trade in this week’s Dirty Dozen (excerpt below).

“Speaking of PMs, it looks like the silver sentiment is also washed out.

Our 6m CoT Oscillator shows both large and small specs recently dipped below the 10% level, triggering a CoT buy signal.”

According to the Silver Institute, industrial demand should reach record highs in 2024, while mine supply will barely grow by 1%.

Here’s a snippet from their November 2024 report (emphasis added):

“The global silver market is set to record a physical deficit in 2024 for the fourth consecutive year. Record industrial demand and a recovery in jewelry and silverware will lift demand to 1.21 billion ounces in 2024, while mine supply will rise by just 1%. Exchange-traded products are on track for their first annual inflows in three years as expectations of Fed rate cuts, periods of dollar weakness and falling yields have raised silver’s investment appeal.”

You can’t talk about silver without mentioning Trump’s potential 25% tariff on Mexico, the world’s largest silver producer. Rising costs in Mexico raise the entire industry cost curve.

Higher AISCs mean fewer economically viable projects and lower production, which is bullish for the silver price and our recent purchase of Andean Precious Metals (APM).

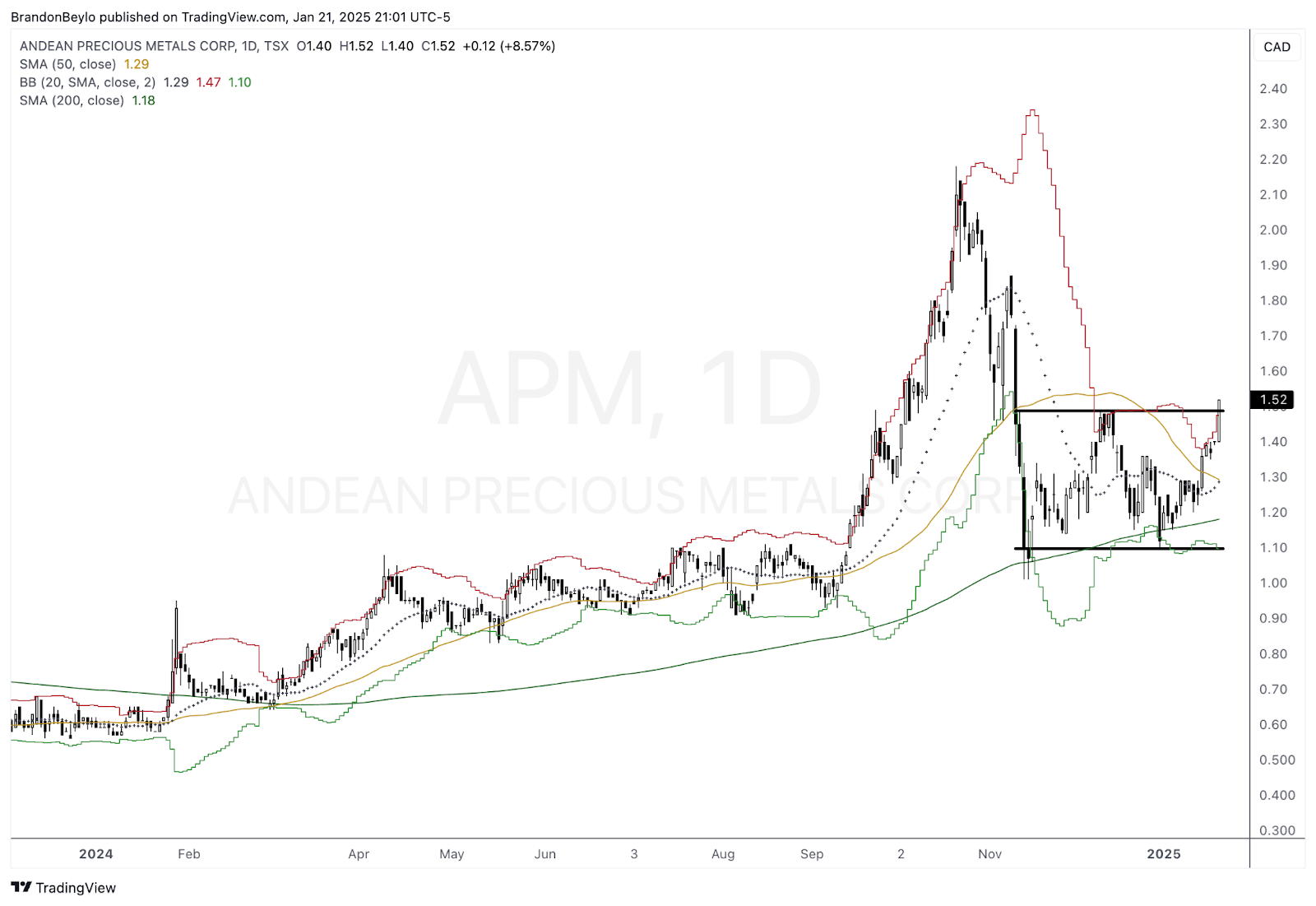

Andean Precious Metals (APM): Doing The Right Things

It’s been an on-again-off-again relationship with APM. To recap, we first bought the stock at around CAD 0.70. Made a ton of money as it rose to CAD 1.50. Then sold after APM ended its supply agreement with Silver Elephant (ELEF) over ELEF failing to meet various regulatory standards.

Investing in junior miners feels like walking through the Overlook Hotel in The Shining. You don’t know which door (read: company) leads to bloody hallways, an ax murderer, or possessed twins.

I spook easily. So when I saw that news release, I sold first and asked questions later.

However, APM has done all the right things since that news release. They renewed their NCIB for another 7.5M shares; management bought shares on the open market, uplisted to the TSX, and signed a new 100,000-ton ore purchase agreement from the Trapiche Concession in Bolivia.

The 100Kt purchase agreement still leaves a 700Kt supply gap. But it’s a step in the right direction.

Here’s some more good news. Given current gold prices, the company could fully repay the debt it used to acquire Golden Queen by next November. This should provide a re-rating as APM becomes debt-free with two PM-producing operations, over $100M in net cash, ample share buybacks, and a potential acquisition.

Check out APM’s chart.

I love this entry point. Price consolidated after an ETF flows-driven sell-off and found support at the 200D MA. Today, we broke out from that two-month rectangle. Let’s see if it holds.

