It’s Portfolio Update time!

This week, we have Part 1 of our Portfolio Update.

We will cover oil, VLE, VIST, RHM, NICU, and IDR. We will also discuss strategies for adding to current positions, stop-loss rationalizations, and notional size goals.

But before we dive into the review, I want to pitch our Macro Ops Collective.

The Collective is the most unique group of traders, investors, and entrepreneurs on the Internet. Our central goal is to become consistently profitable in any market regime while having a ton of fun.

The MO portfolio officially closed the year with a +50.4% return. We’ll soon publish our year-end review, which will discuss our painful mistakes and total blunders, what we’ve learned, and what we’ll try to do better in the year ahead. So keep an eye out for that.

If you’d like to join our Collective as we tackle 2025 head-on, click here.

Let’s get after it.

Portfolio Update: Running Through Our Book

We’re up ~4% to start the year (as of this writing). I like what we own, where we own it, and our current risk management strategies (i.e., be ruthless with cutting losses to preserve actual capital).

I’ll review the book and provide quick blurbs on our current positions before exploring some watchlist names that might appear in the port in a few weeks.

Crude Oil: Steady As She Goes

Our crude long positions, which have an average cost of $70.78, are up ~12% on average.

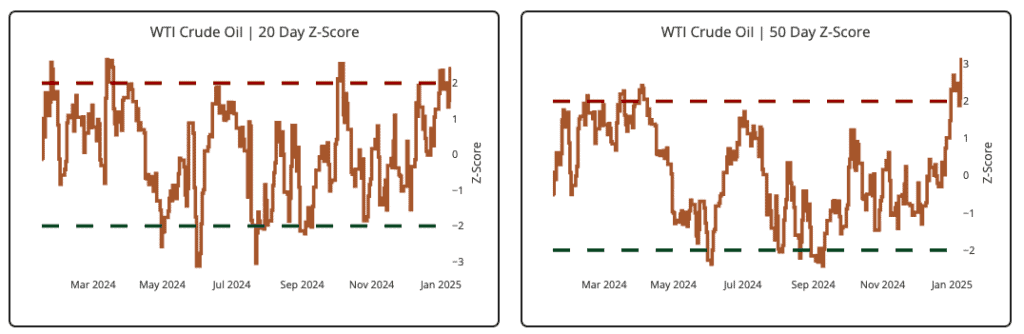

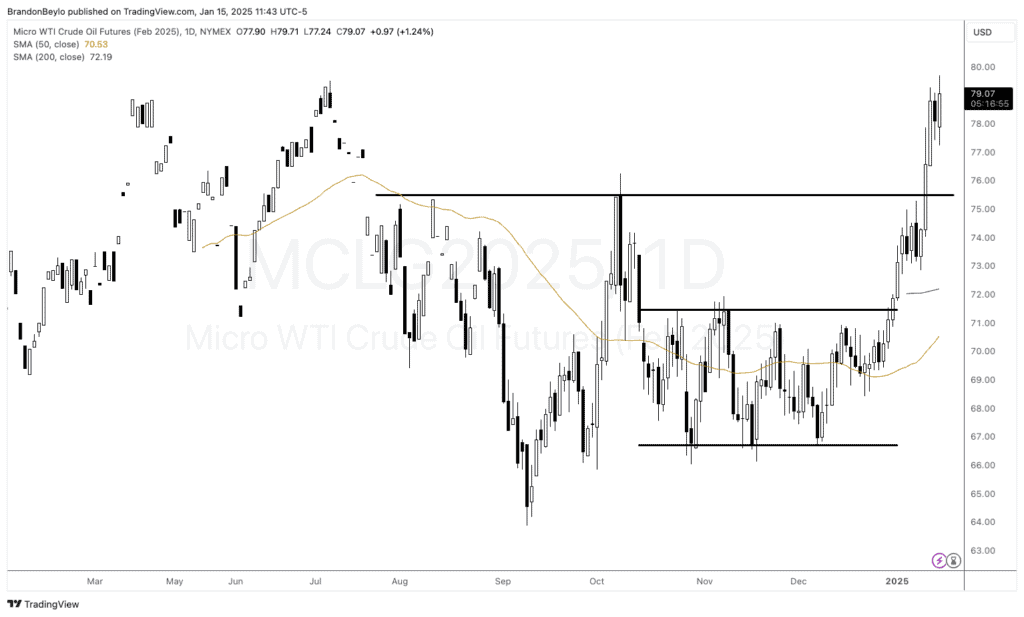

Oil has overshot to the upside and is now two stds above its 20D and 50D MAs (see HUD data below).

