It’s interesting how quickly the consensus around what a Trump presidency means for markets went from “it’d be an unequivocal disaster” to “his policies will bring forth a new and lasting economic expansion.”

Moral of the story: consensus has a habit of being wrong and reality tends to be bit more nuanced.

What should we make of all the hoopla then?

Let’s first note that:

- Presidents and political parties don’t drive business cycles, they simply enhance or dampen them.

- There are still many unknowns regarding exactly what a Trump presidency will look like.

Trump will be moving his oversized self-portraits into the West Wing at a time when the current bull market will be nearly 3,000 days old — 34 months longer than the average advance since the 1930s.

Obama was able to dodge a recession during his presidency (apart from the one he inherited). Trump won’t be so lucky.

But the little that we do know about Trump’s intended policies are, for the most part, very equity market positive.

The tax cuts/reforms, foreign profit repatriation, and deregulation are all low hanging fruit that will help boost the economy. His “yuuge” fiscal and infrastructure spending plan, if passed in full, will drive GDP up a few points through demand growth.

The single most important thing I gather though, from the election of Trump, is the change we’re experiencing in public sentiment.

The concern over public debt that put many “Tea Party” republicans into congress has now clearly been supplanted by a “growth at any cost” narrative. We’re seeing a global shift from fiscal austerity to a call for free spending.

This is a massive regime change that will impact markets over the coming decade.

Ray Dalio, the founder of Bridgewater (world’s largest and most successful hedge fund) wrote a note this week that is worth reading in full..

Ray thinks Trump’s election means we’ll “have a profound president-led ideological shift that is of a magnitude, and in more ways than one, analogous to Ronald Reagan’s shift to the right.” And he remarks that “there is a good chance that we are at one of those major reversals that last a decade (like the 1970-71 shift from the 1960s period of non-inflationary growth to the 1970s decade of stagflation….)”.

He included this nifty chart of real returns broken down by asset class per decade.

Stanley Druckenmiller, another market slugger, flipped his previous call for impending market doom to one of constructive bullishness. Druck thinks “there’s so much low-hanging fruit in terms of deregulation and tax reform, we could get a jolt of 4% growth for about 18 months”.

Both Druck and Dalio agree the secular cycle of falling interest rates is now over and that rates have only one direction to go — up.

And while they think the stock market will benefit from Trump’s fiscal expansion, the lasting positive impact on equities will depend on how quickly rates rise.

Here’s Dalio again.

The question will be when will this move short-circuit itself—i.e., when will the rise in nominal (and, more importantly, real) bond yields and risk premiums start hurting other asset prices. That will depend on a number of things, most importantly how the rise in inflation and growth will be accommodated…

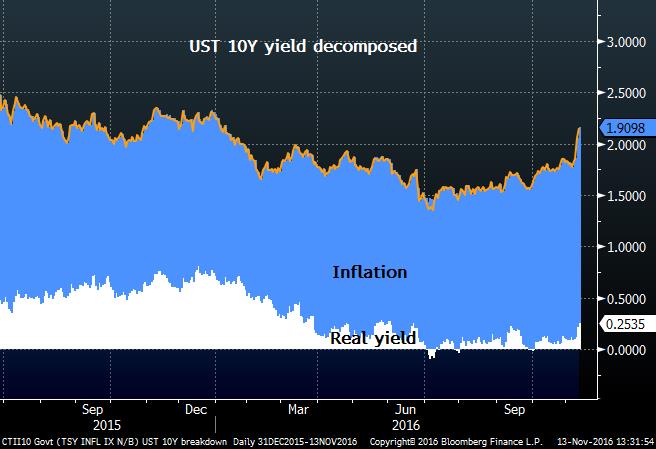

Since the election, rates have had one of their swiftest climbs in years. The 10-year treasury rate now stands at 2.22% — it’s highest level in over a year.

The increase in rates is being driven by both inflation (inflation expectations shot through the roof since the election) and a rise in real rates, which you can see on the chart below of the 10yr yield decomposed.

This is a regime change. It’s the start of our first secular rate rising cycle in over 30 years. And it includes a Republican president who aims to carry out one of the largest deficit fueled fiscal spending programs in US history outside of wartime.

All I can say is, as a dyed in the wool macro trader, I’m looking forward to the next four years…