Famed Tastytrade icon Karen “The Supertrader” has gone rogue. On May 31, 2016 the SEC filed a complaint against Karen and her investment advisory Hope Advisors LLC.

For those who don’t know, Karen achieved widespread recognition through the Tastytrade financial network. Tastytrade focuses on option selling and Karen in particular sells strangles on stock indices, which she does in size. So large, that Tastytrade had her on air multiple times for promotional purposes with headlines like “Made $41 Million Profit in 3 Years Option Trading.”

By early 2016 Karen was trading over 200 million dollars for herself and clients. These funds were split between HDB Investments and Hope Investments (HI).

Karen was using a “0 and 20” fee structure for both HDB and HI. This meant she took a 0% management fee on total assets, plus a 20% incentive fee on all profits.

Normally in the hedge fund world, the 20% incentive fee is only taken on new profits. Profits must exceed the high water mark of the fund before fees are taken.

So say you’re a fund manager with a NAV (net asset value) starting at $100,000. In month one, your NAV increases to $120,000. At this point you would be entitled to a share of that 20k in profits through your incentive fees.

Now imagine in month two you have a drawdown and the account falls to $105,000. You don’t earn any fees for the losses.

Then in month three you have a gain that brings the NAV up to $118,000. Even though you made a $13,000 gain here, you would still not be entitled to any incentive fees. And that’s because you didn’t exceed the high water mark of $120,000. You would need to make new profits above the $120,000 to earn your fees.

This is the standard practice in money management for how incentive fees are calculated.

But this is not what Karen did. Instead of basing her incentive fees off her NAV’s high water mark, Karen based them off realized profits.

This was handy because she could defer trading losses by never realizing them and still take an incentive fee every month, despite her NAV not exceeding the high water mark.

In HDB’s operating agreement there was nothing to indicate that she was allowed to take fees on realized profits without hitting a high water mark.

But for HI, there’s actually language in the agreement that fees were based off realized profits despite unrealized trading losses. But it’s also explicit in saying that losses would only be deferred for a maximum of 90 days, not rolled indefinitely.

The SEC is now on Karen’s case because of her shady fee structures. They claim she’s perpetually rolled losses through “scheme trades” since November of 2014. By taking an incentive fee each month despite her failure to make new NAV highs, she violated both her agreements and defrauded her investors.

It’s interesting how she did it. Between October and December of 2014, Karen took some heavy losses selling her options. But to keep the incentive fees coming in, she organized a sophisticated options roll at the end of each month. This allowed her to still “realize gains” of 1% every month to take fees from, while pushing unrealized losses out to the next month. Month after month the losses continued to snowball while she continued to collect her fees.

Each month began with a huge realized loss. (The SEC reports that these losses now exceed $50 million dollars.) She offset these accrued losses by selling a ton of in-the-money call options on the S&P 500 E-mini futures due to expire at the end of the month. This injected fresh cash into the fund. Just enough so that she could report a small realized gain to investors. That way she could take fees that month too…

But of course there’s no free lunch in trading. You don’t get gains out of nowhere. When these call options expired, yes she had her cash injection (from the option premium), but she was also left with a futures position (due to assignment) that carried a huge unrealized loss.

Here’s where the loss rolling came in. She needed that futures position to stay open until the next month because if she closed it beforehand, that would realize a loss and cancel out the profits from the calls she sold. That means no incentive fees.

So to cover this futures position, she would simultaneously purchase in-the-money call options expiring the following month on the same day she sold those original in-the-money call options. These calls allowed her to offset any gains or losses the futures incurred at the end of the month until the beginning of the next month.

When the second tranche of options expired at the beginning of the next month, her fund finally realized the huge loss again.

The cycle then repeated.

And on top of all this funny business, the redemption practices of the HI Fund were screwy. Basically, investors could withdraw money from the fund without having to take a hit from these perpetually rolled unrealized losses. So people that got out early would get a windfall, while those slow to act would be left holding an empty bag.

The SEC also claims that Karen did not inform new investors that their investment immediately lost value when entering the fund due to the built up unrealized losses.

This all smells like a classic Ponzi scheme…Pay the old investors with money from the new ones.

But rather than shout from the mountain tops about how Karen is a fraud or how selling options is stupid. I will give her the benefit of the doubt. We’ll let the court systems sort it out after hearing the other side.

Instead let’s focus on the lessons investors and traders can learn from this situation.