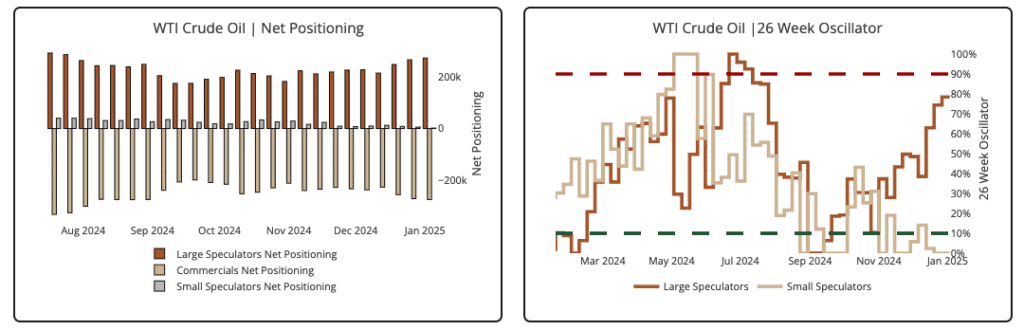

Large specs are also ~80% long, up from 13% in December (see below).

We should expect a short-term pullback in oil and oil-related equities. My base case is that we retrace to prior resistance/new support of ~$75.50/bbl (see below).

Onto our energy-related equity positions.

Valeura Energy (VLE) & Vista Energy (VIST): Relative Strength Leaders

VLE and VIST represent ~18% of our portfolio NAV as of this writing (VLE at 11% and VIST at 7% notional).

Here’s our research on VLE:

- Most recent deep dive

- Adrian Godas 2023 deep dive (should’ve bought here!)

And our research on VIST:

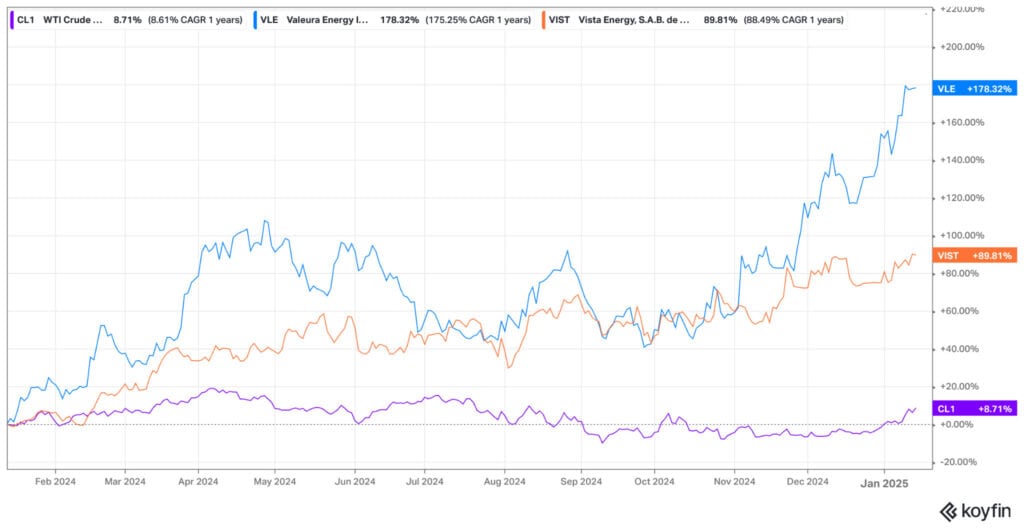

Both stocks have outperformed the underlying commodity on a 3M, 6M, and 1YR basis (see 1YR returns below).