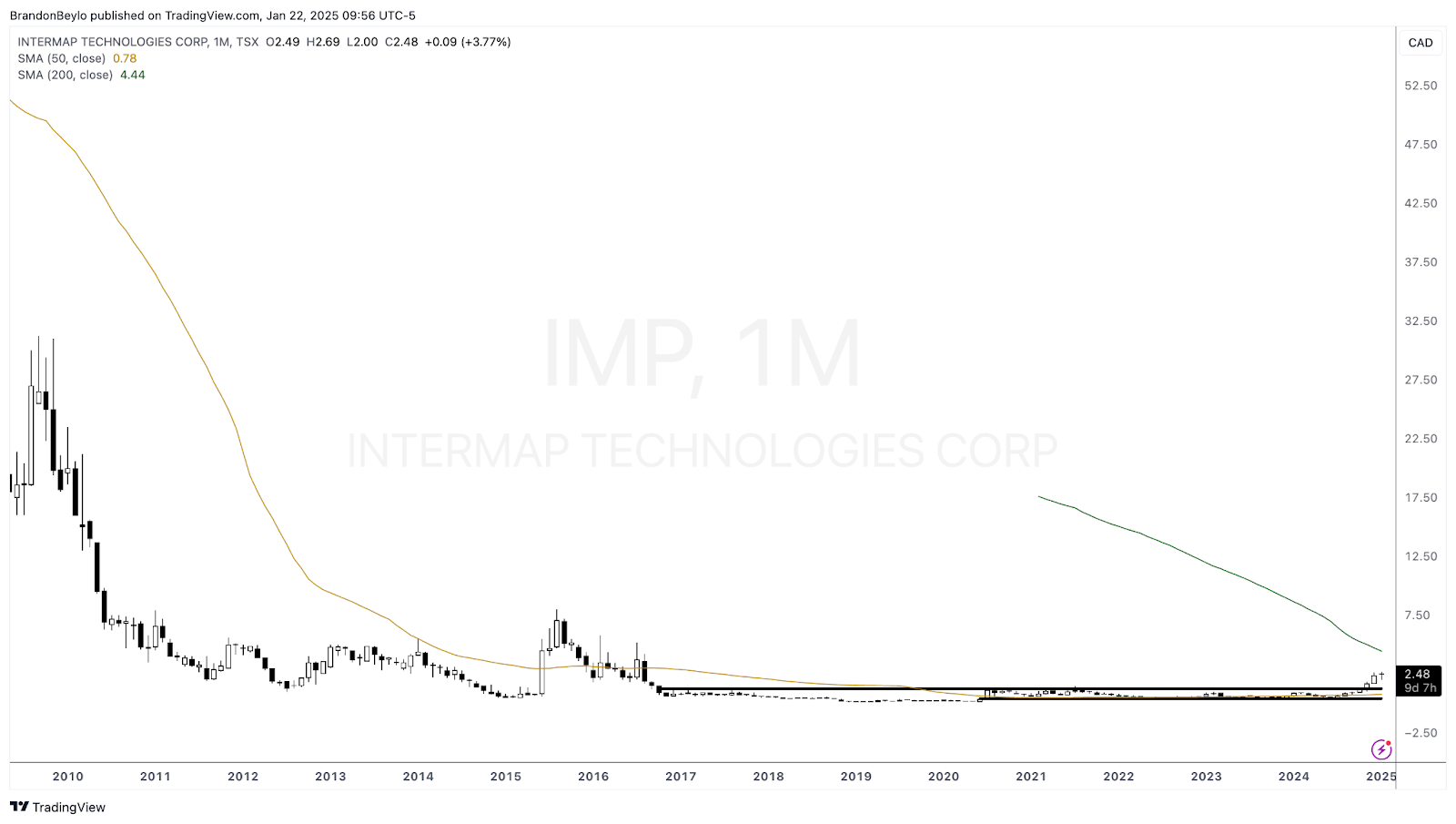

Intermap Technologies (IMP.V): Winning More Contracts

IMP is a geospatial intelligence company that provides 3D terrain data, software, and solutions for various industries.

They help insurance companies underwrite more accurate policies, aviation experts navigate elevation and terrain, and military personnel operate in non-GPS zones.

You can read our deep dive on the company here.

The elevator pitch is that by 2026, the company should generate its market cap in revenue at 40%+ profit margins with no debt.

At a conservative 15x multiple, shares would be worth $7 or 500% higher than our cost basis.

To do that, IMP needs large contracts from government/military agencies.

This week, the National Geospatial-Intelligence Agency (“NGA”) selected IMP as one of the vendors for the $200 million Luno B commercial data indefinite delivery, indefinite quantity contract.

IMP won’t win most of that contract, but even getting some of it validates its technology and standing as a company. Remember, IMP’s new CEO had to fix many mistakes. He had to show customers that IMP was a real business that would deliver on its promises and have the balance sheet to endure long-duration contracts.

Let’s head to the charts.

IMP is a textbook Ted Warren stock. This is a left-for-dead chart. Nobody wants to touch this company. But look to the right. Over the past two months, IMP broke out of its 9YR base on above-average volume.

We’re up ~50% on our cost basis and will add on pullbacks within the bull trend.

ClearPoint Neuro (CLPT): A Potential Compounder On Our Hands

CLPT is a neurological platform company that enables neurosurgeons to perform minimally invasive procedures under real-time MRI guidance. The company provides these solutions through its ClearPoint Neuro Navigation System or CNNS.

I wrote about the company three years ago (read here).

The product pitch was that CLPT allows doctors to see the entire “map” of the brain in real-time as they implant electrodes, perform biopsies, or trigger Deep Brain Stimulation (DBS). More importantly, CLPT allows doctors to see MRI scans in real-time, whether in the MRI room or the OR.

