At their highest level, investment returns can be subdivided into three components: the cash rate, beta, and alpha.

return = cash + beta + alpha

The cash rate is the base interest rate controlled by central banks. Every other asset is priced off this rate, including stocks and bonds.

A majority of the time stocks and bonds return more than the cash rate to incentivize investors to take risk. This makes intuitive sense. Why would someone buy risky assets if they could earn the same return in their checking account?

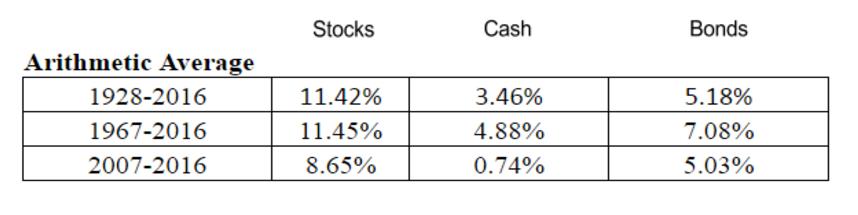

Pictured below are the average arithmetic returns for stocks, cash, and bonds since 1928.

The data confirms the logic. On average, stocks and bonds earn more than cash, which is why investors are willing to take on the additional risks.

The returns for stocks and bonds are examples of investment betas. Betas are cheap and easy to obtain, especially in the modern market environment. All you need to do is purchase a cheap index fund and hold.

The harvesting of this risk premium doesn’t require market timing. Nor does it require time and energy. It only requires the mental fortitude to hold through volatility. That’s the real “cost” of market beta. Can you watch your nest egg lose 50% and still hold on? If you can, you’ll realize the beta returns.

Improving on these passive beta returns requires something called alpha. Alpha is the reward for good trading strategy. You capture it by making a series of tactical bets against other market participants.

But capturing alpha is a zero-sum game. If you win, someone else loses. In this sense you’re actually fighting against others in the marketplace to grab alpha from each other. And that’s why the process takes far more time and energy than collecting beta returns.

At Macro Ops our goal is harvesting alpha, not beta. This causes our portfolios to look drastically different than the standard asset-allocation mix.

Asset-allocation portfolios deploy 100% of their cash into a mix of asset classes including large caps, fixed income, annuities, small caps, and more. They always play to the long side and never bet on an asset depreciating in value. Their goal is to generate beta.

Macro Ops’ portfolios on the other hand are focused on alpha. They start from a cash position and use that cash to collateralize tiny tactical bets when the time is right. These portfolios aren’t constrained by market type or long-only mandates. They look for both bull and bear moves across all markets. Domestic equities, foreign equities, commodities, currencies, fixed income, volatility… it doesn’t matter. These portfolios trade it all, long and short.

Sometimes stocks are boring and don’t have attractive risk/reward setups. Sometimes currencies are the only markets moving. No matter the case, these portfolios’ flexibility makes it easy to avoid dead money markets and focus on the where the money is hot. Alpha is fleeting. Harvesting it is a constant chase. And that means you gotta go where the gettin’ is good.

There are two things we use the cash + beta + alpha framework for:

- Setting return expectations for the year

- Determining our trading strategy

We need to know the rate of return on cash to set our expectations for the year. If cash is returning 10%, then our return expectations should be well over 10%. But if cash is returning 1%, we’ll expect much less.

We alter our trading strategies based off this information too. For example, if cash rates are high, we may decide to collect interest and use those proceeds to buy out-of-the-money options on high conviction macro themes. But if cash rates are near 0, this strategy obviously doesn’t work.

Beta comes into play here as well. There could be times when a pure beta strategy looks great. After a large market crash, the total expected returns on stocks could warrant an index allocation. But if cash rates are low and bonds and stocks are expensive (low beta), then we’d focus on making frequent tactical alpha bets.

Having an idea of this alpha/beta/cash return framework is vital to proper portfolio construction.

Do yourself a favor and bookmark the following links to keep track of cash and beta returns.

Base rate

10-Yr. Treasury rate

Earnings yield on the S&P 500

Awareness of these return metrics will help to hone your trading strategy. And maximize return in any market environment.

If you want to learn more about our trading process, check out our 80-page Macro Ops Handbook by clicking here.