I’ve written extensively about “leaders leading,” and that’s what you see here. Oil is up ~9% over the past year, while VLE is up 178% and VIST is up 70%.

VLE released Q4 and FY2024 results last week. Here are the highlights:

- Record oil production, averaging 26,109 bbls/d in Q4 2024

- Full-year average oil production of 22,825 bbls/d(1)

- 2.95 million bbls of oil sold in Q4 2024

- 8.35 million bbls for the full year 2024

- Q4 average oil price of US$76.7/bbl

- US$679 million in revenue for the full year 2024

- US$259.4 million in cash with no debt

- Completed internal restructuring, allowing VLE to monetize its NOLs and pull forward cash flow generation.

- Repurchase of 348,400 shares in Q4 2024, following the commencement of the Company’s normal course issuer bid (“NCIB”) in mid-November 2024.

VLE is in a great spot. It has $260M in cash, no debt, and can fund reserve growth with cash from operations. At ~$75 oil, it’ll have plenty of cash to meet all growth capex requirements while buying back stock and maybe making a small acquisition.

Let’s check the tape.

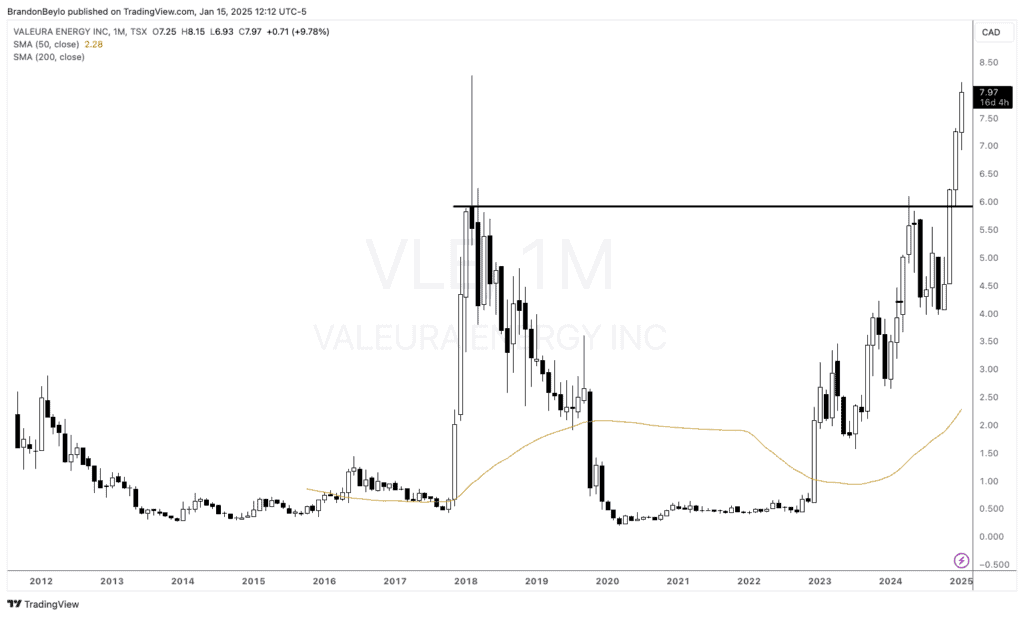

Find me a more bullish monthly chart in the E&P space … I’ll wait.