Lesson 1:

Don’t fuck up your fund’s disclosure docs. Don’t write in policies that are destined to get scrutinized by the SEC/CFTC. If you want to trade other people’s money, do it correctly.

Lesson 2:

Leverage kills. Now it’s unfair to throw out a blanket statement like “never use leverage.” Leverage can be a wonderful tool if used correctly. We use it all the time. But it must be used safely and responsibly.

A lot of investors abuse leverage because it can create short-term fame and fortune. You can over-lever and put up amazing numbers, attracting a lot of investors. But without fail, an over-levered trading operation will always go under. High leverage is a double-edged sword. It comes with massive upside and massive downside. Over-levering will blow up your fund.

Now when I first read through the SEC complaint, I was confused why Karen would need to run this scheme in the first place. After all… she is a strangle seller/volatility seller in equity indices. Thinking back to the beginning of 2014 I couldn’t remember any market events that would cause a vol seller to hit an unrecoverable drawdown. Volatility sellers should have done very well since the beginning of 2014.

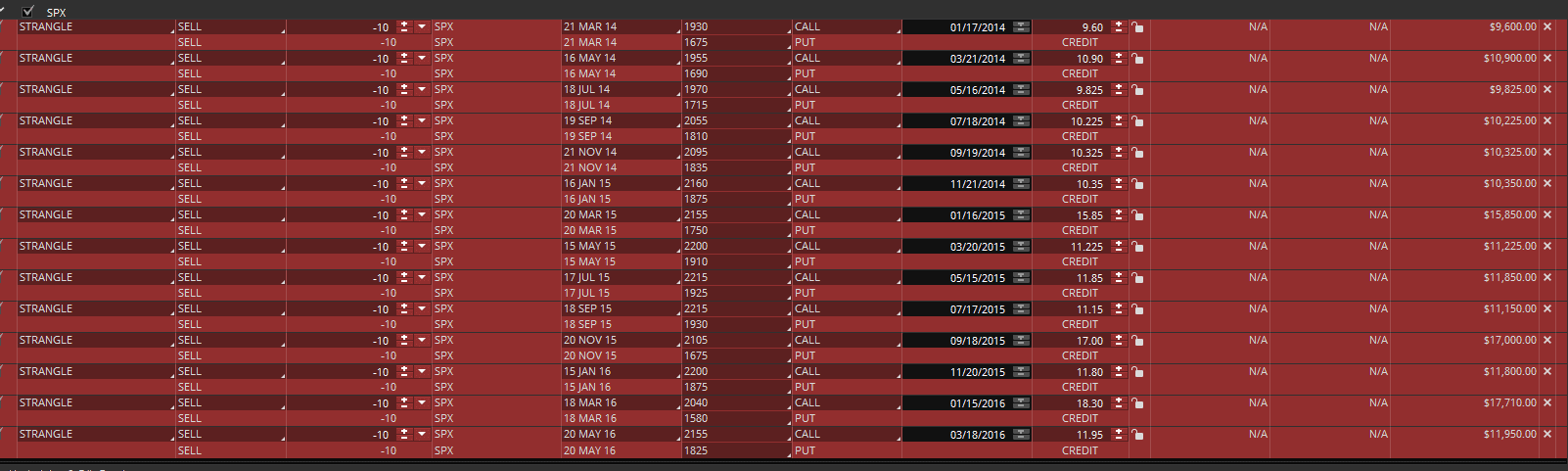

To test this assumption, I ran a very basic backtest of strangle selling in the Thinkorswim platform.

I went back to Jan 2014 and mechanically sold a 10 delta strangle with 60 days to expiration. For position sizing I assumed a $1,000,000 account and sold 1 SPX option per $100,000 of capital.

Here were the results:

You can see in the profit and loss table that there was not a single expiration cycle that ended in a loss.