That’s a big deal as more pharmaceutical companies develop gene therapy drugs that target neurological conditions like Alzheimer’s and Dementia.

It all comes back to the Blood-Brain barrier (snippet from my original write-up):

“The Blood-Brain Barrier makes it difficult for neurological therapies to enter the brain and get to healin’! In our recent podcast, Peter Mantas of Logos LP explained this challenge better than I ever could.

Paraphrasing Peter, a therapy that can help the brain of a Parkinson’s Patient, might also destroy a liver or a kidney. And if you deliver that Parkinson’s treatment orally or through the bloodstream, you risk that therapy damaging other organs on its journey toward the brain.

CLPT’s SmartFlow Cannula eliminates this problem.

Doctors can use the CLPT’s technology with exact accuracy for drug delivery into the brain.”

Peter recently did a podcast updating his thoughts on CLPT; listen here.

The 30,000ft view is that all these gene therapies will eventually use CLPT delivery mechanisms to administer drugs to patients. Once they choose the delivery mechanism, it’s locked. Switching costs are incredibly high, complex, and time-intensive.

That thesis is working as evidenced by recent partner wins:

- PTC Therapeutics approval of KEBILIDI

- QURE Huntington’s disease accelerated clinical development

- Bayer’s BlueRock Therapeutics for Parkinson’s Disease

- Four other CLPT partners with enhanced FDA approval processes

Lake Street Capital also raised its price target from $17 to $30/share.

The stock trades at a ~$490M EV. You don’t have to make many wild assumptions to get to $1-2B in EV over the next few years.

Check out the long-term chart, too.

It reminds me of the GDXJ chart… a long cup and handle base waiting to break out. In this bull trend, we’ll add to our core ~5% notional position on pullbacks.