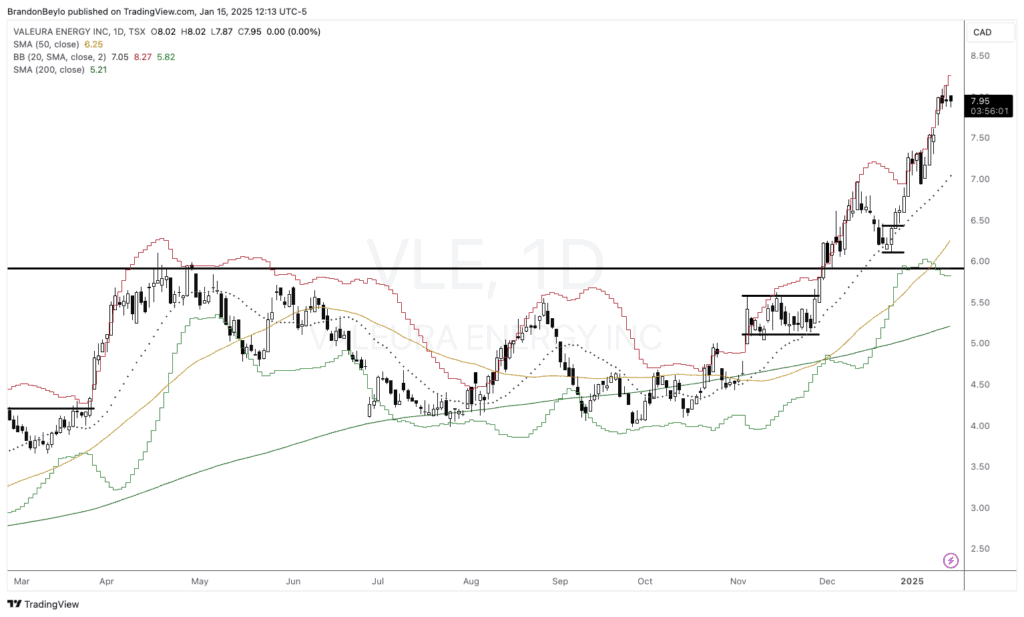

That said, VLE is overextended on every time frame (daily, weekly, etc.). My base case is that we retrace toward the midline on the daily time frame at ~$7/share before heading higher.

You can see how much VLE respects that midline.

Despite its share price increase, VLE trades at only 2x NTM profits.

Onto VIST.

The company will report earnings in February, but we’re hearing good news from Vaca Muerta, VIST’s central operating region.

In November, Reuters reported that Vaca Muerta hit record Q3 oil production.

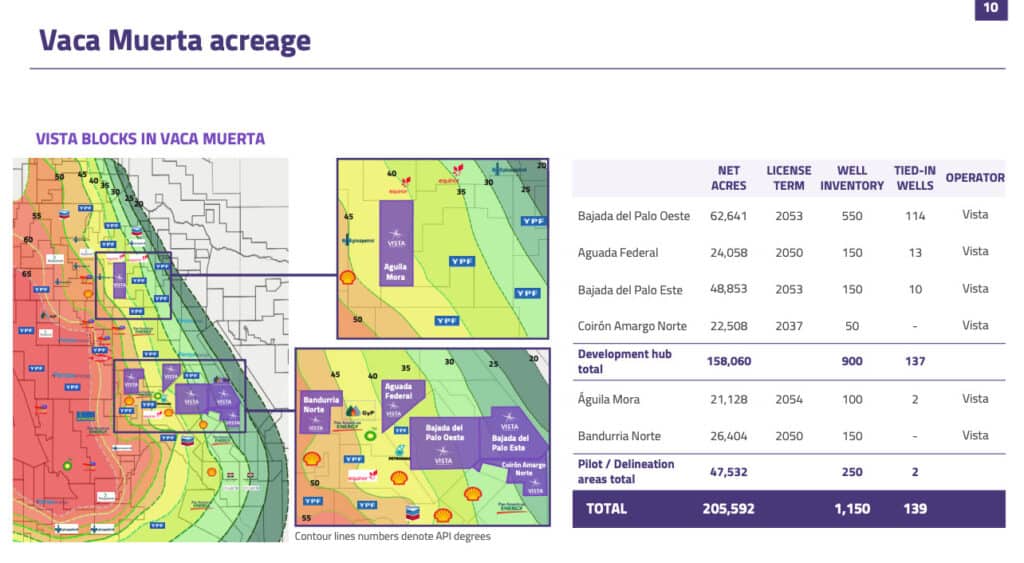

VIST owns 205,592 acres in the Vaca Muerta. They have 139 tied-in (read: existing/online) wells, with another 1,150 in the pipeline (see below).