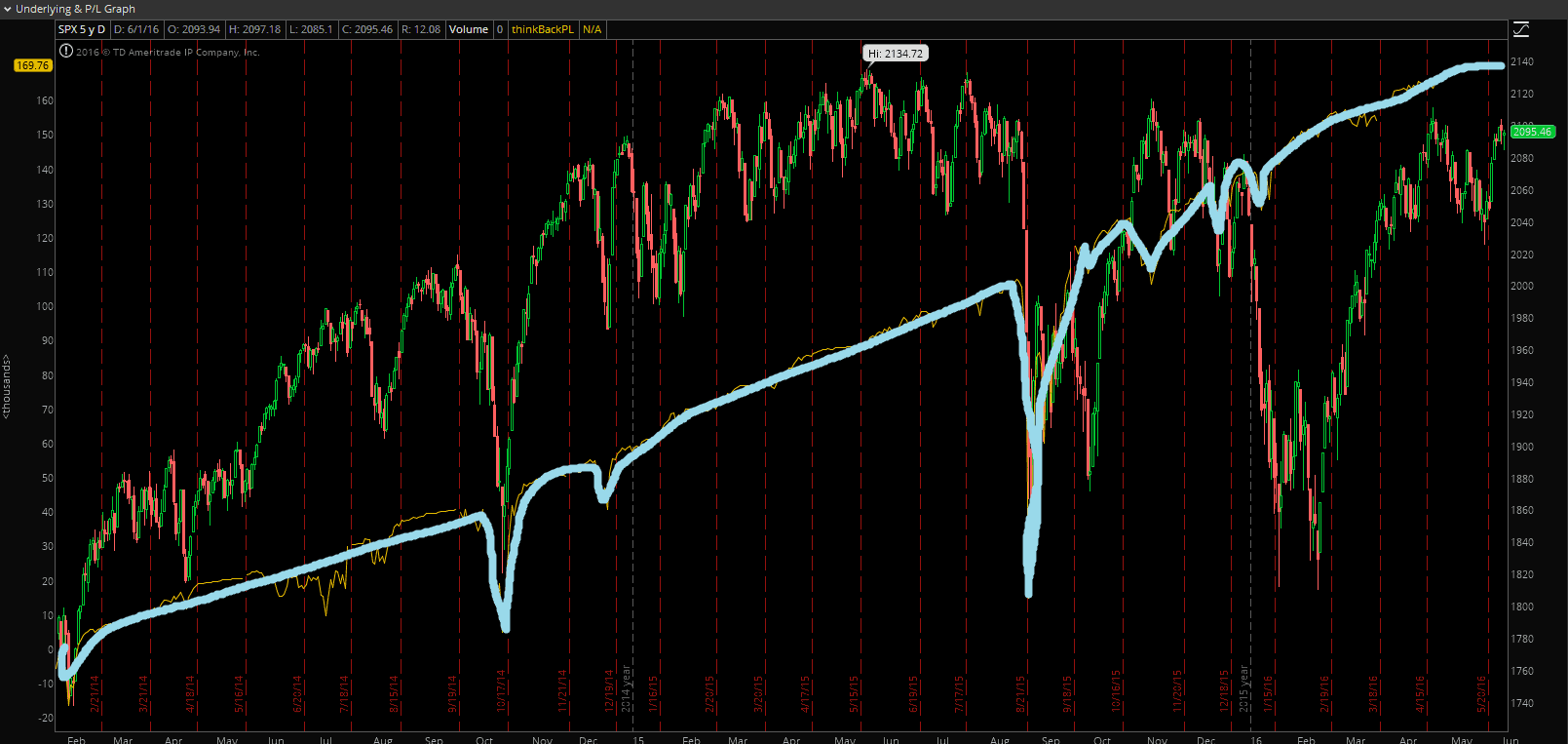

The blue line above shows the strategy’s equity curve versus the SPX. You can see there were some violent drawdowns during the sell off in October 2014 (where Karen allegedly got burnt) and then again in the summer of 2015. But the losses were quickly recovered as volatility contracted and markets continued to range.

By the end of the simulation the net profits were around $170,000. That’s a 17% gain on a million dollar account. On a notional basis the position sizing I used was 2x the cash value of the account. But even with this leverage, the worst drawdown (August 2015 flash crash) was only around 9.5%. That would not end your fund.

Now Karen doesn’t mechanically sell strangles in this fashion, but this example is used to illustrate that even blindly selling strangles with a respectful position size actually worked very well since early 2014.

So how did Karen get caught in a situation where she was left with huge unrealized losses?

The only answer is by using too much leverage. When you get over-levered, whipsaws like the one in 2014 can force you to adjust and tinker your strategy to your detriment. Give the market enough time, and it will exterminate all over-levered players. Especially those using leverage on short gamma strategies like option selling.

The point here is not to dismiss all volatility and option selling strategies as useless and blow up prone. The short volatility trade on equity indices is one of the best trades out there. It does very well long-term.

The key takeaway is that you must get position sizing right if you want to last in this game. Without a deep understanding of how to size positions and how to manage trades once they’re on, you’ll surely die out.

If you want to make sure you’re sizing and managing your options strategy correctly, then check out our options special report by clicking here.