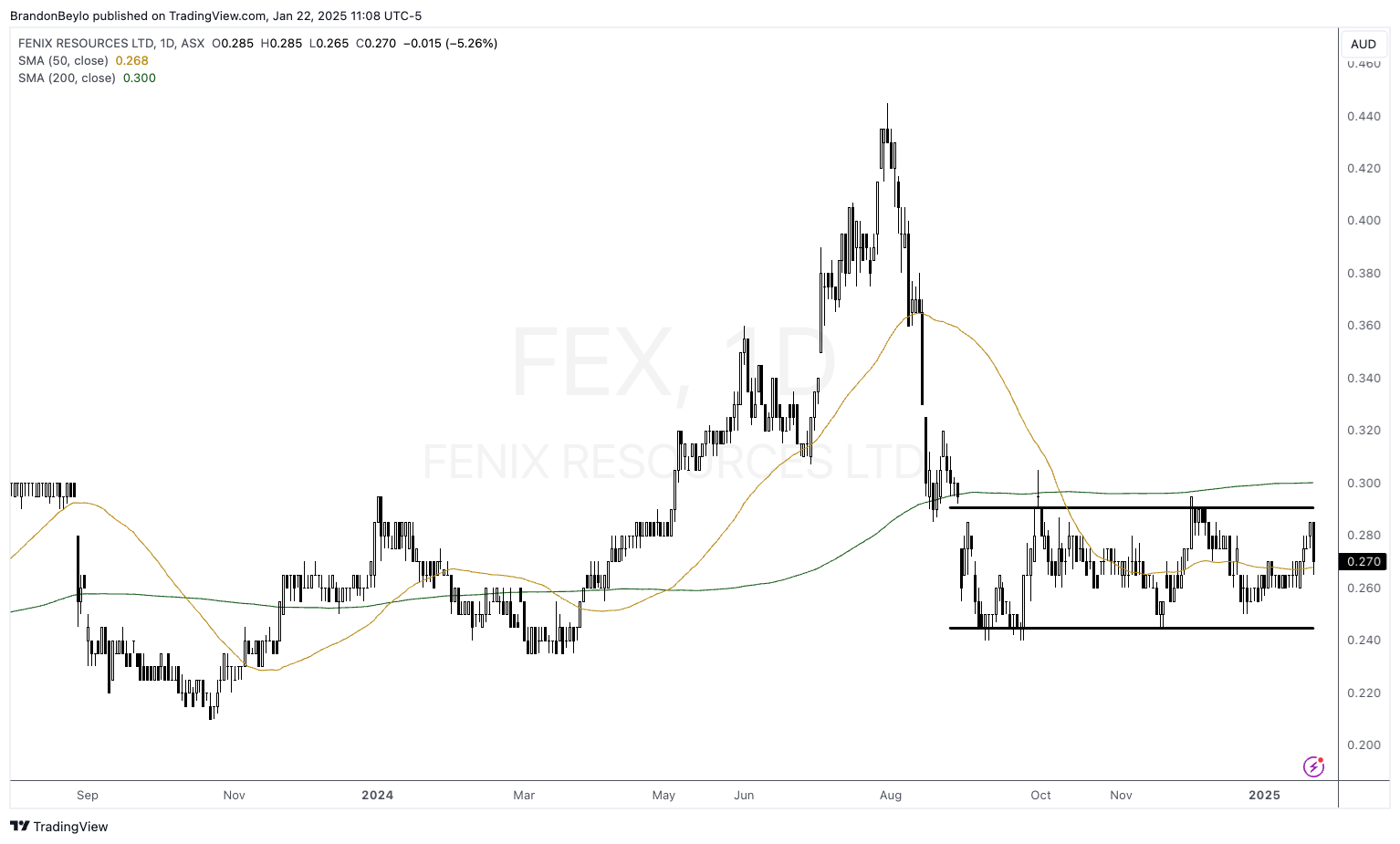

Fenix Resources (FEX.AX): I Have No Idea Why The Price Is Still Low

The market is mostly efficient most of the time. However, there are times when I have no idea why a stock trades at such low prices. Fenix Resources (FEX) is one of those companies.

FEX is an Australian-based iron ore producer. You can read our deep dive here.

The elevator pitch at the time was that “FEX is not just a single-asset producer of ~1.3Mt/year. It’s a company in rapid transformation, expanding into a four-mine operation that will generate 4Mt+/year of iron ore at $50/t+ margins.

The company also owns a mining logistics business and was recently awarded a $70M contract from just one customer (not to mention its ~ $50M replacement cost value).

Additionally, FEX owns irreplaceable port infrastructure assets in Geraldton, which help deliver bulk commodities globally from Mid-West Australia. The port assets have between $80 and $150M in insurance-backed replacement value.

Finally, the company has ~$25M in net cash on the balance sheet and has paid $45M in cumulative dividends since 2022. Company insiders also own 13% of the business.”

Since then, FEX has only improved. The company has $26M in net cash, hedged 660,000t of iron ore at AUD 154/t, expanded its resource base, and is on pace to triple iron ore production in 2025.

Yet the stock price has fallen 17% since my write-up. My base case is that I’m wrong somewhere, and it’s my job to find out where.

If I had to guess, the market isn’t valuing FEX’s growth because it would rather see capital returns via dividends and buybacks. I get that. However, the company wants to hit 4-5Mt of annual production before resuming capital returns, which costs money.

Read my CEO call notes to learn more about John’s 3-5 year vision.

Also, FEX will trade with iron ore, which hasn’t moved much this year. Iron ore trades around $100/t. FEX generates tons of cash at that price with ~$52/t cash costs.

At some point, the market must recognize FEX’s cash-generating abilities. If iron ore stays around $100/t, FEX will generate ~2x its market cap in pre-tax profits in 2025. Valuing the rest of the business at less than zero (logistics, future production, etc.).

Finally, I like the chart (see below).

You have a five-month rectangle base below the 200MA. A breakout above resistance could send the stock to recent highs of AUD 0.44/share. Part of me wants to buy a starter position here with a stop below the rectangle, then add if/when the stock breaks out. Look for a trade alert.

That’s all I have for this week, guys! Thanks so much for reading. As I said last week, I love writing these Portfolio Updates. They help me more deeply understand our businesses and why we own them.

Quick reminder … If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the below and sign up. We look forward to seeing you in our Slack!