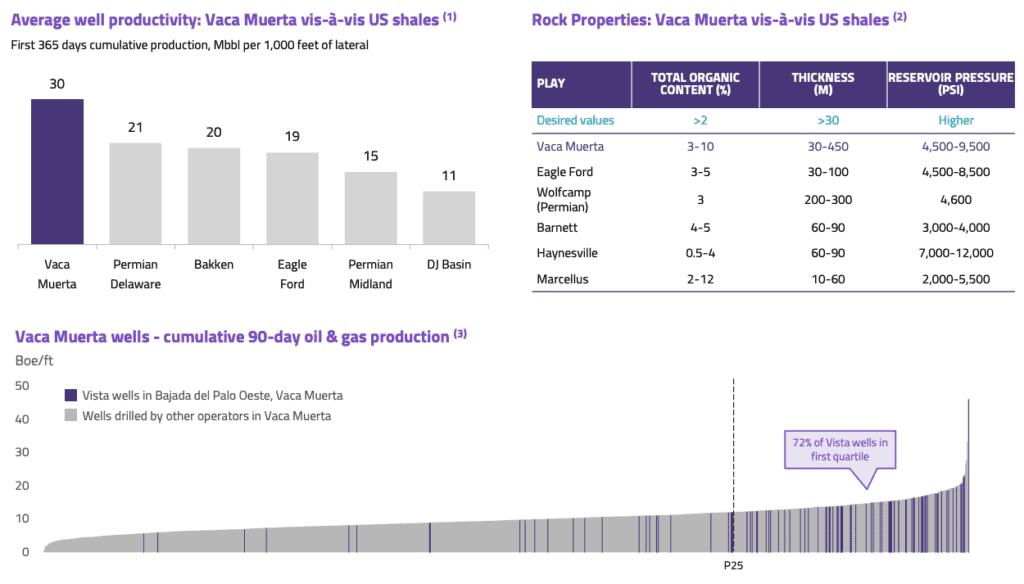

The Vaca Muerta also has higher average well productivity than the Permian, Bakken, Eagle Ford, and DJ Basins (see below).

VIST’s financial achievements are incredible. Since 2018, the company has increased its EBITDA from $144M to $1.1B, and its EBITDA margins have expanded from 43% to 73%.

Meanwhile, the stock still trades at <5x NTM EBITDA.

Let’s head to the charts.

I like this base around the 50D MA in a Bull-Quiet regime. Hopefully, we get a few weeks of sideways action before the next base breakout. You could add either on the breakout or a retracement to support at $53/share.

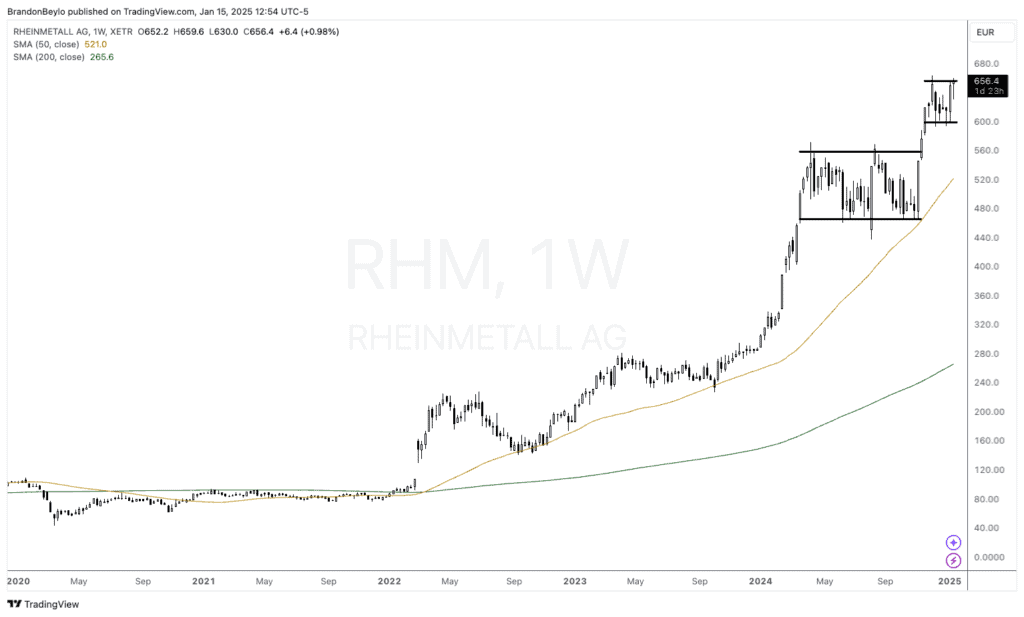

War / Trump Hedge: Rheinmetall (RHM.XTR)

RHM Military/Defense Powerhouse RHM, our EUR 30B global military/defense manufacturer, is a force to be reckoned with. The company’s diverse product range, from vehicles to ‘night night’ devices, positions it as a hedge against global uncertainties.

The company is a hedge against anything terrible happening worldwide, including any Trump tweet (Truth Socials?) or geopolitical stance.

Our thesis is that Trump will demand Germany/EU to spend more on their defense and military (i.e., rely less on the US) and that RHM is the best-positioned company to meet that future demand.

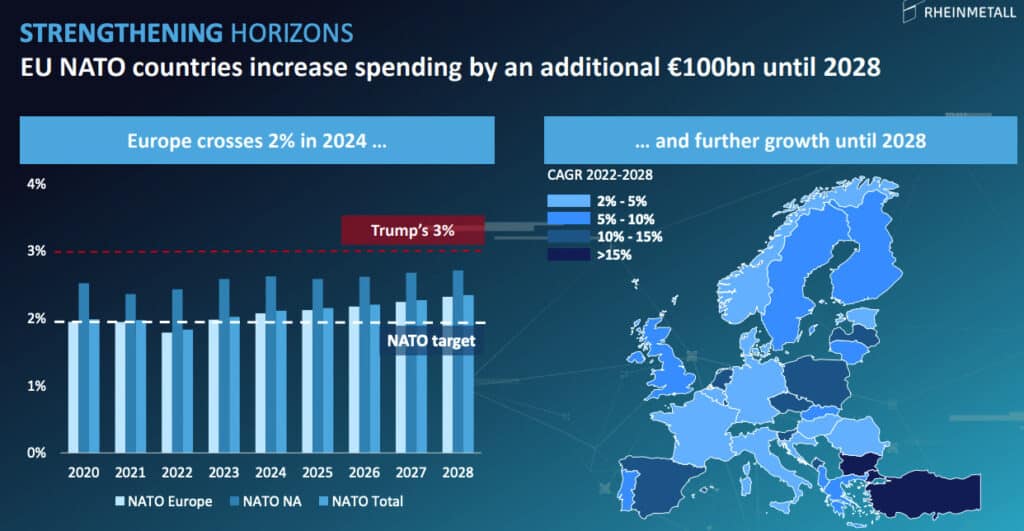

Here’s a simple way to frame it: In 2024, Europe spent ~2% of GDP on national defense. Trump wants them to spend at least 3%. A 1% increase would result in an additional EUR 100B in annual spending until 2028 (see the graph below from RHM Investor Day).

There are a few reasons why I think RHM will get the lion’s share of this additional spending:

- They’re the largest defense company in Germany and the fifth-largest in Europe.

- They’re quickly creating one of the largest military vehicle fleets globally.

- They were one of the leading defense partners for Ukraine.

- They have one of the most badass CEOs in the game (Russia/KGB tried to assassinate him at one point).

RHM recently partnered with Leonardo (LDO) to enter the EUR 50B+ Italian defense market. They also acquired a US-based company that will double its US defense sales.

The company already has EUR 30B in booked backlog from Germany alone.

Let’s do some napkin valuation math. RHM estimates they’ll generate EUR 20B in revenue by 2027, with 18% operating margins (EUR 3.6B) and a 40%+ % cash conversion rate (EUR 1.62B, assuming 45%).

The company trades at ~8.3x 2027E operating profits. Given the heightened tension and global conflict, RHM should command a premium multiple (20-25x).

By 2027, RHM could trade for ~EUR 72B or ~EUR 1,670/share (155%+ upside).

Let’s head to the charts.

This is a textbook bull market chart: Consolidation → expansion → consolidation. We’re using the 50D MA as our initial stop-loss target.

We have a ~6% notional position with only 40bps of actual risk (perfect size for now).

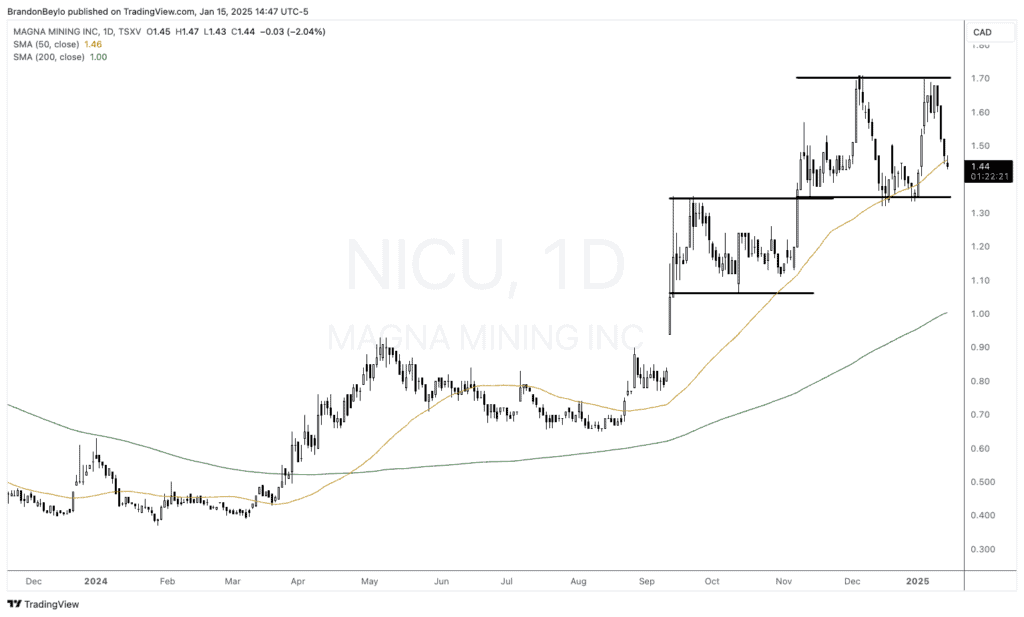

Mining Plays: Magna Mining (NICU) and Idaho Strategic (IDR)

I recently wrote about NICU, so I won’t spend too much time on it here. But for newer Collective members, NICU is a Sudbury-based junior copper, nickel, PGM/gold developer who’s about to become a producer after purchasing the McCreedy West copper mine and other assets from KGHM.

CEO Jason Jessup worked at FNX Mining – which owned the same assets, in the same jurisdiction, with the same executive team – and saw the stock price rise from $0.25/share to $15/share.

NICU is FNX Mining 2.0. This Bet The Jockey investment is backed by significant assets and a production plan to see NICU producing from four mines by 2027.

The math gets silly if NICU reaches four producing mines by 2027. The company would generate over $200M in annual FCF versus its current market cap of $200M.

Sudbury is one of the best mining jurisdictions globally (if not the best). If NICU reaches its 2027 targets, we could see a 5-10x multiple on FCF and a multi-billion dollar market cap.

Jason also owns 10% of the company and will not sell a share until NICU reaches a $1B market cap (his own words!).

Let’s review the tape.

Another stair-step bull quiet market regime. We don’t need to overthink this. I’m a buyer at the CAD 1.34 support level.

There’s also some interesting macro news in the nickel market. This week, Indonesia announced they may cut nickel production by 45%.

Nickel currently trades around $7/lb, and nobody makes money at that price. I talked with a few nickel mining investors, who told me, “Indonesia doesn’t make much money at these prices. They need around $10/lb to generate decent returns.”

NICU is fortunate in that it can “turn on” nickel production whenever it wants. It has stopes ready for Vale or Glencore’s mills. In the meantime, it can profitably mine copper, PGMs, and precious metals.

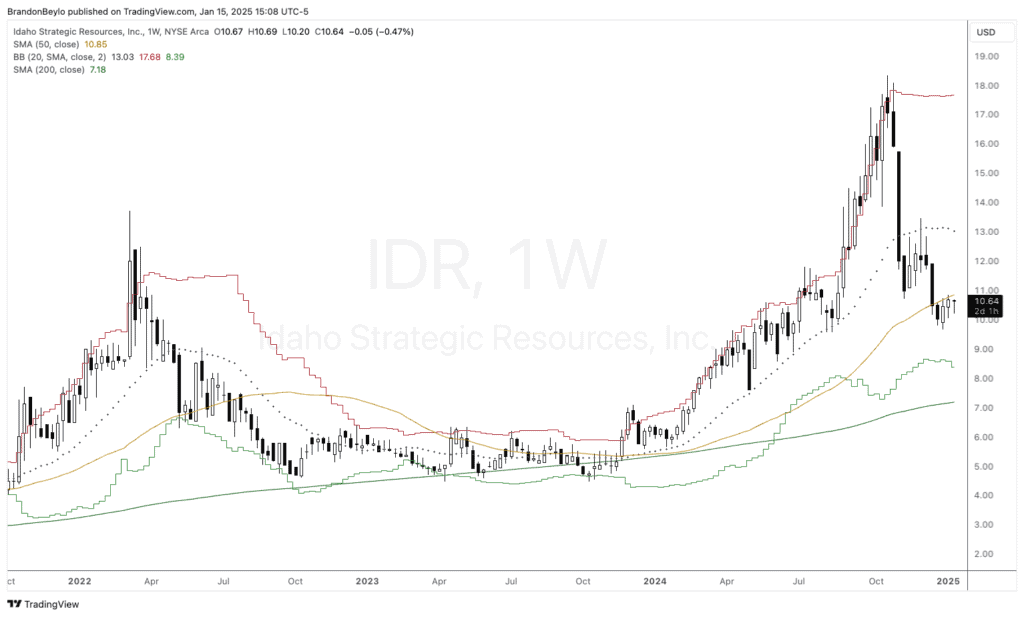

Idaho Strategic (IDR): Getting Attractive Again

Idaho Strategic (IDR) is an Idaho-based gold producer and developer of rare earth elements (REE).

The company has had one of its best years ever. Here’s CEO John Swallow on the company’s 2024 achievements (emphasis mine):

“Our Company has turned the corner on profitability, which has allowed us to reinvest in the business in ways we couldn’t in the past.

Through the first three reported quarters, IDR has increased its total revenue by 84%, its net income by 744%, and its earnings per share by 600% – and the Company closed out the year strongly with its best quarter ever.

Additionally, the Company’s cash per share increased from approximately $0.18 at the end of 2023 to $0.85 at the end of the third quarter in 2024, a 372% increase.“

IDR’s stock briefly touched $18/share before falling 40%+ to today’s price of ~$10.60/share.

I used the sell-off to increase my position in my retirement account, and I’m looking for a spot to add it back to the MO portfolio.

IDR trades for ~10x 2025 profits with $12M in cash and no debt. That’s 10x profits for a growing and profitable gold producer with the US’s most extensive REE land package thrown in for free.

Not bad!

At current gold prices, the company will generate a lot of cash, which it will use to reinvest in production growth, asset expansion (maybe its mill), and the development of its REE land package.

Check out the chart below.

You have a potential bear trap where the stock trades below the 50D MA but quickly recovers and trades back above it.

Be on the lookout for a trade alert to get back in by the end of the week.

Quick reminder … If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the below and sign up. We look forward to seeing you in our Slack!